Key Insights

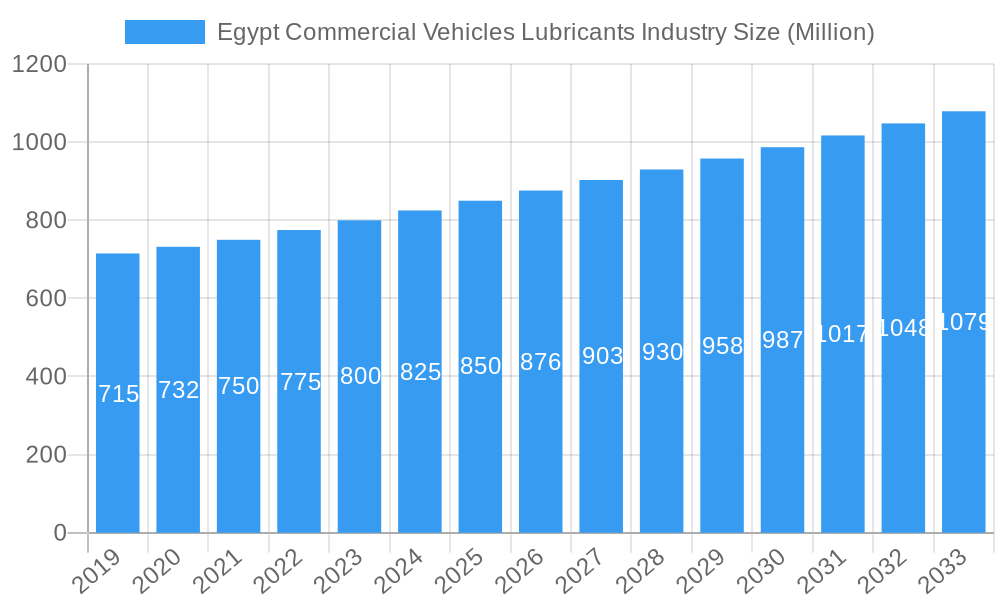

The Egyptian Commercial Vehicles Lubricants Market is poised for significant expansion, projected to reach $1.5 billion by 2024, with a Compound Annual Growth Rate (CAGR) of 2.3% expected through 2033. This growth is propelled by a thriving logistics and transportation sector, fueled by escalating trade and e-commerce, which demands an expanding commercial fleet. Government investments in infrastructure modernization and industrial development further stimulate the need for high-performance lubricants essential for the efficient operation of heavy-duty engines, transmissions, and hydraulic systems. The adoption of advanced engine technologies and stringent emission standards also drives demand for sophisticated, premium lubricants, presenting substantial opportunities for manufacturers. Additionally, the burgeoning construction industry and agricultural mechanization consistently contribute to the demand for specialized commercial vehicle lubricants.

Egypt Commercial Vehicles Lubricants Industry Market Size (In Billion)

Despite this positive trajectory, the market faces challenges, including volatility in crude oil prices, a key input for lubricant production, impacting manufacturing costs and pricing. The presence of a considerable unorganized sector offering lower-priced, often lower-quality lubricants, presents competition to established brands. Nevertheless, increasing awareness among fleet operators concerning the long-term advantages of high-quality lubricants—such as reduced maintenance, enhanced fuel efficiency, and extended vehicle life—is progressively steering market preference towards premium offerings. Key product segments include engine oils, greases, hydraulic fluids, and transmission & gear oils, with demand influenced by the operational requirements of diverse commercial vehicles. Leading companies such as Shell, ExxonMobil, and BP (Castrol) are active participants, competing through product innovation, distribution, and strategic alliances to secure market share.

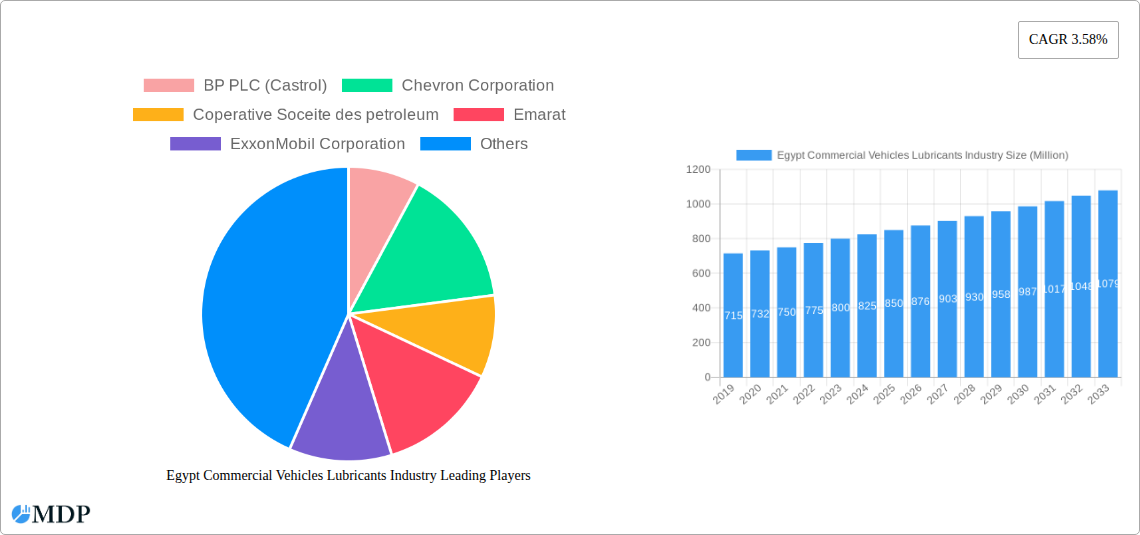

Egypt Commercial Vehicles Lubricants Industry Company Market Share

Unlocking the Potential: Egypt Commercial Vehicles Lubricants Industry Market Analysis and Forecast (2019–2033)

Gain unparalleled insights into the dynamic Egyptian Commercial Vehicles Lubricants industry. This comprehensive report delves into market dynamics, emerging trends, competitive landscapes, and future opportunities. Discover key drivers, challenges, and strategic outlooks for stakeholders navigating the evolving Egyptian market. With data spanning from 2019 to 2033, including base year (2025) and forecast periods, this report is your definitive guide to capitalizing on the projected growth of this vital sector. We cover product types like Engine Oils, Greases, Hydraulic Fluids, and Transmission & Gear Oils, with detailed analysis of leading players such as BP PLC (Castrol), Chevron Corporation, and Royal Dutch Shell PLC.

Egypt Commercial Vehicles Lubricants Industry Market Dynamics & Concentration

The Egyptian commercial vehicles lubricants market is characterized by a moderate level of concentration, with a few major international players dominating the landscape, alongside significant local manufacturers. Key companies like BP PLC (Castrol), Chevron Corporation, ExxonMobil Corporation, Royal Dutch Shell PLC, and TotalEnergies hold substantial market share, leveraging their global brand recognition, extensive distribution networks, and advanced product technologies. The market is driven by increasing demand from the logistics, construction, and transportation sectors, which are expanding due to ongoing infrastructure development and economic growth initiatives in Egypt. Innovation plays a crucial role, with lubricant manufacturers continuously introducing advanced formulations to meet the evolving needs of modern commercial vehicles, focusing on enhanced fuel efficiency, extended drain intervals, and reduced emissions. Regulatory frameworks, primarily overseen by the Egyptian Ministry of Petroleum and Mineral Resources, focus on product quality standards and environmental compliance. The threat of product substitutes, such as alternative fuels or lubricants derived from different base stocks, remains a consideration, though the essential role of lubricants in vehicle maintenance limits their impact. End-user trends are shifting towards higher-performance, longer-lasting lubricants that contribute to operational cost savings. Mergers and acquisitions (M&A) activity, while not consistently high, can be strategic for market consolidation and expansion, with an estimated xx M&A deals observed in the historical period.

Egypt Commercial Vehicles Lubricants Industry Industry Trends & Analysis

The Egyptian commercial vehicles lubricants industry is poised for significant growth, propelled by a confluence of robust economic factors and evolving technological landscapes. The expanding logistics and transportation sectors, driven by Egypt's strategic geographical location and increasing trade volumes, are the primary engines of demand for commercial vehicle lubricants. Government investments in infrastructure, including new road networks and port expansions, further stimulate the commercial vehicle fleet size, directly translating into higher lubricant consumption. The forecast period, particularly from 2025 to 2033, anticipates a Compound Annual Growth Rate (CAGR) of approximately xx%, reflecting sustained economic momentum and industrial activity. Market penetration for advanced lubricants is steadily increasing as fleet operators recognize the long-term economic benefits of superior lubrication, such as reduced maintenance costs, improved fuel efficiency, and extended engine life. Technological disruptions are primarily centered around the development of synthetic and semi-synthetic lubricants that offer enhanced performance under extreme operating conditions and contribute to lower emissions. While the current market is dominated by internal combustion engine (ICE) vehicles, the nascent development of electric commercial vehicles in Egypt presents a future trend to monitor, necessitating the development of specialized e-fluids, as indicated by industry developments. Consumer preferences are increasingly leaning towards lubricants that offer greater value through extended drain intervals and improved vehicle protection, pushing manufacturers to innovate. Competitive dynamics remain intense, with global players vying for market share against established local brands. The industry is also witnessing a growing emphasis on sustainability, with a demand for environmentally friendly lubricant formulations.

Leading Markets & Segments in Egypt Commercial Vehicles Lubricants Industry

Within the Egyptian commercial vehicles lubricants industry, Engine Oils stand out as the dominant segment, accounting for an estimated xx% of the total market value. This dominance is directly attributable to the sheer volume of internal combustion engine (ICE) commercial vehicles operating across Egypt. The robust logistics, construction, and public transportation sectors, all heavily reliant on a vast fleet of trucks, buses, and heavy-duty vehicles, necessitate continuous and substantial consumption of engine oils for optimal performance and longevity.

- Engine Oils: This segment's leadership is bolstered by government initiatives focused on modernizing the transportation infrastructure, leading to an increased number of new commercial vehicle registrations and a greater demand for high-quality engine lubricants that comply with stringent emission standards and fuel efficiency requirements. The ongoing economic development and trade activities further amplify the need for reliable engine operation, making engine oils the cornerstone of the lubricants market.

Transmission & Gear Oils represent the second-largest segment, holding an estimated xx% market share. The demanding operational environments and heavy loads experienced by commercial vehicles place significant stress on their transmission and gear systems, necessitating specialized lubricants for smooth operation and wear protection. The continuous operation of long-haul trucks and heavy machinery in sectors like mining and construction drives consistent demand for these products.

- Transmission & Gear Oils: Factors contributing to this segment's strength include the increasing complexity of modern transmission systems, which require highly specialized lubricants to ensure optimal performance and efficiency. The emphasis on extending vehicle lifespan and reducing maintenance downtime also fuels the demand for high-performance transmission and gear oils.

Hydraulic Fluids constitute a significant portion of the market, estimated at xx%. This segment is driven by the extensive use of hydraulic systems in construction equipment, agricultural machinery, and material handling vehicles, all of which are integral to Egypt's economic activities and infrastructure development projects.

- Hydraulic Fluids: The growth in infrastructure projects, agricultural modernization, and industrial manufacturing directly translates into a higher demand for hydraulic fluids. These fluids are critical for the operation of essential equipment, making this segment a consistent contributor to the overall market.

Greases hold the smallest, yet still vital, share of the market, estimated at xx%. Greases are essential for lubricating components that experience slow speeds, heavy loads, and require long-lasting lubrication, such as bearings, chassis points, and universal joints in commercial vehicles.

- Greases: While a smaller segment by volume, greases are critical for ensuring the proper functioning and longevity of various moving parts in commercial vehicles. The maintenance and repair sector, alongside the ongoing operation of existing fleets, ensures a steady demand for these specialized lubricants.

Egypt Commercial Vehicles Lubricants Industry Product Developments

The Egyptian commercial vehicles lubricants industry is witnessing a surge in product innovation aimed at enhancing performance, extending vehicle life, and meeting evolving environmental regulations. A key trend is the development of advanced synthetic and semi-synthetic engine oils that offer superior protection against wear, improved fuel economy, and extended drain intervals, crucial for cost-conscious fleet operators. Furthermore, the industry is responding to the global shift towards electrification with the introduction of specialized e-fluids, as exemplified by Castrol's ON range designed for electric vehicles, featuring e-gear oils, e-coolants, and e-greases. This proactive development caters to future market needs and positions companies for the transition to electric commercial mobility.

Key Drivers of Egypt Commercial Vehicles Lubricants Industry Growth

The growth of the Egyptian commercial vehicles lubricants industry is propelled by several key factors. Robust economic expansion and significant government investment in infrastructure projects are directly increasing the number of commercial vehicles on the road, thus boosting lubricant demand. The growing logistics and transportation sectors, crucial for trade and commerce, necessitate reliable fleet operations supported by high-quality lubricants. Technological advancements in lubricant formulations, focusing on enhanced fuel efficiency and extended drain intervals, are appealing to fleet operators seeking cost savings and operational efficiency. Furthermore, stricter emission standards are driving the adoption of advanced, cleaner-burning lubricants.

Challenges in the Egypt Commercial Vehicles Lubricants Industry Market

Despite the positive outlook, the Egyptian commercial vehicles lubricants market faces several challenges. Intense price competition, particularly from unbranded or lower-quality products, can pressure margins for premium lubricant manufacturers. Fluctuations in crude oil prices, the primary feedstock for lubricant production, introduce volatility in raw material costs. The informal sector's distribution of lubricants can also pose a challenge to established players. Additionally, navigating evolving regulatory frameworks and ensuring consistent supply chain efficiency across a diverse geographical landscape require continuous strategic attention and investment.

Emerging Opportunities in Egypt Commercial Vehicles Lubricants Industry

The Egyptian commercial vehicles lubricants market is ripe with emerging opportunities. The burgeoning e-commerce sector is fueling demand for last-mile delivery vehicles, creating a growing need for specialized lubricants. The ongoing infrastructure development projects, including highways and urban expansion, will continue to increase the operational hours and demand for lubricants in construction and heavy-duty vehicles. Furthermore, the gradual adoption of hybrid and electric commercial vehicles presents a significant long-term opportunity for manufacturers to innovate and supply advanced e-fluids. Strategic partnerships with vehicle manufacturers and fleet management companies can unlock new market segments and foster brand loyalty.

Leading Players in the Egypt Commercial Vehicles Lubricants Industry Sector

- BP PLC (Castrol)

- Chevron Corporation

- Coperative Soceite des petroleum

- Emarat

- ExxonMobil Corporation

- FUCHS

- Misr Petroleum

- Petromin Corporation

- Royal Dutch Shell PLC

- TotalEnergie

Key Milestones in Egypt Commercial Vehicles Lubricants Industry Industry

- March 2021: Castrol announced the launch of Castrol ON, a Castrol e-fluid range that includes e-gear oils, e-coolants, and e-greases. This range is specially designed for electric vehicles.

- July 2021: ExxonMobil and Trella signed a partnership that will allow Trella to improve trucking productivity and efficiency while also empowering drivers and fleets through the usage of Mobil Delvac.

- January 2022: Effective April 1, ExxonMobil Corporation was organized along three business lines - ExxonMobil Upstream Company, ExxonMobil Product Solutions and ExxonMobil Low Carbon Solutions.

Strategic Outlook for Egypt Commercial Vehicles Lubricants Industry Market

The strategic outlook for the Egyptian commercial vehicles lubricants industry is one of sustained growth and evolving innovation. The market is expected to be driven by the increasing demand for high-performance, fuel-efficient, and environmentally friendly lubricants. Key strategies for success will involve strengthening distribution networks to reach a wider customer base, investing in research and development to introduce advanced formulations that meet future technological demands, and adapting to the potential growth of electric and hybrid commercial vehicles by expanding e-fluid portfolios. Focus on sustainability, cost-effectiveness for fleet operators, and building strong partnerships with industry stakeholders will be crucial for long-term market leadership.

Egypt Commercial Vehicles Lubricants Industry Segmentation

-

1. Product Type

- 1.1. Engine Oils

- 1.2. Greases

- 1.3. Hydraulic Fluids

- 1.4. Transmission & Gear Oils

Egypt Commercial Vehicles Lubricants Industry Segmentation By Geography

- 1. Egypt

Egypt Commercial Vehicles Lubricants Industry Regional Market Share

Geographic Coverage of Egypt Commercial Vehicles Lubricants Industry

Egypt Commercial Vehicles Lubricants Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Engine Oils

- 5.1.2. Greases

- 5.1.3. Hydraulic Fluids

- 5.1.4. Transmission & Gear Oils

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Egypt

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Egypt Commercial Vehicles Lubricants Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Engine Oils

- 6.1.2. Greases

- 6.1.3. Hydraulic Fluids

- 6.1.4. Transmission & Gear Oils

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 BP PLC (Castrol)

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Chevron Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Coperative Soceite des petroleum

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Emarat

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 ExxonMobil Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 FUCHS

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Misr Petroleum

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Petromin Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Royal Dutch Shell PLC

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 TotalEnergie

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 BP PLC (Castrol)

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Egypt Commercial Vehicles Lubricants Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Egypt Commercial Vehicles Lubricants Industry Share (%) by Company 2025

List of Tables

- Table 1: Egypt Commercial Vehicles Lubricants Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Egypt Commercial Vehicles Lubricants Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Egypt Commercial Vehicles Lubricants Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 4: Egypt Commercial Vehicles Lubricants Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Egypt Commercial Vehicles Lubricants Industry?

The projected CAGR is approximately 2.3%.

2. Which companies are prominent players in the Egypt Commercial Vehicles Lubricants Industry?

Key companies in the market include BP PLC (Castrol), Chevron Corporation, Coperative Soceite des petroleum, Emarat, ExxonMobil Corporation, FUCHS, Misr Petroleum, Petromin Corporation, Royal Dutch Shell PLC, TotalEnergie.

3. What are the main segments of the Egypt Commercial Vehicles Lubricants Industry?

The market segments include Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.5 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Largest Segment By Product Type : Engine Oils.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

January 2022: Effective April 1, ExxonMobil Corporation was organized along three business lines - ExxonMobil Upstream Company, ExxonMobil Product Solutions and ExxonMobil Low Carbon Solutions.July 2021: ExxonMobil and Trella signed a partnership that will allow Trella to improve trucking productivity and efficiency while also empowering drivers and fleets through the usage of Mobil Delvac.March 2021: Castrol announced the launch of Castrol ON (a Castrol e-fluid range that includes e-gear oils, e-coolants, and e-greases) to its product portfolio. This range is specially designed for electric vehicles.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Egypt Commercial Vehicles Lubricants Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Egypt Commercial Vehicles Lubricants Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Egypt Commercial Vehicles Lubricants Industry?

To stay informed about further developments, trends, and reports in the Egypt Commercial Vehicles Lubricants Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence