Key Insights

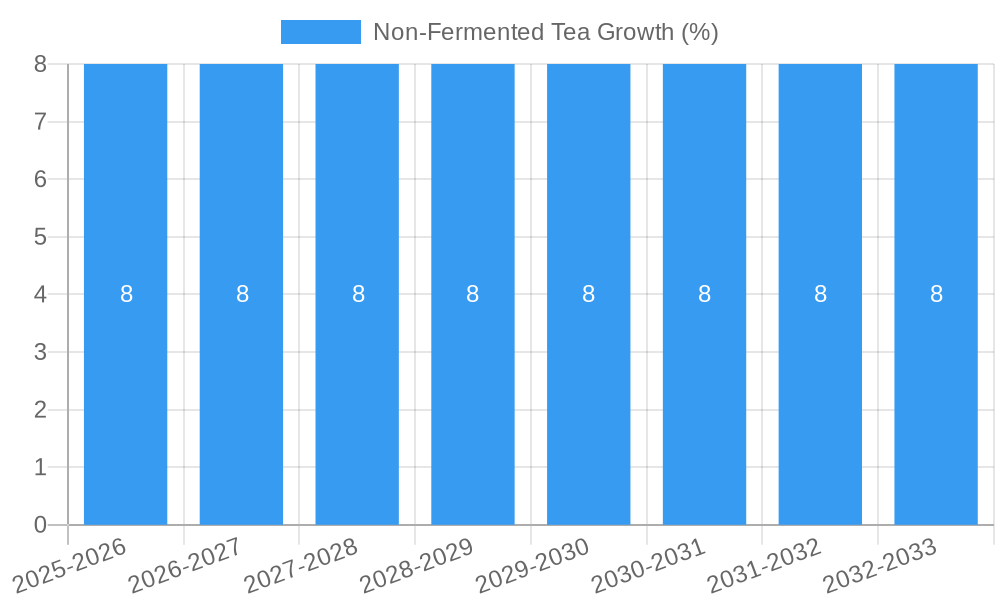

The global Non-Fermented Tea market is poised for significant expansion, projected to reach an estimated market size of USD XXX million by 2025, with a robust Compound Annual Growth Rate (CAGR) of XX% during the study period of 2019-2033. This growth is primarily fueled by a growing consumer preference for healthier beverage options, driven by the perceived health benefits associated with non-fermented teas such as green tea and white tea. The increasing awareness of antioxidants and other beneficial compounds found in these teas, coupled with their role in promoting overall well-being, is a major catalyst. Furthermore, the rising disposable incomes in emerging economies, particularly in the Asia Pacific region, are enabling greater access to premium tea products, thereby contributing to market expansion. The diverse applications of non-fermented teas, spanning beverages, pharmaceuticals, and cosmetics, also offer broad avenues for market penetration and innovation.

Several key trends are shaping the non-fermented tea landscape. The surge in demand for specialty and artisanal teas, including varieties like Huangshan Maofeng and Longjing, underscores a consumer desire for unique flavors and high-quality products. The premiumization of the tea market, with consumers willing to pay more for ethically sourced and sustainably produced teas, is another significant driver. Innovations in packaging and product formats, such as ready-to-drink (RTD) non-fermented teas and tea-infused products, are enhancing convenience and accessibility, appealing to a wider demographic. However, the market faces certain restraints, including price volatility of raw materials and intense competition from other beverage categories, including fermented teas and functional drinks. Nonetheless, the overarching trend towards health consciousness and the sustained interest in natural products provide a strong foundation for continued growth and development within the non-fermented tea sector.

Unlocking the Green Gold: A Comprehensive Report on the Global Non-Fermented Tea Market (2019-2033)

Dive deep into the flourishing world of non-fermented teas with this in-depth market analysis. Explore market dynamics, emerging trends, leading players, and strategic opportunities shaping the future of this billion-dollar industry. This report is an essential resource for beverage manufacturers, pharmaceutical companies, cosmetic brands, and tea connoisseurs seeking to capitalize on the surging demand for premium, natural, and health-conscious tea products.

This comprehensive report provides an unparalleled view of the non-fermented tea market, projecting its trajectory from 2019 through 2033. Leveraging a robust analytical framework, it dissects market concentration, identifies innovation drivers, analyzes regulatory landscapes, and pinpoints the impact of product substitutes and evolving end-user preferences. The study encompasses a rigorous examination of mergers and acquisitions (M&A) activities, revealing key consolidations and strategic alliances that have shaped the competitive arena. With an estimated market size of over $XX billion, the non-fermented tea sector is poised for significant expansion, driven by a growing awareness of health benefits and a global palate increasingly drawn to sophisticated, natural beverages. Our analysis, based on a study period from 2019 to 2033, with a base year of 2025, offers actionable insights for stakeholders to navigate this dynamic market landscape.

Non-Fermented Tea Market Dynamics & Concentration

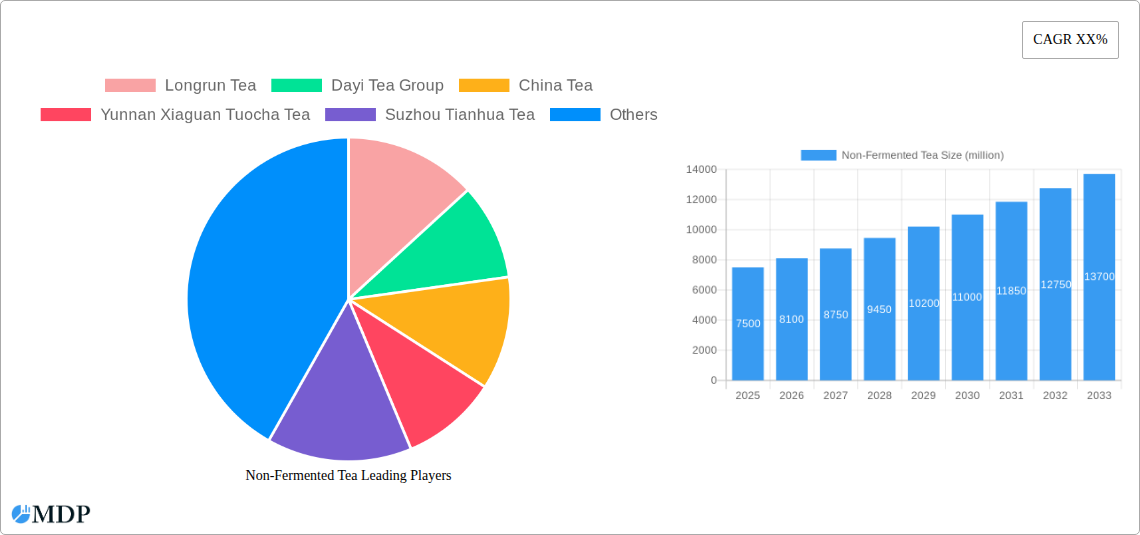

The global non-fermented tea market exhibits a moderate level of concentration, with a few dominant players holding significant market share, estimated at over 40% collectively. However, a robust ecosystem of regional and specialized producers ensures a competitive environment. Innovation is a key driver, fueled by advancements in processing techniques, the development of novel flavor profiles, and the integration of functional ingredients. Regulatory frameworks, particularly concerning food safety, organic certification, and international trade, play a crucial role in shaping market access and product development. Product substitutes, such as other beverages and functional drinks, present a constant challenge, necessitating continuous differentiation through quality, branding, and perceived health benefits. End-user trends lean heavily towards wellness-oriented consumption, with consumers actively seeking teas with purported health advantages. M&A activities have been steady, with an estimated XX deals in the historical period (2019-2024), primarily focused on consolidating market share, acquiring new technologies, and expanding geographical reach. For instance, strategic acquisitions have been instrumental in bolstering the portfolios of major companies, ensuring a broader offering to meet diverse consumer demands.

Non-Fermented Tea Industry Trends & Analysis

The non-fermented tea industry is experiencing robust growth, driven by a confluence of factors. The increasing global awareness of the health benefits associated with non-fermented teas, such as their antioxidant properties and potential to aid digestion, is a primary growth catalyst. This has led to a significant rise in consumer demand for premium, high-quality green teas, white teas, and oolong teas. Technological disruptions are continuously reshaping the industry, with innovations in cultivation, harvesting, processing, and packaging enhancing product quality, shelf life, and sustainability. Automated harvesting and advanced drying techniques, for example, are optimizing production efficiency and preserving the delicate flavors and nutrients of these teas. Consumer preferences are evolving, with a growing demand for single-origin teas, artisanal blends, and teas with specific functional attributes like stress relief or immune support. The "natural" and "organic" labeling is becoming increasingly important, influencing purchasing decisions across developed and developing markets. Competitive dynamics are intensifying, with both established global brands and agile niche players vying for market share. Strategic partnerships and collaborations are becoming more prevalent as companies seek to expand their product offerings and distribution networks. The market penetration of non-fermented teas is projected to reach over XX% by 2025, with a Compound Annual Growth Rate (CAGR) estimated at approximately XX% during the forecast period (2025–2033). This growth is underpinned by expanding distribution channels, including online retail and direct-to-consumer models, making these teas more accessible to a wider audience. The overall market size is projected to exceed $XX billion by 2033, a testament to the sustained consumer interest and industry innovation.

Leading Markets & Segments in Non-Fermented Tea

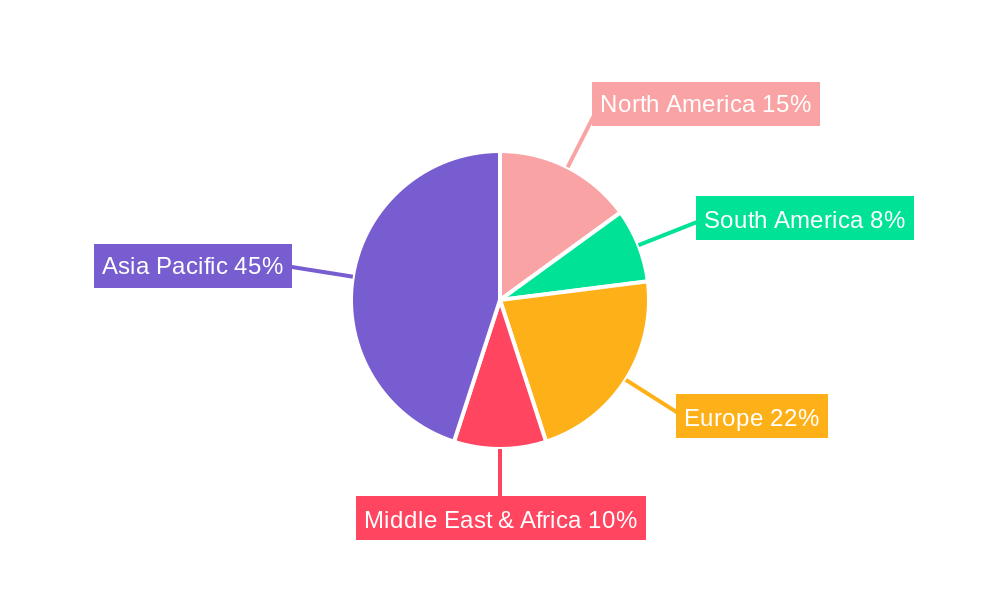

The Beverages application segment is the undisputed leader in the non-fermented tea market, accounting for an estimated XX% of the global market share. This dominance is driven by the widespread consumption of tea as a daily beverage across diverse cultures and demographics. Within the beverage segment, chilled ready-to-drink (RTD) non-fermented teas are experiencing particularly rapid growth, fueled by convenience and on-the-go consumption trends. The Huangshan Maofeng type of non-fermented tea is a significant contributor to this segment's success, renowned for its delicate aroma and complex flavor profile, appealing to connoisseurs and everyday tea drinkers alike. Asia-Pacific, particularly China, remains the largest regional market for non-fermented teas, owing to its deep-rooted tea culture and significant domestic production. Economic policies in these regions, such as government support for agricultural development and export promotion, further bolster market growth. Infrastructure development, including enhanced logistics and cold chain facilities, is crucial for ensuring the efficient distribution of perishable tea products.

Beverages Application Dominance:

- Consumer Habit: Tea is a staple beverage globally, with increasing preference for healthier, natural alternatives.

- RTD Growth: The ready-to-drink segment is expanding due to convenience and busy lifestyles.

- Health & Wellness Trend: Consumers are actively seeking teas for their perceived health benefits.

- Premiumization: Demand for high-quality, single-origin, and artisanal teas is on the rise.

Type Dominance (Huangshan Maofeng):

- Cultural Significance: Deeply embedded in Chinese tea culture, with a long history of appreciation.

- Sensory Appeal: Distinctive aroma and nuanced flavor profile attract a broad consumer base.

- Perceived Quality: Often associated with superior quality and traditional craftsmanship.

- Growing International Acclaim: Increasing recognition and demand in Western markets.

The Pharmaceuticals and Cosmetics segments, while smaller, are demonstrating significant growth potential. In pharmaceuticals, non-fermented teas are being explored for their therapeutic properties, leading to the development of novel functional ingredients and health supplements. The cosmetic industry is leveraging the antioxidant and anti-inflammatory properties of these teas in skincare and beauty products. The market penetration in these segments is expected to increase as scientific research further validates the benefits of non-fermented tea extracts.

Non-Fermented Tea Product Developments

Product innovations in the non-fermented tea market are primarily focused on enhancing health benefits and catering to evolving consumer tastes. Companies are developing fortified non-fermented teas with added vitamins, minerals, and probiotics to boost their wellness appeal. The exploration of novel flavor infusions, combining traditional teas with fruits, herbs, and spices, is creating exciting new product lines. Advances in extraction and encapsulation technologies are enabling the incorporation of concentrated tea compounds into functional foods, beverages, and topical applications, offering distinct competitive advantages in niche markets. The emphasis on sustainable sourcing and eco-friendly packaging further enhances product desirability.

Key Drivers of Non-Fermented Tea Growth

The non-fermented tea market's growth is propelled by several key drivers. The escalating global demand for natural and healthy beverages is paramount, driven by increasing consumer awareness of the health benefits associated with green, white, and oolong teas, such as their antioxidant and metabolic support properties. Technological advancements in cultivation, processing, and packaging are improving quality, extending shelf life, and enhancing sustainability, making these teas more accessible and appealing. Favorable regulatory landscapes in many regions, supporting organic certifications and fair trade practices, are also contributing to market expansion. Furthermore, innovative marketing strategies and the growing popularity of tea tourism are creating new avenues for consumer engagement and market penetration.

Challenges in the Non-Fermented Tea Market

Despite its robust growth, the non-fermented tea market faces several challenges. Fluctuations in raw material prices due to climate change and geopolitical factors can impact profitability. Stringent and varying international food safety regulations across different countries can create trade barriers and necessitate extensive compliance efforts. Intense competition from both established brands and emerging players, coupled with the threat of substitute products like coffee and other beverages, requires continuous innovation and differentiation. Supply chain disruptions, particularly for specialty or single-origin teas, can affect availability and pricing.

Emerging Opportunities in Non-Fermented Tea

Emerging opportunities in the non-fermented tea market are abundant, driven by innovation and evolving consumer demands. The functional beverage trend presents a significant avenue for growth, with opportunities to develop teas specifically formulated for immunity boosting, stress relief, or enhanced cognitive function. Strategic partnerships with pharmaceutical and nutraceutical companies can unlock new applications for tea extracts in health supplements and medicinal products. The burgeoning e-commerce landscape offers direct-to-consumer channels, enabling brands to reach a wider global audience and build stronger customer relationships. Furthermore, the growing interest in sustainable and ethically sourced products creates opportunities for brands that prioritize environmental responsibility and fair labor practices.

Leading Players in the Non-Fermented Tea Sector

- Longrun Tea

- Dayi Tea Group

- China Tea

- Yunnan Xiaguan Tuocha Tea

- Suzhou Tianhua Tea

- Hunan Spark Tea

- Tazo

- Bigelow

- Yabukita

- Ito En

Key Milestones in Non-Fermented Tea Industry

- 2019: Increased investment in research and development for functional tea benefits.

- 2020: Surge in online sales of specialty non-fermented teas, driven by global lockdowns.

- 2021: Growing consumer demand for organic and ethically sourced non-fermented tea certifications.

- 2022: Innovations in sustainable packaging solutions for non-fermented tea products.

- 2023: Expansion of ready-to-drink (RTD) non-fermented tea options in convenience stores.

- 2024: Emerging market entries for premium non-fermented tea brands in Europe and North America.

- 2025 (Estimated): Continued growth in the functional beverage segment, with non-fermented teas playing a key role.

Strategic Outlook for Non-Fermented Tea Market

The strategic outlook for the non-fermented tea market is exceptionally positive, characterized by sustained growth and evolving consumer preferences. Key growth accelerators include the expanding functional beverage market, where non-fermented teas are poised to play a significant role due to their inherent health benefits. Strategic investments in product innovation, focusing on unique flavor profiles, fortified options, and convenient formats like RTD teas, will be crucial. Furthermore, companies that prioritize sustainability and transparent sourcing will resonate strongly with conscious consumers, building brand loyalty and market differentiation. Exploring emerging markets and leveraging digital channels for direct-to-consumer engagement will further amplify reach and market penetration.

Non-Fermented Tea Segmentation

-

1. Application

- 1.1. Beverages

- 1.2. Pharmaceuticals

- 1.3. Cosmetics

- 1.4. Others

-

2. Types

- 2.1. Huangshan Maofeng

- 2.2. Longjing

- 2.3. Others

Non-Fermented Tea Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Non-Fermented Tea REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Non-Fermented Tea Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Beverages

- 5.1.2. Pharmaceuticals

- 5.1.3. Cosmetics

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Huangshan Maofeng

- 5.2.2. Longjing

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Non-Fermented Tea Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Beverages

- 6.1.2. Pharmaceuticals

- 6.1.3. Cosmetics

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Huangshan Maofeng

- 6.2.2. Longjing

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Non-Fermented Tea Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Beverages

- 7.1.2. Pharmaceuticals

- 7.1.3. Cosmetics

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Huangshan Maofeng

- 7.2.2. Longjing

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Non-Fermented Tea Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Beverages

- 8.1.2. Pharmaceuticals

- 8.1.3. Cosmetics

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Huangshan Maofeng

- 8.2.2. Longjing

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Non-Fermented Tea Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Beverages

- 9.1.2. Pharmaceuticals

- 9.1.3. Cosmetics

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Huangshan Maofeng

- 9.2.2. Longjing

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Non-Fermented Tea Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Beverages

- 10.1.2. Pharmaceuticals

- 10.1.3. Cosmetics

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Huangshan Maofeng

- 10.2.2. Longjing

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Longrun Tea

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Dayi Tea Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 China Tea

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Yunnan Xiaguan Tuocha Tea

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Suzhou Tianhua Tea

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Hunan Spark Tea

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Tazo

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Bigelow

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Yabukita

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Ito En

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Longrun Tea

List of Figures

- Figure 1: Global Non-Fermented Tea Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Non-Fermented Tea Revenue (million), by Application 2024 & 2032

- Figure 3: North America Non-Fermented Tea Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Non-Fermented Tea Revenue (million), by Types 2024 & 2032

- Figure 5: North America Non-Fermented Tea Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Non-Fermented Tea Revenue (million), by Country 2024 & 2032

- Figure 7: North America Non-Fermented Tea Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Non-Fermented Tea Revenue (million), by Application 2024 & 2032

- Figure 9: South America Non-Fermented Tea Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Non-Fermented Tea Revenue (million), by Types 2024 & 2032

- Figure 11: South America Non-Fermented Tea Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Non-Fermented Tea Revenue (million), by Country 2024 & 2032

- Figure 13: South America Non-Fermented Tea Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Non-Fermented Tea Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Non-Fermented Tea Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Non-Fermented Tea Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Non-Fermented Tea Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Non-Fermented Tea Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Non-Fermented Tea Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Non-Fermented Tea Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Non-Fermented Tea Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Non-Fermented Tea Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Non-Fermented Tea Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Non-Fermented Tea Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Non-Fermented Tea Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Non-Fermented Tea Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Non-Fermented Tea Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Non-Fermented Tea Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Non-Fermented Tea Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Non-Fermented Tea Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Non-Fermented Tea Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Non-Fermented Tea Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Non-Fermented Tea Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Non-Fermented Tea Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Non-Fermented Tea Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Non-Fermented Tea Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Non-Fermented Tea Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Non-Fermented Tea Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Non-Fermented Tea Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Non-Fermented Tea Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Non-Fermented Tea Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Non-Fermented Tea Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Non-Fermented Tea Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Non-Fermented Tea Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Non-Fermented Tea Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Non-Fermented Tea Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Non-Fermented Tea Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Non-Fermented Tea Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Non-Fermented Tea Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Non-Fermented Tea Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Non-Fermented Tea Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Non-Fermented Tea?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Non-Fermented Tea?

Key companies in the market include Longrun Tea, Dayi Tea Group, China Tea, Yunnan Xiaguan Tuocha Tea, Suzhou Tianhua Tea, Hunan Spark Tea, Tazo, Bigelow, Yabukita, Ito En.

3. What are the main segments of the Non-Fermented Tea?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Non-Fermented Tea," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Non-Fermented Tea report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Non-Fermented Tea?

To stay informed about further developments, trends, and reports in the Non-Fermented Tea, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence