Key Insights

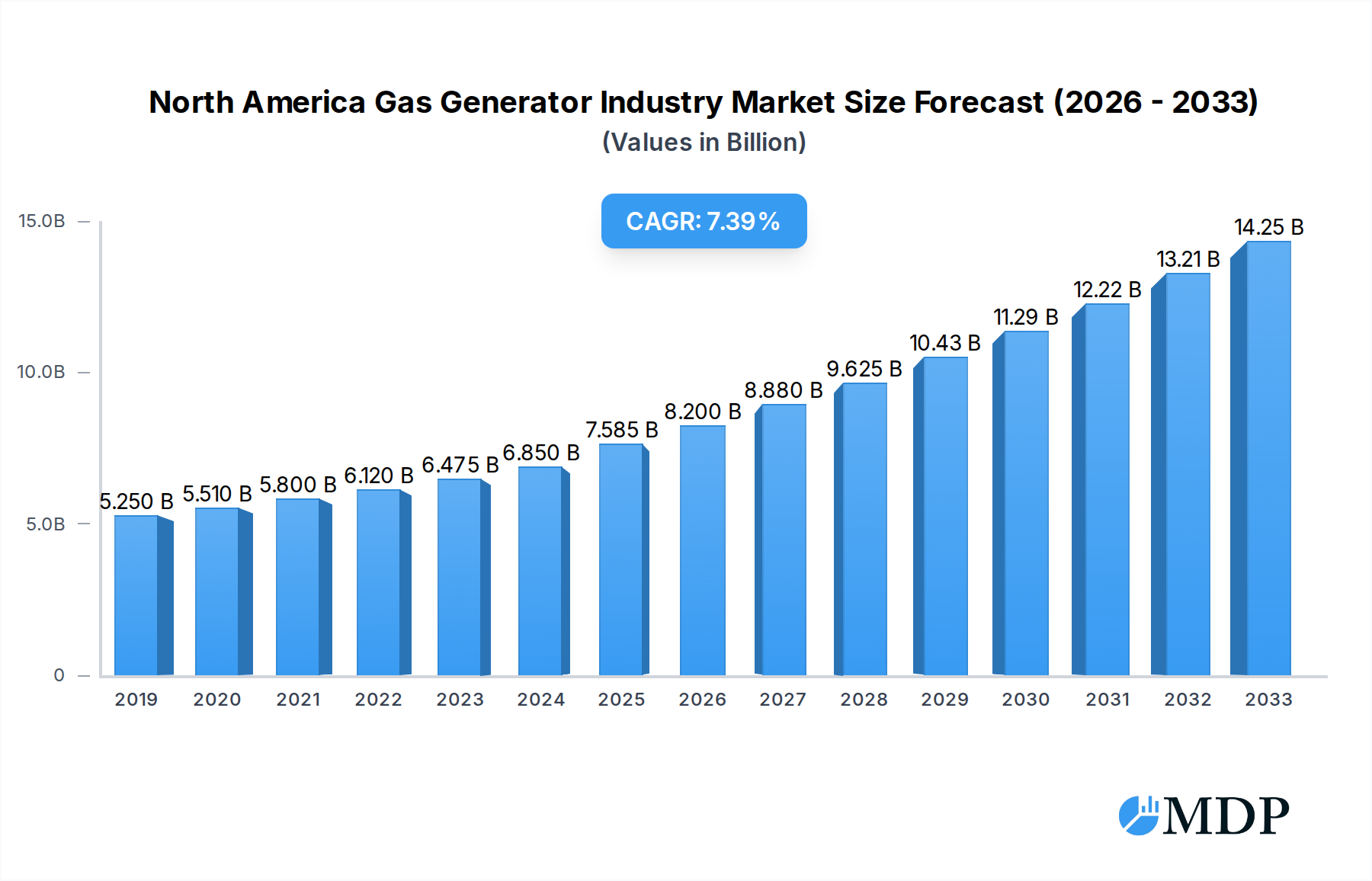

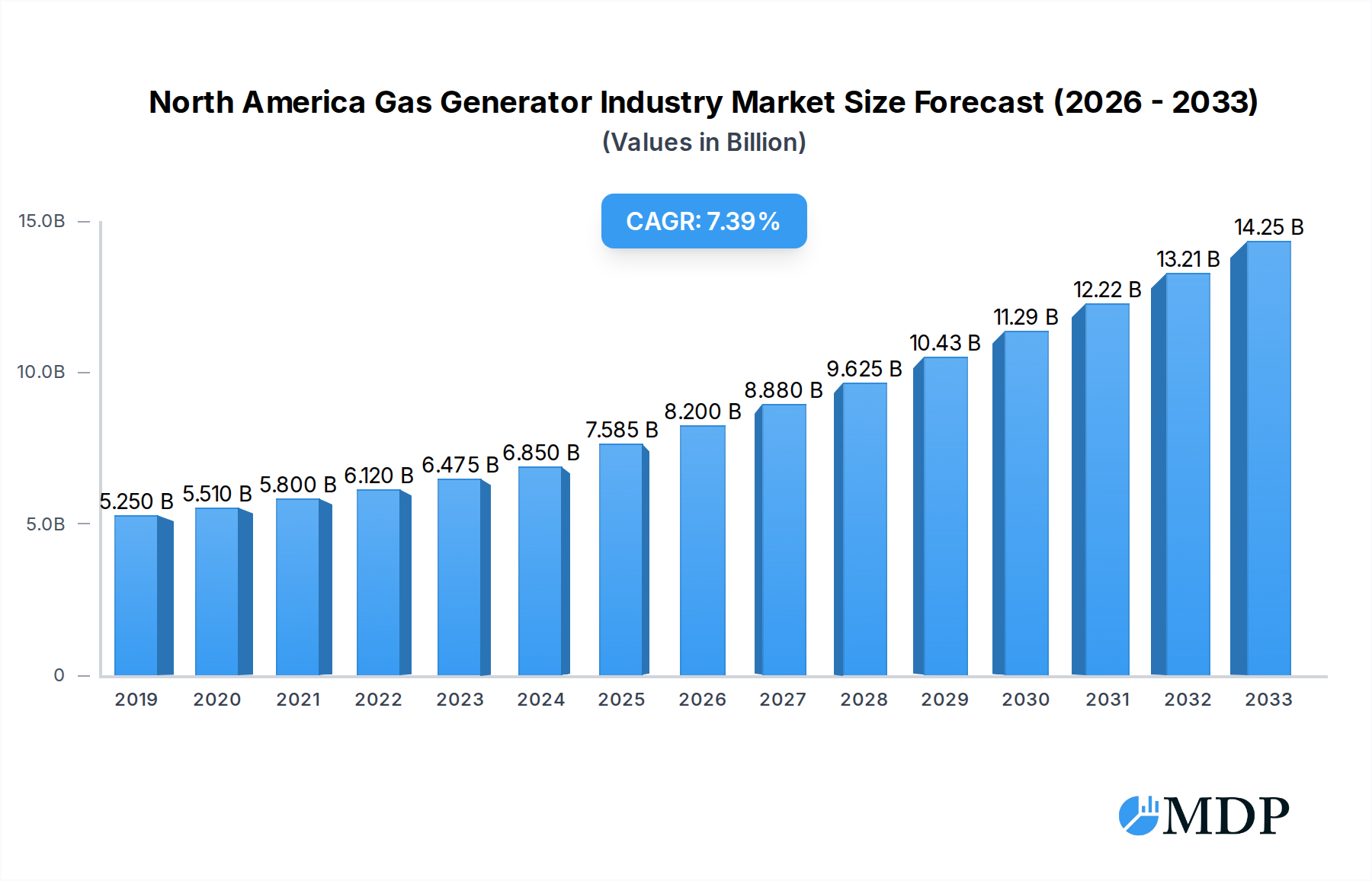

The North American Gas Generator market is poised for robust expansion, projected to reach an estimated $7,585 million in 2025. This significant market size underscores the critical role of gas generators in providing reliable power across diverse sectors. The industry is driven by an increasing demand for backup and prime power solutions, especially in regions facing grid instability and an escalating need for continuous operations in industrial and commercial settings. Furthermore, the growing emphasis on cleaner energy alternatives, compared to traditional diesel generators, positions natural gas-powered units as a more environmentally conscious choice, further fueling market growth. The CAGR of 8.8% from 2019 to 2033 indicates a sustained period of healthy growth, driven by technological advancements in generator efficiency, the expansion of natural gas infrastructure, and supportive government initiatives promoting cleaner power generation.

North America Gas Generator Industry Market Size (In Billion)

The market's trajectory is further shaped by key trends such as the rising adoption of smart grid technologies and the integration of IoT for remote monitoring and control of gas generators, enhancing operational efficiency and predictive maintenance. The increasing demand for modular and scalable generator solutions across various capacity segments – less than 75 kVA for residential and smaller commercial needs, 75-375 kVA for medium-sized businesses, and above 375 kVA for large industrial facilities – reflects a market catering to a wide spectrum of power requirements. While the market is experiencing strong growth, potential restraints could include fluctuating natural gas prices and stringent environmental regulations in certain sub-regions, though the overall shift towards cleaner energy is expected to mitigate these challenges. Geographically, the United States dominates the market, followed by Canada and the rest of North America, with each region exhibiting unique drivers and adoption rates for gas generator technologies.

North America Gas Generator Industry Company Market Share

North America Gas Generator Market: Growth, Trends, and Competitive Landscape 2019-2033

This comprehensive report provides an in-depth analysis of the North America Gas Generator Industry from 2019 to 2033, with a base year of 2025. Explore critical market dynamics, emerging trends, leading segments, product innovations, growth drivers, challenges, opportunities, and the competitive landscape. Uncover insights into market concentration, technological advancements, regulatory frameworks, and end-user preferences across the United States, Canada, and the rest of North America. With projected market value reaching billions of dollars, this report is an essential resource for industry stakeholders seeking to capitalize on the robust growth of the gas generator market.

North America Gas Generator Industry Market Dynamics & Concentration

The North America Gas Generator Industry exhibits a moderate to high market concentration, with a few key players dominating market share. Caterpillar Inc. and Cummins Inc. hold significant portions of the industrial and commercial segments, while Generac Holdings Inc. leads in the residential sector. Innovation drivers are primarily focused on increasing fuel efficiency, reducing emissions, enhancing smart connectivity for remote monitoring and control, and improving load response times, especially for critical applications. Regulatory frameworks, particularly concerning emissions standards and grid reliability, significantly influence product development and market penetration. Product substitutes, such as diesel generators and renewable energy sources like solar and wind power with battery storage, present a competitive challenge, though gas generators offer a reliable and cost-effective primary or backup power solution. End-user trends reveal a growing demand for reliable and on-demand power across industrial, commercial, and residential sectors, driven by increasing digitalization and the need for uninterrupted operations. Mergers and acquisitions (M&A) activities are notable, with companies seeking to expand their product portfolios, technological capabilities, and market reach. For instance, the acquisition of smaller technology firms by larger players aims to bolster their smart generator offerings. The M&A deal count in the past three years has been approximately 10-15, indicating strategic consolidation within the industry.

North America Gas Generator Industry Industry Trends & Analysis

The North America Gas Generator Industry is poised for substantial growth, driven by an increasing demand for reliable and flexible power solutions. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 5.5% during the forecast period of 2025–2033. This growth is fueled by several key factors, including the expansion of industrial and commercial sectors, the need for backup power in the face of an aging grid infrastructure and increasing extreme weather events, and the growing adoption of natural gas as a cleaner and more cost-effective fuel source compared to diesel. Technological disruptions are at the forefront of market evolution. Advancements in engine technology are leading to more fuel-efficient and low-emission generator sets, meeting stringent environmental regulations. The integration of IoT and AI is enabling smarter, connected generators that offer predictive maintenance, remote diagnostics, and optimized performance. Consumer preferences are shifting towards generator sets that are not only reliable but also environmentally conscious and cost-effective. The residential segment, in particular, is witnessing a surge in demand for compact, quiet, and smart generators that provide seamless power backup. Competitive dynamics are characterized by intense innovation and strategic partnerships. Companies are investing heavily in research and development to differentiate their offerings and capture market share. The market penetration of gas generators is steadily increasing across all end-user segments, displacing older technologies and solidifying their position as a preferred choice for primary and standby power. The growing electrification of various industries also necessitates robust and dependable power backup, further bolstering the demand for gas generators.

Leading Markets & Segments in North America Gas Generator Industry

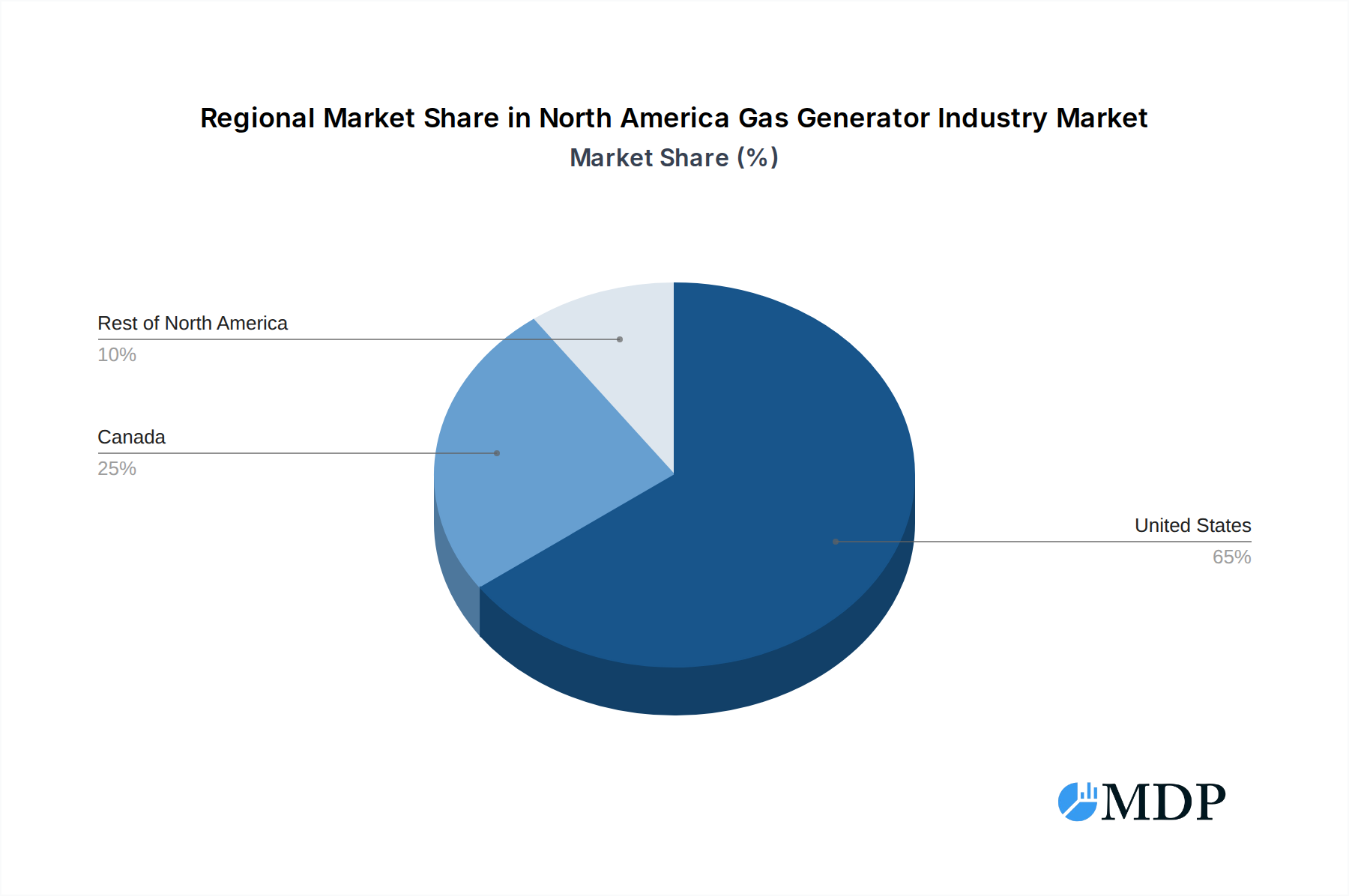

The United States stands as the dominant region within the North America Gas Generator Industry, accounting for an estimated 70% of the total market revenue. This leadership is driven by a robust industrial base, significant investments in commercial infrastructure, and a large and growing residential market that prioritizes energy security and resilience. Key economic policies and ongoing infrastructure development projects in the U.S. further stimulate demand for reliable power generation solutions.

Segments Dominance Analysis:

- Capacity: Above 375 kVA segment holds the largest market share, primarily driven by the industrial and commercial end-users who require substantial power for manufacturing facilities, data centers, hospitals, and large commercial complexes. The increasing complexity of industrial operations and the need for uninterrupted power supply to avoid significant financial losses are key drivers for this segment's dominance.

- End User: Industrial segment is the leading end-user category. The manufacturing sector, oil and gas exploration, and chemical processing plants rely heavily on uninterrupted power to maintain production cycles. The growing trend of automation and digitalization in industries further amplifies the need for reliable backup power.

- End User: Commercial segment follows closely, encompassing sectors like healthcare, retail, hospitality, and data centers. The increasing reliance on digital infrastructure and the critical need for continuous operation in these sectors make gas generators a crucial investment for power continuity.

- Geography: United States as discussed, is the primary market due to its vast industrial and commercial landscape, coupled with increasing concerns about grid reliability.

- Capacity: 75-375 kVA segment is also experiencing significant growth, catering to medium-sized businesses, larger residential complexes, and specific industrial applications where the power requirements fall within this range.

- End User: Residential segment, while currently smaller than industrial and commercial, is projected to witness the highest growth rate due to increasing awareness of power outage risks and a rising preference for home autonomy and comfort.

- Capacity: Less than 75 kVA segment is essential for smaller commercial establishments and specific residential backup needs, offering a cost-effective solution for localized power requirements.

- Geography: Canada represents a significant portion of the market, driven by its own industrial sectors, resource extraction, and a growing emphasis on energy independence.

- Geography: Rest of North America (including Mexico) is an emerging market with substantial growth potential, fueled by industrial expansion and increasing investments in power infrastructure.

North America Gas Generator Industry Product Developments

The North America Gas Generator Industry is witnessing continuous innovation focused on enhanced performance and sustainability. Recent developments include the introduction of generator sets with advanced load acceptance capabilities, crucial for mission-critical applications like data centers and healthcare facilities, as highlighted by Caterpillar Inc.'s Cat G3516 Fast Reaction generator set. Companies are also prioritizing the integration of smart technologies, enabling remote monitoring, predictive maintenance, and seamless integration with existing power grids. Furthermore, a growing emphasis on reducing emissions and improving fuel efficiency is leading to the development of more environmentally friendly and cost-effective natural gas generator solutions. These innovations provide competitive advantages by offering improved reliability, lower operating costs, and compliance with evolving environmental regulations, thereby meeting the diverse needs of industrial, commercial, and residential end-users.

Key Drivers of North America Gas Generator Industry Growth

Several critical factors are propelling the growth of the North America Gas Generator Industry. Firstly, the increasing demand for reliable and uninterrupted power across industrial, commercial, and residential sectors is a primary driver, especially in regions prone to grid instability and extreme weather events. Secondly, the growing adoption of natural gas as a cleaner and more cost-effective alternative to diesel fuel, coupled with the expanding natural gas infrastructure, significantly boosts demand. Thirdly, stringent environmental regulations pushing for lower emissions are favoring gas generators over traditional fossil fuel-powered alternatives. Technological advancements, such as the development of more fuel-efficient engines, smart connectivity, and improved load response times, are also crucial growth accelerators, making gas generators a preferred choice for various applications. The expansion of critical infrastructure, including data centers and healthcare facilities, further necessitates robust backup power solutions.

Challenges in the North America Gas Generator Industry Market

The North America Gas Generator Industry faces several hurdles that could impede its growth trajectory. Stringent and evolving environmental regulations, while driving demand for cleaner technologies, also impose higher compliance costs and R&D investments for manufacturers. Fluctuations in natural gas prices can impact the operational cost-effectiveness of gas generators, creating uncertainty for end-users. Supply chain disruptions, as witnessed in recent years, can lead to increased lead times and higher component costs, affecting production and delivery schedules. Furthermore, the ongoing advancements and decreasing costs of renewable energy sources like solar power coupled with battery storage present a growing competitive challenge, particularly in certain applications where intermittency is manageable. The initial capital investment for gas generator systems can also be a barrier for smaller businesses and some residential consumers.

Emerging Opportunities in North America Gas Generator Industry

The North America Gas Generator Industry is ripe with emerging opportunities driven by technological breakthroughs and evolving market demands. The increasing focus on grid modernization and the deployment of microgrids presents a significant opportunity for distributed generation solutions offered by gas generators, ensuring enhanced grid resilience and reliability. The burgeoning demand for backup power in the data center industry, fueled by the exponential growth of cloud computing and AI, is a substantial growth catalyst. Furthermore, the transition towards a more sustainable energy landscape opens avenues for hybrid power solutions that integrate gas generators with renewable energy sources, offering both reliability and reduced carbon footprints. Strategic partnerships between generator manufacturers and technology providers for smart grid integration and advanced control systems will unlock new market potential. Expansion into emerging markets within North America, driven by industrial development and infrastructure upgrades, also presents considerable long-term growth prospects.

Leading Players in the North America Gas Generator Industry Sector

- Cooper Corporation

- Kohler Co

- Caterpillar Inc.

- Cummins Inc.

- AKSA Power Generation

- MTU America Inc.

- General Electric Company

- Honda Power Equipment Mfg Inc.

- Generac Holdings Inc.

Key Milestones in North America Gas Generator Industry Industry

- January 2022: Caterpillar Inc. unveiled the Cat G3516 Fast Reaction generator set, adding a 1.5 MW power node to its portfolio, offering enhanced load acceptance and transient response for mission-critical applications.

- December 2021: HIPOWER SYSTEMS, HIMOINSA's North American production hub, commenced operations in its new 515,000-square-foot factory in Olathe, Kansas, equipped with advanced technology for producing generator sets for the North American market.

Strategic Outlook for North America Gas Generator Industry Market

The strategic outlook for the North America Gas Generator Industry remains exceptionally positive, driven by an unwavering demand for reliable and efficient power solutions. The industry is expected to witness continued growth fueled by technological advancements in smart connectivity, fuel efficiency, and emission reduction. Emphasis on developing integrated power solutions that combine gas generators with renewable energy sources and energy storage systems will be a key growth accelerator, catering to the evolving needs for sustainable and resilient power. Companies that focus on innovation, particularly in areas of IoT integration and predictive maintenance, will gain a competitive edge. The expansion of microgrids and the increasing need for robust backup power in critical infrastructure like data centers and healthcare facilities will continue to be significant market drivers. Strategic collaborations and potential M&A activities will likely shape the competitive landscape, enabling companies to enhance their market reach and technological capabilities, ensuring sustained growth and market dominance in the coming years.

North America Gas Generator Industry Segmentation

-

1. Capacity

- 1.1. Less than 75 kVA

- 1.2. 75-375 kVA

- 1.3. Above 375 kVA

-

2. End User

- 2.1. Industrial

- 2.2. Commercial

- 2.3. Residential

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Rest of North America

North America Gas Generator Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest of North America

North America Gas Generator Industry Regional Market Share

Geographic Coverage of North America Gas Generator Industry

North America Gas Generator Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 5.1.1. Less than 75 kVA

- 5.1.2. 75-375 kVA

- 5.1.3. Above 375 kVA

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Industrial

- 5.2.2. Commercial

- 5.2.3. Residential

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Rest of North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 6. North America Gas Generator Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 6.1.1. Less than 75 kVA

- 6.1.2. 75-375 kVA

- 6.1.3. Above 375 kVA

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Industrial

- 6.2.2. Commercial

- 6.2.3. Residential

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 7. United States North America Gas Generator Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 7.1.1. Less than 75 kVA

- 7.1.2. 75-375 kVA

- 7.1.3. Above 375 kVA

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Industrial

- 7.2.2. Commercial

- 7.2.3. Residential

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 8. Canada North America Gas Generator Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 8.1.1. Less than 75 kVA

- 8.1.2. 75-375 kVA

- 8.1.3. Above 375 kVA

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Industrial

- 8.2.2. Commercial

- 8.2.3. Residential

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 9. Rest of North America North America Gas Generator Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 9.1.1. Less than 75 kVA

- 9.1.2. 75-375 kVA

- 9.1.3. Above 375 kVA

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Industrial

- 9.2.2. Commercial

- 9.2.3. Residential

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Cooper Corporation

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Kohler Co

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Caterpillar Inc

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Cummins Inc

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 AKSA Power Generation*List Not Exhaustive

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 MTU America Inc

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 General Electric Company

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Honda Power Equipment Mfg Inc

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Generac Holdings Inc

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.1 Cooper Corporation

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Gas Generator Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: North America Gas Generator Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Gas Generator Industry Revenue million Forecast, by Capacity 2020 & 2033

- Table 2: North America Gas Generator Industry Volume K Unit Forecast, by Capacity 2020 & 2033

- Table 3: North America Gas Generator Industry Revenue million Forecast, by End User 2020 & 2033

- Table 4: North America Gas Generator Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 5: North America Gas Generator Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 6: North America Gas Generator Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 7: North America Gas Generator Industry Revenue million Forecast, by Region 2020 & 2033

- Table 8: North America Gas Generator Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: North America Gas Generator Industry Revenue million Forecast, by Capacity 2020 & 2033

- Table 10: North America Gas Generator Industry Volume K Unit Forecast, by Capacity 2020 & 2033

- Table 11: North America Gas Generator Industry Revenue million Forecast, by End User 2020 & 2033

- Table 12: North America Gas Generator Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 13: North America Gas Generator Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 14: North America Gas Generator Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 15: North America Gas Generator Industry Revenue million Forecast, by Country 2020 & 2033

- Table 16: North America Gas Generator Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: North America Gas Generator Industry Revenue million Forecast, by Capacity 2020 & 2033

- Table 18: North America Gas Generator Industry Volume K Unit Forecast, by Capacity 2020 & 2033

- Table 19: North America Gas Generator Industry Revenue million Forecast, by End User 2020 & 2033

- Table 20: North America Gas Generator Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 21: North America Gas Generator Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 22: North America Gas Generator Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 23: North America Gas Generator Industry Revenue million Forecast, by Country 2020 & 2033

- Table 24: North America Gas Generator Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: North America Gas Generator Industry Revenue million Forecast, by Capacity 2020 & 2033

- Table 26: North America Gas Generator Industry Volume K Unit Forecast, by Capacity 2020 & 2033

- Table 27: North America Gas Generator Industry Revenue million Forecast, by End User 2020 & 2033

- Table 28: North America Gas Generator Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 29: North America Gas Generator Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 30: North America Gas Generator Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 31: North America Gas Generator Industry Revenue million Forecast, by Country 2020 & 2033

- Table 32: North America Gas Generator Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Gas Generator Industry?

The projected CAGR is approximately 8.8%.

2. Which companies are prominent players in the North America Gas Generator Industry?

Key companies in the market include Cooper Corporation, Kohler Co, Caterpillar Inc, Cummins Inc, AKSA Power Generation*List Not Exhaustive, MTU America Inc, General Electric Company, Honda Power Equipment Mfg Inc, Generac Holdings Inc.

3. What are the main segments of the North America Gas Generator Industry?

The market segments include Capacity, End User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 7585 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Supply and Consumption of Gas-based Systems in Various End-user Industry4.; Implementation of stricter emission regulations worldwide.

6. What are the notable trends driving market growth?

Below 75 kVA Capacity Gas Generator to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Growing Inclination towards Renewable Sources.

8. Can you provide examples of recent developments in the market?

Jan 2022: Caterpillar Inc. unveiled the Cat G3516 Fast Reaction generator set, which adds a 1.5 MW power node to its increasing array of natural-gas power solutions that deliver market-leading load acceptance, transient response, and EPA certification for mission-critical applications.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Gas Generator Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Gas Generator Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Gas Generator Industry?

To stay informed about further developments, trends, and reports in the North America Gas Generator Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence