Key Insights

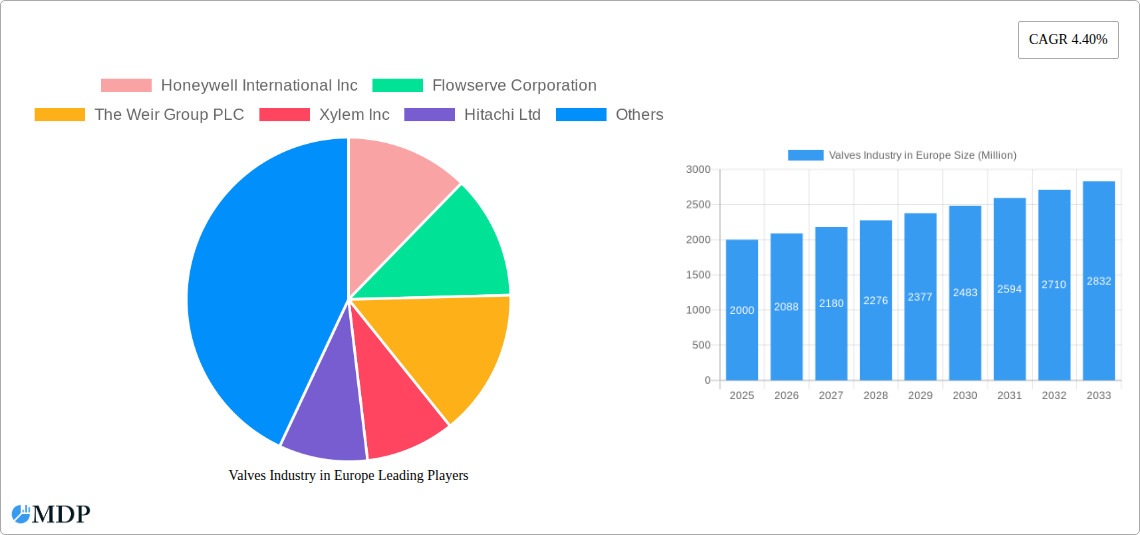

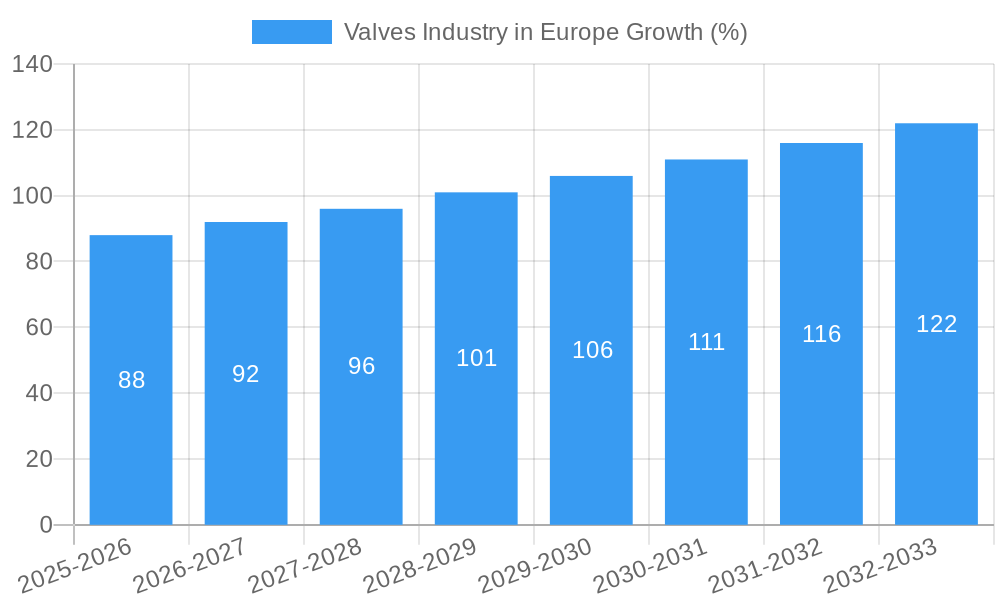

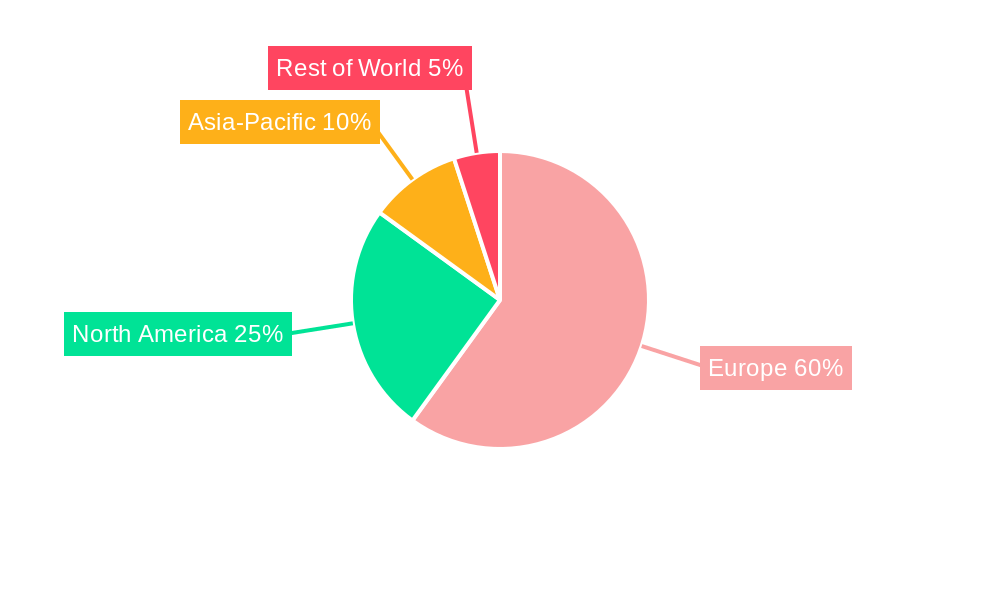

The European valves market, valued at approximately €[Estimate based on market size XX and assuming XX represents a global market size, and deriving a European market share based on regional data, e.g., 20% of XX] million in 2025, is projected to experience robust growth, driven by a Compound Annual Growth Rate (CAGR) of 4.40% from 2025 to 2033. This expansion is fueled by several key factors. The increasing demand for efficient and reliable valve solutions across various end-use industries, including oil & gas, chemicals, water & wastewater treatment, and power generation, is a primary driver. Furthermore, stringent environmental regulations promoting sustainable practices and reducing emissions are pushing for the adoption of advanced valve technologies with improved energy efficiency and reduced leakage. Growth in renewable energy projects also contributes significantly. Germany, France, and the United Kingdom represent the largest national markets within Europe, benefitting from established industrial bases and substantial investments in infrastructure development. However, economic fluctuations and potential supply chain disruptions pose challenges to sustained growth.

The market segmentation reveals significant opportunities. Ball valves are likely to remain the dominant type, driven by their versatility and cost-effectiveness. However, increasing demand for specialized applications in challenging environments is boosting the growth of butterfly, gate/globe/check, and control valves. The oil & gas sector is expected to be a key driver, although fluctuations in energy prices could impact investment. The water & wastewater treatment sector presents a promising avenue for growth given the global emphasis on water management and infrastructure upgrades. Competitive dynamics are shaped by major players like Honeywell, Flowserve, Weir Group, Xylem, and Emerson Electric, who are constantly innovating and expanding their product portfolios to meet evolving market demands. Smaller, specialized players focus on niche segments and regions, contributing to market diversity. Future growth will likely be driven by technological advancements in smart valves, improved materials for extreme conditions, and increased adoption of digitalization and predictive maintenance strategies to optimize operational efficiency and minimize downtime.

Valves Industry in Europe: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the European valves industry, offering invaluable insights for stakeholders across the value chain. From market dynamics and leading players to emerging trends and future opportunities, this report is essential for strategic decision-making. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The report leverages extensive data analysis to predict a xx Million market value in 2025.

Valves Industry in Europe Market Dynamics & Concentration

The European valves market is characterized by a moderate level of concentration, with several multinational corporations holding significant market share. The market share of the top 5 players is estimated to be around xx%. Innovation in materials, design, and automation drives market growth, while stringent environmental regulations and safety standards influence product development. The industry witnesses frequent mergers and acquisitions (M&A) activities, with an estimated xx M&A deals recorded between 2019 and 2024. Product substitution, primarily from more energy-efficient and smart valve technologies, presents both challenges and opportunities. End-user trends toward automation and digitalization are reshaping the industry landscape.

- Market Concentration: Top 5 players hold approximately xx% market share in 2025.

- Innovation Drivers: Material advancements, automation, and smart valve technologies.

- Regulatory Framework: Stringent environmental and safety regulations.

- Product Substitutes: Energy-efficient and smart valve technologies.

- End-User Trends: Increased automation and digitalization in various end-user industries.

- M&A Activities: xx M&A deals recorded between 2019 and 2024.

Valves Industry in Europe Industry Trends & Analysis

The European valves market is poised for steady growth, driven by factors such as increasing infrastructure development, particularly in water and wastewater management, and the expansion of the oil & gas and chemical industries. Technological disruptions, such as the adoption of smart valves and IoT-enabled solutions, are transforming industry operations. Consumer preferences are shifting towards energy-efficient and environmentally friendly products. The competitive landscape is dynamic, with established players and new entrants vying for market share. The CAGR for the period 2025-2033 is projected to be xx%. Market penetration of smart valves is expected to reach xx% by 2033.

Leading Markets & Segments in Valves Industry in Europe

The report identifies Germany and the United Kingdom as the leading markets for valves in Europe, driven by robust industrial activity and infrastructure investment. The ball valve segment dominates by type, owing to its versatility and cost-effectiveness. The Oil & Gas and Water & Wastewater sectors are significant end-user industries.

By Type:

- Ball Valves: Leading segment due to versatility and cost-effectiveness.

- Butterfly Valves: Significant market share, driven by applications in water and wastewater.

- Gate/Globe/Check Valves: Steady demand across multiple end-user industries.

- Plug Valves: Niche applications in specialized industries.

- Control Valves: Growing demand due to increased automation in industrial processes.

- Other Types: Includes specialized valves for specific applications.

By End-user Industry:

- Oil & Gas: Significant driver due to ongoing exploration and production activities.

- Chemicals: High demand for specialized valves in chemical processing plants.

- Water & Wastewater: Strong growth driven by investments in water infrastructure.

- Power Generation: Demand for high-pressure and high-temperature valves.

- Mining: Demand for robust and durable valves in harsh operating conditions.

- Other End-user Industries: Includes food and beverage, pharmaceuticals, and other sectors.

By Country:

- Germany: Strong industrial base and significant investment in infrastructure.

- United Kingdom: Significant oil & gas activity and investments in water management.

- France: Growing industrial sector and infrastructure development.

- Rest of Europe: Showcases a diverse range of end-user industries and market dynamics.

Valves Industry in Europe Product Developments

Recent product innovations focus on smart valves integrating IoT technology for remote monitoring and control, enhancing efficiency and reducing maintenance costs. Advances in materials science enable the development of valves capable of withstanding harsh operating conditions, expanding applications in challenging environments. The market is witnessing a surge in the adoption of energy-efficient valve designs, promoting sustainability and lowering operational costs.

Key Drivers of Valves Industry in Europe Growth

The growth of the European valves industry is fueled by several key factors. Technological advancements leading to improved efficiency and reduced maintenance costs are paramount. Increasing government investments in infrastructure projects, particularly in water management and renewable energy, are crucial drivers. Stringent environmental regulations promoting the adoption of sustainable technologies are also significant.

Challenges in the Valves Industry in Europe Market

The European valves industry faces challenges, including supply chain disruptions, impacting production and delivery timelines. Intense competition from both established players and new entrants creates price pressures. Regulatory complexities and compliance costs add to the operational burden. These factors collectively impact profit margins and investment decisions.

Emerging Opportunities in Valves Industry in Europe

The integration of advanced technologies like AI and machine learning in valve design and operation offers significant opportunities for growth. Strategic collaborations among industry players can foster innovation and market expansion. Targeting emerging markets within Europe and expanding into new applications for valve technology presents further opportunities.

Leading Players in the Valves Industry in Europe Sector

- Honeywell International Inc

- Flowserve Corporation

- The Weir Group PLC

- Xylem Inc

- Hitachi Ltd

- Emerson Electric Co

- ITT INC

- AVK Holding A/S

- Danfoss A/S

- Schlumberger Limited

- Pentair PLC

- KITZ Corporation

Key Milestones in Valves Industry in Europe Industry

- April 2022: ITT Inc. acquired Habonim for USD 140 Million, expanding its ball valve offerings and strengthening its position in harsh application markets.

Strategic Outlook for Valves Industry in Europe Market

The European valves market is poised for continued growth driven by technological advancements, infrastructure development, and increasing demand from key end-user industries. Strategic partnerships, focusing on innovation and market expansion, will be crucial for success in this competitive landscape. The potential for growth in smart valves and energy-efficient solutions is significant.

Valves Industry in Europe Segmentation

-

1. Type

- 1.1. Ball

- 1.2. Butterfly

- 1.3. Gate/Globe/Check

- 1.4. Plug

- 1.5. Control

- 1.6. Other Types

-

2. End-user Industry

- 2.1. Oil & Gas

- 2.2. Chemicals

- 2.3. Water & Wastewater

- 2.4. Power Generation

- 2.5. Mining

- 2.6. Other End-user Industries

Valves Industry in Europe Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Russia

- 1.7. Benelux

- 1.8. Nordics

- 1.9. Rest of Europe

Valves Industry in Europe REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.40% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing emphasis on Power and Water & Wastewater in Emerging Markets; Focus of End Users on Environmental Issues and Refurbishment of Aging Infrastructure to Stay Competitive

- 3.3. Market Restrains

- 3.3.1. High Cost of Microplate Systems

- 3.4. Market Trends

- 3.4.1. Control Valves to Hold a Significant Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Ball

- 5.1.2. Butterfly

- 5.1.3. Gate/Globe/Check

- 5.1.4. Plug

- 5.1.5. Control

- 5.1.6. Other Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Oil & Gas

- 5.2.2. Chemicals

- 5.2.3. Water & Wastewater

- 5.2.4. Power Generation

- 5.2.5. Mining

- 5.2.6. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 7. France Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 8. Italy Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Valves Industry in Europe Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Honeywell International Inc

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Flowserve Corporation

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 The Weir Group PLC

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Xylem Inc

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Hitachi Ltd

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Emerson Electric Co

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 ITT INC

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 AVK Holding A/S

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Danfoss A/S

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Schlumberger Limited

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Pentair PLC

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 KITZ Corporation

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.1 Honeywell International Inc

List of Figures

- Figure 1: Valves Industry in Europe Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Valves Industry in Europe Share (%) by Company 2024

List of Tables

- Table 1: Valves Industry in Europe Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Valves Industry in Europe Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Valves Industry in Europe Revenue Million Forecast, by Type 2019 & 2032

- Table 4: Valves Industry in Europe Volume K Unit Forecast, by Type 2019 & 2032

- Table 5: Valves Industry in Europe Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 6: Valves Industry in Europe Volume K Unit Forecast, by End-user Industry 2019 & 2032

- Table 7: Valves Industry in Europe Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Valves Industry in Europe Volume K Unit Forecast, by Region 2019 & 2032

- Table 9: Valves Industry in Europe Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Valves Industry in Europe Volume K Unit Forecast, by Country 2019 & 2032

- Table 11: Germany Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Germany Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 13: France Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: France Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 15: Italy Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Italy Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 17: United Kingdom Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: United Kingdom Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 19: Netherlands Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Netherlands Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 21: Sweden Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Sweden Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 23: Rest of Europe Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Rest of Europe Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 25: Valves Industry in Europe Revenue Million Forecast, by Type 2019 & 2032

- Table 26: Valves Industry in Europe Volume K Unit Forecast, by Type 2019 & 2032

- Table 27: Valves Industry in Europe Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 28: Valves Industry in Europe Volume K Unit Forecast, by End-user Industry 2019 & 2032

- Table 29: Valves Industry in Europe Revenue Million Forecast, by Country 2019 & 2032

- Table 30: Valves Industry in Europe Volume K Unit Forecast, by Country 2019 & 2032

- Table 31: United Kingdom Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: United Kingdom Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 33: Germany Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Germany Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 35: France Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: France Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 37: Italy Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Italy Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 39: Spain Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Spain Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 41: Russia Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Russia Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 43: Benelux Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Benelux Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 45: Nordics Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Nordics Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 47: Rest of Europe Valves Industry in Europe Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Rest of Europe Valves Industry in Europe Volume (K Unit) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Valves Industry in Europe?

The projected CAGR is approximately 4.40%.

2. Which companies are prominent players in the Valves Industry in Europe?

Key companies in the market include Honeywell International Inc, Flowserve Corporation, The Weir Group PLC, Xylem Inc, Hitachi Ltd, Emerson Electric Co, ITT INC, AVK Holding A/S, Danfoss A/S, Schlumberger Limited, Pentair PLC, KITZ Corporation.

3. What are the main segments of the Valves Industry in Europe?

The market segments include Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing emphasis on Power and Water & Wastewater in Emerging Markets; Focus of End Users on Environmental Issues and Refurbishment of Aging Infrastructure to Stay Competitive.

6. What are the notable trends driving market growth?

Control Valves to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

High Cost of Microplate Systems.

8. Can you provide examples of recent developments in the market?

April 2022 - ITT Inc announced that the company had acquired Habonim, a provider of industrial valves and actuators, for USD 140 million. Habonim will become part of ITT's Industrial Process (IP) segment. The company's complementary ball valve offering and focus on harsh applications in attractive end-user markets will drive stronger sales growth for Industrial Process and ITT over the long term.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Valves Industry in Europe," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Valves Industry in Europe report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Valves Industry in Europe?

To stay informed about further developments, trends, and reports in the Valves Industry in Europe, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence