Key Insights

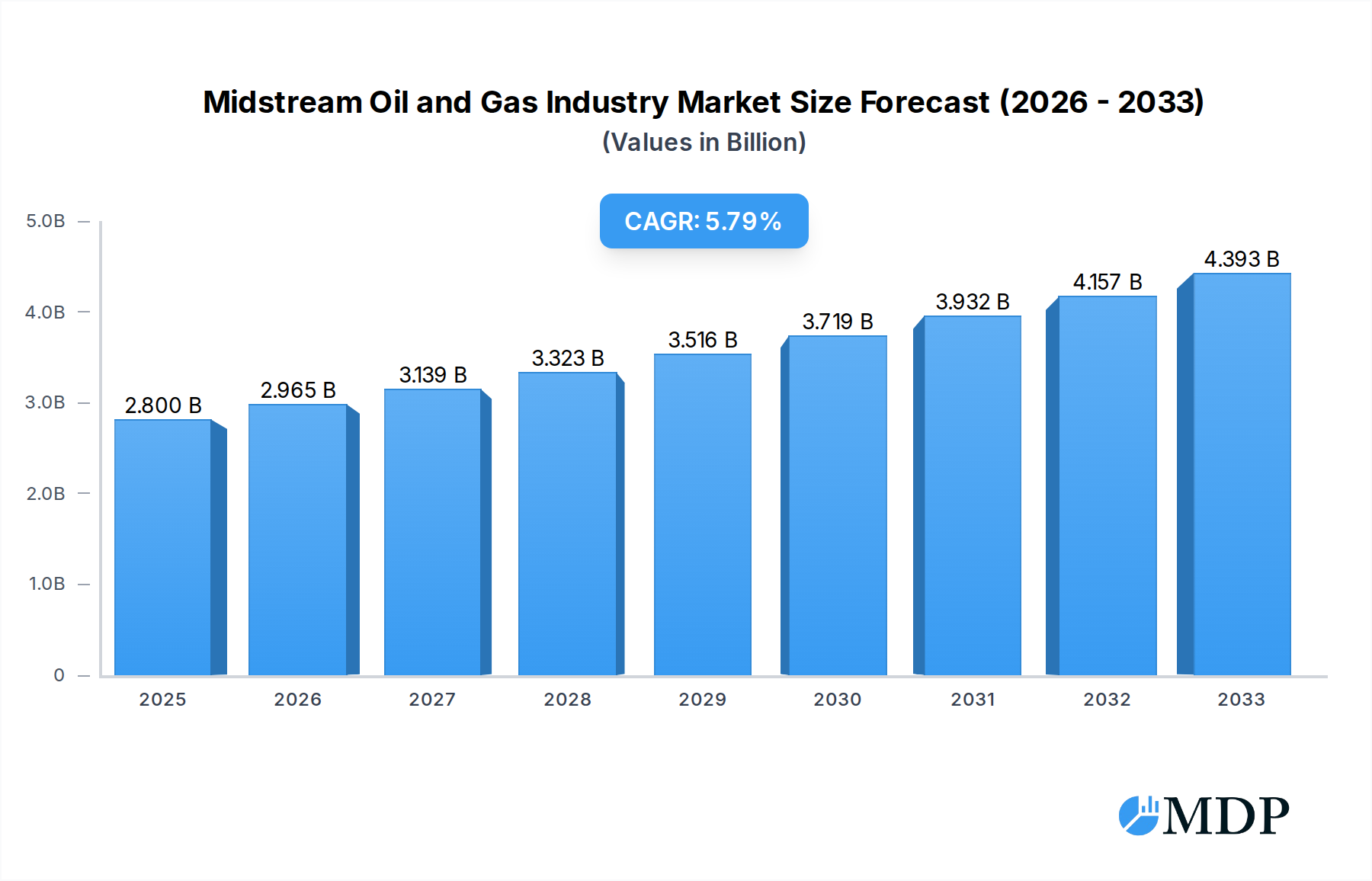

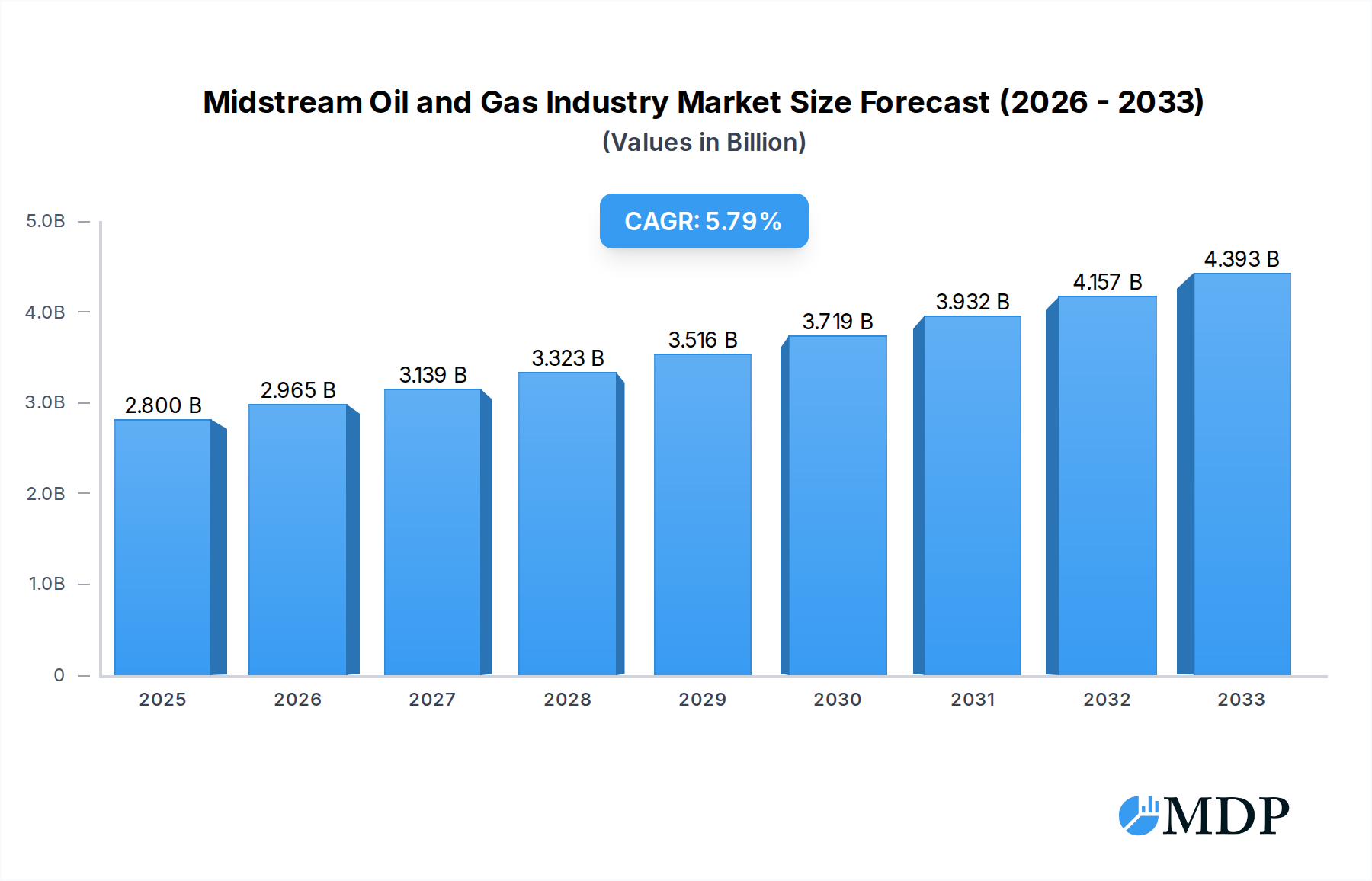

The Midstream Oil and Gas industry is poised for significant expansion, with the market size projected to reach USD 2.8 billion in 2025, demonstrating robust growth with a Compound Annual Growth Rate (CAGR) of 5.9% through 2033. This upward trajectory is primarily fueled by critical drivers such as the increasing demand for oil and gas globally, necessitating efficient transportation, storage, and terminal services. The strategic expansion of energy infrastructure, including pipelines, storage facilities, and liquefaction plants, is paramount to meeting this demand. Furthermore, advancements in technology for pipeline integrity monitoring and enhanced operational efficiency are contributing to market growth. The sector's focus on optimizing supply chains and reducing transit times for crude oil and natural gas is a key element in its ongoing development and investment attraction.

Midstream Oil and Gas Industry Market Size (In Billion)

Several key trends are shaping the Midstream Oil and Gas landscape. The growing importance of liquefied natural gas (LNG) infrastructure development, driven by international trade and the pursuit of cleaner energy sources, is a major factor. Investments in upgrading and expanding existing pipeline networks, alongside the construction of new ones, are crucial for alleviating transportation bottlenecks and ensuring reliable supply. Moreover, the integration of digital technologies, such as IoT and AI, for real-time monitoring and predictive maintenance of assets is enhancing operational efficiency and safety. However, the market faces certain restraints, including stringent environmental regulations and the ongoing transition towards renewable energy sources, which may impact long-term demand for fossil fuels. Geopolitical uncertainties and fluctuating commodity prices also present challenges that require strategic navigation by industry players.

Midstream Oil and Gas Industry Company Market Share

This in-depth report provides a definitive analysis of the global Midstream Oil and Gas industry, covering the crucial period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period of 2025–2033. Delve into critical market dynamics, emerging trends, leading segments within Transportation, Storage, and Terminals, pivotal product developments, growth drivers, inherent challenges, and burgeoning opportunities. Examine the strategic initiatives of key industry players and understand the significant milestones shaping the future of oil and gas logistics. This report is essential for stakeholders seeking actionable insights and a robust understanding of the evolving midstream landscape.

Midstream Oil and Gas Industry Market Dynamics & Concentration

The Midstream Oil and Gas industry is characterized by a dynamic interplay of factors influencing its market concentration. Innovation drivers, particularly in pipeline integrity, digital monitoring, and the integration of renewable energy feedstocks, are pushing for greater efficiency and reduced environmental impact. Regulatory frameworks, including stringent environmental, social, and governance (ESG) standards and evolving permitting processes, significantly shape operational strategies and investment decisions. Product substitutes, such as advancements in liquefied natural gas (LNG) transportation and the increasing adoption of electric vehicles impacting future demand for refined products, present ongoing considerations. End-user trends, driven by a global push towards cleaner energy sources and growing demand for natural gas, are redefining the scope of midstream operations. Mergers and acquisitions (M&A) activities remain a key indicator of market concentration. Over the historical period (2019–2024), we observed an estimated XX M&A deals, reflecting strategic consolidation and portfolio optimization among major players aiming to achieve economies of scale and enhance market share. Leading companies like Enbridge Pipelines Inc. and Williams Inc. have actively participated in such strategic moves to bolster their infrastructure and service offerings, influencing overall market concentration. While precise market share data varies by segment, significant players hold substantial portions of key transportation and storage capacities.

Midstream Oil and Gas Industry Industry Trends & Analysis

The Midstream Oil and Gas industry is undergoing a transformative period driven by robust market growth drivers, disruptive technological advancements, evolving consumer preferences, and intensified competitive dynamics. The increasing global demand for energy, coupled with a projected rise in natural gas consumption as a cleaner alternative to coal and oil, is a primary growth catalyst. This surge necessitates substantial investment in pipeline expansion, liquefied natural gas (LNG) terminals, and storage facilities. Technological disruptions are at the forefront, with the widespread adoption of digital solutions such as AI-powered predictive maintenance for pipelines, advanced SCADA systems for real-time monitoring, and the integration of blockchain for enhanced supply chain transparency. These innovations are not only optimizing operational efficiency and reducing costs but also improving safety and environmental performance. Consumer preferences are increasingly leaning towards sustainable and cleaner energy sources, directly impacting the demand for natural gas and the infrastructure required to transport it. This shift is prompting midstream companies to explore the transportation of biofuels, hydrogen, and captured CO2. Competitive dynamics are intensifying, with established players vying for market share while new entrants explore niche opportunities. The CAGR for the midstream oil and gas sector is projected to be approximately XX% during the forecast period (2025–2033), driven by these multifaceted trends. Market penetration of advanced digital technologies is expected to reach an estimated XX% by 2033, revolutionizing how midstream assets are managed and operated.

Leading Markets & Segments in Midstream Oil and Gas Industry

The Transportation segment, within the broader Transportation, Storage and Terminals sector, stands out as the dominant force in the global Midstream Oil and Gas industry. This dominance is underpinned by several key drivers, including robust economic policies that prioritize energy security and infrastructure development, and a persistent need for efficient and cost-effective methods to move large volumes of crude oil, natural gas, and refined products across vast geographical distances. The sheer scale of existing and planned pipeline networks, particularly for natural gas, positions transportation as the primary artery of the midstream value chain.

- Economic Policies and Infrastructure Investment: Governments worldwide are actively investing in energy infrastructure to support economic growth and ensure reliable energy supply. Initiatives like India's significant investment in gas infrastructure and the Nigeria-Morocco joint gas pipeline project exemplify this trend, directly bolstering the transportation segment.

- Growing Natural Gas Demand: The global shift towards natural gas as a cleaner transition fuel fuels demand for extensive pipeline networks and LNG import/export terminals, further solidifying the transportation segment's leadership.

- Technological Advancements in Pipeline Construction and Maintenance: Innovations in horizontal directional drilling, advanced materials, and remote monitoring technologies enable the construction and maintenance of pipelines in challenging terrains, expanding the reach and efficiency of transportation networks.

- Strategic Location of Reserves and Consumption Centers: The geographical distribution of oil and gas reserves often necessitates long-haul transportation to major consumption hubs, making pipelines the most economical solution for bulk movement.

The dominance of the transportation segment is further evident in the substantial capital expenditures allocated to pipeline projects, the high utilization rates of existing networks, and the continuous development of new cross-border and domestic pipelines designed to meet evolving energy demands. While storage and terminals are critical components, their function is intrinsically linked to the flow of hydrocarbons, making transportation the overarching and most impactful segment in the midstream oil and gas industry.

Midstream Oil and Gas Industry Product Developments

Recent product developments in the Midstream Oil and Gas industry are centered on enhancing efficiency, safety, and environmental sustainability. Innovations in pipeline materials, such as the development of more corrosion-resistant and high-strength steel alloys, are extending asset lifespans and reducing maintenance costs. Advanced digital technologies, including AI-powered leak detection systems and real-time flow optimization software, are revolutionizing operational control and minimizing product loss. Furthermore, there is a growing focus on developing infrastructure capable of transporting alternative energy sources like hydrogen and biofuels, reflecting the industry's adaptation to a changing energy landscape. These innovations offer significant competitive advantages by improving operational reliability, reducing environmental footprint, and enabling companies to diversify their service offerings.

Key Drivers of Midstream Oil and Gas Industry Growth

The Midstream Oil and Gas industry's growth is propelled by several interconnected factors. Technological advancements in pipeline construction, digital monitoring, and automation are enhancing efficiency and safety, enabling the development of more complex projects. Economic factors, such as increasing global energy demand, particularly for natural gas as a cleaner transition fuel, are driving investment in new infrastructure. Regulatory support and government initiatives, like India's ambitious gas infrastructure expansion plan and international pipeline projects, create favorable conditions for market expansion. Furthermore, the strategic development of LNG infrastructure to meet global demand and the increasing focus on ESG compliance are also significant growth catalysts, encouraging cleaner and more sustainable midstream operations.

Challenges in the Midstream Oil and Gas Industry Market

Despite robust growth prospects, the Midstream Oil and Gas industry faces significant challenges. Regulatory hurdles and permitting complexities can significantly delay project timelines and increase costs. Supply chain disruptions, as witnessed globally in recent years, can impact the availability of critical materials and equipment. Environmental concerns and public opposition to new pipeline projects, driven by climate change considerations and potential environmental impacts, pose a substantial barrier. Fluctuating commodity prices can affect investment decisions and project viability. Cybersecurity threats to critical infrastructure are an ever-present concern requiring continuous investment in robust protection measures. The competitive pressure from alternative energy sources also presents a long-term challenge to traditional hydrocarbon midstream operations.

Emerging Opportunities in Midstream Oil and Gas Industry

The Midstream Oil and Gas industry is poised for significant growth driven by emerging opportunities. The ongoing global energy transition presents a major catalyst, with increasing demand for natural gas necessitating substantial investment in pipeline infrastructure and LNG terminals. Technological breakthroughs in areas like carbon capture, utilization, and storage (CCUS) are creating new avenues for midstream companies to transport and manage CO2 emissions. Strategic partnerships and joint ventures for cross-border pipeline projects, such as the proposed Nigeria-Morocco gas pipeline, are unlocking new markets and enhancing energy access across regions. Furthermore, the development of infrastructure for transporting emerging energy sources like hydrogen and sustainable biofuels represents a significant long-term growth strategy, allowing midstream operators to diversify their portfolios and adapt to the evolving energy landscape.

Leading Players in the Midstream Oil and Gas Industry Sector

- Shell PLC

- Enlink Midstream LLC

- Williams Inc.

- APA Group

- Chevron Corporation

- Baker Hughes Company

- BP PLC

- Enbridge Pipelines Inc.

Key Milestones in Midstream Oil and Gas Industry Industry

- December 2020: The Petroleum Ministry of India announced a plan to invest approximately USD 60 billion in expanding the gas infrastructure in India by 2024. Through this, the government plans to increase the share of natural gas to 15% by 2030 in the country's energy mix. The investment will majorly focus on the development of pipeline networks and LNG terminals across the country. This initiative is crucial for meeting India's growing energy demands and transitioning towards cleaner fuels.

- February 2021: The Heads of the State of Nigeria and Morocco reaffirmed their commitment to constructing a joint gas pipeline expected to expand energy access across West Africa. The 5,660 km pipeline, which is estimated to cost approximately USD 25 billion, is expected to serve as an extension to the existing West African Gas Pipeline currently serving Benin, Togo, and Ghana and connect with Spain through Cadiz. This project has the potential to reshape regional energy dynamics and foster economic development.

- July 2021: After years of tense relations, Kenya and Tanzania signed a USD 1 billion gas pipeline agreement. The gas pipeline deal will transport gas between the coastal town of Mombasa in Kenya and Dar es Salaam in Tanzania. The project will cover over 600 kilometers. This agreement signifies a significant step towards regional energy cooperation and improved energy security for both nations.

Strategic Outlook for Midstream Oil and Gas Industry Market

The strategic outlook for the Midstream Oil and Gas industry is characterized by adaptation and expansion. Key growth accelerators include the increasing global demand for natural gas as a transition fuel, necessitating significant investments in pipeline infrastructure and LNG facilities. The industry's ability to embrace technological innovation, particularly in digital solutions for operational efficiency and predictive maintenance, will be paramount. Furthermore, a strategic focus on diversifying into the transportation of emerging energy sources like hydrogen and biofuels presents substantial long-term market potential. Companies that proactively invest in sustainable practices, navigate complex regulatory landscapes, and forge strategic partnerships for cross-border projects will be well-positioned for sustained success in the evolving global energy market.

Midstream Oil and Gas Industry Segmentation

-

1. Sector

- 1.1. Transportation

- 1.2. Storage and Terminals

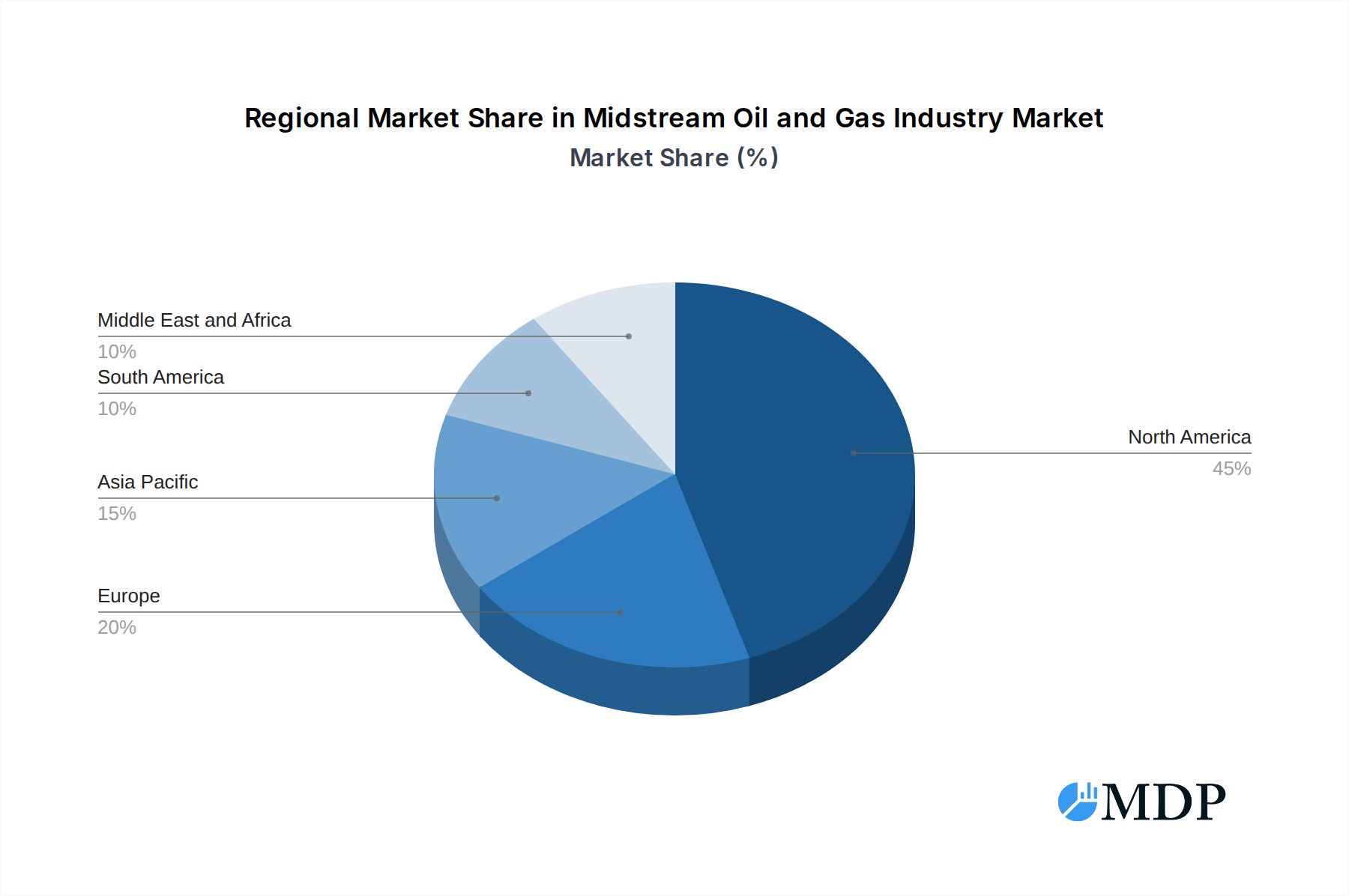

Midstream Oil and Gas Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. South America

- 5. Middle East and Africa

Midstream Oil and Gas Industry Regional Market Share

Geographic Coverage of Midstream Oil and Gas Industry

Midstream Oil and Gas Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Transportation

- 5.1.2. Storage and Terminals

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. South America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Global Midstream Oil and Gas Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 6.1.1. Transportation

- 6.1.2. Storage and Terminals

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 7. North America Midstream Oil and Gas Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Sector

- 7.1.1. Transportation

- 7.1.2. Storage and Terminals

- 7.1. Market Analysis, Insights and Forecast - by Sector

- 8. Europe Midstream Oil and Gas Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Sector

- 8.1.1. Transportation

- 8.1.2. Storage and Terminals

- 8.1. Market Analysis, Insights and Forecast - by Sector

- 9. Asia Pacific Midstream Oil and Gas Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Sector

- 9.1.1. Transportation

- 9.1.2. Storage and Terminals

- 9.1. Market Analysis, Insights and Forecast - by Sector

- 10. South America Midstream Oil and Gas Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Sector

- 10.1.1. Transportation

- 10.1.2. Storage and Terminals

- 10.1. Market Analysis, Insights and Forecast - by Sector

- 11. Middle East and Africa Midstream Oil and Gas Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Sector

- 11.1.1. Transportation

- 11.1.2. Storage and Terminals

- 11.1. Market Analysis, Insights and Forecast - by Sector

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Shell PLC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Enlink Midstream LLC*List Not Exhaustive

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Williams Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 APA Group

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Chevron Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Baker Hughes Company

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 BP PLC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Enbridge Pipelines Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 Shell PLC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Midstream Oil and Gas Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Midstream Oil and Gas Industry Revenue (billion), by Sector 2025 & 2033

- Figure 3: North America Midstream Oil and Gas Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 4: North America Midstream Oil and Gas Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Midstream Oil and Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Midstream Oil and Gas Industry Revenue (billion), by Sector 2025 & 2033

- Figure 7: Europe Midstream Oil and Gas Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 8: Europe Midstream Oil and Gas Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Europe Midstream Oil and Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Midstream Oil and Gas Industry Revenue (billion), by Sector 2025 & 2033

- Figure 11: Asia Pacific Midstream Oil and Gas Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 12: Asia Pacific Midstream Oil and Gas Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific Midstream Oil and Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Midstream Oil and Gas Industry Revenue (billion), by Sector 2025 & 2033

- Figure 15: South America Midstream Oil and Gas Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 16: South America Midstream Oil and Gas Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: South America Midstream Oil and Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Midstream Oil and Gas Industry Revenue (billion), by Sector 2025 & 2033

- Figure 19: Middle East and Africa Midstream Oil and Gas Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 20: Middle East and Africa Midstream Oil and Gas Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Middle East and Africa Midstream Oil and Gas Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Midstream Oil and Gas Industry Revenue billion Forecast, by Sector 2020 & 2033

- Table 2: Global Midstream Oil and Gas Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Midstream Oil and Gas Industry Revenue billion Forecast, by Sector 2020 & 2033

- Table 4: Global Midstream Oil and Gas Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Global Midstream Oil and Gas Industry Revenue billion Forecast, by Sector 2020 & 2033

- Table 6: Global Midstream Oil and Gas Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Midstream Oil and Gas Industry Revenue billion Forecast, by Sector 2020 & 2033

- Table 8: Global Midstream Oil and Gas Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Midstream Oil and Gas Industry Revenue billion Forecast, by Sector 2020 & 2033

- Table 10: Global Midstream Oil and Gas Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Global Midstream Oil and Gas Industry Revenue billion Forecast, by Sector 2020 & 2033

- Table 12: Global Midstream Oil and Gas Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Midstream Oil and Gas Industry?

The projected CAGR is approximately 5.9%.

2. Which companies are prominent players in the Midstream Oil and Gas Industry?

Key companies in the market include Shell PLC, Enlink Midstream LLC*List Not Exhaustive, Williams Inc, APA Group, Chevron Corporation, Baker Hughes Company, BP PLC, Enbridge Pipelines Inc.

3. What are the main segments of the Midstream Oil and Gas Industry?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.8 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Rising Environmental Concerns and Energy Security in the Country4.; Increasing Focus on Renewable Energy.

6. What are the notable trends driving market growth?

The Transportation Sector to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Availability of Abundance Natural Fossil Fuel Reserves.

8. Can you provide examples of recent developments in the market?

In December 2020, the Petroleum Ministry of India announced a plan to invest approximately USD 60 billion in expanding the gas infrastructure in India by 2024. Through this, the government plans to increase the share of natural gas to 15% by 2030 in the country's energy mix. The investment will majorly focus on the development of pipeline networks and LNG terminal across the country.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Midstream Oil and Gas Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Midstream Oil and Gas Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Midstream Oil and Gas Industry?

To stay informed about further developments, trends, and reports in the Midstream Oil and Gas Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence