Key Insights

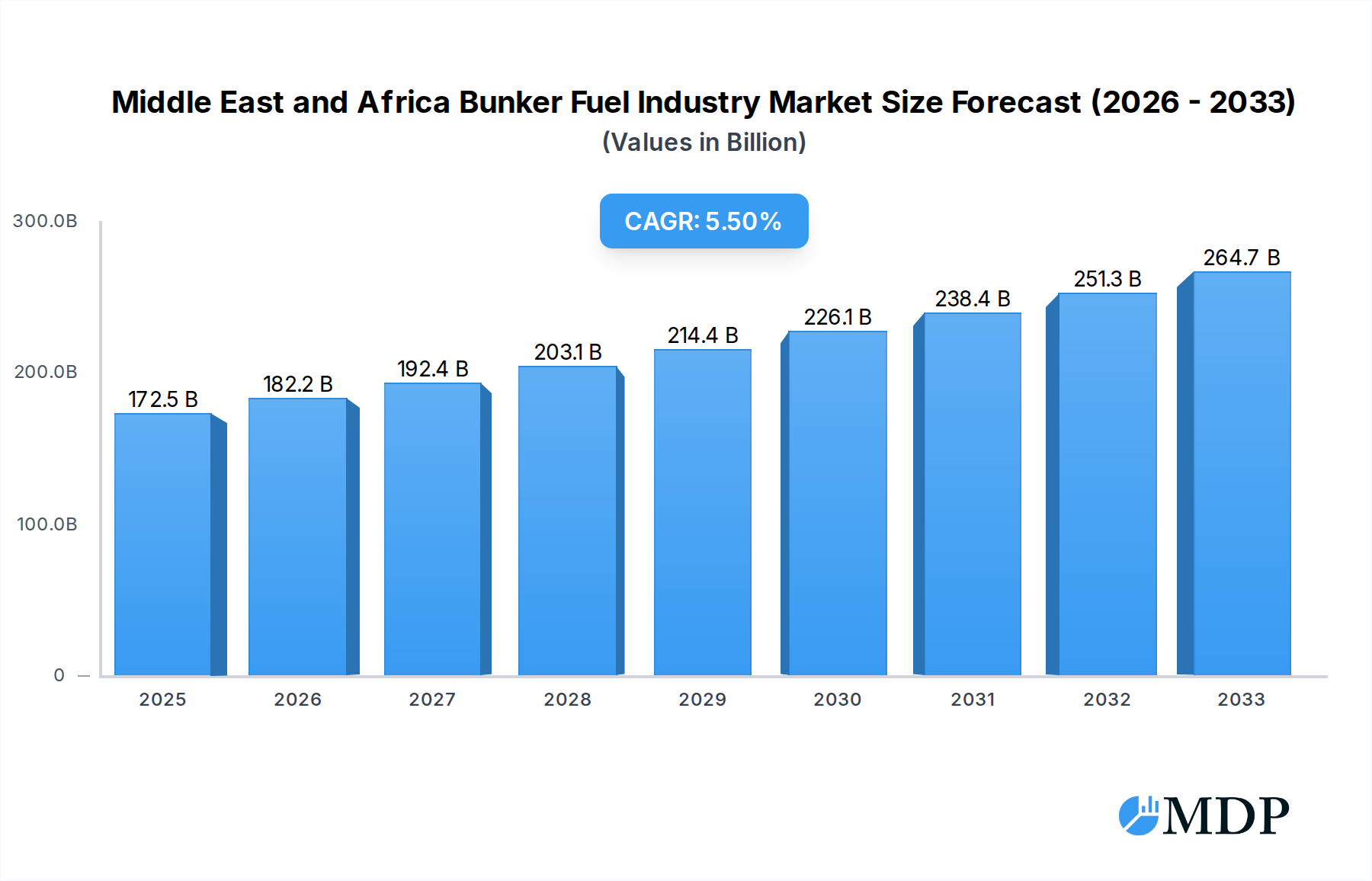

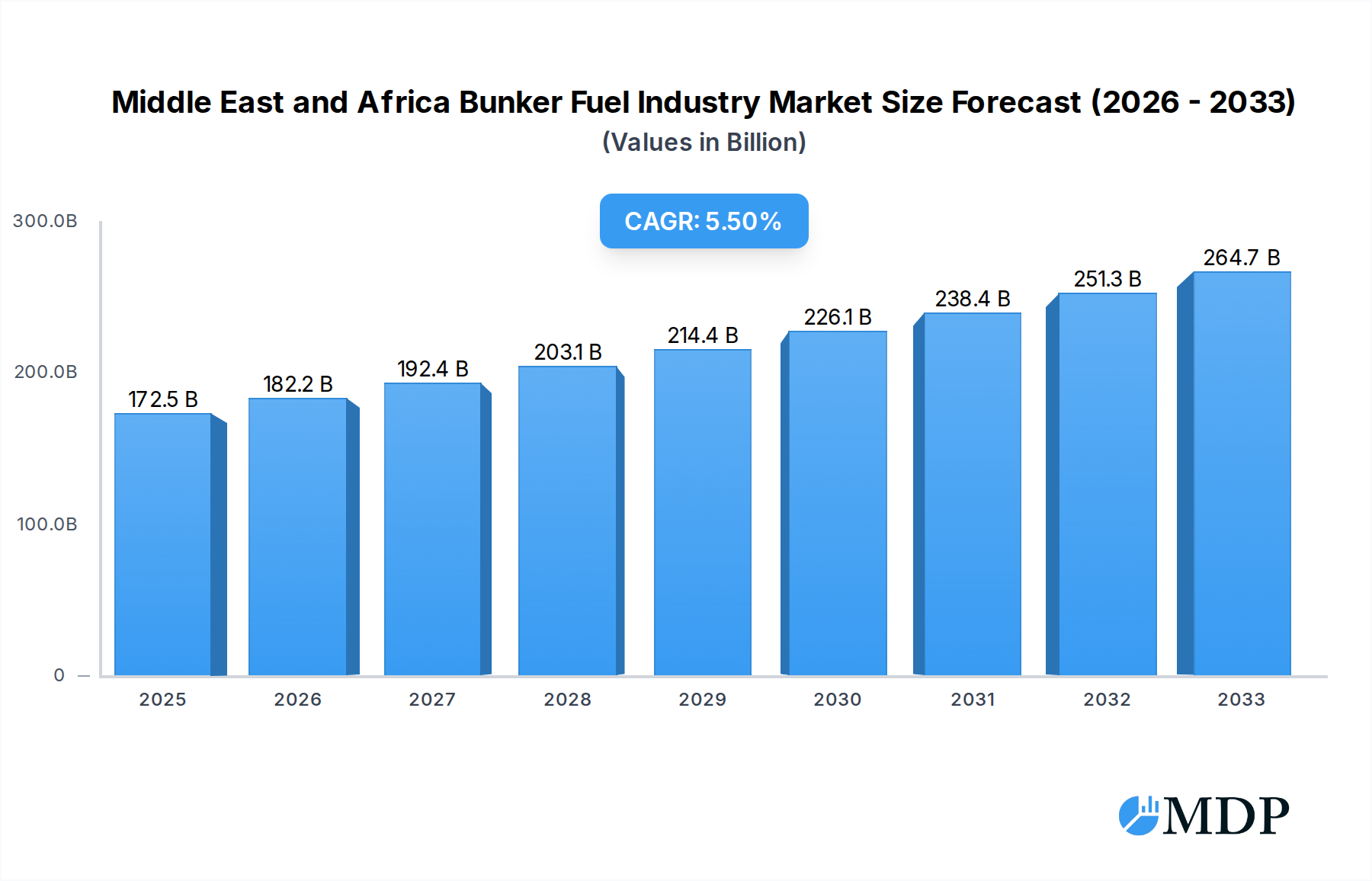

The Middle East and Africa (MEA) Bunker Fuel Industry is poised for significant expansion, projected to reach a market size of $172.5 billion in 2025. This growth is fueled by a robust Compound Annual Growth Rate (CAGR) of 5.6% during the forecast period of 2025-2033. Key drivers for this surge include the increasing maritime trade activities across major shipping lanes in the region, coupled with the growing demand for cleaner fuel alternatives to comply with stricter environmental regulations, particularly the International Maritime Organization's (IMO) sulfur caps. The shift towards Very-Low Sulfur Fuel Oil (VLSFO) and Liquefied Natural Gas (LNG) as preferred bunkering fuels highlights the industry's commitment to sustainability and operational efficiency. Infrastructure development in key bunkering hubs within the UAE, Saudi Arabia, and Nigeria is also a critical enabler of this market expansion, facilitating smoother and more efficient refueling operations for a diverse range of vessel types.

Middle East and Africa Bunker Fuel Industry Market Size (In Billion)

The MEA Bunker Fuel Industry's trajectory is further shaped by emerging trends such as the adoption of digital technologies for optimizing bunkering operations, enhancing supply chain transparency, and improving customer service. While the industry benefits from strong demand, potential restraints include fluctuating crude oil prices, geopolitical instability in certain sub-regions, and the capital-intensive nature of transitioning to alternative fuels. However, the inherent advantages of the MEA region, including its strategic geographical location and growing economies, are expected to outweigh these challenges. The market is segmented across various fuel types, with HSFO, VLSFO, MGO, and LNG representing key segments, and a diverse array of vessel types, including containers, tankers, and bulk carriers, all contributing to the dynamic nature of this industry. Prominent companies like Uniper SE, Shell PLC, and Exxon Mobil Corporation are actively shaping this landscape through strategic investments and service offerings.

Middle East and Africa Bunker Fuel Industry Company Market Share

This comprehensive report offers an in-depth analysis of the Middle East and Africa bunker fuel industry, a critical sector supporting global maritime trade. Covering the period from 2019 to 2033, with a base year of 2025, this study provides unparalleled insights into market dynamics, prevailing trends, leading segments, and future growth trajectories. We delve into the intricacies of fuel types, vessel categories, and geographical hotspots, offering actionable intelligence for stakeholders seeking to navigate this evolving market. Discover key drivers, challenges, emerging opportunities, and the strategic imperatives necessary for success.

Middle East and Africa Bunker Fuel Industry Market Dynamics & Concentration

The Middle East and Africa (MEA) bunker fuel market is characterized by a moderate level of concentration, with a few dominant players holding significant market share, particularly in key oil-producing nations. Innovation is primarily driven by the increasing demand for cleaner fuel alternatives and the push for operational efficiency. Regulatory frameworks, such as IMO 2020 sulfur cap regulations, have profoundly reshaped the market, driving the adoption of Very-Low Sulfur Fuel Oil (VLSFO) and Marine Gas Oil (MGO). Product substitutes like Liquefied Natural Gas (LNG) are gaining traction, albeit with infrastructure limitations. End-user trends highlight a growing preference for reliable supply chains and competitive pricing. Merger and Acquisition (M&A) activities are moderate, often involving strategic partnerships or consolidation of smaller regional players to enhance scale and market reach. For instance, Shell PLC and Exxon Mobil Corporation continue to be major players, while national oil companies like Abu Dhabi National Oil Company (ADNOC) are expanding their refining and bunkering capabilities. The industry is witnessing a gradual shift towards more sustainable practices, influenced by global environmental mandates.

Middle East and Africa Bunker Fuel Industry Industry Trends & Analysis

The Middle East and Africa bunker fuel industry is poised for robust growth, driven by several interconnected trends and analytical insights. A significant growth driver is the increasing volume of global maritime trade, with the MEA region serving as a vital transit hub, particularly through the Suez Canal and key Red Sea and Persian Gulf ports. The CAGR for this sector is estimated to be robust, reflecting increased shipping activity and infrastructure development. Market penetration of cleaner fuels, such as VLSFO and MGO, has accelerated significantly following the IMO 2020 sulfur cap, creating a demand surge for compliant fuels. Conversely, High Sulfur Fuel Oil (HSFO) demand is gradually declining but remains relevant in certain markets with less stringent regulations. The ongoing development of port infrastructure across countries like the United Arab Emirates and Saudi Arabia further enhances the region's attractiveness for bunkering operations, directly contributing to market expansion. Technological disruptions are also playing a crucial role, with advancements in fuel blending technologies and the exploration of alternative marine fuels like LNG and potentially ammonia and methanol for future bunkering needs. Consumer preferences are shifting towards suppliers offering a combination of competitive pricing, guaranteed product quality, and efficient logistics. This is fostering a more dynamic competitive landscape, where established giants like Shell PLC and Chevron Corporation are competing alongside emerging regional players and state-backed enterprises. The push for digitalization in bunkering operations, from order placement to delivery, is also a growing trend aimed at improving efficiency and transparency. The expansion of refining capacities in the MEA region, often supported by significant investments, ensures a stable supply of bunker fuels, further underpinning market growth. The industry's ability to adapt to evolving environmental regulations and technological innovations will be paramount to sustained success.

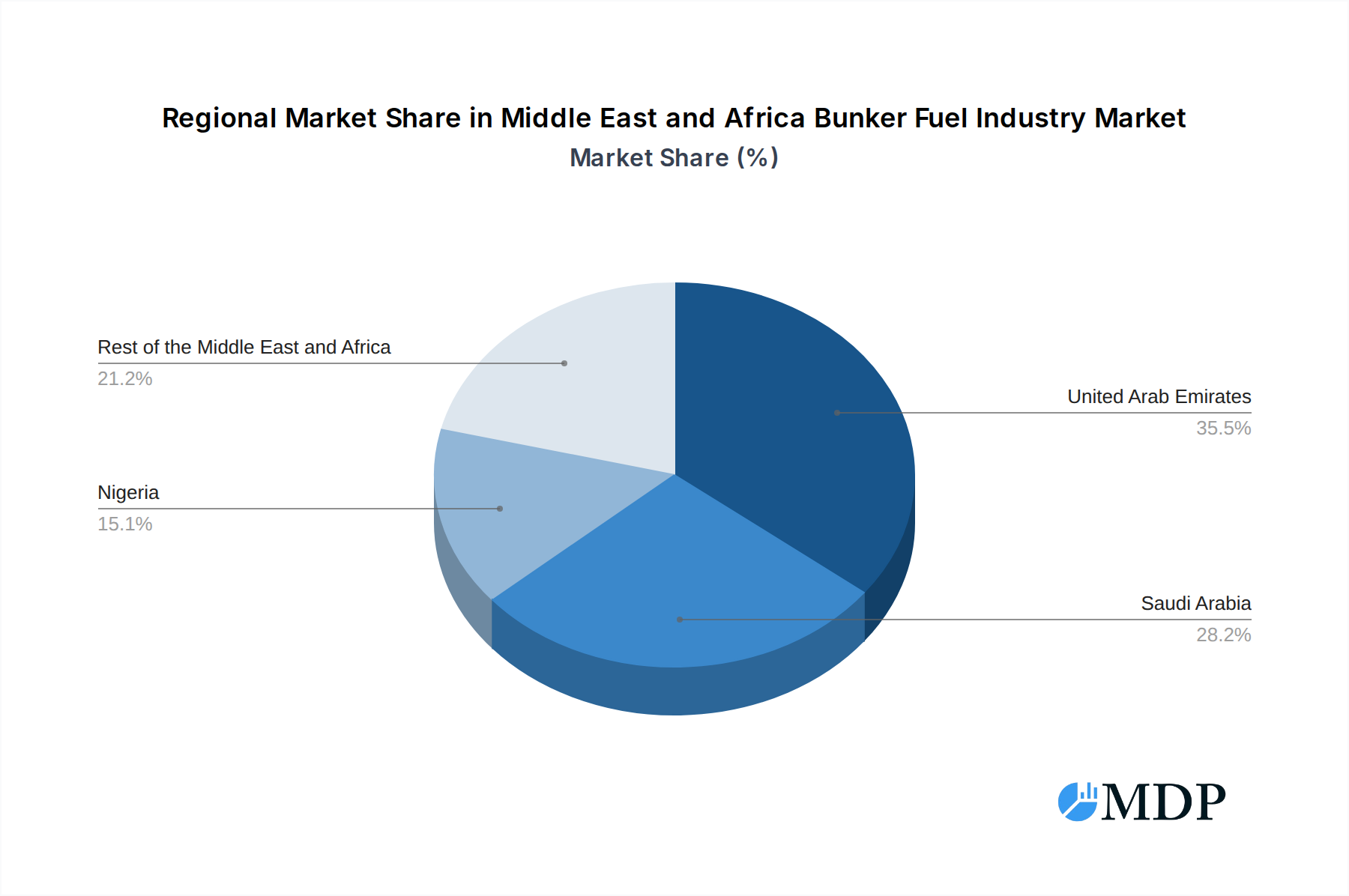

Leading Markets & Segments in Middle East and Africa Bunker Fuel Industry

The United Arab Emirates and Saudi Arabia stand out as the dominant geographical markets within the Middle East and Africa bunker fuel industry, propelled by their strategic locations, world-class port infrastructure, and significant refining capacities.

Dominant Geographies:

- The United Arab Emirates: With major hubs like Fujairah and Dubai, the UAE consistently ranks as a leading global bunkering center. Its commitment to port development and diversified economy supports high volumes of vessel calls across various segments.

- Saudi Arabia: Benefiting from its extensive coastline and substantial crude oil production, Saudi Arabia is a key player, with ongoing investments in port facilities and bunkering infrastructure, particularly on the Red Sea and Arabian Gulf coasts.

- Nigeria: As a major oil producer in Africa, Nigeria holds significant importance, especially for crude oil and refined product exports, driving demand for bunker fuels for its own offshore operations and transit vessels.

- Rest of the Middle-East and Africa: This encompasses a broad spectrum of markets, with growing potential in Egypt (Suez Canal transit), South Africa (Cape Town and Durban), and other emerging economies with developing maritime trade.

Dominant Fuel Types:

- Very-Low Sulfur Fuel Oil (VLSFO): This segment has witnessed exponential growth following the IMO 2020 regulations. Its dominance is expected to continue as the primary compliant fuel for most vessels operating globally.

- Marine Gas Oil (MGO): MGO also plays a crucial role, particularly for smaller vessels or those operating in emission control areas. Its clean-burning properties and ease of use make it a preferred option for many operators.

- High Sulfur Fuel Oil (HSFO): While its market share is declining, HSFO remains relevant in specific markets and for vessels equipped with scrubbers, offering a lower cost alternative.

Dominant Vessel Types:

- Tankers: Given the region's significant role in oil and gas production and export, tanker traffic is exceptionally high, making them the largest consumers of bunker fuel.

- Containers: The growth of global trade and the increasing popularity of mega-ships have made container vessels a significant segment for bunkering operations.

The dominance of these markets and segments is driven by a confluence of factors including economic policies promoting trade, substantial investments in port and logistical infrastructure, growing refining capacities, and adherence to international maritime regulations. For example, the UAE's strategic vision for becoming a global maritime hub, coupled with ADNOC's expanding refining capabilities, solidifies its leading position. Similarly, Saudi Arabia's Vision 2030 initiative includes significant investments in port modernization, which directly supports bunkering demand. The ongoing expansion of global supply chains further amplifies the importance of these regions for container and tanker traffic, reinforcing the demand for VLSFO and MGO.

Middle East and Africa Bunker Fuel Industry Product Developments

Product development in the MEA bunker fuel industry is increasingly focused on sustainability and efficiency. Innovations include advanced fuel blending techniques to meet stringent sulfur limits while optimizing engine performance and reducing emissions. The development of infrastructure for alternative fuels like LNG is a key trend, with pilot projects and planned investments aiming to accommodate dual-fuel vessels. Shell PLC and TotalEnergies SE are at the forefront of exploring and distributing cleaner fuel options, including biofuels and methanol, to support decarbonization efforts. These developments offer competitive advantages by aligning with environmental regulations and meeting the evolving needs of shipowners committed to reducing their carbon footprint. The focus remains on delivering reliable, compliant, and cost-effective bunkering solutions.

Key Drivers of Middle East and Africa Bunker Fuel Industry Growth

Several key drivers are propelling the growth of the Middle East and Africa bunker fuel industry. The escalating volume of global maritime trade, amplified by the region's strategic location on major shipping routes like the Suez Canal, is a primary engine. Significant investments in port infrastructure development and expansion by nations such as the UAE and Saudi Arabia are enhancing bunkering capabilities and attracting more vessel calls. The ongoing transition towards cleaner fuels, driven by stringent environmental regulations like the IMO 2020 sulfur cap, is creating sustained demand for VLSFO and MGO. Furthermore, the region's substantial oil and gas reserves ensure a consistent supply of feedstock for bunker fuel production, contributing to price competitiveness and reliability.

Challenges in the Middle East and Africa Bunker Fuel Industry Market

Despite robust growth, the MEA bunker fuel market faces several challenges. Intense price volatility of crude oil directly impacts bunker fuel pricing, creating forecasting difficulties for stakeholders. Navigating diverse and evolving regulatory landscapes across different African nations can pose compliance hurdles. Significant capital investment is required for developing infrastructure for alternative fuels like LNG, limiting their widespread adoption in many parts of the region. Competitive pressures from established global players and the emergence of new regional suppliers can also lead to margin erosion. Moreover, supply chain disruptions, geopolitical instability in certain areas, and the need for continuous technological upgrades to meet environmental standards present ongoing challenges.

Emerging Opportunities in Middle East and Africa Bunker Fuel Industry

Emerging opportunities in the MEA bunker fuel industry lie in the burgeoning demand for sustainable and alternative marine fuels. The increasing adoption of dual-fuel vessels presents a significant market for LNG, and future opportunities exist for ammonia and methanol as the industry progresses towards decarbonization. Strategic partnerships between fuel suppliers, port authorities, and technology providers can unlock new efficiencies and service offerings. The development of digital platforms for bunkering transactions, optimizing logistics and enhancing transparency, represents a substantial growth avenue. Furthermore, expansion into less developed but strategically located African ports offers untapped potential for market penetration and long-term growth.

Leading Players in the Middle East and Africa Bunker Fuel Industry Sector

- Uniper SE

- Shell PLC

- Exxon Mobil Corporation

- Aegean Bunkering SA

- Abu Dhabi National Oil Company

- Gulf Agency Company Ltd

- Chevron Corporation

- TotalEnergies SE

Key Milestones in Middle East and Africa Bunker Fuel Industry Industry

- May 2022: European Bank for Reconstruction and Development (EBRD) provided a USD 41.6 billion loan to Agence Nationale des Ports (ANP) for the development of Moroccan ports, supplemented by a USD 5.7 billion investment grant from the Global Environment Facility (GEF). This initiative is expected to enhance maritime infrastructure and potentially boost bunkering activities in North Africa.

- December 2022: Sudan signed a USD 6 billion agreement with a consortium led by the United Arab Emirates' AD Ports Group and Invictus Investment to develop a new port and economic zone in the Red Sea. This significant project is poised to transform maritime trade and logistics in the region, creating new opportunities for bunker fuel supply and services.

Strategic Outlook for Middle East and Africa Bunker Fuel Industry Market

The strategic outlook for the MEA bunker fuel industry is one of sustained growth and significant transformation. The continued expansion of global maritime trade, coupled with the region's strategic geographical advantage, will fuel demand. The pivotal shift towards decarbonization will drive investments in cleaner fuel alternatives like LNG, and potentially future fuels. Companies that can offer integrated solutions, encompassing supply, logistics, and sustainability services, will gain a competitive edge. Strategic collaborations with port authorities and shipping lines will be crucial for market penetration and service innovation. Adapting to evolving regulations and embracing digital technologies for operational efficiency will be paramount for long-term success and market leadership in this dynamic sector.

Middle East and Africa Bunker Fuel Industry Segmentation

-

1. Fuel Type

- 1.1. High Sulfur Fuel Oil (HSFO)

- 1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 1.3. Marine Gas Oil (MGO)

- 1.4. Liquefied Natural Gas (LNG)

- 1.5. Other Fuel Types

-

2. Vessel Type

- 2.1. Containers

- 2.2. Tankers

- 2.3. General Cargo

- 2.4. Bulk Carrier

- 2.5. Other Vessel Types

-

3. Geography

- 3.1. The United Arab Emirates

- 3.2. Saudi Arabia

- 3.3. Nigeria

- 3.4. Rest of the Middle-East and Africa

Middle East and Africa Bunker Fuel Industry Segmentation By Geography

- 1. The United Arab Emirates

- 2. Saudi Arabia

- 3. Nigeria

- 4. Rest of the Middle East and Africa

Middle East and Africa Bunker Fuel Industry Regional Market Share

Geographic Coverage of Middle East and Africa Bunker Fuel Industry

Middle East and Africa Bunker Fuel Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 5.1.1. High Sulfur Fuel Oil (HSFO)

- 5.1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 5.1.3. Marine Gas Oil (MGO)

- 5.1.4. Liquefied Natural Gas (LNG)

- 5.1.5. Other Fuel Types

- 5.2. Market Analysis, Insights and Forecast - by Vessel Type

- 5.2.1. Containers

- 5.2.2. Tankers

- 5.2.3. General Cargo

- 5.2.4. Bulk Carrier

- 5.2.5. Other Vessel Types

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. The United Arab Emirates

- 5.3.2. Saudi Arabia

- 5.3.3. Nigeria

- 5.3.4. Rest of the Middle-East and Africa

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. The United Arab Emirates

- 5.4.2. Saudi Arabia

- 5.4.3. Nigeria

- 5.4.4. Rest of the Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6. Middle East and Africa Bunker Fuel Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6.1.1. High Sulfur Fuel Oil (HSFO)

- 6.1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 6.1.3. Marine Gas Oil (MGO)

- 6.1.4. Liquefied Natural Gas (LNG)

- 6.1.5. Other Fuel Types

- 6.2. Market Analysis, Insights and Forecast - by Vessel Type

- 6.2.1. Containers

- 6.2.2. Tankers

- 6.2.3. General Cargo

- 6.2.4. Bulk Carrier

- 6.2.5. Other Vessel Types

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. The United Arab Emirates

- 6.3.2. Saudi Arabia

- 6.3.3. Nigeria

- 6.3.4. Rest of the Middle-East and Africa

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7. The United Arab Emirates Middle East and Africa Bunker Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7.1.1. High Sulfur Fuel Oil (HSFO)

- 7.1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 7.1.3. Marine Gas Oil (MGO)

- 7.1.4. Liquefied Natural Gas (LNG)

- 7.1.5. Other Fuel Types

- 7.2. Market Analysis, Insights and Forecast - by Vessel Type

- 7.2.1. Containers

- 7.2.2. Tankers

- 7.2.3. General Cargo

- 7.2.4. Bulk Carrier

- 7.2.5. Other Vessel Types

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. The United Arab Emirates

- 7.3.2. Saudi Arabia

- 7.3.3. Nigeria

- 7.3.4. Rest of the Middle-East and Africa

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8. Saudi Arabia Middle East and Africa Bunker Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8.1.1. High Sulfur Fuel Oil (HSFO)

- 8.1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 8.1.3. Marine Gas Oil (MGO)

- 8.1.4. Liquefied Natural Gas (LNG)

- 8.1.5. Other Fuel Types

- 8.2. Market Analysis, Insights and Forecast - by Vessel Type

- 8.2.1. Containers

- 8.2.2. Tankers

- 8.2.3. General Cargo

- 8.2.4. Bulk Carrier

- 8.2.5. Other Vessel Types

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. The United Arab Emirates

- 8.3.2. Saudi Arabia

- 8.3.3. Nigeria

- 8.3.4. Rest of the Middle-East and Africa

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9. Nigeria Middle East and Africa Bunker Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9.1.1. High Sulfur Fuel Oil (HSFO)

- 9.1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 9.1.3. Marine Gas Oil (MGO)

- 9.1.4. Liquefied Natural Gas (LNG)

- 9.1.5. Other Fuel Types

- 9.2. Market Analysis, Insights and Forecast - by Vessel Type

- 9.2.1. Containers

- 9.2.2. Tankers

- 9.2.3. General Cargo

- 9.2.4. Bulk Carrier

- 9.2.5. Other Vessel Types

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. The United Arab Emirates

- 9.3.2. Saudi Arabia

- 9.3.3. Nigeria

- 9.3.4. Rest of the Middle-East and Africa

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10. Rest of the Middle East and Africa Middle East and Africa Bunker Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10.1.1. High Sulfur Fuel Oil (HSFO)

- 10.1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 10.1.3. Marine Gas Oil (MGO)

- 10.1.4. Liquefied Natural Gas (LNG)

- 10.1.5. Other Fuel Types

- 10.2. Market Analysis, Insights and Forecast - by Vessel Type

- 10.2.1. Containers

- 10.2.2. Tankers

- 10.2.3. General Cargo

- 10.2.4. Bulk Carrier

- 10.2.5. Other Vessel Types

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. The United Arab Emirates

- 10.3.2. Saudi Arabia

- 10.3.3. Nigeria

- 10.3.4. Rest of the Middle-East and Africa

- 10.1. Market Analysis, Insights and Forecast - by Fuel Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Uniper SE

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Shell PLC

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Exxon Mobil Corporation

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Aegean Bunkering SA

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Abu Dhabi National Oil Company

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Gulf Agency Company Ltd

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Chevron Corporation

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 TotalEnergies SE

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.1 Uniper SE

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Middle East and Africa Bunker Fuel Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Middle East and Africa Bunker Fuel Industry Share (%) by Company 2025

List of Tables

- Table 1: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 2: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 3: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 4: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 5: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 7: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Region 2020 & 2033

- Table 9: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 10: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 11: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 12: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 13: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 14: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 15: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2020 & 2033

- Table 17: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 18: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 19: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 20: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 21: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 22: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 23: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2020 & 2033

- Table 25: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 26: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 27: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 28: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 29: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 30: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 31: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2020 & 2033

- Table 33: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 34: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 35: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 36: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 37: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 38: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 39: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East and Africa Bunker Fuel Industry?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the Middle East and Africa Bunker Fuel Industry?

Key companies in the market include Uniper SE, Shell PLC, Exxon Mobil Corporation, Aegean Bunkering SA, Abu Dhabi National Oil Company, Gulf Agency Company Ltd, Chevron Corporation, TotalEnergies SE.

3. What are the main segments of the Middle East and Africa Bunker Fuel Industry?

The market segments include Fuel Type, Vessel Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 172.5 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Declining Cost of Solar PV Installations4.; Supportive Government Policies For Renewable Energy.

6. What are the notable trends driving market growth?

VLSFO to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Penetration of Other Energy Sources.

8. Can you provide examples of recent developments in the market?

May 2022: European Bank for Reconstruction and Development (EBRD) provided a USD 41.6 million loan to Agence Nationale des Ports (ANP) for the development of Moroccan ports. The loan will be supplemented by an investment grant of USD 5.7 million from the Global Environment Facility (GEF).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in metric tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East and Africa Bunker Fuel Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East and Africa Bunker Fuel Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East and Africa Bunker Fuel Industry?

To stay informed about further developments, trends, and reports in the Middle East and Africa Bunker Fuel Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence