Key Insights

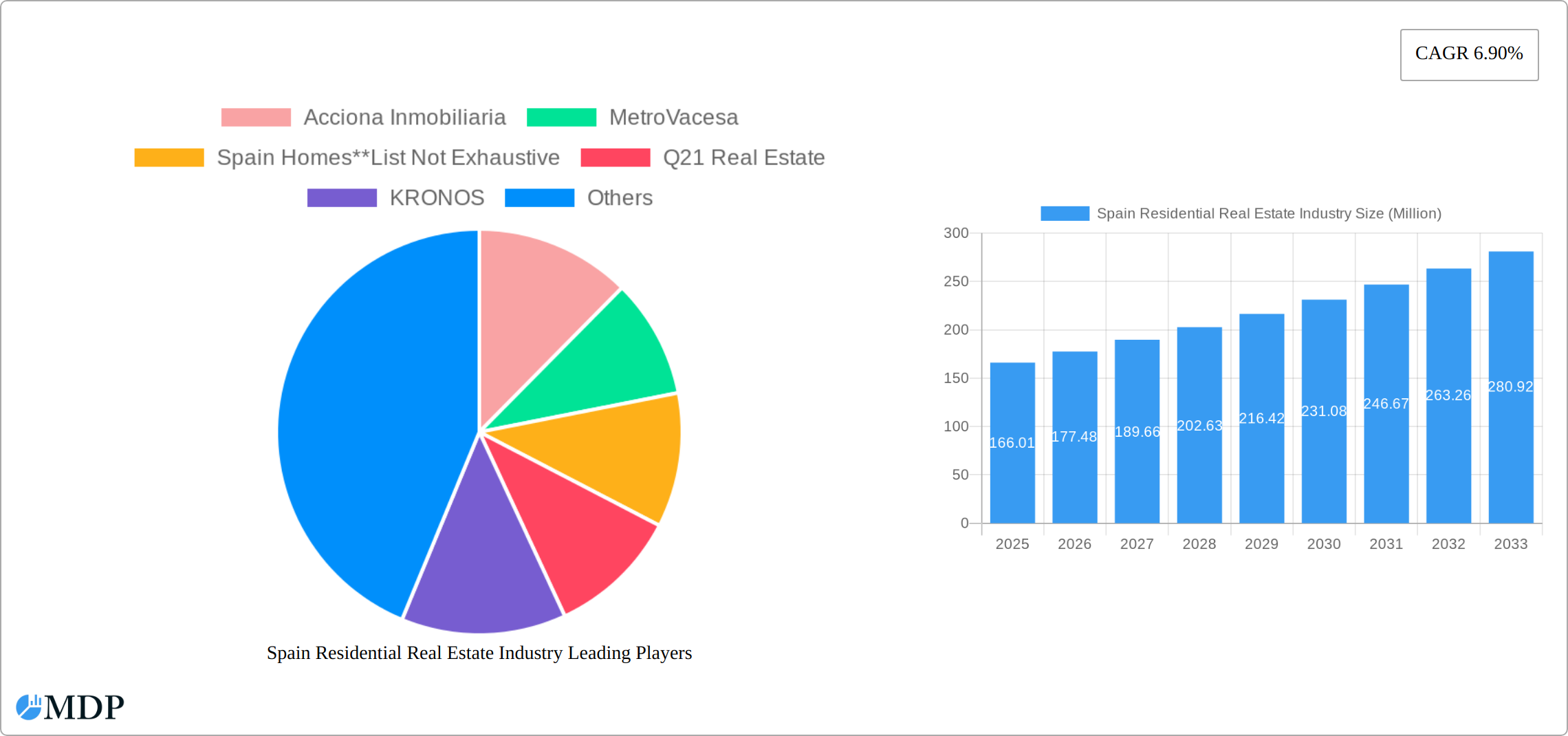

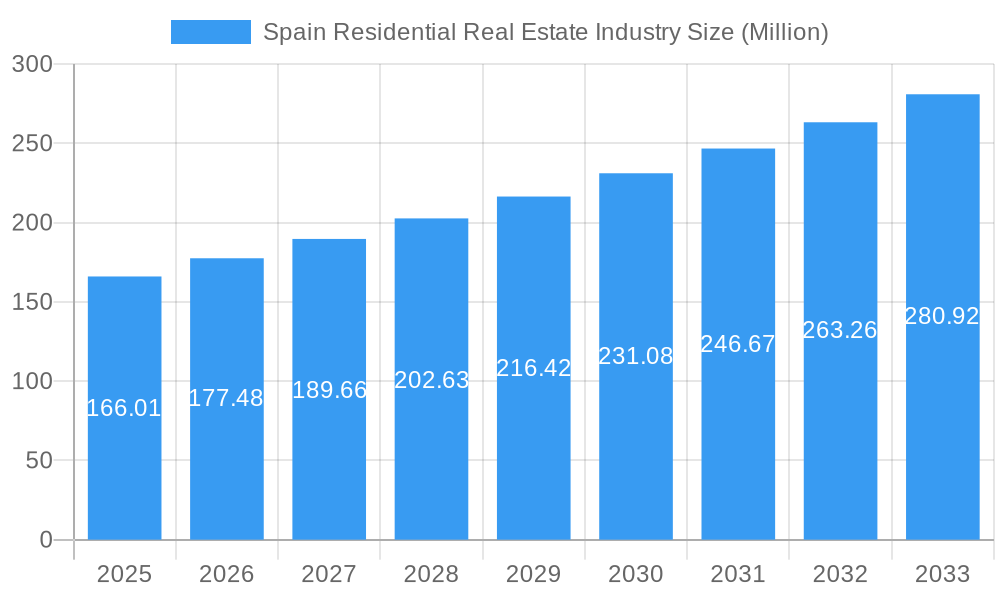

The Spanish residential real estate market, valued at €166.01 million in 2025, is projected for robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 6.90% from 2025 to 2033. This positive trajectory is driven by several factors. Increasing urbanization, particularly in major cities like Madrid and Barcelona, fuels demand for housing. A growing tourism sector contributes to the demand for vacation homes and rental properties, especially in coastal regions such as Malaga and Valencia. Furthermore, government initiatives aimed at stimulating the construction sector and improving housing affordability, coupled with historically low interest rates (though this may be subject to change depending on future economic conditions), are contributing to market expansion. Competition among developers like Acciona Inmobiliaria, Neinor Homes, and others is intensifying, leading to innovation in design and construction, and a broader range of housing options catering to diverse buyer preferences. The market is segmented by property type (apartments/condominiums, villas/landed houses) and key cities, reflecting regional variations in demand and pricing. While potential constraints such as fluctuating economic conditions and material costs exist, the overall outlook for the Spanish residential real estate market remains optimistic over the forecast period.

Spain Residential Real Estate Industry Market Size (In Million)

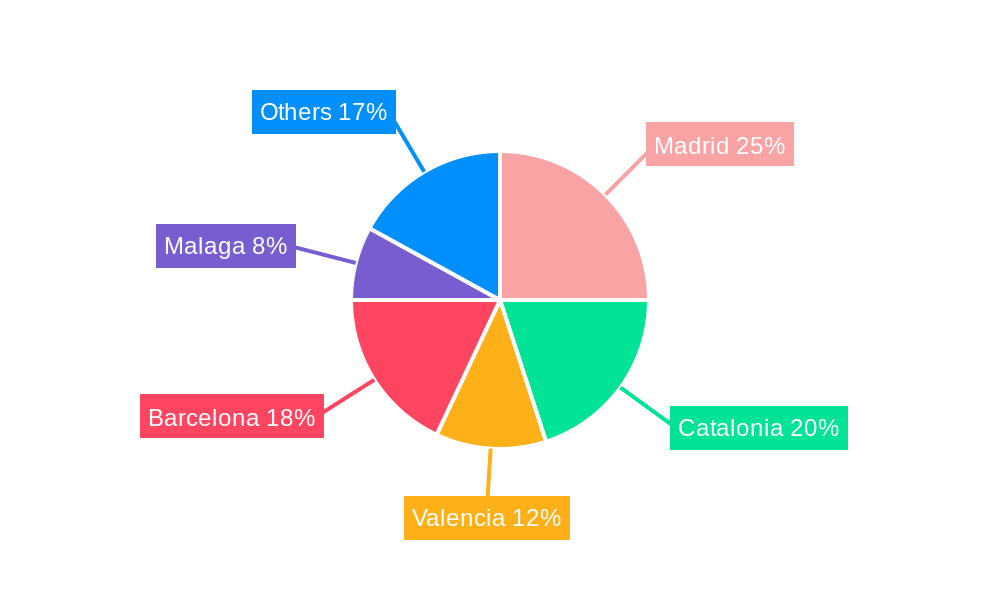

The segmentation of the market reveals interesting dynamics. Apartments and condominiums likely dominate the market share due to their affordability and suitability for urban living, especially in densely populated cities like Barcelona and Madrid. Villas and landed houses, while commanding higher prices, appeal to a more affluent segment and are popular in suburban areas and coastal regions. The regional distribution of the market highlights the significance of key cities as major economic and population hubs. While Madrid and Barcelona are expected to maintain strong positions, cities like Valencia and Malaga are also likely to experience significant growth due to their attractive lifestyle and economic opportunities. The continued success of the market will depend on the ability of developers to respond effectively to evolving buyer preferences, address affordability concerns, and navigate potential macroeconomic headwinds. The next decade is likely to see further consolidation in the industry, with larger players expanding their market share and smaller firms facing increasing competitive pressure.

Spain Residential Real Estate Industry Company Market Share

Spain Residential Real Estate Industry Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Spain residential real estate market, offering invaluable insights for investors, developers, and industry stakeholders. Covering the period 2019-2033, with a focus on 2025, this report unveils market dynamics, leading players, emerging trends, and future growth opportunities within the Spanish residential sector. The report analyzes key segments, including apartments and condominiums, villas and landed houses, across major cities like Madrid, Barcelona, Valencia, Malaga, and other regions. With a detailed examination of market concentration, M&A activity, and key industry developments, this report is an essential resource for navigating the complexities of the Spanish real estate landscape. Projected market value exceeds €XX Million.

Spain Residential Real Estate Industry Market Dynamics & Concentration

This section provides a comprehensive analysis of the competitive landscape within the Spanish residential real estate market. We delve into market concentration, the burgeoning trends of innovation, the influence of the regulatory framework, and the extent of Mergers & Acquisitions (M&A) activity observed from 2019 to 2024. Our examination also scrutinizes the pivotal factors shaping market dynamics, including evolving end-user preferences and the impact of substitute housing solutions. Market concentration is meticulously assessed using key metrics, such as the market share held by leading industry players, drawing data from available revenue figures and informed estimations.

- Market Concentration: The Spanish residential market is characterized by a moderately concentrated structure. Prominent players like Acciona Inmobiliaria, Neinor Homes, and AEDAS Homes command a substantial portion of the market share. Nevertheless, a vibrant ecosystem of smaller developers and regional enterprises plays a crucial role in the overall market's vitality. A detailed breakdown of individual player market shares will be presented in the forthcoming comprehensive report.

- Innovation Drivers: The industry is being propelled forward by significant technological advancements in construction methodologies, the increasing adoption of sustainable building materials, and sophisticated digital marketing strategies. The burgeoning integration of PropTech (Property Technology) solutions is also a key force reshaping market dynamics and driving efficiency.

- Regulatory Framework: Government policies at the national and regional levels concerning housing affordability, stringent building codes, and evolving environmental regulations exert a profound influence on market activity and development projects. These regulatory aspects are analyzed in depth to understand their impact on construction costs, project timelines, and the overall feasibility of new developments.

- Product Substitutes: The market faces a degree of substitution from the availability of a robust rental property sector and the rise of alternative accommodation models, such as co-living spaces and short-term rental platforms. The relative impact and interplay of these substitutes are thoroughly explored in the analysis.

- End-User Trends: Shifting demographic landscapes, evolving lifestyle aspirations, and transformations in household structures are significantly influencing the demand for diverse property types and geographical locations. Understanding these deep-seated trends is critical for anticipating future market needs.

- M&A Activity: The report meticulously tracks the volume and financial value of Mergers & Acquisitions (M&A) transactions within the industry during the specified historical period. This analysis aims to identify prevailing trends and their implications for market consolidation and strategic repositioning. Preliminary estimates suggest a total of approximately [Insert Number] M&A deals, with an aggregate value estimated at around €[Insert Value] Million, for the period spanning 2019-2024.

Spain Residential Real Estate Industry Industry Trends & Analysis

This section delves into the key trends shaping the Spanish residential real estate market, examining growth drivers, technological disruptions, consumer preferences, and competitive dynamics. We analyze the Compound Annual Growth Rate (CAGR) for the historical period and project the CAGR for the forecast period (2025-2033). Specific market penetration rates for key segments will also be analyzed, providing granular insights into market performance. The impact of macroeconomic factors, such as interest rates, inflation and employment rates on the market will be examined. The influence of changing consumer preferences regarding location, property size, and sustainability will also be thoroughly investigated. Detailed competitive analysis will highlight the strategies employed by major players, analyzing their market positioning and market share movements.

Leading Markets & Segments in Spain Residential Real Estate Industry

This section meticulously identifies and analyzes the leading markets and prominent segments within the Spanish residential real estate industry, highlighting their market dominance and the key factors driving their performance.

By Type:

- Apartments and Condominiums: This segment consistently demonstrates robust demand, largely attributable to its affordability and the allure of urban living. Key growth drivers include sustained population influx into urban centers and proactive government initiatives aimed at bolstering affordable housing options.

- Villas and Landed Houses: This segment caters to a more affluent demographic seeking expansive living spaces and enhanced privacy, particularly in desirable coastal regions. Increasing disposable incomes and the enduring appeal of second homes are significant drivers for this segment.

By Key Cities:

- Madrid: Bolstered by a strong economy, abundant employment opportunities, and a diverse range of housing offerings, Madrid consistently experiences high demand in its capital city. Ongoing infrastructure enhancements and supportive government policies for urban regeneration further amplify its attractiveness.

- Barcelona: Barcelona's world-renowned tourism industry and its vibrant cultural scene significantly contribute to its prominence as a sought-after residential location. Its prime coastal proximity and dynamic lifestyle further fuel sustained demand.

- Valencia: Offering a more cost-effective alternative to Madrid and Barcelona, Valencia is increasingly drawing homebuyers and investors. The city's continuously improving infrastructure and rich cultural heritage are significant contributors to the sector's growth.

- Catalonia: With its diverse geographical tapestry, encompassing picturesque coastal areas and serene mountainous regions, Catalonia appeals to a broad spectrum of buyers. Regional economic growth and a thriving tourism sector solidify its position as a key residential market.

- Malaga: Blessed with a quintessential Mediterranean climate, stunning beaches, and a burgeoning tourism industry, Malaga stands out as an exceptionally desirable residential destination. The region benefits significantly from substantial investments in major infrastructure projects.

- Others: Various other regions across Spain are exhibiting promising growth potential, driven by localized economic conditions and distinct lifestyle advantages that attract a diverse range of residents and investors.

Spain Residential Real Estate Industry Product Developments

The Spanish residential real estate sector is currently experiencing a wave of innovation characterized by advancements in building design, the utilization of novel materials, and the integration of cutting-edge technology. The incorporation of smart home technology, the widespread adoption of sustainable building practices focused on energy efficiency, and the increasing use of prefabricated construction methods are gaining significant momentum. These innovations are directly responding to a growing consumer demand for housing solutions that are both environmentally conscious and technologically advanced. The emphasis on sustainable and energy-efficient housing is particularly pronounced, reflecting heightened awareness of environmental concerns and the government's strong commitment to promoting sustainable development initiatives.

Key Drivers of Spain Residential Real Estate Industry Growth

Several compelling factors are fueling the sustained growth of the Spanish residential real estate market. These include a robust and expanding economy, ongoing urbanization trends, significant improvements in infrastructure networks, targeted government initiatives designed to enhance affordable housing access, and a notable increase in foreign investment. Furthermore, technological advancements in construction techniques and property management solutions are making substantial contributions to the sector's expansion. The burgeoning popularity and strategic adoption of the build-to-rent model are also creating new avenues for investment and development within the industry.

Challenges in the Spain Residential Real Estate Industry Market

Despite its growth trajectory, the Spanish residential real estate market encounters several persistent challenges. These include navigating complex regulatory hurdles that can potentially cause project delays, facing supply chain disruptions that impact material costs, and contending with intense competition among developers. Additionally, fluctuating interest rates and broader macroeconomic uncertainties can significantly affect consumer confidence and investment decisions, thereby influencing housing demand. The ongoing impact and residual effects of the COVID-19 pandemic continue to introduce an added layer of complexity and uncertainty into the prevailing market conditions.

Emerging Opportunities in Spain Residential Real Estate Industry

The Spanish residential real estate sector presents compelling opportunities. The increasing adoption of PropTech solutions, strategic partnerships between developers and investors, and the expansion into new markets are promising areas. The rising demand for sustainable and energy-efficient housing presents an opportunity for developers who can provide green building solutions. Furthermore, the growing popularity of build-to-rent schemes offers significant investment potential.

Leading Players in the Spain Residential Real Estate Industry Sector

- Acciona Inmobiliaria

- MetroVacesa

- Spain Homes

- Q21 Real Estate

- KRONOS

- Via Celere

- AELCA

- Neinor Homes

- Pryconsa

- AEDAS homes

Key Milestones in Spain Residential Real Estate Industry Industry

- October 2022: Layetana Living and Aviva Investors establish a EUR 500 million (USD 531.20 Million) build-to-rent (BTR) joint venture, acquiring a 71-unit building in Barcelona.

- September 2022: Berkshire Hathaway HomeServices expands into the Valencian Community, opening a new office in Denia.

Strategic Outlook for Spain Residential Real Estate Industry Market

The Spanish residential real estate market exhibits significant long-term growth potential. Continued economic growth, urban development, and technological advancements will drive demand. Strategic partnerships, focus on sustainability, and leveraging technological innovations will be key to success in this dynamic market. The build-to-rent sector is poised for significant expansion, presenting major investment opportunities.

Spain Residential Real Estate Industry Segmentation

-

1. Type

- 1.1. Apartments and Condominiums

- 1.2. Villas and Landed Houses

-

2. Key Cities

- 2.1. Madrid

- 2.2. Catalonia

- 2.3. Valencia

- 2.4. Barcelona

- 2.5. Malaga

- 2.6. Others

Spain Residential Real Estate Industry Segmentation By Geography

- 1. Spain

Spain Residential Real Estate Industry Regional Market Share

Geographic Coverage of Spain Residential Real Estate Industry

Spain Residential Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.90% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing Number of High Net-Worth Individuals (HNWIs)

- 3.3. Market Restrains

- 3.3.1. 4.; Rising Interest Rates

- 3.4. Market Trends

- 3.4.1. Rise in International Property Buyers in Spain

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Spain Residential Real Estate Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Apartments and Condominiums

- 5.1.2. Villas and Landed Houses

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Madrid

- 5.2.2. Catalonia

- 5.2.3. Valencia

- 5.2.4. Barcelona

- 5.2.5. Malaga

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Acciona Inmobiliaria

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 MetroVacesa

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Spain Homes**List Not Exhaustive

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Q21 Real Estate

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 KRONOS

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Via Celere

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 AELCA

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Neinor Homes

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Pryconsa

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 AEDAS homes

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Acciona Inmobiliaria

List of Figures

- Figure 1: Spain Residential Real Estate Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Spain Residential Real Estate Industry Share (%) by Company 2025

List of Tables

- Table 1: Spain Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Spain Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 3: Spain Residential Real Estate Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Spain Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Spain Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 6: Spain Residential Real Estate Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Residential Real Estate Industry?

The projected CAGR is approximately 6.90%.

2. Which companies are prominent players in the Spain Residential Real Estate Industry?

Key companies in the market include Acciona Inmobiliaria, MetroVacesa, Spain Homes**List Not Exhaustive, Q21 Real Estate, KRONOS, Via Celere, AELCA, Neinor Homes, Pryconsa, AEDAS homes.

3. What are the main segments of the Spain Residential Real Estate Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 166.01 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Number of High Net-Worth Individuals (HNWIs).

6. What are the notable trends driving market growth?

Rise in International Property Buyers in Spain.

7. Are there any restraints impacting market growth?

4.; Rising Interest Rates.

8. Can you provide examples of recent developments in the market?

October 2022: A build-to-rent (BTR) cooperation between Layetana Living and Aviva Investors was established in Spain. According to the statement, the collaboration between Aviva and the Spanish developer Layetana will construct a more than EUR 500 million (USD 531.20 Million) residential portfolio, already securing its first development project. Based on the recommendation of international real estate consultancy Knight Frank, the partnership purchased a 71-unit residential building in Barcelona's Sants neighborhood. Construction is scheduled to begin at the end of 2023.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Residential Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Residential Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Residential Real Estate Industry?

To stay informed about further developments, trends, and reports in the Spain Residential Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence