Key Insights

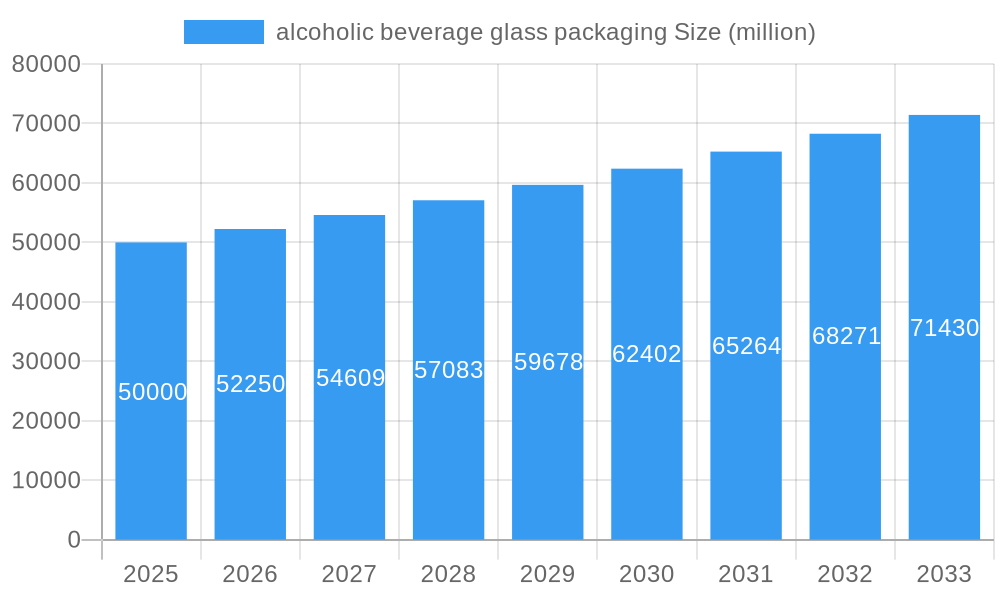

The global alcoholic beverage glass packaging market is projected for significant expansion, forecasted to reach approximately 78.63 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 5.8% between 2019 and 2033. This growth is propelled by increasing worldwide demand for alcoholic beverages, especially premium spirits and craft beers, where glass packaging is preferred for its visual appeal, quality perception, and inert properties that maintain taste and aroma. Rising disposable incomes in emerging markets and shifting consumer preferences for sophisticated products further support market growth. The convenience and recyclability of glass bottles align with environmental consciousness and circular economy principles, contributing to its enduring popularity. Key applications, including Beer and Spirits, are expected to dominate, driven by innovative packaging designs and the rise of single-serving formats and unique bottle shapes.

alcoholic beverage glass packaging Market Size (In Billion)

Market dynamics are shaped by key drivers and trends, notably the premiumization of alcoholic beverages, leading to a demand for high-quality glass packaging that enhances brand image. Technological advancements in glass manufacturing, yielding lighter, stronger, and more sustainable packaging, also contribute to market growth. Strategic actions by major players, including mergers, acquisitions, and capacity expansions, are influencing the competitive landscape. However, challenges such as increasing raw material costs and competition from alternative materials like PET and aluminum may moderate growth. Continuous innovation is crucial for addressing these challenges and capitalizing on opportunities, particularly in the Asia-Pacific region, which shows substantial growth potential.

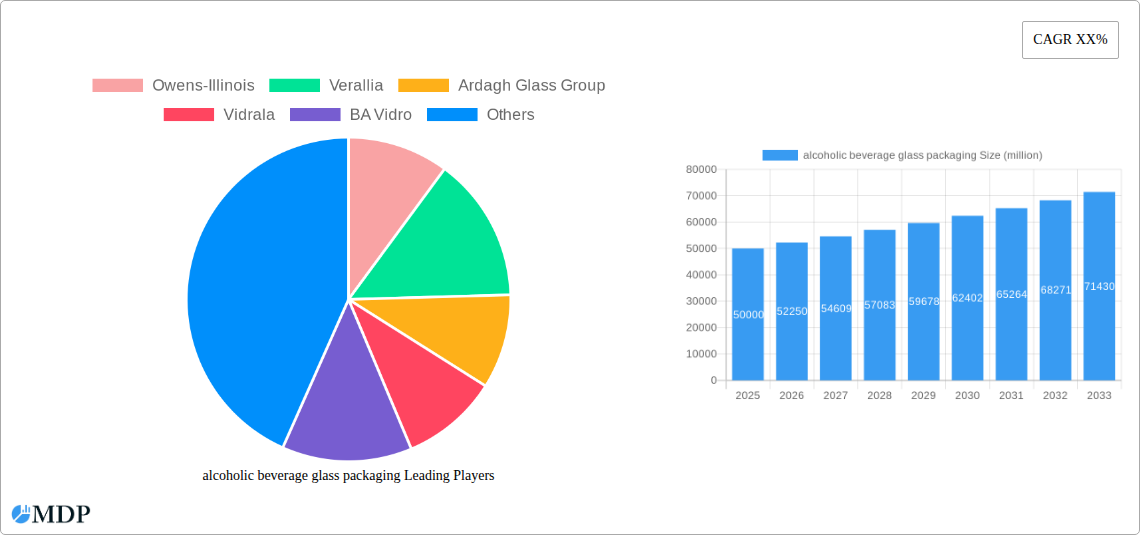

alcoholic beverage glass packaging Company Market Share

This comprehensive report offers an in-depth analysis of the global alcoholic beverage glass packaging market, including trends, dynamics, and future projections. The study covers the period from 2019 to 2033, with a base year of 2025. It provides actionable insights for industry stakeholders, examining historical data from 2019 to 2024 to establish a thorough market understanding. The report focuses on key segments such as Beer, Spirits, Baijiu, and Other applications, as well as popular glass packaging sizes including 250ml, 500ml, 600ml, and other capacities.

alcoholic beverage glass packaging Market Dynamics & Concentration

The alcoholic beverage glass packaging market exhibits a moderate to high level of concentration, with a few dominant players holding significant market share. Leading companies like Owens-Illinois, Verallia, and Ardagh Glass Group have established strong global footprints through strategic acquisitions and continuous innovation. The market is driven by increasing consumer demand for premium and visually appealing packaging, coupled with growing environmental consciousness, which favors the recyclability of glass. Regulatory frameworks concerning product safety and sustainability play a crucial role in shaping manufacturing processes and material choices. Product substitutes, such as plastic and aluminum, present ongoing challenges, but glass packaging's perceived quality and inertness for spirits and premium beers continue to ensure its dominance. End-user trends lean towards bespoke bottle designs and lightweighting initiatives to reduce transportation costs and environmental impact. Mergers and acquisitions (M&A) activities are a key feature, with an estimated 50+ significant M&A deals observed during the historical period, indicating consolidation and strategic expansion efforts among key players to enhance their market reach and technological capabilities.

alcoholic beverage glass packaging Industry Trends & Analysis

The alcoholic beverage glass packaging industry is poised for substantial growth, driven by a confluence of evolving consumer preferences, technological advancements, and expanding global markets. The projected Compound Annual Growth Rate (CAGR) for the forecast period (2025–2033) is estimated to be around 4.2%, with the market expected to reach a valuation of over $50,000 million by 2025. Market penetration for high-quality glass packaging, particularly for premium spirits and craft beers, continues to rise, fueled by a discerning consumer base that associates glass with superior product quality and an enhanced drinking experience. Technological disruptions are largely focused on enhancing the efficiency and sustainability of glass manufacturing, including advancements in furnace technology, lightweighting techniques, and the increased use of recycled cullet, aiming to reduce energy consumption and carbon emissions. Consumer preferences are increasingly gravitating towards aesthetically pleasing, custom-designed bottles that offer a distinct brand identity on crowded retail shelves. The competitive dynamics are characterized by a blend of global giants and agile regional players, all vying for market share through product innovation, cost optimization, and strategic partnerships. The industry is also witnessing a surge in demand for innovative features such as embossed logos, unique shapes, and colored glass options, further differentiating products and appealing to brand owners seeking to capture consumer attention. Furthermore, the growing demand for ready-to-drink (RTD) beverages and the resurgence of traditional spirits are significant tailwinds, requiring diverse packaging solutions. The emphasis on sustainability and the circular economy is also a critical trend, pushing manufacturers to invest in recyclable glass formulations and closed-loop recycling programs. The global market is projected to be worth over $60,000 million by the end of 2033.

Leading Markets & Segments in alcoholic beverage glass packaging

The Spirits segment is a dominant force within the alcoholic beverage glass packaging market, accounting for an estimated 35% of the market share in 2025. This dominance is driven by the premium perception associated with spirits, where glass packaging is crucial for preserving flavor integrity and conveying a sense of luxury and heritage. Within spirits, whisky and vodka are major contributors, with a strong preference for sophisticated bottle designs. The Beer segment follows closely, representing approximately 30% of the market share in 2025. The increasing popularity of craft beers and premium lagers has spurred demand for distinctive glass bottles, including the 600ml size, which has become a standard for many craft breweries.

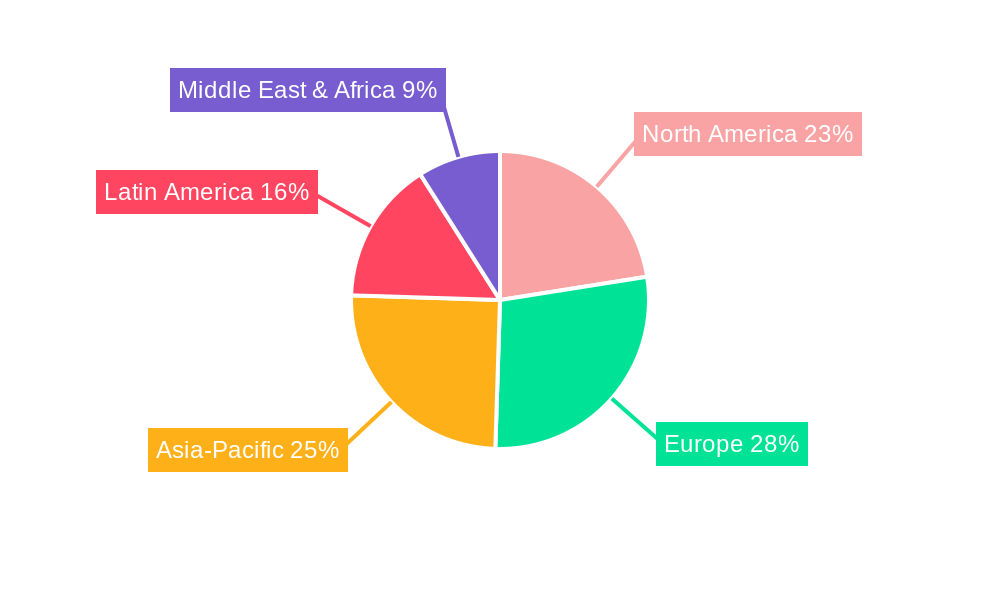

Regionally, Europe continues to be the leading market, holding an estimated 35% of the global market share in 2025. This leadership is attributed to a mature beverage industry, strong consumer demand for premium alcoholic products, and stringent environmental regulations that favor recyclable materials like glass. The presence of established glass manufacturers and a well-developed distribution network further solidify Europe's position. The North America region is another significant market, contributing around 28% in 2025, driven by the thriving spirits and craft beer industries.

In terms of Types, the 600ml bottle size is experiencing robust growth, particularly within the beer and certain spirit categories, representing an estimated 25% of the market in 2025. The 500ml size remains a strong contender, especially for premium spirits and ready-to-drink (RTD) beverages, holding approximately 22%. The 250ml segment is witnessing an upward trend, driven by single-serve portions and the growing RTD market, capturing an estimated 18% in 2025. The Other types, encompassing various bespoke and specialized bottle sizes, collectively account for the remaining market share.

Key drivers for the dominance of these segments include:

- Economic Policies: Favorable trade agreements and economic growth in key regions stimulate consumer spending on premium alcoholic beverages.

- Consumer Preferences: Growing demand for visually appealing, high-quality packaging that enhances brand perception.

- Regulatory Frameworks: Strict regulations promoting the use of sustainable and recyclable materials like glass, particularly in Europe.

- Technological Advancements: Innovations in bottle design and lightweighting techniques that enhance both aesthetics and cost-effectiveness.

- Beverage Industry Growth: The overall expansion of the alcoholic beverage market, including craft spirits and premium beers, directly fuels the demand for specialized glass packaging.

alcoholic beverage glass packaging Product Developments

Product innovations in alcoholic beverage glass packaging are primarily focused on enhancing sustainability, aesthetic appeal, and functional performance. Manufacturers are actively developing lightweight glass bottles that reduce material usage and transportation costs without compromising strength. Advancements in decorative techniques, such as advanced printing, embossing, and specialized coatings, allow for unique brand storytelling and premium finishes. The development of tinted glass formulations offers UV protection for sensitive beverages like certain wines and spirits, extending shelf life. Furthermore, the industry is exploring smart packaging solutions, integrating features like QR codes for enhanced consumer engagement and traceability. These innovations provide competitive advantages by meeting evolving consumer demands for premium, sustainable, and personalized packaging experiences.

Key Drivers of alcoholic beverage glass packaging Growth

Several key factors are propelling the growth of the alcoholic beverage glass packaging market. Firstly, the increasing consumer preference for premium and craft alcoholic beverages directly translates to a higher demand for high-quality, aesthetically pleasing glass packaging that conveys brand value and authenticity. Secondly, growing environmental consciousness and the emphasis on sustainability are significant drivers, as glass is infinitely recyclable and perceived as a more eco-friendly option compared to plastic. Technological advancements in lightweighting and efficient manufacturing processes are also contributing, making glass packaging more cost-competitive and reducing its carbon footprint. Finally, favorable regulatory landscapes in many regions that encourage the use of recyclable materials further bolster demand.

Challenges in the alcoholic beverage glass packaging Market

Despite robust growth, the alcoholic beverage glass packaging market faces several challenges. Fluctuations in raw material costs, particularly for soda ash and sand, can impact manufacturing expenses and profit margins. Intense competition from alternative packaging materials, such as aluminum cans and PET bottles, which often offer lower price points and lighter weight, poses a continuous threat. Energy-intensive manufacturing processes contribute to higher operational costs and environmental concerns, necessitating ongoing investment in energy-efficient technologies. Furthermore, complex supply chain logistics and the inherent fragility of glass can lead to higher transportation and handling costs, and an increased risk of breakage.

Emerging Opportunities in alcoholic beverage glass packaging

Emerging opportunities in the alcoholic beverage glass packaging market lie in several key areas. The burgeoning ready-to-drink (RTD) beverage segment presents a significant avenue for growth, with demand for smaller, single-serving glass bottles increasing. Continued innovation in sustainable packaging solutions, such as the increased use of recycled glass content and bio-based coatings, aligns with growing consumer and regulatory demands. Strategic partnerships between glass manufacturers and beverage brands can lead to the development of bespoke and innovative bottle designs that enhance brand differentiation and consumer engagement. Furthermore, expansion into emerging economies with growing middle classes and increasing disposable incomes offers substantial untapped market potential for premium alcoholic beverages and their associated glass packaging.

Leading Players in the alcoholic beverage glass packaging Sector

- Owens-Illinois

- Verallia

- Ardagh Glass Group

- Vidrala

- BA Vidro

- Vetropack

- Wiegand Glass

- Zignago Vetro

- Stölzle Glas Group

- HNGIL

- Nihon Yamamura

- Allied Glass

- Bormioli Luigi

Key Milestones in alcoholic beverage glass packaging Industry

- 2019: Increased adoption of lightweighting technologies across major players to reduce material usage.

- 2020: Growing emphasis on sustainability initiatives, with significant investments in recycling infrastructure.

- 2021: Launch of new decorative techniques for enhanced bottle aesthetics and branding.

- 2022: Significant M&A activity as companies sought to expand market share and product portfolios.

- 2023: Rise in demand for custom-designed bottles for premium spirits and craft beers.

- 2024: Advancements in energy-efficient furnace technologies to reduce carbon footprint.

- 2025 (Estimated): Continued growth in the RTD segment driving demand for smaller glass formats.

- 2026-2033 (Forecast): Anticipated further integration of recycled content and development of smart packaging solutions.

Strategic Outlook for alcoholic beverage glass packaging Market

The strategic outlook for the alcoholic beverage glass packaging market is one of sustained growth and innovation. The industry is expected to capitalize on the enduring consumer preference for premium and sustainable packaging. Key growth accelerators will include continued investment in research and development for lightweighting and enhanced recyclability, further bolstering the environmental credentials of glass. Strategic collaborations between glass manufacturers and beverage brands will be crucial in developing unique and market-differentiating packaging solutions. Expansion into high-growth emerging markets and a focus on catering to the evolving needs of the RTD segment will also be critical for long-term success. The market's ability to adapt to technological advancements and evolving consumer demands will ensure its continued relevance and profitability.

alcoholic beverage glass packaging Segmentation

-

1. Application

- 1.1. Beer

- 1.2. Spirits

- 1.3. Baijiu

- 1.4. Other

-

2. Types

- 2.1. 250ml

- 2.2. 500ml

- 2.3. 600ml

- 2.4. Other

alcoholic beverage glass packaging Segmentation By Geography

- 1. CA

alcoholic beverage glass packaging Regional Market Share

Geographic Coverage of alcoholic beverage glass packaging

alcoholic beverage glass packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Beer

- 5.1.2. Spirits

- 5.1.3. Baijiu

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 250ml

- 5.2.2. 500ml

- 5.2.3. 600ml

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. CA

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. alcoholic beverage glass packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Beer

- 6.1.2. Spirits

- 6.1.3. Baijiu

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 250ml

- 6.2.2. 500ml

- 6.2.3. 600ml

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Owens-Illinois

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Verallia

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Ardagh Glass Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Vidrala

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 BA Vidro

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Vetropack

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Wiegand Glass

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Zignago Vetro

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Stölzle Glas Group

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 HNGIL

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Nihon Yamamura

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Allied Glass

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Bormioli Luigi

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Owens-Illinois

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: alcoholic beverage glass packaging Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: alcoholic beverage glass packaging Share (%) by Company 2025

List of Tables

- Table 1: alcoholic beverage glass packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 2: alcoholic beverage glass packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 3: alcoholic beverage glass packaging Revenue billion Forecast, by Region 2020 & 2033

- Table 4: alcoholic beverage glass packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 5: alcoholic beverage glass packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 6: alcoholic beverage glass packaging Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the alcoholic beverage glass packaging?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the alcoholic beverage glass packaging?

Key companies in the market include Owens-Illinois, Verallia, Ardagh Glass Group, Vidrala, BA Vidro, Vetropack, Wiegand Glass, Zignago Vetro, Stölzle Glas Group, HNGIL, Nihon Yamamura, Allied Glass, Bormioli Luigi.

3. What are the main segments of the alcoholic beverage glass packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 78.63 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3400.00, USD 5100.00, and USD 6800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "alcoholic beverage glass packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the alcoholic beverage glass packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the alcoholic beverage glass packaging?

To stay informed about further developments, trends, and reports in the alcoholic beverage glass packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence