Key Insights

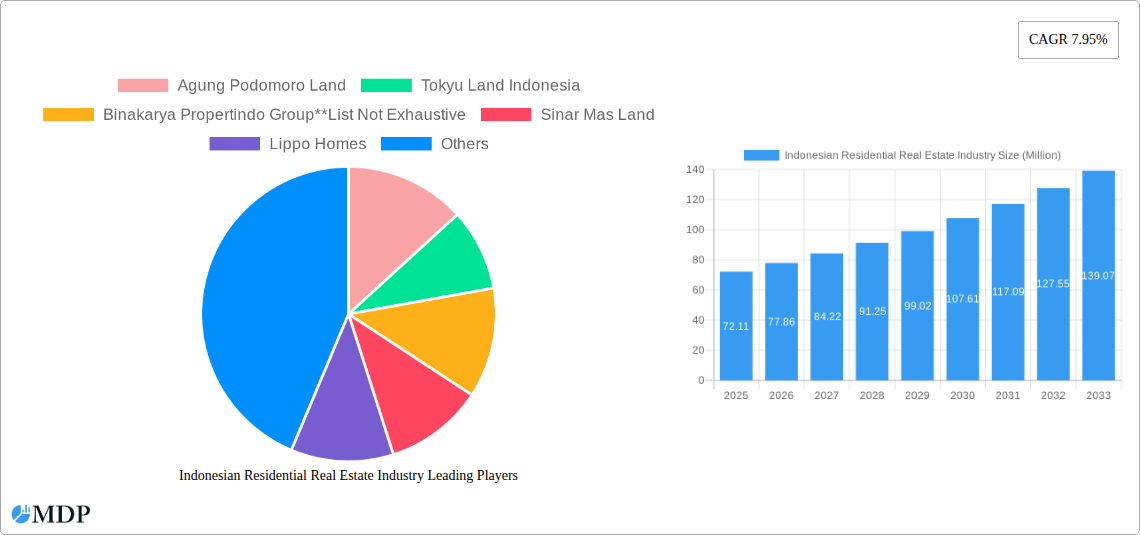

The Indonesian residential real estate market, valued at $72.11 million in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 7.95% from 2025 to 2033. This positive trajectory is driven by several key factors. A burgeoning middle class with increasing disposable income fuels demand for improved housing, particularly in rapidly urbanizing areas like Jakarta, Surabaya, and Semarang. Government initiatives aimed at improving infrastructure and affordable housing further contribute to market expansion. The market is segmented by property type (condominiums and apartments, villas and landed houses) and key cities, reflecting diverse consumer preferences and regional economic disparities. Competition is fierce, with major players like Agung Podomoro Land, Tokyu Land Indonesia, and Sinar Mas Land vying for market share. While challenges exist, such as land scarcity in prime locations and fluctuating interest rates, the overall outlook remains optimistic due to Indonesia's strong economic fundamentals and the continued urbanization trend.

Indonesian Residential Real Estate Industry Market Size (In Million)

The projected market size for 2033 can be estimated by applying the CAGR. While precise figures for individual segments are unavailable, the data suggests a significant concentration in Jakarta and other major cities, with considerable growth potential in secondary markets as infrastructure improves. The dominance of large developers highlights the scale of the industry, however, the emergence of smaller, niche players catering to specific market segments is also anticipated. Furthermore, sustainable and eco-friendly housing options are likely to gain increasing traction, driven by growing environmental awareness among consumers. The long-term forecast indicates continued growth, albeit potentially at a slightly moderated pace as the market matures and development reaches saturation points in some areas. This necessitates adaptation and diversification by developers to maintain competitive edge in a dynamic market landscape.

Indonesian Residential Real Estate Industry Company Market Share

Indonesian Residential Real Estate Market Report: 2019-2033

Uncover the lucrative opportunities and challenges shaping Indonesia's dynamic residential real estate sector. This comprehensive report provides an in-depth analysis of the Indonesian residential real estate market, forecasting trends from 2025 to 2033. Benefit from detailed insights into market dynamics, leading players, and emerging opportunities, empowering strategic decision-making within this high-growth sector. The report covers a historical period of 2019-2024, with a base year of 2025 and an estimated year of 2025.

This report is crucial for investors, developers, and industry stakeholders seeking to navigate the complexities and capitalize on the immense potential of the Indonesian residential real estate market. With a focus on key players like Agung Podomoro Land, Tokyu Land Indonesia, Binakarya Propertindo Group, Sinar Mas Land, Lippo Homes, JABABEKA, PT Pakuwon Jati, Ciputra Group, PP Properti, and Duta Anggada Realty (list not exhaustive), this report provides granular insights into market segments including condominiums and apartments, villas and landed houses, across key cities like Jakarta, Greater Surabaya, Semarang, and the Rest of Indonesia.

Indonesian Residential Real Estate Industry Market Dynamics & Concentration

The Indonesian residential real estate market, valued at xx Million in 2024, exhibits a moderately concentrated landscape. Major players like Sinar Mas Land and Lippo Homes hold significant market share, estimated at approximately xx% and xx%, respectively (2024 data). However, a considerable number of smaller developers contribute to market dynamism. Innovation is driven by evolving consumer preferences, particularly towards sustainable and technologically advanced housing solutions. The regulatory framework, while undergoing reforms, presents both opportunities and challenges for developers. Product substitutes, such as rental properties and co-living spaces, are gaining traction, impacting the market share of traditional residential offerings. End-user trends show a growing preference for properties in strategic locations with improved infrastructure and amenities. M&A activity has seen a steady increase in recent years, with an estimated xx M&A deals recorded in 2024. This activity is largely driven by the need to consolidate market share and expand into new geographical areas or product segments.

- Market Concentration: Moderately concentrated, with top players holding xx% market share (2024).

- Innovation Drivers: Sustainable design, smart home technology, and improved amenities.

- Regulatory Framework: Ongoing reforms impacting development timelines and costs.

- Product Substitutes: Rental properties and co-living spaces are gaining popularity.

- End-User Trends: Demand for strategically located properties with superior infrastructure.

- M&A Activity: xx M&A deals in 2024, indicating consolidation and expansion efforts.

Indonesian Residential Real Estate Industry Industry Trends & Analysis

The Indonesian residential real estate market is experiencing robust growth, driven by a burgeoning middle class, rapid urbanization, and government initiatives promoting affordable housing. The Compound Annual Growth Rate (CAGR) during the historical period (2019-2024) was estimated at xx%, and is projected to remain strong at xx% during the forecast period (2025-2033). Technological disruptions, such as the adoption of proptech platforms and digital marketing strategies, are transforming the industry. Consumer preferences are shifting towards sustainable and technologically advanced homes, emphasizing energy efficiency and smart home features. Competitive dynamics are marked by increasing competition among established players and the emergence of new entrants. Market penetration of smart home technologies remains relatively low but is expected to experience significant growth, driven by increasing affordability and consumer awareness. The market penetration of green building certifications is also expected to increase from xx% in 2024 to xx% by 2033.

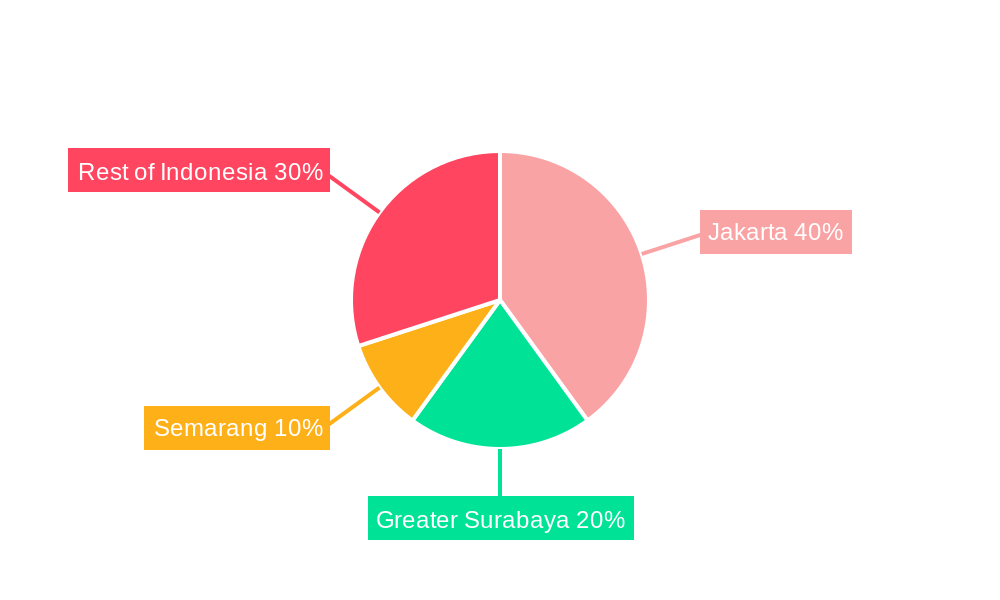

Leading Markets & Segments in Indonesian Residential Real Estate Industry

Jakarta remains the dominant market, accounting for approximately xx% of total transactions in 2024, driven by strong economic activity, high population density, and robust infrastructure development. Greater Surabaya and Semarang also show considerable potential, experiencing growth rates above the national average. Within segments, condominiums and apartments continue to be the most popular choice, primarily due to their affordability and convenient location within urban centers. However, the demand for villas and landed houses in suburban areas is also rising, driven by changing lifestyle preferences and the increasing affordability of these properties.

- Key Drivers for Jakarta's Dominance: Strong economy, high population, excellent infrastructure.

- Greater Surabaya & Semarang Growth: Above-national-average growth driven by infrastructure improvements and economic development.

- Condominiums & Apartments: High demand due to affordability and convenient location.

- Villas & Landed Houses: Rising popularity driven by lifestyle changes and affordability.

Indonesian Residential Real Estate Industry Product Developments

Product innovation is largely focused on incorporating sustainable and technologically advanced features. Developers are increasingly integrating smart home technology, energy-efficient designs, and sustainable building materials into their projects. This reflects a growing consumer demand for environmentally friendly and technologically advanced housing solutions, increasing their competitive advantage in the market. The integration of PropTech solutions for property management is also improving efficiency and customer experience.

Key Drivers of Indonesian Residential Real Estate Industry Growth

Several factors contribute to the growth of the Indonesian residential real estate market: Firstly, a rapidly expanding middle class fuels increasing demand. Secondly, government initiatives aimed at providing affordable housing and improving infrastructure are crucial. Thirdly, urbanization continues to drive demand for housing in major cities. Finally, the growing adoption of technology is enhancing efficiency and creating new market opportunities.

Challenges in the Indonesian Residential Real Estate Industry Market

The Indonesian residential real estate market faces challenges including land acquisition complexities, bureaucratic hurdles, and infrastructure constraints in certain areas. Supply chain disruptions and fluctuating material costs also impact profitability. Furthermore, intense competition among developers puts pressure on pricing and margins. These factors together can reduce profit margins and slow down overall market growth.

Emerging Opportunities in Indonesian Residential Real Estate Industry

Long-term growth is fueled by technological advancements in construction and property management, strategic partnerships to access funding and expertise, and government support for sustainable development. Expansion into underserved markets and the development of affordable housing solutions present significant opportunities. Leveraging PropTech solutions for streamlined processes and enhanced customer engagement will be crucial for future success.

Leading Players in the Indonesian Residential Real Estate Industry Sector

- Agung Podomoro Land

- Tokyu Land Indonesia

- Binakarya Propertindo Group

- Sinar Mas Land

- Lippo Homes

- JABABEKA

- PT Pakuwon Jati

- Ciputra Group

- PP Properti

- Duta Anggada Realty

Key Milestones in Indonesian Residential Real Estate Industry Industry

- 2020: Government launches a new affordable housing program.

- 2022: Significant increase in PropTech investment.

- 2023: Several large-scale residential projects are completed in Jakarta.

- 2024: Merger of two major developers creates a new market leader.

Strategic Outlook for Indonesian Residential Real Estate Industry Market

The Indonesian residential real estate market is poised for continued growth, driven by strong fundamentals and emerging opportunities. Strategic partnerships, technological innovation, and government support will be critical for success. Focusing on sustainable development and addressing the challenges of affordability and infrastructure will unlock the sector's immense long-term potential. The market's future trajectory depends heavily on successful navigation of regulatory changes and adoption of innovative construction and property management technologies.

Indonesian Residential Real Estate Industry Segmentation

-

1. Type

- 1.1. Condominiums and Apartments

- 1.2. Villas and landed houses

-

2. Key Cities

- 2.1. Jakarta

- 2.2. Greater Surabaya

- 2.3. Semarang

- 2.4. Rest of Indonesia

Indonesian Residential Real Estate Industry Segmentation By Geography

- 1. Indonesia

Indonesian Residential Real Estate Industry Regional Market Share

Geographic Coverage of Indonesian Residential Real Estate Industry

Indonesian Residential Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.95% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Condominiums and Apartments

- 5.1.2. Villas and landed houses

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Jakarta

- 5.2.2. Greater Surabaya

- 5.2.3. Semarang

- 5.2.4. Rest of Indonesia

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Indonesia

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Indonesian Residential Real Estate Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Condominiums and Apartments

- 6.1.2. Villas and landed houses

- 6.2. Market Analysis, Insights and Forecast - by Key Cities

- 6.2.1. Jakarta

- 6.2.2. Greater Surabaya

- 6.2.3. Semarang

- 6.2.4. Rest of Indonesia

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Agung Podomoro Land

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Tokyu Land Indonesia

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Binakarya Propertindo Group**List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Sinar Mas Land

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Lippo Homes

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 JABABEKA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 PT Pakuwon Jati

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Ciputra Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 PP Properti

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Duta Anggada Realty

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Agung Podomoro Land

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Indonesian Residential Real Estate Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Indonesian Residential Real Estate Industry Share (%) by Company 2025

List of Tables

- Table 1: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 3: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 6: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indonesian Residential Real Estate Industry?

The projected CAGR is approximately 7.95%.

2. Which companies are prominent players in the Indonesian Residential Real Estate Industry?

Key companies in the market include Agung Podomoro Land, Tokyu Land Indonesia, Binakarya Propertindo Group**List Not Exhaustive, Sinar Mas Land, Lippo Homes, JABABEKA, PT Pakuwon Jati, Ciputra Group, PP Properti, Duta Anggada Realty.

3. What are the main segments of the Indonesian Residential Real Estate Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 72.11 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Investment in Infrastructure Projects; The rising popularity of sustainable architecture.

6. What are the notable trends driving market growth?

Jakarta Emerging as a Prime Rental Market.

7. Are there any restraints impacting market growth?

Volatility in Raw material prices.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indonesian Residential Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indonesian Residential Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indonesian Residential Real Estate Industry?

To stay informed about further developments, trends, and reports in the Indonesian Residential Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence