Key Insights

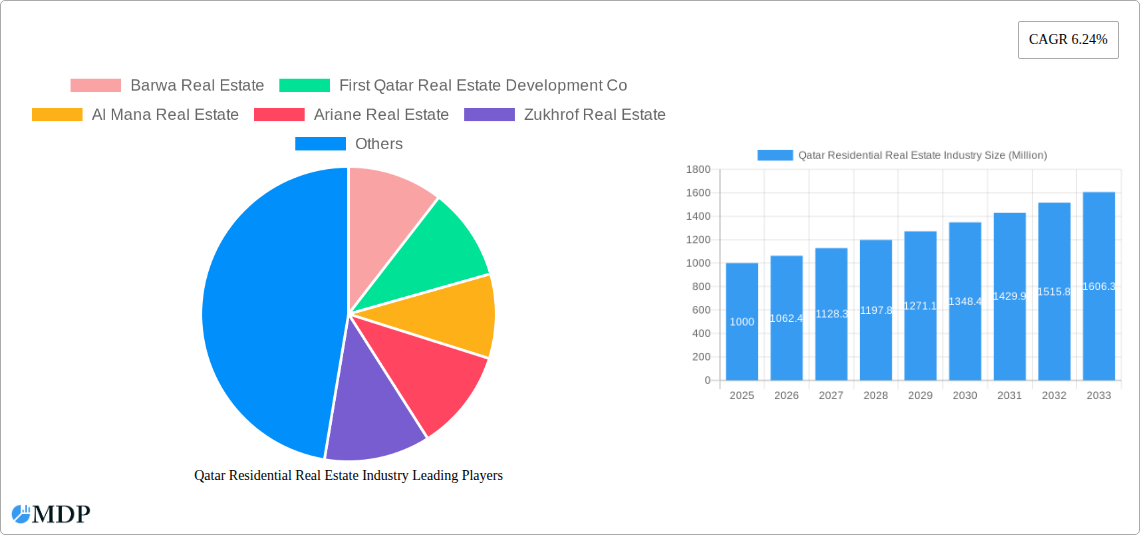

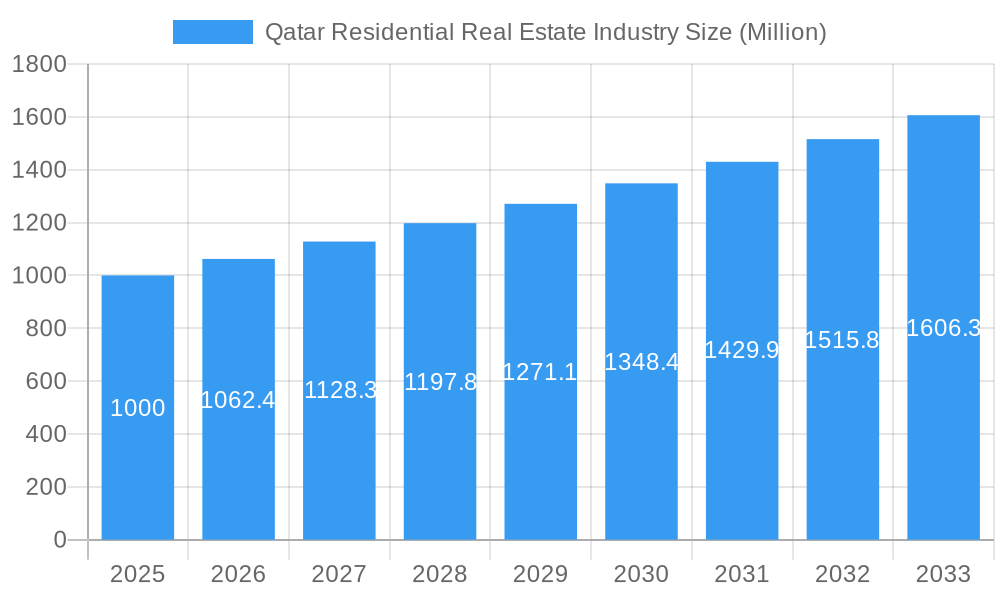

The Qatar residential real estate market is projected to reach $7831.75 million by 2033, demonstrating a robust Compound Annual Growth Rate (CAGR) of 7.46% from the base year 2024. This growth is propelled by Qatar's strong economic performance, driven by the energy and infrastructure sectors, which attracts foreign investment and enhances domestic purchasing power. Legacy projects from the FIFA World Cup and associated infrastructure enhancements significantly boost demand for residential properties, particularly in major cities such as Doha, Al Wakrah, and Al Rayyan. Government initiatives focused on affordable housing and improving living standards further stimulate sustained market activity. The market is segmented by property type, including apartments & condominiums and villas & landed houses, and by location, reflecting diverse demand and price points across different regions. Leading market participants like Barwa Real Estate and First Qatar Real Estate Development Co are actively influencing market dynamics through new developments and strategic investments.

Qatar Residential Real Estate Industry Market Size (In Billion)

Despite significant growth potential, market restraints include fluctuations in global oil prices and the risk of economic downturns. Challenges such as the availability of skilled labor and the cost of construction materials require careful management. Increasing market competition, particularly with the emergence of new developers, also presents a factor. Nonetheless, the long-term outlook for the Qatar residential real estate market remains optimistic, supported by consistent economic expansion, ongoing infrastructure development, and a growing population. The diversification of Qatar's economy beyond oil and gas further supports the sector's sustained progress. Demand for various property types is expected to remain strong, catering to both local and expatriate communities.

Qatar Residential Real Estate Industry Company Market Share

Qatar Residential Real Estate Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Qatar residential real estate market, offering invaluable insights for investors, developers, and industry stakeholders. Covering the period from 2019 to 2033, with a focus on 2025, this report meticulously examines market dynamics, trends, leading players, and future growth potential. The analysis incorporates data-driven forecasts and expert opinions to deliver a clear and actionable understanding of this dynamic sector. The report projects a market valued at XX Million in 2025, with a Compound Annual Growth Rate (CAGR) of XX% from 2025 to 2033.

Qatar Residential Real Estate Industry Market Dynamics & Concentration

This section analyzes the competitive landscape, regulatory environment, and key trends shaping the Qatar residential real estate market. We examine market concentration, identifying major players and their respective market shares. The impact of mergers and acquisitions (M&A) activities is also assessed, including deal counts and their influence on market structure. Innovation drivers, such as sustainable building practices and technological advancements in property management, are explored, along with the impact of product substitutes (e.g., rental apartments) and evolving end-user preferences. The regulatory framework, including government policies and building codes, is analyzed for its impact on market growth and investment decisions.

- Market Concentration: The Qatar residential real estate market exhibits a moderately concentrated structure, with a handful of major players controlling a significant share of the market. Precise market share data for individual companies is not publicly available and requires further primary research; however, we estimate that the top 5 players hold approximately XX% of the market share in 2025.

- M&A Activity: The number of M&A deals in the sector during 2019-2024 was approximately XX, primarily driven by consolidation among smaller developers and strategic acquisitions by larger players.

- Innovation Drivers: The sector is witnessing growing adoption of sustainable building materials and technologies aimed at enhancing energy efficiency and reducing environmental impact.

- Regulatory Framework: Government initiatives aimed at promoting affordable housing and attracting foreign investment significantly impact the market.

Qatar Residential Real Estate Industry Industry Trends & Analysis

This section delves into the key trends driving growth and shaping the competitive dynamics within the Qatar residential real estate market. We analyze factors such as population growth, urbanization, economic diversification, infrastructure development, and evolving consumer preferences, using a combination of qualitative and quantitative analysis to provide a comprehensive understanding of market dynamics. The analysis also takes into account technological disruptions, such as the use of PropTech solutions and digital marketing strategies, and their impact on market participants.

The significant increase in infrastructure spending and population growth acts as crucial drivers for the market’s expansion. Furthermore, the government’s initiatives towards constructing more affordable housing have boosted the sector. Technological integration, such as the introduction of smart homes and improved digital marketing, have also enhanced market growth. This has led to an increase in competition amongst leading companies.

Leading Markets & Segments in Qatar Residential Real Estate Industry

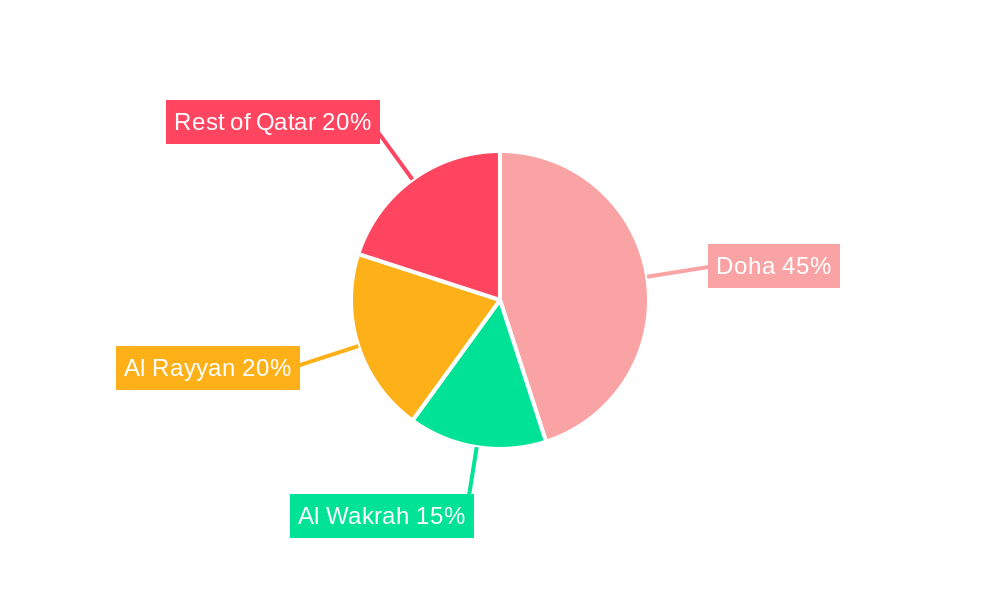

This section identifies the dominant segments and regions within the Qatar residential real estate market. The analysis focuses on the performance of key segments, including apartments and condominiums, villas and landed houses, across major cities (Doha, Al Wakrah, Al Rayyan, and Rest of Qatar). We analyze the underlying drivers of dominance, considering factors such as economic policies, infrastructure development, and consumer preferences.

- By Type: Apartments and condominiums constitute the largest segment, driven by high demand from young professionals and families. Villas and landed houses cater to a more affluent demographic, representing a smaller but still significant segment.

- By Key Cities: Doha accounts for the largest share of the market, followed by Al Rayyan and Al Wakrah. The "Rest of Qatar" segment demonstrates steady growth, driven by government-led infrastructure development projects in peripheral areas.

- Key Drivers:

- Doha: Strong economic activity, extensive infrastructure, and high population density contribute to its dominant market share.

- Al Rayyan: Proximity to Doha and the development of new residential projects drive growth in this area.

- Al Wakrah: The World Cup 2022 has stimulated significant infrastructure development and investments in residential properties.

Qatar Residential Real Estate Industry Product Developments

The Qatar residential real estate market is witnessing ongoing product innovations, driven by technological advancements and evolving consumer preferences. Smart home technologies, sustainable building materials, and innovative architectural designs are becoming increasingly common. These developments enhance the value proposition of residential properties, providing improved functionality, energy efficiency, and enhanced living experiences. The competitive landscape is shaped by companies' ability to offer technologically advanced and sustainable products that meet the evolving needs of the market.

Key Drivers of Qatar Residential Real Estate Industry Growth

Several factors contribute to the growth of the Qatar residential real estate industry. Government initiatives promoting affordable housing and infrastructure development are key catalysts. A growing population and a strong economy further fuel demand. Furthermore, technological advancements such as the use of smart home technologies and improved construction methods contribute to increased efficiency and productivity, impacting market growth positively.

Challenges in the Qatar Residential Real Estate Industry Market

Despite the positive outlook, the Qatar residential real estate industry faces challenges, including the high cost of construction materials and labor, and sometimes stringent regulations. The existing supply chain constraints can impact project timelines and costs. Competition among developers and fluctuating market demand pose additional challenges. These factors necessitate careful planning and risk management for businesses operating in the sector.

Emerging Opportunities in Qatar Residential Real Estate Industry

The Qatar residential real estate market presents significant long-term opportunities. Government investments in infrastructure and sustainable development initiatives present considerable potential. Strategic partnerships between local and international developers can create access to advanced technologies and best practices. The market expansion into new areas, incorporating innovative and sustainable designs, can bring new opportunities for growth and profitability.

Leading Players in the Qatar Residential Real Estate Industry Sector

- Barwa Real Estate

- First Qatar Real Estate Development Co

- Al Mana Real Estate

- Ariane Real Estate

- Zukhrof Real Estate

- Mazaya Real Estate Development

- United Development Company

- Les Roses Real Estate

- Qatari Diar Real Estate Company

- Mirage International Property Consultants

- Ezdan Holding Group

- Al Asmakh Real Estate

Key Milestones in Qatar Residential Real Estate Industry Industry

- 2022 (November): Completion of major infrastructure projects related to the FIFA World Cup, boosting the demand for residential properties.

- 2023 (Ongoing): Launch of several new residential developments focusing on sustainable building practices and smart home technologies.

- 2024 (Q1): Introduction of new government regulations aimed at promoting affordable housing and protecting consumer rights.

Strategic Outlook for Qatar Residential Real Estate Industry Market

The Qatar residential real estate market is poised for continued growth, driven by sustained economic growth, infrastructure development, and population increase. Companies that embrace technological innovation, sustainable practices, and strategic partnerships are best positioned to capture market share. Focusing on developing affordable housing options will become increasingly vital to meet the rising demand in the market.

Qatar Residential Real Estate Industry Segmentation

-

1. Type

- 1.1. Apartments & Condominiums

- 1.2. Villas & Landed Houses

Qatar Residential Real Estate Industry Segmentation By Geography

- 1. Qatar

Qatar Residential Real Estate Industry Regional Market Share

Geographic Coverage of Qatar Residential Real Estate Industry

Qatar Residential Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.46% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Apartments & Condominiums

- 5.1.2. Villas & Landed Houses

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Qatar

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Qatar Residential Real Estate Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Apartments & Condominiums

- 6.1.2. Villas & Landed Houses

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Barwa Real Estate

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 First Qatar Real Estate Development Co

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Al Mana Real Estate

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Ariane Real Estate

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Zukhrof Real Estate

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Mazaya Real Estate Development

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 United Development Company

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Les Roses Real Estate

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Qatari Diar Real Estate Company

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Mirage International Property Consultants**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Ezdan Holding Group

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Al Asmakh Real Estate

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Barwa Real Estate

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Qatar Residential Real Estate Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Qatar Residential Real Estate Industry Share (%) by Company 2025

List of Tables

- Table 1: Qatar Residential Real Estate Industry Revenue million Forecast, by Type 2020 & 2033

- Table 2: Qatar Residential Real Estate Industry Revenue million Forecast, by Region 2020 & 2033

- Table 3: Qatar Residential Real Estate Industry Revenue million Forecast, by Type 2020 & 2033

- Table 4: Qatar Residential Real Estate Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Qatar Residential Real Estate Industry?

The projected CAGR is approximately 7.46%.

2. Which companies are prominent players in the Qatar Residential Real Estate Industry?

Key companies in the market include Barwa Real Estate, First Qatar Real Estate Development Co, Al Mana Real Estate, Ariane Real Estate, Zukhrof Real Estate, Mazaya Real Estate Development, United Development Company, Les Roses Real Estate, Qatari Diar Real Estate Company, Mirage International Property Consultants**List Not Exhaustive, Ezdan Holding Group, Al Asmakh Real Estate.

3. What are the main segments of the Qatar Residential Real Estate Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 7831.75 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Rapid Urabanization4.; Increasing government investments.

6. What are the notable trends driving market growth?

Qatar’s Housing Market is Gradually Improving.

7. Are there any restraints impacting market growth?

4.; Increasing cost of raw materials affecting the construction industry4.; Slowdown in economic growth affecting the market.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Qatar Residential Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Qatar Residential Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Qatar Residential Real Estate Industry?

To stay informed about further developments, trends, and reports in the Qatar Residential Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence