Key Insights

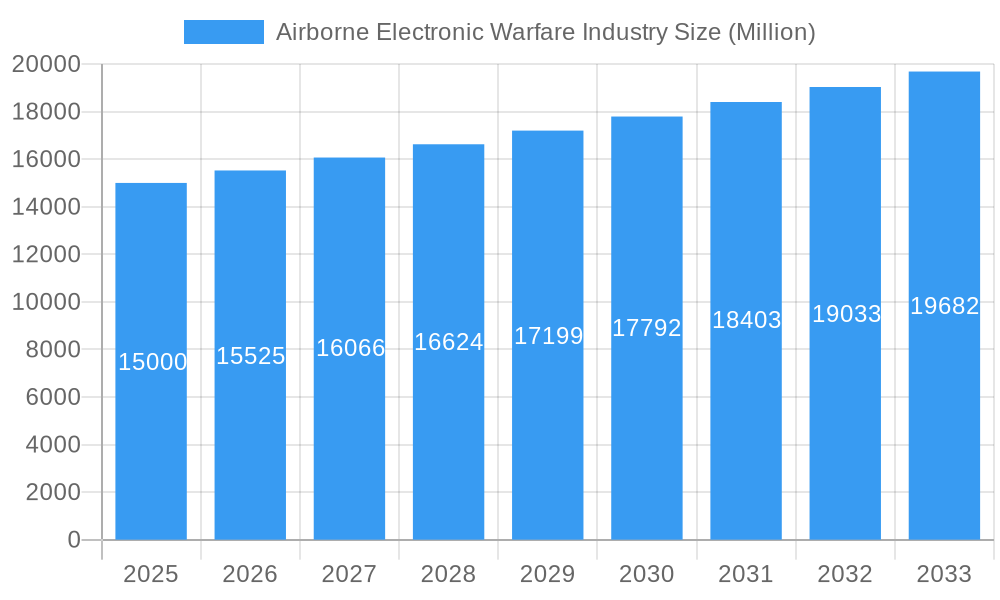

The global Airborne Electronic Warfare (AEW) market is poised for significant expansion, propelled by heightened geopolitical instability and the escalating demand for sophisticated defense capabilities. The market, currently valued at $5.69 billion as of the base year 2025, is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.63% through 2033. Key growth drivers include the modernization of military aviation fleets, the advancement of electronic attack and protection technologies, and the increasing integration of Unmanned Aircraft Systems (UAS) in defense operations. Substantial investments in research and development across North America, Europe, and the Asia-Pacific are further accelerating market growth.

Airborne Electronic Warfare Industry Market Size (In Billion)

The electronic attack segment is anticipated to lead market share due to its crucial role in neutralizing adversarial electronic systems. While manned aircraft currently represent a larger market segment than unmanned systems, reflecting established infrastructure, the unmanned segment is expected to exhibit superior growth rates, driven by advancements in autonomy and cost-effectiveness.

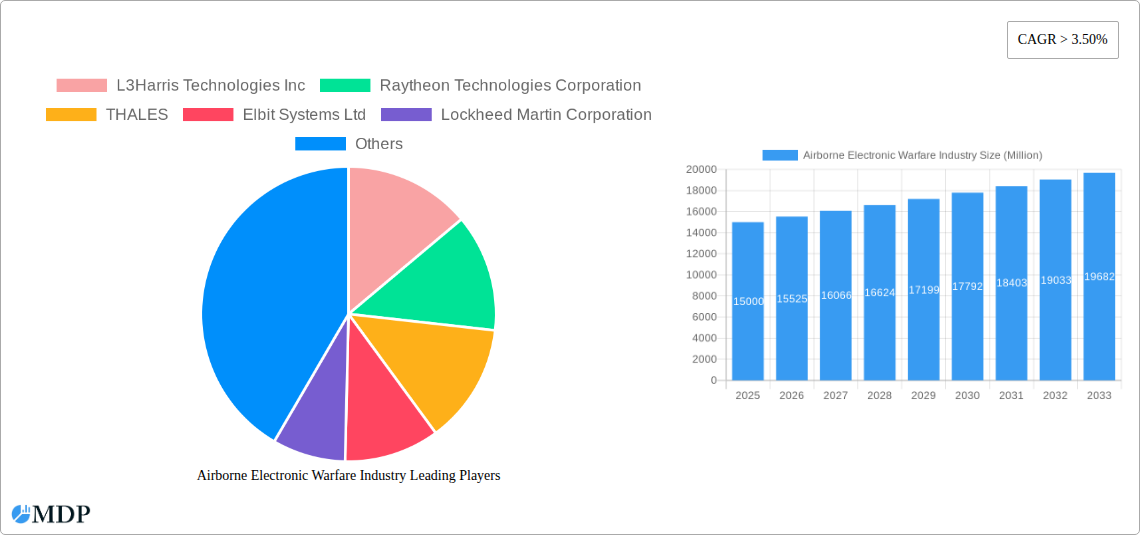

Airborne Electronic Warfare Industry Company Market Share

A competitive landscape analysis reveals that established industry leaders such as L3Harris, Raytheon, Thales, and Lockheed Martin command significant market positions, leveraging their extensive experience and technological expertise. However, emerging companies are actively contributing to market innovation and fostering a dynamic competitive environment.

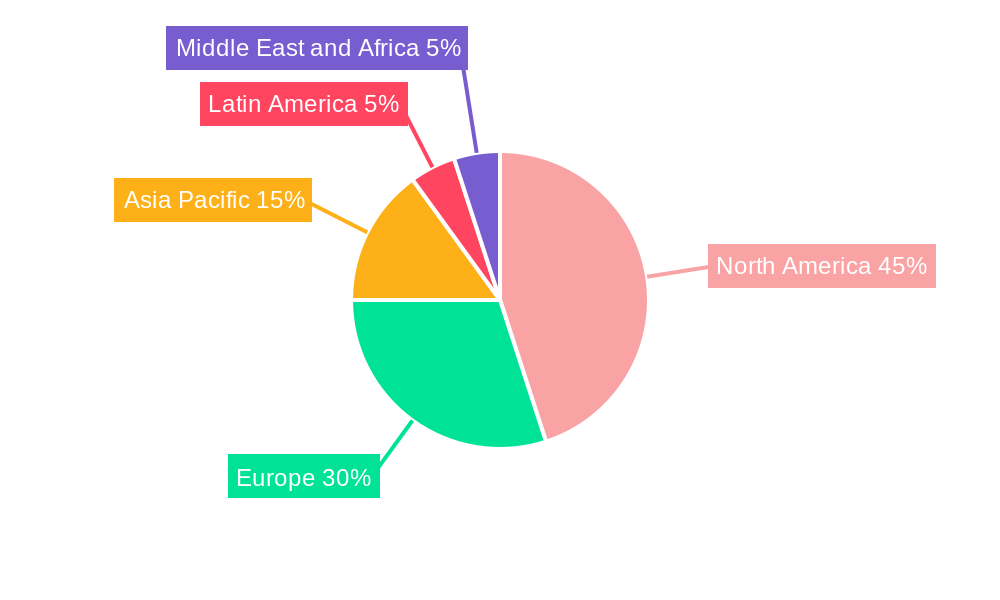

Despite a favorable growth outlook, several factors may present challenges to market progress. These include the substantial costs associated with developing and deploying advanced AEW systems, the complexities of integrating these systems into existing military platforms, and potential regulatory considerations surrounding electronic warfare technologies. Furthermore, the continuous evolution of countermeasures against current AEW capabilities poses a challenge to sustained growth. Nevertheless, ongoing global military modernization initiatives are expected to largely mitigate these constraints, ensuring consistent market expansion throughout the forecast period. Geographically, North America and Europe are projected to maintain market dominance, supported by robust defense budgets and advanced technological infrastructure. The Asia-Pacific region is anticipated to experience substantial growth, fueled by increasing defense expenditures in key nations such as China and India.

Airborne Electronic Warfare Industry Report: 2019-2033 Forecast

Dive deep into the dynamic Airborne Electronic Warfare (AEW) industry with this comprehensive report, offering invaluable insights for strategic decision-making. This in-depth analysis covers the period from 2019 to 2033, with a focus on 2025, providing a detailed overview of market dynamics, leading players, technological advancements, and future growth potential. The report projects a market valued at xx Million by 2033, showcasing significant opportunities for investment and expansion. This report is crucial for industry stakeholders, investors, and researchers seeking a thorough understanding of this critical sector.

Airborne Electronic Warfare Industry Market Dynamics & Concentration

The Airborne Electronic Warfare (AEW) market, valued at xx Million in 2025, exhibits a moderately concentrated landscape dominated by a handful of major players. These key players leverage extensive R&D capabilities, established supply chains, and strategic partnerships to maintain their market dominance. Market share is largely determined by technological innovation, successful contract wins, and a proven track record in delivering robust and reliable systems. The industry is characterized by significant M&A activity, further consolidating market power. Over the study period (2019-2024), approximately xx M&A deals were recorded, reflecting the intense competition and pursuit of technological leadership.

- Market Concentration: High, with top 5 players holding approximately xx% of the market share in 2025.

- Innovation Drivers: Demand for advanced electronic warfare capabilities, ongoing technological advancements in sensor technology, AI, and software-defined systems.

- Regulatory Frameworks: Stringent government regulations and export controls influence market growth and technology adoption.

- Product Substitutes: Limited substitutes exist, given the specialized nature of AEW systems.

- End-User Trends: Increasing demand for sophisticated AEW systems from both military and civilian sectors (e.g., cybersecurity).

- M&A Activities: High level of mergers and acquisitions to acquire technology and expand market reach.

Airborne Electronic Warfare Industry Industry Trends & Analysis

The global Airborne Electronic Warfare (AEW) market is projected to experience robust growth, with a CAGR of xx% from 2025 to 2033. This growth is fueled by several key factors. The increasing geopolitical instability and the need for advanced defense systems are driving significant investments in AEW technology. Technological disruptions, such as the integration of Artificial Intelligence (AI) and machine learning algorithms in EW systems, are enhancing their effectiveness and capabilities, creating a positive feedback loop for growth. Market penetration of advanced AEW systems in both manned and unmanned platforms continues to grow steadily. Competitive dynamics are marked by continuous innovation, strategic partnerships, and a focus on providing customized solutions to meet evolving customer needs.

Leading Markets & Segments in Airborne Electronic Warfare Industry

The North American region holds a dominant position in the AEW market, driven by significant defense budgets and robust technological capabilities. Within the segment breakdown:

Type: The Manned Aircraft segment dominates the market due to its established presence and integration in existing defense platforms. However, the Unmanned Aircraft segment is witnessing significant growth due to the increasing adoption of UAVs across various applications.

Capability: Electronic Attack systems command the largest market share due to their offensive capabilities, followed by Electronic Protection and Electronic Support systems.

Key Drivers for North American Dominance:

- Large defense budgets and strong government support.

- Presence of major AEW system manufacturers and technological innovation hubs.

- Robust aerospace and defense ecosystem.

Detailed Dominance Analysis: North America's dominance stems from the presence of major players, strong R&D capabilities, and sustained investments in AEW technology. The region's superior technological capabilities and integration within existing military architectures contribute significantly to its leading position.

Airborne Electronic Warfare Industry Product Developments

Recent product developments highlight a trend towards modular, software-defined AEW systems, enabling rapid upgrades and customization to meet evolving threat landscapes. This enhances flexibility and reduces life cycle costs. Examples include BAE Systems' Storm electronic warfare modules, which offer customized offensive and defensive capabilities. The focus is shifting towards improved situational awareness, survivability, and increased electromagnetic capabilities to address the complexities of modern warfare. These advancements ensure a strong market fit and enhance the competitive edge of system providers.

Key Drivers of Airborne Electronic Warfare Industry Growth

Several key factors propel the growth of the AEW market:

- Technological Advancements: AI integration, advanced sensor technologies, and software-defined systems enhance system effectiveness and adaptability.

- Geopolitical Instability: Rising global tensions and conflicts necessitate increased investment in defense and security technologies, including AEW systems.

- Government Regulations: Government mandates and regulations, particularly those related to cybersecurity and network defense, drive demand for sophisticated AEW systems.

Challenges in the Airborne Electronic Warfare Industry Market

The AEW market faces various challenges:

- Regulatory Hurdles: Complex export controls and stringent regulatory approvals can slow down product deployment and market expansion.

- Supply Chain Issues: Disruptions in the global supply chain can impact production schedules and overall costs.

- Competitive Pressures: Intense competition among major players necessitates continuous innovation and cost optimization to maintain market share.

Emerging Opportunities in Airborne Electronic Warfare Industry

Significant opportunities exist for growth in the AEW market:

- Technological breakthroughs, such as advanced AI algorithms and miniaturized components, will enhance system capabilities and create new applications.

- Strategic partnerships between technology providers and defense organizations foster innovation and accelerate product development.

- Market expansion into emerging economies, where there's growing demand for advanced defense technologies, presents significant growth potential.

Leading Players in the Airborne Electronic Warfare Industry Sector

- L3Harris Technologies Inc

- Raytheon Technologies Corporation

- THALES

- Elbit Systems Ltd

- Lockheed Martin Corporation

- Terma Grou

- ASELSAN AS

- Israel Aerospace Industries Ltd

- Leonardo S p A

- BAE Systems plc

- Northrop Grumman Corporation

- Saab AB

Key Milestones in Airborne Electronic Warfare Industry Industry

- March 2022: BAE Systems plc launched its Storm electronic warfare modules, introducing customizable offensive and defensive capabilities and accelerating the delivery of software-based electronic warfare capabilities. This launch significantly impacts market dynamics by offering a flexible and adaptable solution.

- November 2021: Lockheed Martin Corporation received a USD 585 Million contract to develop new ASQ-239 electronic warfare/countermeasure hardware for the F-35 aircraft program. This substantial investment signifies the ongoing need for advanced AEW technology and drives market growth.

Strategic Outlook for Airborne Electronic Warfare Industry Market

The AEW market is poised for sustained growth, driven by continuous technological innovation, increasing geopolitical instability, and significant investments in defense modernization. Strategic opportunities lie in developing cutting-edge AEW systems that leverage AI, advanced sensors, and software-defined architectures. Partnerships and collaborations will play a critical role in accelerating innovation and expanding market reach. Focus on delivering cost-effective, adaptable, and highly reliable systems will be essential for success in this competitive landscape.

Airborne Electronic Warfare Industry Segmentation

-

1. Capability

- 1.1. Electronic Attack

- 1.2. Electronic Protection

- 1.3. Electronic Support

-

2. Type

- 2.1. Manned Aircraft

- 2.2. Unmanned Aircraft

Airborne Electronic Warfare Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Russia

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Latin America

- 4.1. Mexico

- 4.2. Brazil

- 4.3. Rest of Latin America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. United Arab Emirates

- 5.3. Israel

- 5.4. Rest of Middle East and Africa

Airborne Electronic Warfare Industry Regional Market Share

Geographic Coverage of Airborne Electronic Warfare Industry

Airborne Electronic Warfare Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increase in Internet of Things (IoT) and Autonomous Systems; Rise in Demand for Military and Defense Satellite Communication Solutions

- 3.3. Market Restrains

- 3.3.1. Cybersecurity Threats to Satellite Communication; Interference in Transmission of Data

- 3.4. Market Trends

- 3.4.1. Unmanned Aircraft Segment to Witness Rapid Growth During the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Airborne Electronic Warfare Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Capability

- 5.1.1. Electronic Attack

- 5.1.2. Electronic Protection

- 5.1.3. Electronic Support

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Manned Aircraft

- 5.2.2. Unmanned Aircraft

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Capability

- 6. North America Airborne Electronic Warfare Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Capability

- 6.1.1. Electronic Attack

- 6.1.2. Electronic Protection

- 6.1.3. Electronic Support

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Manned Aircraft

- 6.2.2. Unmanned Aircraft

- 6.1. Market Analysis, Insights and Forecast - by Capability

- 7. Europe Airborne Electronic Warfare Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Capability

- 7.1.1. Electronic Attack

- 7.1.2. Electronic Protection

- 7.1.3. Electronic Support

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Manned Aircraft

- 7.2.2. Unmanned Aircraft

- 7.1. Market Analysis, Insights and Forecast - by Capability

- 8. Asia Pacific Airborne Electronic Warfare Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Capability

- 8.1.1. Electronic Attack

- 8.1.2. Electronic Protection

- 8.1.3. Electronic Support

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Manned Aircraft

- 8.2.2. Unmanned Aircraft

- 8.1. Market Analysis, Insights and Forecast - by Capability

- 9. Latin America Airborne Electronic Warfare Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Capability

- 9.1.1. Electronic Attack

- 9.1.2. Electronic Protection

- 9.1.3. Electronic Support

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Manned Aircraft

- 9.2.2. Unmanned Aircraft

- 9.1. Market Analysis, Insights and Forecast - by Capability

- 10. Middle East and Africa Airborne Electronic Warfare Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Capability

- 10.1.1. Electronic Attack

- 10.1.2. Electronic Protection

- 10.1.3. Electronic Support

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Manned Aircraft

- 10.2.2. Unmanned Aircraft

- 10.1. Market Analysis, Insights and Forecast - by Capability

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 L3Harris Technologies Inc

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Raytheon Technologies Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 THALES

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Elbit Systems Ltd

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Lockheed Martin Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Terma Grou

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 ASELSAN AS

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Israel Aerospace Industries Ltd

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Leonardo S p A

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 BAE Systems plc

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Northrop Grumman Corporation

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Saab AB

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 L3Harris Technologies Inc

List of Figures

- Figure 1: Global Airborne Electronic Warfare Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Airborne Electronic Warfare Industry Revenue (billion), by Capability 2025 & 2033

- Figure 3: North America Airborne Electronic Warfare Industry Revenue Share (%), by Capability 2025 & 2033

- Figure 4: North America Airborne Electronic Warfare Industry Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Airborne Electronic Warfare Industry Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Airborne Electronic Warfare Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Airborne Electronic Warfare Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Airborne Electronic Warfare Industry Revenue (billion), by Capability 2025 & 2033

- Figure 9: Europe Airborne Electronic Warfare Industry Revenue Share (%), by Capability 2025 & 2033

- Figure 10: Europe Airborne Electronic Warfare Industry Revenue (billion), by Type 2025 & 2033

- Figure 11: Europe Airborne Electronic Warfare Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Europe Airborne Electronic Warfare Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Airborne Electronic Warfare Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Airborne Electronic Warfare Industry Revenue (billion), by Capability 2025 & 2033

- Figure 15: Asia Pacific Airborne Electronic Warfare Industry Revenue Share (%), by Capability 2025 & 2033

- Figure 16: Asia Pacific Airborne Electronic Warfare Industry Revenue (billion), by Type 2025 & 2033

- Figure 17: Asia Pacific Airborne Electronic Warfare Industry Revenue Share (%), by Type 2025 & 2033

- Figure 18: Asia Pacific Airborne Electronic Warfare Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Airborne Electronic Warfare Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Airborne Electronic Warfare Industry Revenue (billion), by Capability 2025 & 2033

- Figure 21: Latin America Airborne Electronic Warfare Industry Revenue Share (%), by Capability 2025 & 2033

- Figure 22: Latin America Airborne Electronic Warfare Industry Revenue (billion), by Type 2025 & 2033

- Figure 23: Latin America Airborne Electronic Warfare Industry Revenue Share (%), by Type 2025 & 2033

- Figure 24: Latin America Airborne Electronic Warfare Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America Airborne Electronic Warfare Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Airborne Electronic Warfare Industry Revenue (billion), by Capability 2025 & 2033

- Figure 27: Middle East and Africa Airborne Electronic Warfare Industry Revenue Share (%), by Capability 2025 & 2033

- Figure 28: Middle East and Africa Airborne Electronic Warfare Industry Revenue (billion), by Type 2025 & 2033

- Figure 29: Middle East and Africa Airborne Electronic Warfare Industry Revenue Share (%), by Type 2025 & 2033

- Figure 30: Middle East and Africa Airborne Electronic Warfare Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Airborne Electronic Warfare Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Capability 2020 & 2033

- Table 2: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Capability 2020 & 2033

- Table 5: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Capability 2020 & 2033

- Table 10: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Germany Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: France Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Russia Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Rest of Europe Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Capability 2020 & 2033

- Table 18: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 19: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: China Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Japan Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: India Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: South Korea Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Rest of Asia Pacific Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Capability 2020 & 2033

- Table 26: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 27: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 28: Mexico Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Brazil Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of Latin America Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Capability 2020 & 2033

- Table 32: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 33: Global Airborne Electronic Warfare Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: Saudi Arabia Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: United Arab Emirates Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Israel Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East and Africa Airborne Electronic Warfare Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Airborne Electronic Warfare Industry?

The projected CAGR is approximately 7.63%.

2. Which companies are prominent players in the Airborne Electronic Warfare Industry?

Key companies in the market include L3Harris Technologies Inc, Raytheon Technologies Corporation, THALES, Elbit Systems Ltd, Lockheed Martin Corporation, Terma Grou, ASELSAN AS, Israel Aerospace Industries Ltd, Leonardo S p A, BAE Systems plc, Northrop Grumman Corporation, Saab AB.

3. What are the main segments of the Airborne Electronic Warfare Industry?

The market segments include Capability, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.69 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in Internet of Things (IoT) and Autonomous Systems; Rise in Demand for Military and Defense Satellite Communication Solutions.

6. What are the notable trends driving market growth?

Unmanned Aircraft Segment to Witness Rapid Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

Cybersecurity Threats to Satellite Communication; Interference in Transmission of Data.

8. Can you provide examples of recent developments in the market?

March 2022: BAE Systems plc launched its versatile Storm electronic warfare modules designed to provide customized, state-of-the-art offensive and defense electronic warfare mission systems for combat platforms for the broader United States and allied fleets. Storm electronic warfare modules use a proven common core architecture to accelerate the delivery of software-based electronic warfare capabilities, providing warfighters with the situational awareness, survivability, and electromagnetic capabilities needed for today's complex missions.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Airborne Electronic Warfare Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Airborne Electronic Warfare Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Airborne Electronic Warfare Industry?

To stay informed about further developments, trends, and reports in the Airborne Electronic Warfare Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence