Key Insights

The North American satellite bus market is projected for significant expansion, propelled by escalating demand for advanced satellite communication, earth observation, and navigation solutions. With a Compound Annual Growth Rate (CAGR) of 7.2%, the market is set to reach a size of $15.45 billion by 2025. Key growth catalysts include the proliferation of commercial satellite constellations for broadband services, the modernization of governmental and military satellite infrastructure for enhanced surveillance and communication, and the increasing need for precise navigation systems. Technological advancements in satellite miniaturization and payload capacity are further accelerating market growth.

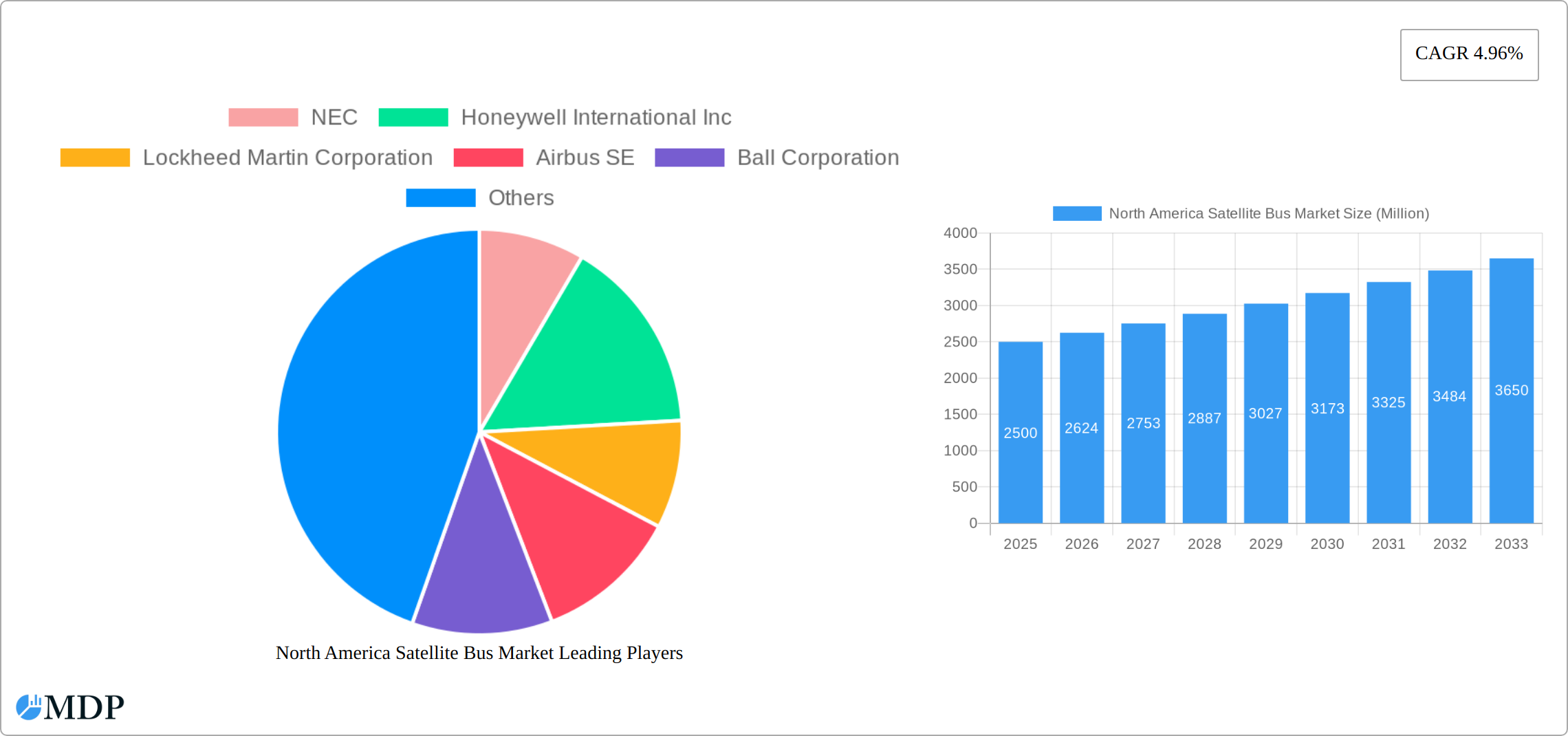

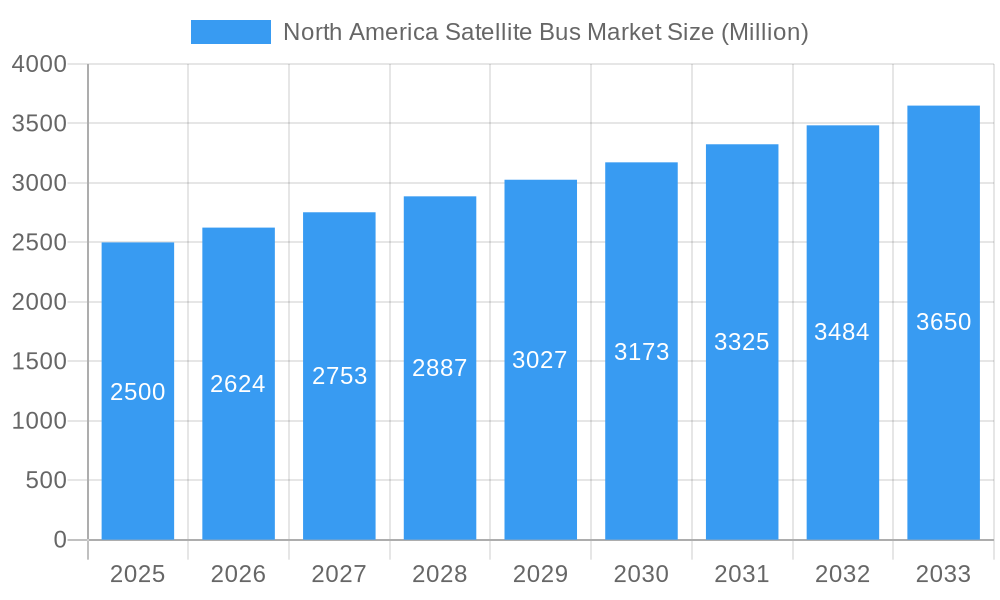

North America Satellite Bus Market Market Size (In Billion)

Geographically, the Geosynchronous Earth Orbit (GEO) segment is expected to maintain a substantial market share, while the Low Earth Orbit (LEO) segment is poised for remarkable growth due to its suitability for high-bandwidth applications and reduced latency. The growing adoption of smaller, more affordable satellite buses, particularly within the 10-100kg mass category, will democratize access for emerging companies and fuel market expansion. Leading entities such as Lockheed Martin, Northrop Grumman, and Airbus are strategically investing in innovative bus technologies and forging partnerships to strengthen their market presence. The United States is anticipated to lead the North American market share throughout the forecast period.

North America Satellite Bus Market Company Market Share

Market restraints primarily stem from the substantial initial investment costs for satellite development and launch, coupled with regulatory compliance complexities and space debris concerns. However, increased investment in space exploration and the development of reusable launch vehicles are expected to mitigate these challenges. Continuous innovation in miniaturized components and software-defined radios is enhancing the cost-effectiveness and flexibility of satellite buses, thereby lowering entry barriers and promoting further market expansion in North America. This dynamic interplay of growth drivers and mitigating factors solidifies the North American satellite bus market's trajectory for sustained, considerable growth.

North America Satellite Bus Market: A Comprehensive Analysis (2019-2033)

This in-depth report provides a comprehensive analysis of the North America Satellite Bus Market, offering invaluable insights for industry stakeholders. Covering the period from 2019 to 2033, with a focus on 2025, this report dissects market dynamics, trends, leading players, and future growth potential. The market is segmented by orbit class (GEO, LEO, MEO), end-user (Commercial, Military & Government, Other), application (Communication, Earth Observation, Navigation, Space Observation, Others), and satellite mass (Below 10 Kg, 10-100kg, 100-500kg, 500-1000kg, above 1000kg). Expect detailed analysis of key players including NEC, Honeywell International Inc, Lockheed Martin Corporation, Airbus SE, Ball Corporation, Sierra Nevada Corporation, Nano Avionics, Thales, and Northrop Grumman Corporation. The report projects a market valued at xx Million by 2033.

North America Satellite Bus Market Market Dynamics & Concentration

The North America satellite bus market is characterized by a dynamic interplay of established players and emerging innovators, leading to a moderately concentrated landscape. Leading manufacturers like Lockheed Martin, Boeing, and Airbus SE continue to hold significant market share, collectively representing approximately **[Insert specific percentage here]%** of the market in 2024. However, the competitive environment is intensifying with the advent of agile, smaller companies that are driving innovation and pushing the boundaries of satellite technology. Key growth catalysts include the relentless pursuit of miniaturization, significant advancements in cost reduction strategies, and the development of enhanced payload capacities. The market's trajectory is also shaped by a stringent regulatory environment governing space activities, which influences market entry and operational frameworks. Simultaneously, the escalating demand for high-throughput communication services and sophisticated earth observation capabilities is a primary growth engine. While terrestrial communication networks present product substitutes, their applicability is limited in scenarios demanding the unique, global reach and resilience offered by satellite systems. The market has also seen a surge in strategic mergers and acquisitions, with **[Insert specific number here]** substantial deals finalized between 2019 and 2024, underscoring consolidation and strategic growth initiatives. End-user trends reveal a robust and growing demand from both the commercial and government sectors, propelling the market toward sustained expansion.

- Market Concentration: Moderately concentrated, with a core group of key players dominating but facing increasing competition from innovative new entrants.

- Innovation Drivers: Miniaturization of satellite components, significant advancements in cost reduction methodologies, and the development of enhanced payload capacities are paramount.

- Regulatory Frameworks: Stringent and evolving regulations governing space activities continue to impact market entry strategies and operational compliance.

- Product Substitutes: Limited, as satellite systems offer unique advantages for specific applications where terrestrial alternatives fall short.

- End-User Trends: A clear upward trend in demand from both the commercial and government sectors, indicating broad market appeal.

- M&A Activities: A notable increase in strategic mergers and acquisitions, with **[Insert specific number here]** significant deals recorded between 2019 and 2024.

North America Satellite Bus Market Industry Trends & Analysis

The North America satellite bus market exhibits robust growth, projected at a CAGR of xx% during the forecast period (2025-2033). This growth is primarily driven by increasing demand for satellite-based communication, navigation, and earth observation services, coupled with advancements in satellite technologies. The market penetration of small satellites is increasing rapidly, driving down costs and enabling the development of constellations for diverse applications. Technological disruptions, such as the adoption of advanced materials and propulsion systems, are improving satellite performance and longevity. Consumer preferences are shifting towards higher bandwidth, lower latency, and more reliable satellite services, creating opportunities for innovative satellite bus designs. Competitive dynamics are characterized by intense competition among established players and emerging entrants, fostering innovation and price reductions.

Leading Markets & Segments in North America Satellite Bus Market

The North America satellite bus market is currently experiencing a pronounced dominance from the Low Earth Orbit (LEO) segment. This surge is primarily attributable to the burgeoning demand for satellite constellations designed for global internet connectivity and advanced earth observation applications. On the end-user front, the Commercial sector stands as the largest and most influential segment, closely followed by the substantial Military & Government sector.

- Orbit Class:

- LEO: The leading segment, propelled by the rapid growth of satellite constellations addressing the increasing demand for ubiquitous internet access, the proliferation of IoT devices, and the critical need for high-resolution earth imagery.

- GEO: Demonstrates strong growth potential, largely driven by the persistent demand from telecommunications and broadcasting industries for reliable, high-capacity services.

- MEO: Exhibits moderate but steady growth, primarily fueled by applications in satellite navigation and communication systems requiring a balance between coverage and latency.

- End User:

- Commercial: The largest and most dynamic segment, characterized by significant investment and activity from private companies. Key drivers include the expansion of satellite-based internet access, sophisticated environmental monitoring, and crucial disaster relief operations.

- Military & Government: A vital and substantial segment, driven by national security imperatives, intelligence gathering, advanced surveillance capabilities, and secure communication needs.

- Other: This segment encompasses research and development organizations and academic institutions contributing to technological advancements and scientific missions.

- Application:

- Communication: The largest and most significant application area, propelled by the ever-increasing global demand for high-speed internet connectivity and robust communication services.

- Earth Observation: Experiencing strong growth, driven by critical needs in environmental monitoring, climate change research, resource management, and agricultural applications.

- Navigation: Demonstrating steady and reliable growth, underpinned by the indispensable role of GPS and other satellite-based navigation systems in various sectors.

- Satellite Mass:

- 100-500kg: Currently the most prevalent mass category, offering an optimal balance between payload capacity and launch costs. This segment is influenced by the overarching trend towards smaller, more efficient spacecraft.

- 10-100kg: This category is rapidly gaining market traction, particularly due to the burgeoning demand for smallsat constellations that enable agile and cost-effective deployment for a variety of missions.

North America Satellite Bus Market Product Developments

Recent product innovations in the North America satellite bus market are heavily focused on achieving significant breakthroughs in miniaturization, enhancing payload capacity, and improving overall fuel efficiency. Manufacturers are actively developing next-generation satellite buses designed to accommodate a wider array of applications, including CubeSats, nanosatellites, and microsatellites. The integration of cutting-edge technologies, such as artificial intelligence (AI) and machine learning (ML), is revolutionizing onboard processing and autonomy, leading to substantially improved operational efficiency and mission effectiveness. These advancements not only provide manufacturers with critical competitive advantages but also enable them to deliver higher performance, reduced costs, and greater adaptability to the diverse and evolving requirements of various space missions.

Key Drivers of North America Satellite Bus Market Growth

The North America satellite bus market is propelled by several factors. Technological advancements, such as improved propulsion systems and miniaturization techniques, significantly reduce launch costs and increase satellite lifespan. Favorable government policies and increased funding for space exploration and defense initiatives bolster market growth. The rising demand for high-bandwidth communication, precise navigation, and comprehensive earth observation fuels the market's expansion.

Challenges in the North America Satellite Bus Market Market

Several challenges hinder the market's growth. Stringent regulatory requirements and licensing procedures pose obstacles to market entry. Supply chain disruptions and the reliance on limited suppliers can impact production and delivery timelines. The competitive landscape, with established players and new entrants, creates pressure on pricing and margins. These challenges impact market growth, leading to a slower overall increase than what might otherwise be anticipated. For example, supply chain issues in 2022-2023 reduced production by an estimated xx%.

Emerging Opportunities in North America Satellite Bus Market

The long-term growth trajectory of the North America satellite bus market is significantly bolstered by ongoing technological breakthroughs in critical areas such as electric propulsion systems and advanced lightweight materials. Strategic collaborations and partnerships between government agencies and private sector enterprises are fostering a fertile ground for innovation and market expansion. The increasing public and commercial interest in space tourism and private space exploration is further contributing to the expanding market potential and creating new avenues for development. The market is exceptionally well-positioned to capitalize on the escalating demand for Internet-of-Things (IoT) applications and the expanding utility of satellites for crucial functions like disaster relief coordination and comprehensive environmental monitoring.

Leading Players in the North America Satellite Bus Market Sector

Key Milestones in North America Satellite Bus Market Industry

- July 2020: Space News Inc. (SNC) was awarded a contract by the Defense Innovation Unit (DIU) to repurpose its Shooting Star transport vehicle into an Unmanned Orbital Outpost, highlighting advancements in orbital infrastructure.

- August 2020: Space News Inc. (SNC) unveiled two new satellite platforms, the SN-200M (designed for Medium Earth Orbit) and the SN-1000, showcasing expanded product offerings for diverse missions.

- October 2020: NanoAvionics expanded its operational footprint by establishing a presence in the United Kingdom, indicating international growth and market penetration.

These pivotal milestones underscore significant investments in satellite technology and the development of critical space infrastructure, collectively contributing to robust market growth and sustained innovation within the industry.

Strategic Outlook for North America Satellite Bus Market Market

The North America satellite bus market presents significant growth potential driven by technological advancements, increasing demand for satellite-based services, and supportive government policies. Strategic opportunities exist in developing innovative satellite bus designs, expanding into new applications, and forging strategic partnerships. Companies focusing on miniaturization, cost reduction, and enhanced payload capacity are well-positioned to capitalize on the market's future growth. The integration of advanced technologies, such as AI and machine learning, will further enhance the capabilities and efficiency of satellite bus systems, creating additional growth opportunities in the years to come.

North America Satellite Bus Market Segmentation

-

1. Application

- 1.1. Communication

- 1.2. Earth Observation

- 1.3. Navigation

- 1.4. Space Observation

- 1.5. Others

-

2. Satellite Mass

- 2.1. 10-100kg

- 2.2. 100-500kg

- 2.3. 500-1000kg

- 2.4. Below 10 Kg

- 2.5. above 1000kg

-

3. Orbit Class

- 3.1. GEO

- 3.2. LEO

- 3.3. MEO

-

4. End User

- 4.1. Commercial

- 4.2. Military & Government

- 4.3. Other

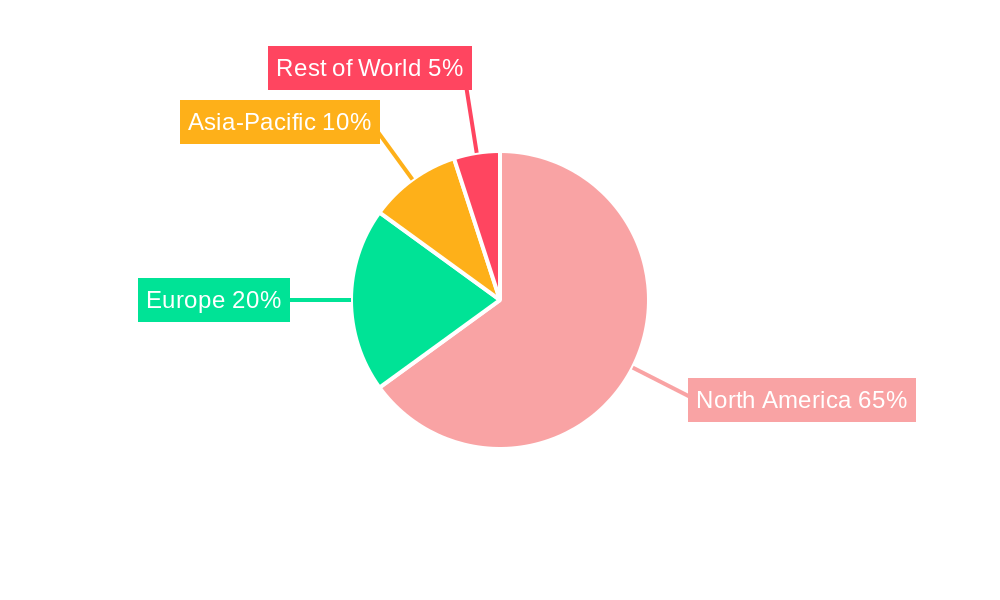

North America Satellite Bus Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Satellite Bus Market Regional Market Share

Geographic Coverage of North America Satellite Bus Market

North America Satellite Bus Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Communication

- 5.1.2. Earth Observation

- 5.1.3. Navigation

- 5.1.4. Space Observation

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Satellite Mass

- 5.2.1. 10-100kg

- 5.2.2. 100-500kg

- 5.2.3. 500-1000kg

- 5.2.4. Below 10 Kg

- 5.2.5. above 1000kg

- 5.3. Market Analysis, Insights and Forecast - by Orbit Class

- 5.3.1. GEO

- 5.3.2. LEO

- 5.3.3. MEO

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Commercial

- 5.4.2. Military & Government

- 5.4.3. Other

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Satellite Bus Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Communication

- 6.1.2. Earth Observation

- 6.1.3. Navigation

- 6.1.4. Space Observation

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Satellite Mass

- 6.2.1. 10-100kg

- 6.2.2. 100-500kg

- 6.2.3. 500-1000kg

- 6.2.4. Below 10 Kg

- 6.2.5. above 1000kg

- 6.3. Market Analysis, Insights and Forecast - by Orbit Class

- 6.3.1. GEO

- 6.3.2. LEO

- 6.3.3. MEO

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Commercial

- 6.4.2. Military & Government

- 6.4.3. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 NEC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Honeywell International Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Lockheed Martin Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Airbus SE

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Ball Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Sierra Nevada Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Nano Avionics

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Thale

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Northrop Grumman Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 NEC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Satellite Bus Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Satellite Bus Market Share (%) by Company 2025

List of Tables

- Table 1: North America Satellite Bus Market Revenue billion Forecast, by Application 2020 & 2033

- Table 2: North America Satellite Bus Market Revenue billion Forecast, by Satellite Mass 2020 & 2033

- Table 3: North America Satellite Bus Market Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 4: North America Satellite Bus Market Revenue billion Forecast, by End User 2020 & 2033

- Table 5: North America Satellite Bus Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: North America Satellite Bus Market Revenue billion Forecast, by Application 2020 & 2033

- Table 7: North America Satellite Bus Market Revenue billion Forecast, by Satellite Mass 2020 & 2033

- Table 8: North America Satellite Bus Market Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 9: North America Satellite Bus Market Revenue billion Forecast, by End User 2020 & 2033

- Table 10: North America Satellite Bus Market Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States North America Satellite Bus Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada North America Satellite Bus Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico North America Satellite Bus Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Satellite Bus Market?

The projected CAGR is approximately 7.2%.

2. Which companies are prominent players in the North America Satellite Bus Market?

Key companies in the market include NEC, Honeywell International Inc, Lockheed Martin Corporation, Airbus SE, Ball Corporation, Sierra Nevada Corporation, Nano Avionics, Thale, Northrop Grumman Corporation.

3. What are the main segments of the North America Satellite Bus Market?

The market segments include Application, Satellite Mass, Orbit Class, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.45 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

October 2020: NanoAvionics expanded its presence in the United Kingdom by beginning operations at its new facility in Basingstoke for satellite assembly, integration, and testing (AIT), as well as sales, technical support, and R&D activities.August 2020: SNC introduced two new satellite platforms to its spacecraft offerings, the SN-200M satellite bus, designed for medium Earth orbit (MEO), and SN-1000.July 2020: SNC was awarded a contract by the Defense Innovation Unit (DIU) for repurposing its Shooting Star transport vehicle to an Unmanned Orbital Outpost, a scalable and autonomous space.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Satellite Bus Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Satellite Bus Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Satellite Bus Market?

To stay informed about further developments, trends, and reports in the North America Satellite Bus Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence