Key Insights

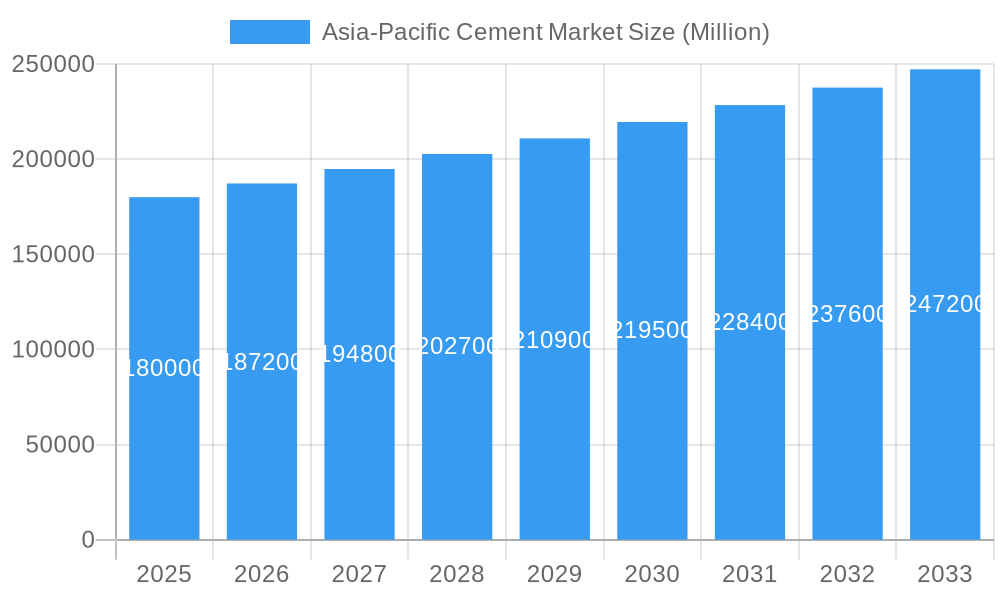

The Asia-Pacific cement market is projected for significant expansion, anticipating a market size of USD 178.4 billion by 2025. The market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.2% during the forecast period (2025-2033). This robust growth is underpinned by substantial infrastructure development, including transportation networks, public housing, and urban renewal, alongside escalating demand from residential and commercial construction. Key drivers include supportive government policies, rising disposable incomes, and the adoption of advanced construction materials and sustainable alternatives. Trends such as digital integration and the use of blended cements further shape market dynamics.

Asia-Pacific Cement Market Market Size (In Billion)

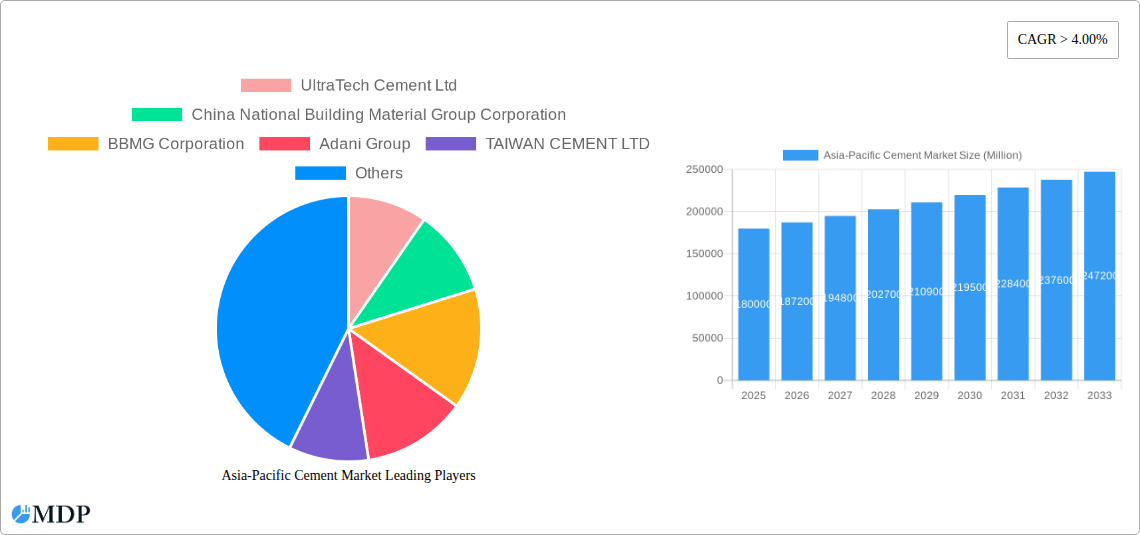

While the market exhibits strong growth potential, it faces challenges including raw material price volatility and stringent environmental regulations. However, strategic investments in product innovation, particularly in blended and fiber cement, demonstrate industry resilience. The competitive landscape is characterized by key players like UltraTech Cement Ltd, China National Building Material Group Corporation, and Anhui Conch Cement Company Limited, who are pursuing strategic expansions through collaborations and M&A to strengthen their market presence in China, India, and Southeast Asia.

Asia-Pacific Cement Market Company Market Share

Asia-Pacific Cement Market Analysis: Growth Drivers, Trends, and Competitive Landscape (2019-2033)

Access comprehensive insights into the dynamic Asia-Pacific Cement Market, covering 2019-2033. This report details market drivers, emerging trends, leading segments, and strategic initiatives within this multi-billion dollar sector. It provides actionable intelligence for stakeholders in cement manufacturing, construction, investment, and policymaking, offering a granular understanding of market concentration, regulations, end-user demands, and M&A activities.

Asia-Pacific Cement Market Market Dynamics & Concentration

The Asia-Pacific cement market is characterized by a moderate to high concentration, with a few key players dominating significant market shares. Innovation drivers are primarily focused on sustainable cement production, energy efficiency, and the development of specialized cementitious materials. Regulatory frameworks, particularly those related to environmental standards and construction codes, play a crucial role in shaping market access and product development. Product substitutes, such as alternative binders and pre-fabricated construction elements, are gaining traction but are yet to significantly disrupt the dominance of traditional cement. End-user trends are heavily influenced by urbanization, infrastructure development, and increasing demand for green building solutions. Mergers and Acquisitions (M&A) activities are a constant feature, indicating strategic consolidation and expansion efforts by major companies to enhance their manufacturing capacity and market presence. For instance, the acquisition of Sanghi Industries by Adani Group signals a strategic move to bolster production capabilities. The M&A deal count in this sector remains robust, reflecting the competitive drive for market leadership.

- Market Concentration: Dominated by a few large corporations with substantial market share.

- Innovation Drivers: Sustainability, energy efficiency, specialized cementitious materials.

- Regulatory Frameworks: Environmental standards, construction codes, safety regulations.

- Product Substitutes: Alternative binders, pre-fabricated construction components.

- End-User Trends: Urbanization, infrastructure boom, green building demand.

- M&A Activities: Strategic consolidation for capacity expansion and market reach.

Asia-Pacific Cement Market Industry Trends & Analysis

The Asia-Pacific cement market is experiencing robust growth, driven by a confluence of factors including rapid urbanization, significant government investments in infrastructure projects across nations like China, India, and Southeast Asian countries, and a burgeoning construction sector catering to residential, commercial, and industrial needs. The projected Compound Annual Growth Rate (CAGR) for this market is estimated at approximately 7.2% during the forecast period. Technological disruptions are manifesting in the adoption of advanced manufacturing processes, such as digitalization of operations, use of artificial intelligence for quality control, and the development of low-carbon footprint cement alternatives. Consumer preferences are shifting towards more sustainable and eco-friendly building materials, pushing manufacturers to innovate in their product offerings. Competitive dynamics are intensifying, with companies focusing on operational efficiency, supply chain optimization, and strategic partnerships to maintain and expand their market penetration. The increasing adoption of blended cements and the continuous demand for Ordinary Portland Cement (OPC) are key indicators of market penetration across various applications. Furthermore, the growing emphasis on resilient infrastructure development, particularly in regions prone to natural disasters, fuels the demand for high-performance cement products. The competitive landscape is marked by both global giants and strong regional players vying for dominance through capacity expansions and strategic acquisitions, as seen in recent industry developments.

Leading Markets & Segments in Asia-Pacific Cement Market

The Asia-Pacific cement market demonstrates distinct leadership across various regions and segments. Dominant regions include China, which accounts for a substantial portion of global cement production and consumption, followed by India, with its massive infrastructure development initiatives. Southeast Asian nations are also emerging as significant growth hubs.

End Use Sector Dominance:

- Infrastructure: This segment is a primary growth engine, fueled by government spending on roads, bridges, airports, and public utilities across the region. The demand for cement in infrastructure projects is consistently high due to the sheer scale and long-term nature of these developments.

- Residential: Rapid population growth and increasing urbanization drive sustained demand for residential construction. This segment benefits from rising disposable incomes and a growing middle class seeking improved housing.

- Commercial, Industrial and Institutional: Expansion of commercial spaces, industrial parks, and institutional facilities in developing economies contributes significantly to cement consumption. This segment is closely tied to economic growth and foreign investment.

Product Segment Dominance:

- Ordinary Portland Cement (OPC): Remains the most widely used cement type due to its versatility, cost-effectiveness, and established use in a vast array of construction applications. Its dominance is expected to continue, though its market share might be gradually influenced by blended alternatives.

- Blended Cement: Gaining significant traction due to its improved durability, reduced environmental impact (lower CO2 emissions), and often superior performance characteristics compared to OPC. Environmental regulations and sustainability initiatives are key drivers for its increasing market penetration.

- Fiber Cement: Witnessing growth in specific applications like roofing, siding, and partitions, particularly in regions focusing on durable and low-maintenance building materials.

The dominance of these segments is underpinned by economic policies promoting construction, significant investments in infrastructure development, and evolving consumer preferences towards sustainable and durable building solutions.

Asia-Pacific Cement Market Product Developments

Product development in the Asia-Pacific cement market is increasingly focused on sustainability and enhanced performance. Innovations include the formulation of low-carbon cements, such as Portland Limestone Cement (PLC) and Geopolymer cement, which significantly reduce greenhouse gas emissions during production. Companies are also developing specialized cementitious materials with improved durability, faster setting times, and enhanced resistance to harsh environmental conditions. These advancements are driven by stringent environmental regulations and the growing demand for green building solutions in both residential and infrastructure projects. The competitive advantage lies in offering products that meet evolving construction needs while adhering to eco-friendly standards, appealing to a market increasingly conscious of its environmental footprint.

Key Drivers of Asia-Pacific Cement Market Growth

The Asia-Pacific cement market's growth is propelled by a powerful combination of factors. Robust economic expansion across major economies in the region fuels demand across all end-use sectors, particularly infrastructure and residential construction. Government initiatives focused on large-scale infrastructure development, including transportation networks, housing projects, and urban renewal programs, provide a consistent stream of demand for cement. Technological advancements in cement production, leading to improved efficiency and cost reduction, also contribute to market expansion. Furthermore, the increasing adoption of sustainable building practices and the demand for eco-friendly construction materials are driving innovation and the uptake of specialized cement products.

- Economic Growth & Urbanization: Driving demand for residential, commercial, and infrastructure development.

- Government Infrastructure Spending: Significant investments in transportation, utilities, and public facilities.

- Technological Advancements: Efficiency gains and cost reductions in cement manufacturing.

- Sustainability Initiatives: Growing preference for eco-friendly and low-carbon cement products.

Challenges in the Asia-Pacific Cement Market Market

Despite its robust growth, the Asia-Pacific cement market faces several challenges that can impede its progress. Stringent environmental regulations concerning emissions and waste management can increase operational costs and necessitate significant investments in compliance technologies. Fluctuations in raw material prices, particularly for key inputs like clinker and energy, can impact profit margins and pricing stability. Intense competition among numerous players, both domestic and international, often leads to price wars and reduced profitability. Moreover, logistical complexities in vast and diverse geographical terrains, coupled with infrastructure limitations in certain areas, can disrupt supply chains and increase distribution costs.

- Environmental Regulations: Increased compliance costs and the need for advanced emission control technologies.

- Raw Material Price Volatility: Impact on production costs and pricing strategies.

- Intense Competition: Leading to price pressures and margin erosion.

- Logistical & Supply Chain Issues: Challenges in distribution across varied geographies.

Emerging Opportunities in Asia-Pacific Cement Market

Emerging opportunities in the Asia-Pacific cement market lie in the growing demand for sustainable and innovative building materials. The increasing focus on smart cities and green building certifications presents a significant avenue for companies offering eco-friendly cement solutions and advanced construction materials. Strategic partnerships and joint ventures with technology providers can unlock new avenues for process optimization and the development of high-performance cements. Furthermore, the gradual shift towards modular and pre-fabricated construction methods could create opportunities for specialized cement products that facilitate these construction techniques. Exploring untapped markets within developing economies and catering to niche applications with value-added cementitious products are also key growth catalysts.

Leading Players in the Asia-Pacific Cement Market Sector

- UltraTech Cement Ltd

- China National Building Material Group Corporation

- BBMG Corporation

- Adani Group

- TAIWAN CEMENT LTD

- Vietnam National Cement Corporation

- Anhui Conch Cement Company Limited

- SCG

- China Resource Cement Holdings

- SIG

Key Milestones in Asia-Pacific Cement Market Industry

- August 2023: The Adani Group's subsidiary, Ambuja Cements Ltd, announced the purchase of a 57% promoter stake in Indian cement manufacturer Sanghi Industries Ltd at an enterprise value of USD 606.5 million, aimed at expanding its manufacturing capacity and market presence.

- June 2023: SIG's subsidiary PT Semen Baturaja Tbk announced plans to expand its cement production capacity to 3.8 million tons of cement per year through three factories in Palembang and Baturaja City, Ogan Komering Ulu (OKU) Regency, South Sumatra, Panjang, Bandar Lampung in Indonesia.

- January 2023: Semen Indonesia (SIG) acquired an 83.52% stake in Solusi Bangun Indonesia, which possesses a 14.8 Mt/yr cement production capacity, thereby strengthening its cement business in Indonesia.

Strategic Outlook for Asia-Pacific Cement Market Market

The strategic outlook for the Asia-Pacific cement market is exceptionally positive, driven by sustained urbanization and massive infrastructure investments. Key growth accelerators include the ongoing push for sustainable construction practices, leading to increased demand for low-carbon cements and specialized building materials. Companies that focus on innovation in product development, particularly in areas of durability, energy efficiency, and reduced environmental impact, will gain a competitive edge. Strategic partnerships and technological collaborations are anticipated to play a crucial role in enhancing operational efficiencies and expanding market reach. The market's future potential is closely tied to its ability to adapt to evolving environmental regulations and to leverage technological advancements for more sustainable and cost-effective production and distribution.

Asia-Pacific Cement Market Segmentation

-

1. End Use Sector

- 1.1. Commercial

- 1.2. Industrial and Institutional

- 1.3. Infrastructure

- 1.4. Residential

-

2. Product

- 2.1. Blended Cement

- 2.2. Fiber Cement

- 2.3. Ordinary Portland Cement

- 2.4. White Cement

- 2.5. Other Types

Asia-Pacific Cement Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. Southeast Asia

- 1.7. Rest of Asia Pacific

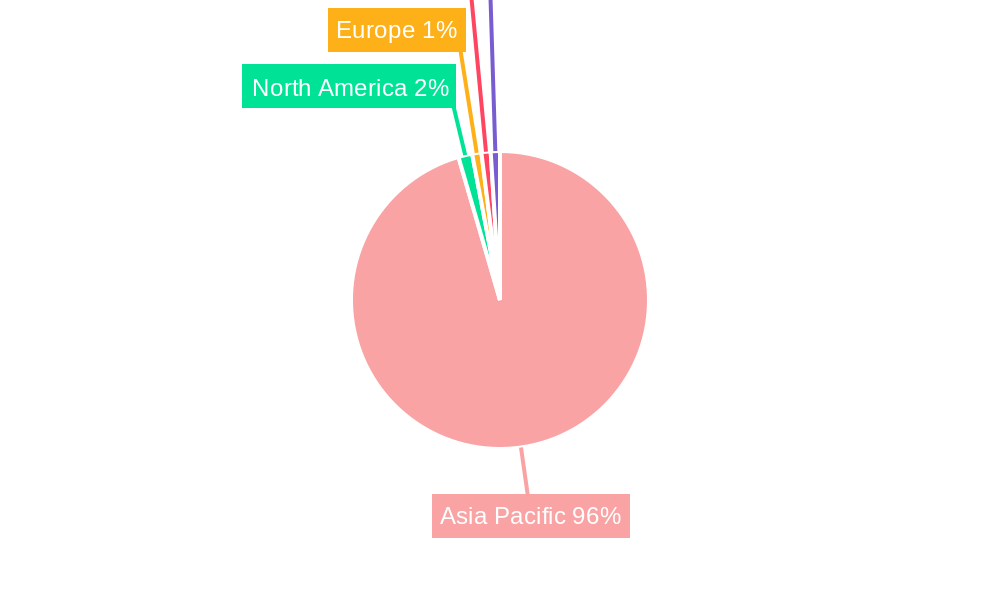

Asia-Pacific Cement Market Regional Market Share

Geographic Coverage of Asia-Pacific Cement Market

Asia-Pacific Cement Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End Use Sector

- 5.1.1. Commercial

- 5.1.2. Industrial and Institutional

- 5.1.3. Infrastructure

- 5.1.4. Residential

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Blended Cement

- 5.2.2. Fiber Cement

- 5.2.3. Ordinary Portland Cement

- 5.2.4. White Cement

- 5.2.5. Other Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by End Use Sector

- 6. Asia-Pacific Cement Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End Use Sector

- 6.1.1. Commercial

- 6.1.2. Industrial and Institutional

- 6.1.3. Infrastructure

- 6.1.4. Residential

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Blended Cement

- 6.2.2. Fiber Cement

- 6.2.3. Ordinary Portland Cement

- 6.2.4. White Cement

- 6.2.5. Other Types

- 6.1. Market Analysis, Insights and Forecast - by End Use Sector

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 UltraTech Cement Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 China National Building Material Group Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 BBMG Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Adani Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 TAIWAN CEMENT LTD

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Vietnam National Cement Corporatio

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Anhui Conch Cement Company Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 SCG

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 China Resource Cement Holdings

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 SIG

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 UltraTech Cement Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Cement Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Cement Market Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Cement Market Revenue billion Forecast, by End Use Sector 2020 & 2033

- Table 2: Asia-Pacific Cement Market Volume K Tons Forecast, by End Use Sector 2020 & 2033

- Table 3: Asia-Pacific Cement Market Revenue billion Forecast, by Product 2020 & 2033

- Table 4: Asia-Pacific Cement Market Volume K Tons Forecast, by Product 2020 & 2033

- Table 5: Asia-Pacific Cement Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Asia-Pacific Cement Market Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: Asia-Pacific Cement Market Revenue billion Forecast, by End Use Sector 2020 & 2033

- Table 8: Asia-Pacific Cement Market Volume K Tons Forecast, by End Use Sector 2020 & 2033

- Table 9: Asia-Pacific Cement Market Revenue billion Forecast, by Product 2020 & 2033

- Table 10: Asia-Pacific Cement Market Volume K Tons Forecast, by Product 2020 & 2033

- Table 11: Asia-Pacific Cement Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Asia-Pacific Cement Market Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: China Asia-Pacific Cement Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: China Asia-Pacific Cement Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 15: Japan Asia-Pacific Cement Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Japan Asia-Pacific Cement Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 17: South Korea Asia-Pacific Cement Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: South Korea Asia-Pacific Cement Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 19: India Asia-Pacific Cement Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: India Asia-Pacific Cement Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 21: Australia Asia-Pacific Cement Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Australia Asia-Pacific Cement Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 23: Southeast Asia Asia-Pacific Cement Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Southeast Asia Asia-Pacific Cement Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 25: Rest of Asia Pacific Asia-Pacific Cement Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Rest of Asia Pacific Asia-Pacific Cement Market Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Cement Market?

The projected CAGR is approximately 5.2%.

2. Which companies are prominent players in the Asia-Pacific Cement Market?

Key companies in the market include UltraTech Cement Ltd, China National Building Material Group Corporation, BBMG Corporation, Adani Group, TAIWAN CEMENT LTD, Vietnam National Cement Corporatio, Anhui Conch Cement Company Limited, SCG, China Resource Cement Holdings, SIG.

3. What are the main segments of the Asia-Pacific Cement Market?

The market segments include End Use Sector, Product.

4. Can you provide details about the market size?

The market size is estimated to be USD 178.4 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand from the Construction Industry; Government Policies to Promote the Usage of Fly Ash.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Harmful Properties of Fly Ash; Non-suitability in Cold Weather Conditions.

8. Can you provide examples of recent developments in the market?

August 2023: The Adani Group's subsidiary, Ambuja Cements Ltd, announced the purchase of a 57% promoter stake in Indian cement manufacturer Sanghi Industries Ltd at an enterprise value of USD 606.5 million to expand its manufacturing capacity and market presence.June 2023: SIG's subsidiary PT Semen Baturaja Tbk announced to expand its cement production capacity to 3.8 million tons of cement per year through three factories in Palembang and Baturaja City, Ogan Komering Ulu (OKU) Regency, South Sumatra, Panjang, Bandar Lampung in Indonesia.January 2023: Semen Indonesia (SIG) acquired an 83.52% stake in Solusi Bangun Indonesia, which has a 14.8 Mt/yr of cement production capacity, strengthening its cement business in Indonesia.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Cement Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Cement Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Cement Market?

To stay informed about further developments, trends, and reports in the Asia-Pacific Cement Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence