Key Insights

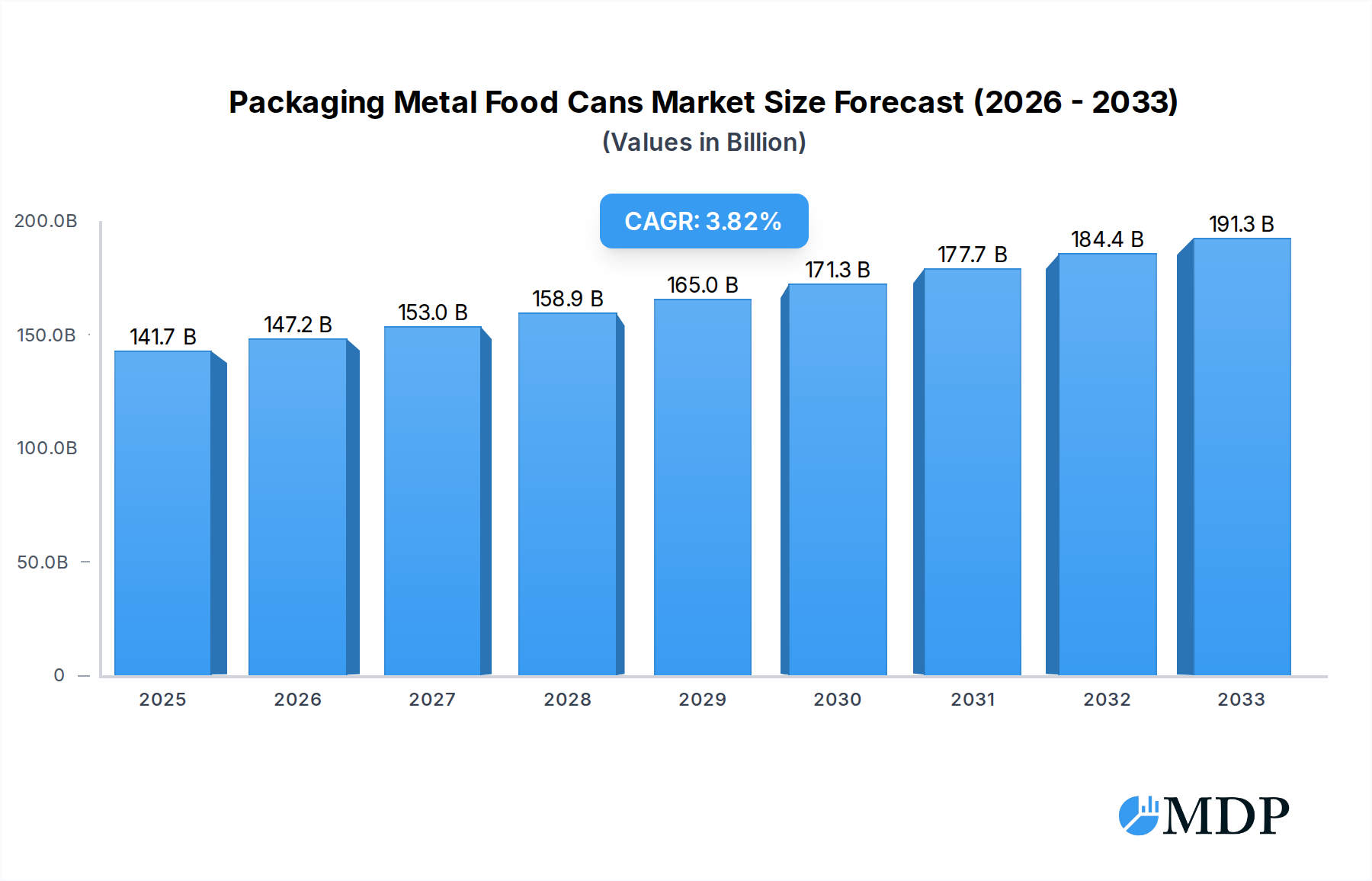

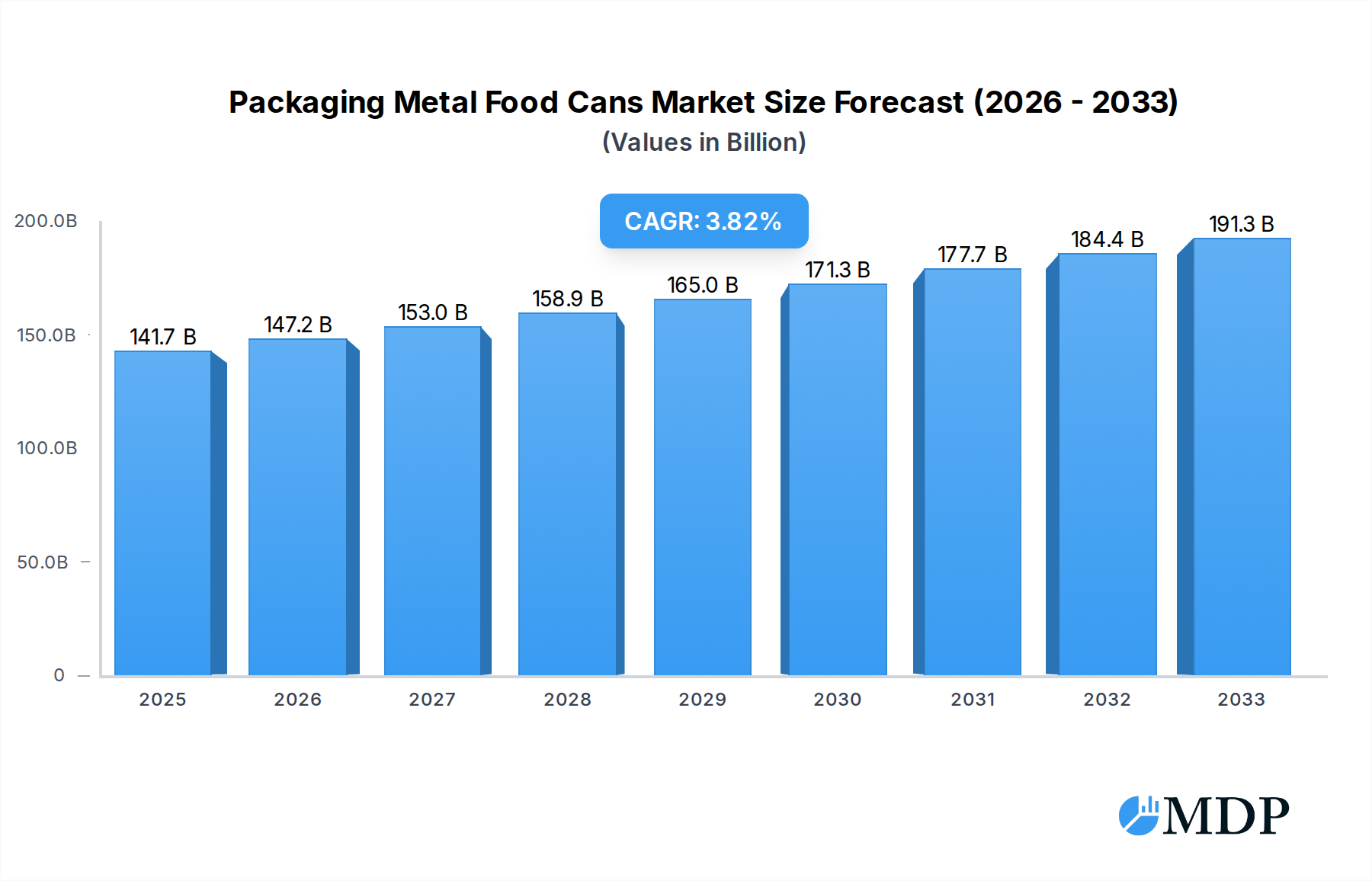

The global market for Metal Food Cans is poised for robust growth, projected to reach an estimated $141.7 billion in 2025. This expansion is fueled by increasing consumer demand for convenient and long-lasting food packaging solutions, coupled with the inherent benefits of metal cans such as their superior barrier properties against light, oxygen, and contaminants, thereby preserving food quality and extending shelf life. The market is expected to witness a Compound Annual Growth Rate (CAGR) of 3.9% during the forecast period of 2025-2033, underscoring its sustained upward trajectory. Key drivers include the growing processed food industry, rising disposable incomes in emerging economies, and the persistent preference for canned goods in preserving seasonal produce. Innovations in can manufacturing, such as lighter weight materials and enhanced recyclability, further contribute to the market's positive outlook, aligning with growing environmental consciousness.

Packaging Metal Food Cans Market Size (In Billion)

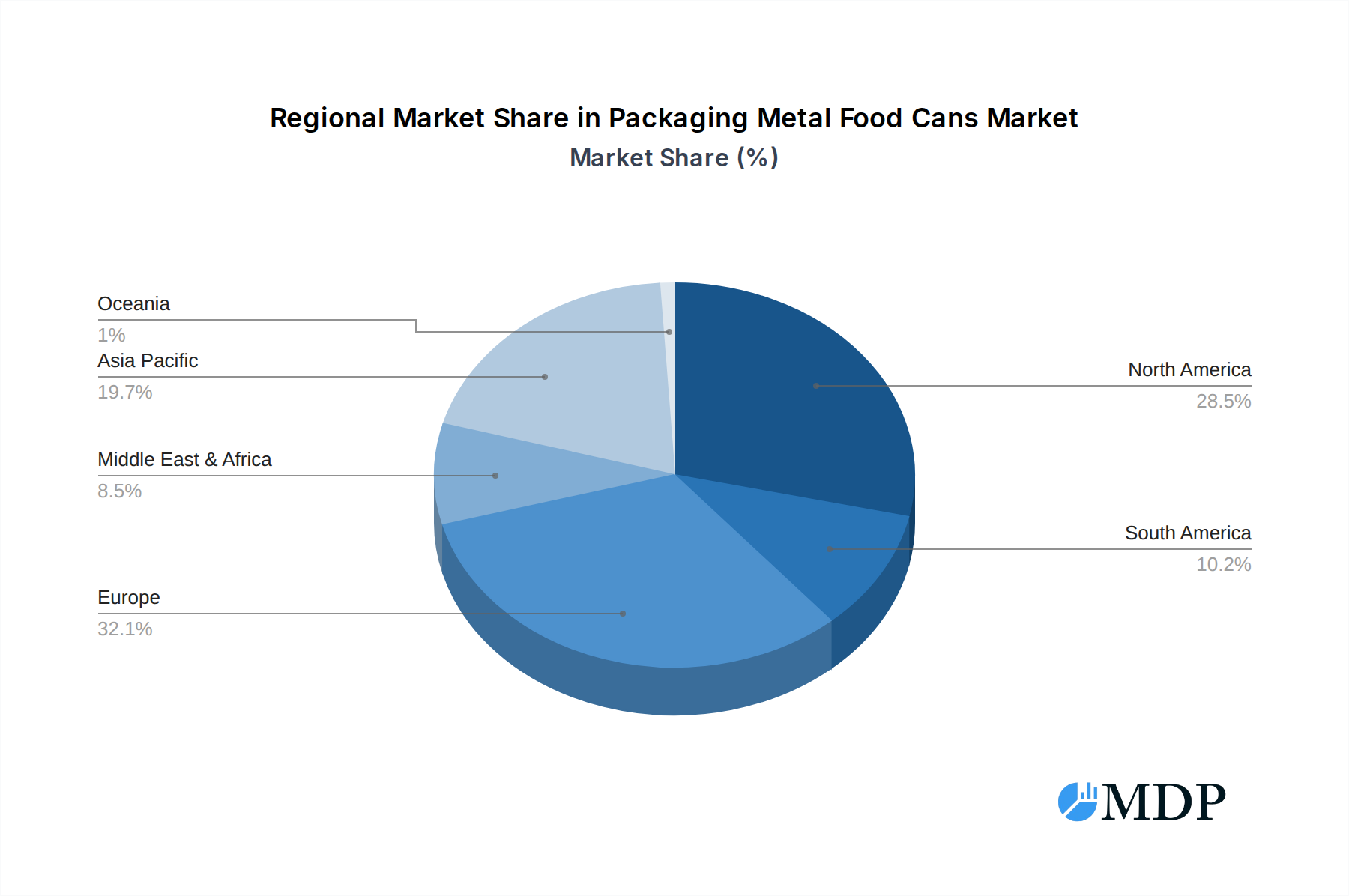

The diverse applications within the Metal Food Cans market highlight its broad reach, with significant contributions from segments like Fruits and Vegetables, Meat and Seafood, and Pet Food. The preference for steel cans remains dominant due to their strength and cost-effectiveness, though aluminum cans are gaining traction, particularly for beverages and certain food items where weight and aesthetic appeal are paramount. Geographically, the Asia Pacific region is expected to be a significant growth engine, driven by rapid industrialization, a burgeoning middle class, and an increasing adoption of packaged foods. North America and Europe continue to represent mature yet substantial markets, characterized by high consumption of convenience foods and a strong emphasis on product quality and safety. Restraints such as fluctuating raw material prices and the emergence of alternative packaging materials are being actively managed through technological advancements and strategic supply chain management by leading companies like Crown Holdings, Silgan Holdings, and Trivium Packaging.

Packaging Metal Food Cans Company Market Share

Unlocking the Billion-Dollar Packaging Metal Food Cans Market: A Comprehensive Industry Report (2019-2033)

Dive deep into the expansive global Packaging Metal Food Cans market, valued in the billions, with this meticulously researched report. Spanning from 2019 to 2033, this analysis provides unparalleled insights for industry stakeholders, investors, and decision-makers. We dissect market dynamics, identify growth trajectories, and spotlight key players shaping the future of food preservation. This report focuses on the critical applications like Fruits and Vegetables, Meat and Seafood, Pet Food, Soup, and Others, analyzing the dominance of Steel and Aluminum can types. Our extensive coverage includes a detailed examination of industry developments, market concentration, leading players, and strategic outlooks, offering actionable intelligence for navigating this dynamic sector.

Packaging Metal Food Cans Market Dynamics & Concentration

The Packaging Metal Food Cans market, a multi-billion dollar industry, exhibits moderate to high concentration, with a significant portion of market share held by leading global manufacturers. Companies such as Crown Holdings, Silgan Holdings, Trivium Packaging, Toyo Seikan, Can Pack Group, Hokkan Holdings, CPMC Holdings, Daiwa Can Company, Kingcan Holdings Limited, and ShengXing Group dominate the landscape through extensive production capacities, robust distribution networks, and strategic acquisitions. Innovation drivers are primarily focused on enhancing can functionality, sustainability, and consumer appeal. This includes advancements in lightweighting technologies, improved barrier properties, and the introduction of easy-open features. Regulatory frameworks, particularly concerning food safety, material recycling, and environmental impact, play a crucial role in shaping manufacturing processes and product development. The availability of product substitutes, such as flexible packaging and glass, poses a constant competitive pressure, necessitating continuous improvement in the cost-effectiveness and performance of metal cans. End-user trends are evolving, with increasing demand for convenient, portion-controlled packaging, and a growing preference for sustainably sourced and recyclable materials. Mergers and acquisitions (M&A) activity remains a key strategy for consolidating market share, expanding geographical reach, and acquiring new technologies. Over the historical period (2019-2024), an estimated 20 significant M&A deals, with an aggregate value exceeding 10 billion, have reshaped the competitive environment.

Packaging Metal Food Cans Industry Trends & Analysis

The global Packaging Metal Food Cans market is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 4.5% during the forecast period (2025-2033). This expansion is fueled by several interconnected market growth drivers. A primary catalyst is the escalating global population, which directly translates into higher demand for preserved food products. The increasing urbanization and the rise of dual-income households also contribute significantly, as consumers seek convenient and ready-to-eat meal solutions, a segment where metal cans excel in maintaining freshness and extending shelf life. Technological disruptions are continuously optimizing the manufacturing process. Innovations in can production, such as advanced coating technologies that improve corrosion resistance and the adoption of high-speed filling and sealing machinery, are enhancing efficiency and reducing operational costs for manufacturers. Furthermore, advancements in material science, including the development of thinner yet stronger steel and aluminum alloys, are contributing to lightweighting efforts, thereby reducing transportation costs and environmental impact. Consumer preferences are also evolving, with a growing awareness and demand for sustainable and recyclable packaging options. Metal cans, particularly those made from aluminum, are highly recyclable, aligning with the global shift towards a circular economy. This trend is further amplified by stringent government regulations promoting recycling and reducing waste. Competitive dynamics within the industry are characterized by intense price competition, a focus on product differentiation through innovative designs and functionalities, and strategic partnerships between can manufacturers and food producers. Market penetration is steadily increasing across various food categories, with canned fruits and vegetables, soups, and pet food representing significant segments. The estimated market penetration for metal food cans in the processed food industry stands at over 75 billion units annually.

Leading Markets & Segments in Packaging Metal Food Cans

The Packaging Metal Food Cans market demonstrates significant regional and segmental variations in its dominance and growth. North America and Europe currently lead in terms of market value, driven by well-established food processing industries, high consumer spending on packaged foods, and robust recycling infrastructure. However, the Asia Pacific region is emerging as the fastest-growing market, propelled by rapid economic development, a burgeoning middle class, and increasing adoption of processed and convenience foods.

Within the Application segment, Fruits and Vegetables consistently represent the largest share, accounting for an estimated 30% of the total market. This dominance is attributed to their widespread consumption, the long shelf-life achievable with metal cans, and their essential role in global food security initiatives. Meat and Seafood also hold a substantial share, estimated at 25%, driven by the demand for preserved protein sources. The Pet Food segment is experiencing particularly strong growth, projected to exceed a 15% market share by 2033, reflecting the humanization of pets and the increasing demand for specialized, high-quality pet nutrition. The Soup segment, while mature, remains a significant contributor, estimated at 20%, while Others, encompassing items like dairy products, edible oils, and ready-to-eat meals, constitute the remaining percentage.

In terms of Type, the market is primarily divided between Steel and Aluminum cans. Steel cans traditionally hold a larger market share due to their cost-effectiveness and strength, particularly for larger can formats and products requiring high structural integrity. However, Aluminum cans are witnessing accelerated growth, estimated to capture over 40% of the market by 2033. This surge is propelled by their lightweight nature, superior corrosion resistance, and higher recyclability rates, aligning with growing consumer and regulatory demands for sustainable packaging. The dominance of specific segments is influenced by various factors:

- Economic Policies: Government incentives for local food processing and manufacturing, coupled with trade agreements, influence regional market dominance.

- Infrastructure: Developed logistics and transportation networks are crucial for the efficient distribution of both raw materials and finished canned goods, particularly supporting the dominance of North America and Europe.

- Consumer Demographics: Aging populations in developed markets, and a growing youth demographic in developing regions, influence the demand for specific canned food categories.

- Food Safety Regulations: Stringent food safety standards, implemented by regulatory bodies, dictate material choices and manufacturing processes, impacting the competitiveness of different can types.

Packaging Metal Food Cans Product Developments

The Packaging Metal Food Cans sector is witnessing a wave of product innovations designed to enhance functionality, sustainability, and consumer appeal. Manufacturers are actively developing lighter-weight cans through advanced alloys and thinner wall designs, significantly reducing material usage and transportation costs. Innovations in interior coatings are improving product shelf-life and preventing metallic taste transfer, a key concern for consumers. Easy-open features, such as pull-tabs and resealable lids, are becoming standard, catering to the demand for convenience. Furthermore, advancements in printing and labeling technologies allow for more vibrant branding and informational content directly on the can, enhancing shelf appeal and consumer engagement. The competitive advantage lies in offering a comprehensive solution that balances cost-effectiveness with superior product protection and an appealing user experience, particularly in the burgeoning plant-based and ready-to-eat meal categories.

Key Drivers of Packaging Metal Food Cans Growth

Several pivotal factors are propelling the growth of the Packaging Metal Food Cans market, estimated to reach billions in value. Technological advancements in manufacturing efficiency and material science are reducing production costs and enhancing product quality. The increasing global population and evolving consumer lifestyles, characterized by a demand for convenience and preserved food solutions, are fundamental drivers. Supportive government regulations promoting food safety and the recyclability of packaging materials further bolster market expansion. The growing preference for sustainable packaging solutions also significantly favors metal cans due to their high recyclability rates.

Challenges in the Packaging Metal Food Cans Market

Despite its growth, the Packaging Metal Food Cans market faces significant hurdles. Intense competition from alternative packaging formats like flexible pouches and cartons poses a constant threat, often offering perceived advantages in terms of weight and perceived sustainability. Volatility in raw material prices, particularly for steel and aluminum, can impact profit margins and pricing strategies, with estimated price fluctuations of up to 20% in a single year. Stringent environmental regulations concerning waste management and the carbon footprint of production can increase operational costs. Furthermore, fluctuating global supply chains and potential geopolitical disruptions can affect the availability and cost of raw materials and finished goods, leading to delays and increased logistical expenses, with supply chain disruptions costing the industry an estimated 5 billion annually.

Emerging Opportunities in Packaging Metal Food Cans

Emerging opportunities in the Packaging Metal Food Cans market are driven by a confluence of technological breakthroughs and evolving market demands. The growing consumer preference for plant-based and health-conscious food products presents a significant avenue for growth, as metal cans effectively preserve the quality and nutritional value of these items. Advancements in the recyclability and circular economy initiatives surrounding metal packaging are creating a more favorable perception, encouraging adoption by environmentally conscious brands. Strategic partnerships between metal can manufacturers and innovative food startups focused on convenience and specialty products offer immense potential. Furthermore, the increasing adoption of smart packaging technologies, such as QR codes for enhanced traceability and consumer engagement, represents a nascent but promising area for innovation and differentiation in the market.

Leading Players in the Packaging Metal Food Cans Sector

- Crown Holdings

- Silgan Holdings

- Trivium Packaging

- Toyo Seikan

- Can Pack Group

- Hokkan Holdings

- CPMC Holdings

- Daiwa Can Company

- Kingcan Holdings Limited

- ShengXing Group

Key Milestones in Packaging Metal Food Cans Industry

- 2019 February: Crown Holdings completes the acquisition of Signode Industrial Group, expanding its global footprint and product portfolio.

- 2020 July: Trivium Packaging is formed through the merger of Ardagh Group's global metal packaging business and Exal.

- 2021 March: Silgan Holdings announces plans to acquire Sonoco's rigid paper and closures business, diversifying its packaging offerings.

- 2022 January: Can Pack Group invests in advanced recycling technologies to enhance the sustainability of its aluminum can production.

- 2023 August: Toyo Seikan announces a new line of lightweight aluminum cans for beverages, targeting enhanced sustainability.

- 2024 April: A significant industry-wide push towards increased recycled content in metal food cans is observed, driven by regulatory pressures.

Strategic Outlook for Packaging Metal Food Cans Market

The strategic outlook for the Packaging Metal Food Cans market is characterized by continued growth and innovation. The focus will remain on enhancing sustainability through increased use of recycled materials and lightweighting technologies, a trend projected to contribute an additional 5 billion in market value. Companies that invest in advanced manufacturing processes and develop differentiated product offerings, particularly those catering to the growing demand for convenient and healthy food options, will be well-positioned. Strategic collaborations with food producers to co-develop packaging solutions for emerging product categories will be crucial. Furthermore, navigating evolving regulatory landscapes and capitalizing on the inherent recyclability of metal will be key to sustained success in this billion-dollar global industry.

Packaging Metal Food Cans Segmentation

-

1. Application

- 1.1. Fruits and Vegetables

- 1.2. Meat and Seafood

- 1.3. Pet Food

- 1.4. Soup

- 1.5. Others

-

2. Type

- 2.1. Steel

- 2.2. Aluminum

- 2.3. Others

Packaging Metal Food Cans Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Packaging Metal Food Cans Regional Market Share

Geographic Coverage of Packaging Metal Food Cans

Packaging Metal Food Cans REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Packaging Metal Food Cans Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Fruits and Vegetables

- 5.1.2. Meat and Seafood

- 5.1.3. Pet Food

- 5.1.4. Soup

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Steel

- 5.2.2. Aluminum

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Packaging Metal Food Cans Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Fruits and Vegetables

- 6.1.2. Meat and Seafood

- 6.1.3. Pet Food

- 6.1.4. Soup

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Steel

- 6.2.2. Aluminum

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Packaging Metal Food Cans Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Fruits and Vegetables

- 7.1.2. Meat and Seafood

- 7.1.3. Pet Food

- 7.1.4. Soup

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Steel

- 7.2.2. Aluminum

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Packaging Metal Food Cans Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Fruits and Vegetables

- 8.1.2. Meat and Seafood

- 8.1.3. Pet Food

- 8.1.4. Soup

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Steel

- 8.2.2. Aluminum

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Packaging Metal Food Cans Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Fruits and Vegetables

- 9.1.2. Meat and Seafood

- 9.1.3. Pet Food

- 9.1.4. Soup

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Steel

- 9.2.2. Aluminum

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Packaging Metal Food Cans Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Fruits and Vegetables

- 10.1.2. Meat and Seafood

- 10.1.3. Pet Food

- 10.1.4. Soup

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Steel

- 10.2.2. Aluminum

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Crown Holdings

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Silgan Holdings

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Trivium Packaging

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Toyo Seikan

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Can Pack Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Hokkan Holdings

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 CPMC Holdings

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Daiwa Can Company

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Kingcan Holdings Limited

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 ShengXing Group

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Crown Holdings

List of Figures

- Figure 1: Global Packaging Metal Food Cans Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Packaging Metal Food Cans Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Packaging Metal Food Cans Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Packaging Metal Food Cans Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Packaging Metal Food Cans Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Packaging Metal Food Cans Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Packaging Metal Food Cans Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Packaging Metal Food Cans Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Packaging Metal Food Cans Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Packaging Metal Food Cans Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Packaging Metal Food Cans Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Packaging Metal Food Cans Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Packaging Metal Food Cans Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Packaging Metal Food Cans Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Packaging Metal Food Cans Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Packaging Metal Food Cans Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Packaging Metal Food Cans Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Packaging Metal Food Cans Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Packaging Metal Food Cans Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Packaging Metal Food Cans Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Packaging Metal Food Cans Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Packaging Metal Food Cans Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Packaging Metal Food Cans Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Packaging Metal Food Cans Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Packaging Metal Food Cans Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Packaging Metal Food Cans Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Packaging Metal Food Cans Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Packaging Metal Food Cans Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Packaging Metal Food Cans Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Packaging Metal Food Cans Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Packaging Metal Food Cans Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Packaging Metal Food Cans Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Packaging Metal Food Cans Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Packaging Metal Food Cans Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Packaging Metal Food Cans Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Packaging Metal Food Cans Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Packaging Metal Food Cans Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Packaging Metal Food Cans Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Packaging Metal Food Cans Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Packaging Metal Food Cans Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Packaging Metal Food Cans Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Packaging Metal Food Cans Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Packaging Metal Food Cans Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Packaging Metal Food Cans Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Packaging Metal Food Cans Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Packaging Metal Food Cans Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Packaging Metal Food Cans Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Packaging Metal Food Cans Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Packaging Metal Food Cans Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Packaging Metal Food Cans Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Packaging Metal Food Cans?

The projected CAGR is approximately 3.9%.

2. Which companies are prominent players in the Packaging Metal Food Cans?

Key companies in the market include Crown Holdings, Silgan Holdings, Trivium Packaging, Toyo Seikan, Can Pack Group, Hokkan Holdings, CPMC Holdings, Daiwa Can Company, Kingcan Holdings Limited, ShengXing Group.

3. What are the main segments of the Packaging Metal Food Cans?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Packaging Metal Food Cans," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Packaging Metal Food Cans report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Packaging Metal Food Cans?

To stay informed about further developments, trends, and reports in the Packaging Metal Food Cans, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence