Key Insights

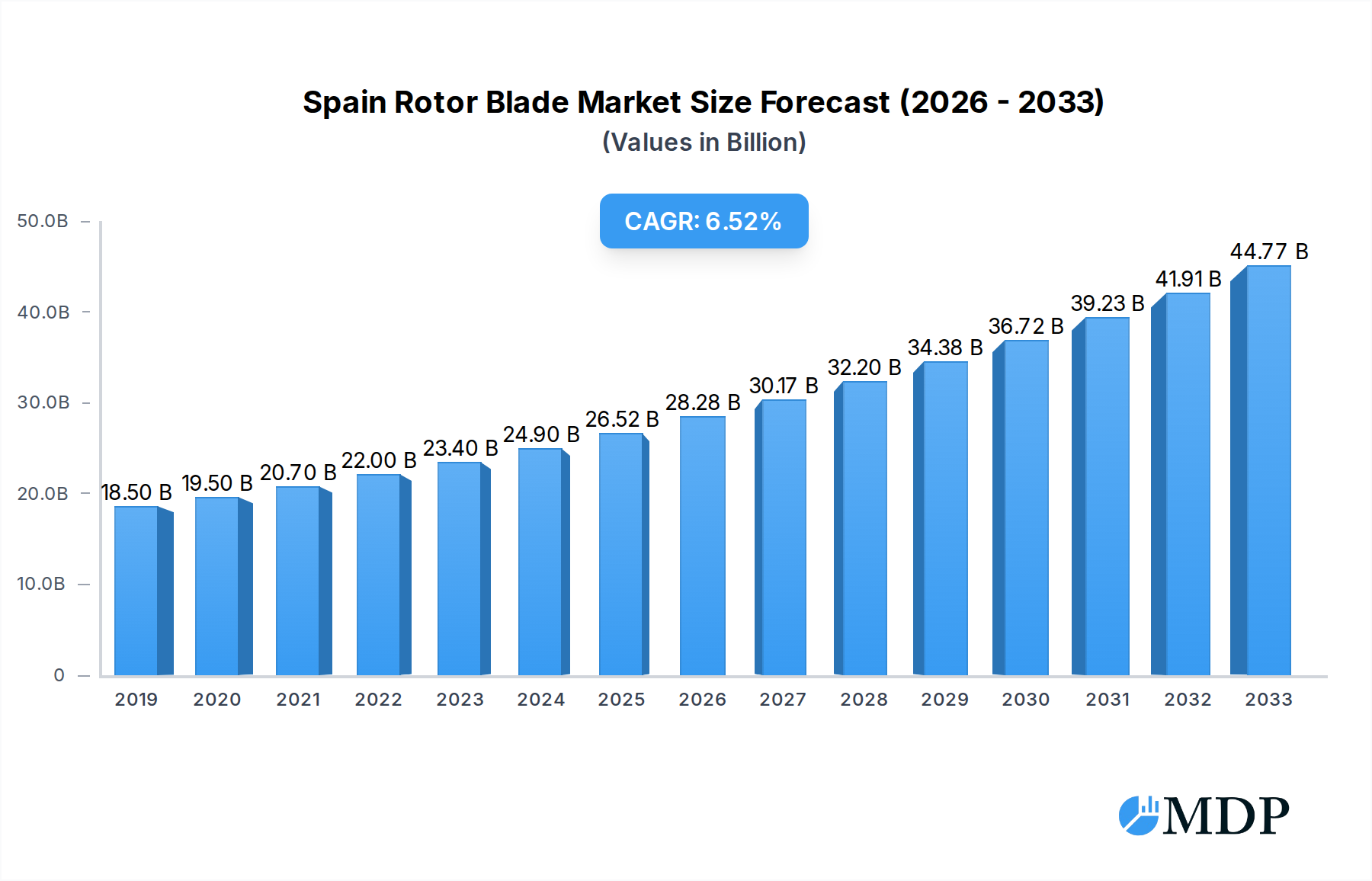

The Spanish Rotor Blade Market is poised for significant expansion, projected to reach €26.52 billion by 2025 and grow at a robust CAGR of 6.9% through 2033. This substantial growth is propelled by Spain's unwavering commitment to renewable energy, particularly wind power, driven by ambitious national targets for decarbonization and energy independence. The increasing adoption of offshore wind projects, supported by favorable government policies and strategic investments, is a key accelerator for the market. Furthermore, technological advancements in blade design and materials, such as the widespread use of lighter and more durable carbon fiber composites, are enhancing turbine efficiency and contributing to market vitality. The ongoing modernization of existing wind farms and the development of new installations across both onshore and offshore locations are creating sustained demand for rotor blades.

Spain Rotor Blade Market Market Size (In Billion)

The market's upward trajectory is further supported by a strong pipeline of wind energy projects and a growing focus on extending the lifespan and performance of wind turbine components. While the market benefits from substantial government incentives and private sector investment in green energy infrastructure, potential challenges include supply chain complexities for specialized materials and the need for skilled labor in blade manufacturing and installation. Nevertheless, the clear strategic direction of Spain towards a renewable energy future, coupled with advancements in wind turbine technology and a growing global imperative to combat climate change, paints a very positive outlook for the Spanish Rotor Blade Market in the coming years. The continuous drive for more efficient and sustainable wind energy solutions ensures a dynamic and evolving landscape for rotor blade manufacturers and suppliers.

Spain Rotor Blade Market Company Market Share

Spain Rotor Blade Market: Comprehensive Analysis and Forecast (2019-2033)

This report provides an in-depth analysis of the Spain Rotor Blade Market, a critical segment within the burgeoning renewable energy sector. With a comprehensive study period spanning from 2019 to 2033, this report offers unparalleled insights into market dynamics, industry trends, and future growth trajectories. Our expert analysis leverages high-traffic keywords such as wind turbine blades Spain, onshore wind blades, offshore wind blades Spain, carbon fiber rotor blades, and Siemens Gamesa blades to maximize search visibility and attract key industry stakeholders.

The report covers the base year of 2025 and provides detailed forecasts for the period 2025–2033, building upon historical data from 2019–2024. We meticulously examine market concentration, innovation drivers, regulatory landscapes, and competitive strategies, offering actionable intelligence for investors, manufacturers, and policymakers alike. The Spain Rotor Blade Market is poised for significant expansion, driven by ambitious renewable energy targets and continuous technological advancements in blade design and manufacturing. Understand the evolving competitive landscape, identify emerging opportunities, and navigate the challenges within this dynamic market.

Spain Rotor Blade Market Market Dynamics & Concentration

The Spain Rotor Blade Market exhibits a moderate to high concentration, primarily driven by the presence of global leaders and specialized domestic manufacturers. Key innovation drivers include the relentless pursuit of enhanced aerodynamic efficiency, lightweight materials, and increased durability to optimize wind energy capture and reduce operational costs. Regulatory frameworks, particularly those set by the European Union and the Spanish government, play a pivotal role in shaping market growth through supportive policies for renewable energy deployment and stringent environmental standards. Product substitutes, while limited in the context of direct rotor blade functionality, can emerge in the form of alternative energy generation technologies that indirectly impact wind power investment. End-user trends are strongly influenced by utility-scale wind farm developers seeking cost-effective and high-performance blade solutions, as well as a growing demand for specialized blades for repowering older wind farms. Merger and acquisition (M&A) activities, though currently at a relatively low volume, are anticipated to increase as larger players seek to consolidate market share and acquire innovative technologies or expand their manufacturing capabilities. With an estimated market share of the top 3 players reaching xx% in 2025, the Spain Rotor Blade Market is characterized by strategic partnerships and a competitive drive for technological supremacy. The M&A deal count for the historical period (2019-2024) stands at xx, indicating a market undergoing consolidation.

Spain Rotor Blade Market Industry Trends & Analysis

The Spain Rotor Blade Market is on a robust growth trajectory, fueled by Spain's ambitious renewable energy targets and the increasing global imperative to decarbonize energy production. The market's expansion is significantly driven by the escalating demand for wind energy, both onshore and offshore, as governments worldwide prioritize sustainable power sources. Technological disruptions are at the forefront of market evolution, with continuous innovation in blade design, materials science, and manufacturing processes. Advancements in composite materials, such as the increasing adoption of carbon fiber for its superior strength-to-weight ratio, are enabling the production of longer, lighter, and more efficient rotor blades. This trend directly contributes to higher energy yields and improved performance of wind turbines, especially in challenging wind conditions. Furthermore, the development of recyclable rotor blades is a transformative trend, aligning the industry with circular economy principles and addressing environmental concerns associated with blade disposal. Consumer preferences, in this context referring to wind farm developers and operators, are shifting towards blades that offer a lower levelized cost of energy (LCOE), enhanced reliability, and reduced maintenance requirements. Competitive dynamics are intensifying, with established global manufacturers vying for market share against emerging players specializing in niche technologies. The market penetration of advanced rotor blade solutions is expected to rise significantly as the cost-effectiveness and performance benefits become more apparent. The compound annual growth rate (CAGR) for the Spain Rotor Blade Market is projected to be xx% from 2025 to 2033, underscoring its substantial growth potential. The market size is estimated to reach $xx billion by 2033, up from an estimated $xx billion in 2025. The growing adoption of larger wind turbines, necessitating longer and more sophisticated rotor blades, is a key factor supporting this expansion. Investment in research and development for next-generation blade technologies, including those designed for higher wind speeds and improved energy capture in low-wind environments, will continue to shape the competitive landscape. The increasing focus on reducing the environmental impact of wind energy infrastructure, particularly concerning the end-of-life management of rotor blades, is spurring innovation in sustainable materials and recycling technologies. This proactive approach to environmental stewardship is not only meeting regulatory demands but also enhancing the public perception and long-term viability of wind power.

Leading Markets & Segments in Spain Rotor Blade Market

The Spain Rotor Blade Market is characterized by significant growth across various deployment locations and material compositions.

Location of Deployment:

- Onshore: The onshore segment currently dominates the Spain Rotor Blade Market. Key drivers for this dominance include:

- Established Infrastructure: Spain has a well-developed onshore wind energy infrastructure, with numerous existing wind farms and readily available sites for new installations.

- Government Support: Favorable government policies and incentives for onshore wind power generation continue to drive investment and deployment.

- Cost-Effectiveness: Onshore wind farms generally offer a lower cost of installation and maintenance compared to offshore projects, making them more attractive for developers.

- Repowering Initiatives: A significant portion of the onshore market growth is attributed to the repowering of older wind farms, where existing turbines are replaced with newer, more efficient models, requiring advanced rotor blades.

- Offshore: While currently smaller than the onshore segment, the offshore rotor blade market in Spain is poised for substantial growth. The primary drivers for this expansion are:

- Ambitious Offshore Wind Targets: Spain has set ambitious targets for offshore wind energy capacity, signaling significant future investment in this sector.

- Technological Advancements: Improvements in offshore turbine technology, including larger turbines and floating foundation solutions, are making offshore wind more viable and economically attractive.

- Resource Potential: Spain possesses considerable offshore wind resource potential, particularly in the Atlantic and Mediterranean coasts, which can support large-scale wind farm development.

- Onshore: The onshore segment currently dominates the Spain Rotor Blade Market. Key drivers for this dominance include:

Blade Material:

- Glass Fiber: Glass fiber remains the most widely used material in rotor blade manufacturing due to its cost-effectiveness, durability, and established manufacturing processes. It continues to be a primary choice for a large portion of the market, particularly for onshore applications where cost optimization is crucial.

- Carbon Fiber: The adoption of carbon fiber is steadily increasing, driven by its superior strength-to-weight ratio. This allows for the production of longer and lighter blades, which are essential for capturing more energy, especially in lower wind speeds and for larger offshore turbines. The technological advancements in carbon fiber manufacturing are making it more accessible and cost-competitive.

- Others: This category includes emerging materials and composite structures, such as hybrid designs incorporating both glass and carbon fiber, as well as advanced resins and manufacturing techniques aimed at improving blade performance, reducing weight, and enhancing recyclability. As the industry pushes for greater efficiency and sustainability, research and development in "other" materials will likely gain prominence.

The dominance of the onshore segment is expected to continue in the short to medium term, but the offshore segment will witness a higher growth rate. The increasing use of carbon fiber and advanced composite materials highlights the market's commitment to innovation and performance enhancement across all deployment types.

Spain Rotor Blade Market Product Developments

Product developments in the Spain Rotor Blade Market are primarily focused on enhancing energy capture efficiency, extending blade lifespan, and improving sustainability. Innovations include the design of longer and more aerodynamically optimized blades, utilizing advanced composite materials like carbon fiber for reduced weight and increased strength. The development of recyclable rotor blades, exemplified by industry-leading initiatives, marks a significant stride towards a circular economy within the wind energy sector. These advancements provide a competitive advantage by offering improved performance, reduced LCOE, and a more environmentally conscious solution, aligning with both regulatory demands and end-user preferences for sustainable and high-performance wind energy components.

Key Drivers of Spain Rotor Blade Market Growth

The growth of the Spain Rotor Blade Market is propelled by several key factors. Foremost among these is the Spanish government's strong commitment to renewable energy targets, which necessitates a significant expansion of wind power capacity. Technological advancements play a crucial role, with continuous innovation in blade design, materials science (such as the increasing use of carbon fiber), and manufacturing processes leading to more efficient and durable rotor blades. The economic viability of wind energy, characterized by decreasing LCOE, makes it an increasingly attractive investment for utilities and independent power producers. Furthermore, supportive regulatory frameworks and incentives for renewable energy deployment create a favorable market environment. The global drive towards decarbonization and climate change mitigation further amplifies the demand for wind energy, consequently driving the need for advanced rotor blades.

Challenges in the Spain Rotor Blade Market Market

Despite its robust growth, the Spain Rotor Blade Market faces several challenges. Supply chain complexities and volatility in raw material prices, particularly for composites like carbon fiber and resins, can impact manufacturing costs and lead times. Logistical hurdles associated with transporting large rotor blades to installation sites, especially in remote or challenging terrains, can also pose significant challenges. Stringent environmental regulations regarding blade disposal and end-of-life management, while driving innovation in recyclability, also present a compliance burden and require substantial investment in new technologies. The intense competition among global and regional manufacturers can exert downward pressure on profit margins. Lastly, intermittency of wind resources and grid integration challenges, though not directly a rotor blade issue, can indirectly affect the pace of wind farm development and, consequently, the demand for rotor blades.

Emerging Opportunities in Spain Rotor Blade Market

The Spain Rotor Blade Market is ripe with emerging opportunities, primarily driven by technological breakthroughs and strategic market expansion. The ongoing development of recyclable and sustainable rotor blade materials presents a significant opportunity to meet growing environmental demands and gain a competitive edge. The growth of offshore wind energy in Spain, with ambitious government targets, opens up a vast new market for specialized offshore rotor blades, including those designed for floating wind platforms. Repowering initiatives for existing wind farms offer continuous demand for advanced rotor blades that can enhance the performance of older installations. Strategic partnerships between blade manufacturers, turbine OEMs, and research institutions can accelerate innovation and market penetration. Furthermore, exploring opportunities in emerging markets within Spain and expanding export capabilities for advanced rotor blade technologies will be crucial for long-term growth.

Leading Players in the Spain Rotor Blade Market Sector

- LM Wind Power

- Vestas Wind Systems A/S

- Suzlon Energy Limited

- Siemens Gamesa Renewable Energy SA

- BayWa R E AG

Key Milestones in Spain Rotor Blade Market Industry

- September 2022: Siemens Gamesa introduced a recyclable rotor blade for onshore wind farms globally, marking a significant step towards a circular economy in wind power.

- 2021: Siemens Gamesa launched its first recyclable rotor blade for offshore wind farms.

- 2020: Significant advancements in composite material research led to the development of lighter and more durable glass fiber and carbon fiber blends for increased blade efficiency.

- 2019: The Spanish government reinforced its commitment to renewable energy, setting higher targets for wind power deployment, which directly influenced rotor blade manufacturing demand.

Strategic Outlook for Spain Rotor Blade Market Market

The strategic outlook for the Spain Rotor Blade Market is exceptionally positive, driven by a confluence of supportive government policies, technological innovation, and increasing global demand for renewable energy. The market is poised for sustained growth, with a strong emphasis on developing and deploying advanced rotor blades that enhance energy capture efficiency and reduce the LCOE. Key growth accelerators include the continued expansion of both onshore and offshore wind farms, the increasing adoption of composite materials like carbon fiber for improved performance, and the critical development of sustainable and recyclable blade solutions. Strategic opportunities lie in forming robust partnerships, investing in R&D for next-generation blade technologies, and capitalizing on the significant potential of the offshore wind sector in Spain. The market is expected to witness further consolidation and technological differentiation as leading players strive to maintain their competitive advantage in this dynamic and essential sector of the renewable energy landscape.

Spain Rotor Blade Market Segmentation

-

1. Location of Deployment

- 1.1. Onshore

- 1.2. Offshore

-

2. Blade Material

- 2.1. Carbon fiber

- 2.2. Glass Fiber

- 2.3. Others

Spain Rotor Blade Market Segmentation By Geography

- 1. Spain

Spain Rotor Blade Market Regional Market Share

Geographic Coverage of Spain Rotor Blade Market

Spain Rotor Blade Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 5.1.1. Onshore

- 5.1.2. Offshore

- 5.2. Market Analysis, Insights and Forecast - by Blade Material

- 5.2.1. Carbon fiber

- 5.2.2. Glass Fiber

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 6. Spain Rotor Blade Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 6.1.1. Onshore

- 6.1.2. Offshore

- 6.2. Market Analysis, Insights and Forecast - by Blade Material

- 6.2.1. Carbon fiber

- 6.2.2. Glass Fiber

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 LM Wind Power

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Vestas Wind Systems A/S

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Suzlon Energy Limited*List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Siemens Gamesa Renewable Energy SA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 BayWa R E AG

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 LM Wind Power

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Spain Rotor Blade Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Spain Rotor Blade Market Share (%) by Company 2025

List of Tables

- Table 1: Spain Rotor Blade Market Revenue billion Forecast, by Location of Deployment 2020 & 2033

- Table 2: Spain Rotor Blade Market Volume K Units Forecast, by Location of Deployment 2020 & 2033

- Table 3: Spain Rotor Blade Market Revenue billion Forecast, by Blade Material 2020 & 2033

- Table 4: Spain Rotor Blade Market Volume K Units Forecast, by Blade Material 2020 & 2033

- Table 5: Spain Rotor Blade Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Spain Rotor Blade Market Volume K Units Forecast, by Region 2020 & 2033

- Table 7: Spain Rotor Blade Market Revenue billion Forecast, by Location of Deployment 2020 & 2033

- Table 8: Spain Rotor Blade Market Volume K Units Forecast, by Location of Deployment 2020 & 2033

- Table 9: Spain Rotor Blade Market Revenue billion Forecast, by Blade Material 2020 & 2033

- Table 10: Spain Rotor Blade Market Volume K Units Forecast, by Blade Material 2020 & 2033

- Table 11: Spain Rotor Blade Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Spain Rotor Blade Market Volume K Units Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Rotor Blade Market?

The projected CAGR is approximately 6.9%.

2. Which companies are prominent players in the Spain Rotor Blade Market?

Key companies in the market include LM Wind Power, Vestas Wind Systems A/S, Suzlon Energy Limited*List Not Exhaustive, Siemens Gamesa Renewable Energy SA, BayWa R E AG.

3. What are the main segments of the Spain Rotor Blade Market?

The market segments include Location of Deployment, Blade Material.

4. Can you provide details about the market size?

The market size is estimated to be USD 26.52 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Demand for Cleaner Energy4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Offshore Segment Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Underdeveloped Power Grid.

8. Can you provide examples of recent developments in the market?

In September 2022, Siemens Gamesa, the German-Spanish Siemens Energy subsidiary, introduced a recyclable rotor blade for the onshore wind farms, at the international level. The launch is an attempt of the company to bring the wind power industry closer to a circular economy. The company already launched the recyclable rotor blade for offshore farms in 2021.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Rotor Blade Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Rotor Blade Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Rotor Blade Market?

To stay informed about further developments, trends, and reports in the Spain Rotor Blade Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence