Key Insights

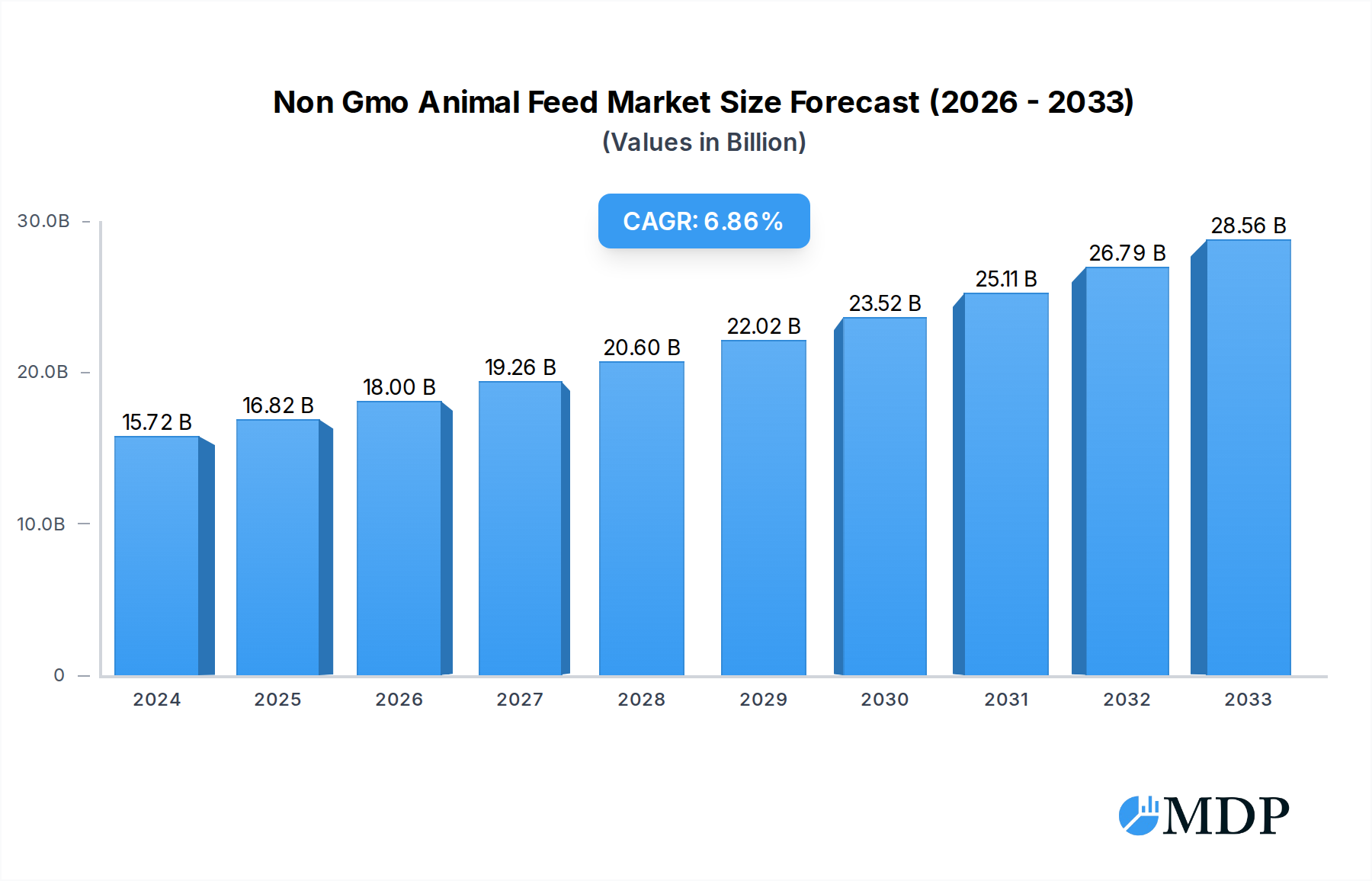

The global Non-GMO Animal Feed market is poised for significant expansion, projected to reach $15.72 billion in 2024, with a robust Compound Annual Growth Rate (CAGR) of 7%. This upward trajectory is driven by a confluence of factors, primarily the escalating consumer demand for transparent and ethically sourced food products, particularly meat and dairy. As awareness regarding the potential health and environmental implications of genetically modified organisms (GMOs) grows, both consumers and feed manufacturers are increasingly prioritizing non-GMO alternatives. This shift is further amplified by stringent regulatory frameworks and labeling requirements in various key markets, compelling producers to invest in non-GMO sourcing and production. The demand spans across diverse animal types, with significant applications in Beef Cattle, Chicken, and Turkeys, as these are major contributors to global protein consumption. The growing emphasis on animal welfare and sustainable agricultural practices also acts as a powerful catalyst for the adoption of non-GMO feed.

Non Gmo Animal Feed Market Size (In Billion)

The market's growth is further underpinned by emerging trends such as the development of specialized non-GMO feed formulations tailored to specific animal life stages and nutritional needs, as well as advancements in agricultural technologies that support the cultivation of non-GMO crops like Field Peas, Corn, and Soybeans. Key players in the food and feed industry, including Kraft Heinz, Unilever, Nestle, and General Mills, are actively investing in or expanding their non-GMO product portfolios, signaling a strong market commitment. While the market presents immense opportunities, certain restraints like the potentially higher cost of non-GMO ingredients and the complexities associated with maintaining a fully non-GMO supply chain can pose challenges. However, the overwhelming consumer preference for traceable, natural, and healthier animal products, coupled with supportive regulatory landscapes, is expected to propel the Non-GMO Animal Feed market towards sustained and significant growth throughout the forecast period.

Non Gmo Animal Feed Company Market Share

This comprehensive report delves into the burgeoning non-GMO animal feed market, offering invaluable insights for farmers, feed manufacturers, livestock producers, and investors seeking to capitalize on this rapidly expanding sector. Our analysis covers the historical trajectory, current landscape, and future projections of the organic animal feed, genetically modified organism-free feed, and sustainable livestock nutrition industries. The report provides actionable strategies for navigating market dynamics, identifying growth opportunities, and understanding the competitive environment.

Non Gmo Animal Feed Market Dynamics & Concentration

The global non-GMO animal feed market, valued at an estimated $xxx billion in the base year of 2025, is experiencing significant growth driven by escalating consumer demand for transparency and naturally produced food products. Market concentration is moderately fragmented, with key players like Nestle, Kraft Heinz, Unilever, ConAgra, The Hain Celestial Group, and General Mills actively participating through strategic initiatives and product diversification. Innovation in feed formulations, focusing on improved animal health and productivity without genetic modification, is a primary driver. Regulatory frameworks, such as country-specific labeling laws for GMO content, are increasingly shaping market entry and consumer trust. Product substitutes, while present in conventional feed, are less impactful as the demand for verified non-GMO options grows. End-user trends highlight a growing preference for traceable and ethically sourced animal products, directly influencing feed choices. Mergers and acquisitions (M&A) are becoming more prevalent, with an estimated xx significant deals occurring between 2019 and 2024, totaling an investment of over $xxx billion, indicating consolidation and strategic expansion within the industry.

Non Gmo Animal Feed Industry Trends & Analysis

The non-GMO animal feed industry is poised for robust expansion, with an anticipated Compound Annual Growth Rate (CAGR) of approximately xx% during the forecast period of 2025–2033, reaching a projected market size of $xxx billion by 2033. This growth is propelled by several interconnected factors. Consumer awareness regarding the potential health and environmental implications of GMOs in the food chain is at an all-time high, creating substantial pull from the end consumer for non-GMO certified animal products. This demand cascades down to feed manufacturers and livestock producers, making non-GMO feed a critical component of their value proposition. Technological disruptions are playing a crucial role, not just in the cultivation of non-GMO crops like Field Peas, Corn, Milo, and Soybeans, but also in advanced feed processing techniques that enhance nutrient bioavailability and animal well-being. The increasing adoption of these feeds in various applications, including Beef Cattle, Turkeys, Chicken, Goats, and Horses, signifies a broadening market penetration. Competitive dynamics are characterized by a mix of established multinational corporations and specialized non-GMO feed producers, each vying for market share through product innovation, certification, and strategic partnerships. The global market penetration of non-GMO animal feed is estimated to reach xx% by 2025, a figure expected to rise significantly. The Epermarket and Dr. Schar are examples of companies actively catering to this demand. The rising cost and limited availability of certain conventional feed ingredients further incentivize the shift towards diversified non-GMO sources.

Leading Markets & Segments in Non Gmo Animal Feed

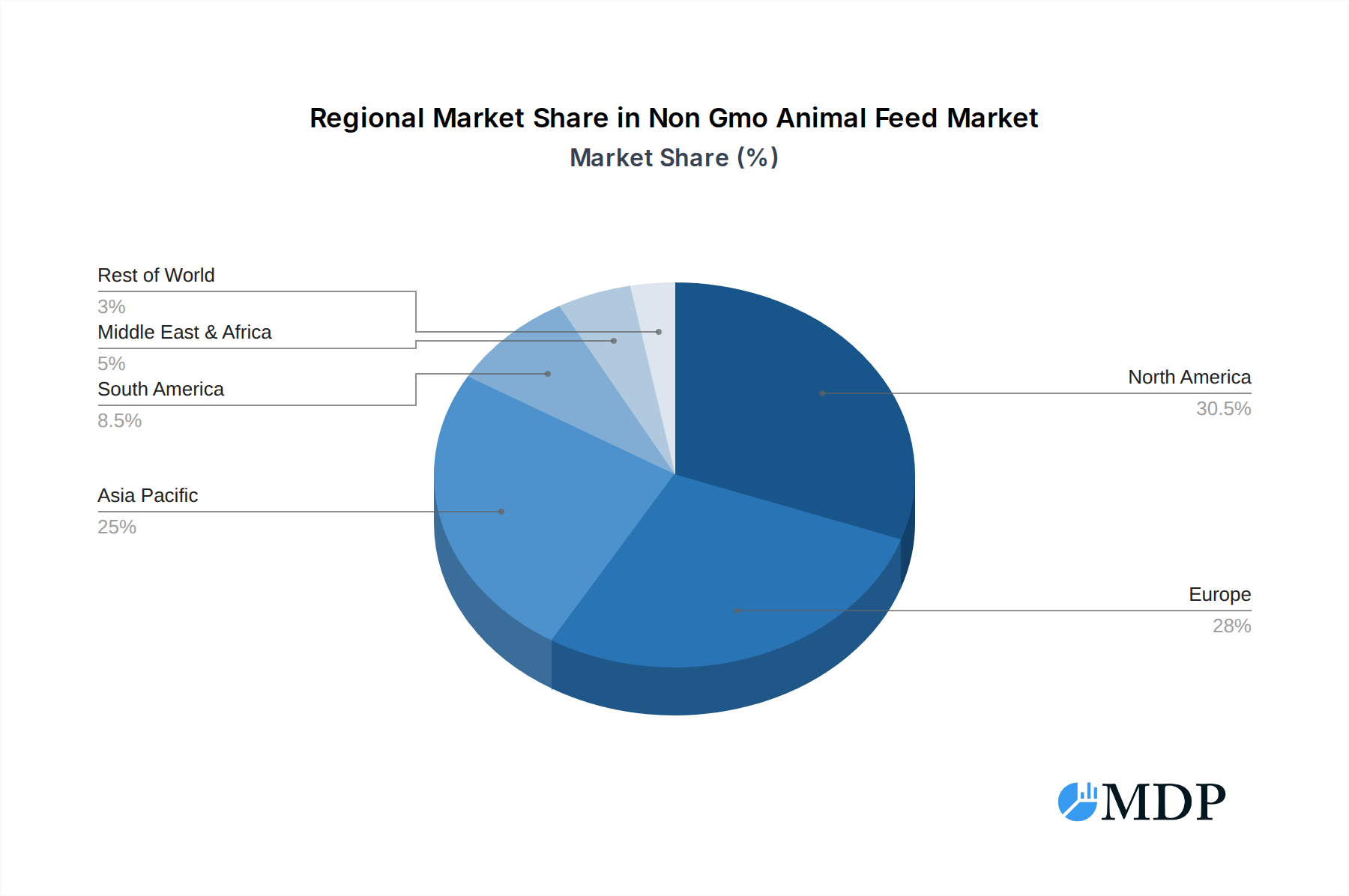

The Asia-Pacific region is emerging as a dominant market in the non-GMO animal feed sector, driven by rapidly growing populations, increasing disposable incomes, and a heightened consumer focus on health and safety in countries like China and India. Within this region, Chicken feed represents the largest application segment, accounting for an estimated xx% of the total market value in 2025. This dominance is attributed to the widespread consumption of poultry products and the proactive adoption of non-GMO feed by major poultry producers seeking to differentiate their products and meet consumer expectations.

Dominance Drivers in Asia-Pacific:

- Economic Policies: Supportive government initiatives promoting sustainable agriculture and food safety standards.

- Infrastructure Development: Enhanced logistics and supply chain networks facilitating the distribution of specialized non-GMO feed ingredients.

- Rising Disposable Incomes: Increased consumer spending power translates to a greater willingness to pay a premium for non-GMO certified food products.

- Urbanization: Concentration of consumer bases in urban centers with higher awareness of health and nutrition trends.

Dominance Drivers in Chicken Segment:

- High Consumption Rates: Poultry is a staple protein source, leading to substantial demand for feed.

- Brand Differentiation: Poultry producers are actively using non-GMO feed as a key marketing tool.

- Disease Prevention: Non-GMO diets are sometimes associated with improved gut health in poultry, reducing the need for antibiotics.

- Supply Chain Integration: Major feed manufacturers have established robust supply chains for non-GMO Corn and Soybeans, the primary components of chicken feed.

Furthermore, Soybeans and Corn remain the most significant types of non-GMO feed ingredients due to their widespread availability and suitability for various animal species, holding a combined market share of approximately xx% in 2025. The continuous innovation in processing and sourcing these crops ensures their continued relevance in the non-GMO feed market. The influence of companies like 2 Sisters Food Group in the poultry sector underscores the importance of this segment.

Non Gmo Animal Feed Product Developments

Product development in the non-GMO animal feed market is characterized by a focus on enhancing animal health, optimizing feed conversion ratios, and achieving specific nutritional profiles without relying on genetically modified ingredients. Innovations often involve exploring diverse protein sources, functional ingredients for gut health and immunity, and optimized blends of non-GMO grains like Field Peas, Corn, Milo, and Soybeans. Companies are investing in research and development to create customized feed solutions for Beef Cattle, Turkeys, Chicken, Goats, and Horses, offering competitive advantages through improved animal performance and reduced reliance on antibiotics.

Key Drivers of Non Gmo Animal Feed Growth

The non-GMO animal feed market's growth is propelled by a confluence of powerful drivers. Consumer demand for transparent and natural food production, coupled with increasing awareness of potential health and environmental impacts of GMOs, is a primary catalyst. Supportive regulatory frameworks and labeling initiatives that encourage or mandate non-GMO claims further stimulate market adoption. Technological advancements in agriculture, leading to more accessible and cost-effective non-GMO crop cultivation and processing, also play a crucial role. Economic factors, such as the premium pricing consumers are willing to pay for non-GMO products, create a favorable market environment for feed producers who can meet these demands.

Challenges in the Non Gmo Animal Feed Market

Despite its robust growth, the non-GMO animal feed market faces several challenges. Regulatory hurdles related to the definition and certification of non-GMO products can vary significantly across regions, creating complexities for international trade and market entry. Supply chain issues, including the availability and consistent quality of non-GMO raw materials, can impact production costs and availability. Competitive pressures from established conventional feed producers, who may offer lower price points, also pose a restraint. Furthermore, consumer education remains vital to differentiate genuinely non-GMO products from misleading claims and to justify the often higher price point associated with non-GMO feed.

Emerging Opportunities in Non Gmo Animal Feed

Emerging opportunities in the non-GMO animal feed market are primarily driven by technological breakthroughs and strategic market expansion. The development of novel, sustainable protein sources beyond traditional crops, such as insect protein and algae-based ingredients, offers exciting avenues for innovation. Strategic partnerships between feed manufacturers, farmers, and certification bodies are crucial for building robust and trusted non-GMO supply chains. Furthermore, the growing global demand for sustainably produced meat, dairy, and eggs presents significant market expansion opportunities, particularly in developing economies where awareness of non-GMO benefits is steadily increasing.

Leading Players in the Non Gmo Animal Feed Sector

- Kraft Heinz

- Givaudan

- Unilever

- ConAgra

- 2 Sisters Food Group

- Nestle

- The Hain Celestial Group

- General Mills

- Dr. Schar

- Epermarket

Key Milestones in Non Gmo Animal Feed Industry

- 2019: Increased global focus on non-GMO labeling regulations, prompting greater industry adoption.

- 2020: Significant rise in consumer surveys highlighting preference for non-GMO animal products.

- 2021: Major agricultural biotechnology companies announce expanded portfolios of non-GMO seed varieties.

- 2022: Several large-scale poultry and cattle producers commit to sourcing 100% non-GMO feed.

- 2023: Growing number of independent third-party non-GMO certifications gain traction in the market.

- 2024: Innovations in alternative protein sources for animal feed gain momentum.

Strategic Outlook for Non Gmo Animal Feed Market

The strategic outlook for the non-GMO animal feed market is exceptionally positive, characterized by sustained growth accelerators. The increasing consumer demand for transparency, coupled with a growing emphasis on animal welfare and sustainable agriculture, will continue to drive market expansion. Companies that can effectively leverage technological innovations in feed formulation, secure reliable non-GMO supply chains, and build strong brand credibility through robust certifications will be well-positioned for success. Strategic partnerships and market penetration into emerging economies represent significant growth opportunities, solidifying the non-GMO animal feed market's role in shaping the future of food production.

Non Gmo Animal Feed Segmentation

-

1. Application

- 1.1. Beef Cattle

- 1.2. Turkeys

- 1.3. Chicken

- 1.4. Goats

- 1.5. Horses

- 1.6. Other

-

2. Type

- 2.1. Field Peas

- 2.2. Corn

- 2.3. Milo

- 2.4. Soybeans

- 2.5. Other

Non Gmo Animal Feed Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Non Gmo Animal Feed Regional Market Share

Geographic Coverage of Non Gmo Animal Feed

Non Gmo Animal Feed REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Non Gmo Animal Feed Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Beef Cattle

- 5.1.2. Turkeys

- 5.1.3. Chicken

- 5.1.4. Goats

- 5.1.5. Horses

- 5.1.6. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Field Peas

- 5.2.2. Corn

- 5.2.3. Milo

- 5.2.4. Soybeans

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Non Gmo Animal Feed Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Beef Cattle

- 6.1.2. Turkeys

- 6.1.3. Chicken

- 6.1.4. Goats

- 6.1.5. Horses

- 6.1.6. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Field Peas

- 6.2.2. Corn

- 6.2.3. Milo

- 6.2.4. Soybeans

- 6.2.5. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Non Gmo Animal Feed Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Beef Cattle

- 7.1.2. Turkeys

- 7.1.3. Chicken

- 7.1.4. Goats

- 7.1.5. Horses

- 7.1.6. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Field Peas

- 7.2.2. Corn

- 7.2.3. Milo

- 7.2.4. Soybeans

- 7.2.5. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Non Gmo Animal Feed Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Beef Cattle

- 8.1.2. Turkeys

- 8.1.3. Chicken

- 8.1.4. Goats

- 8.1.5. Horses

- 8.1.6. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Field Peas

- 8.2.2. Corn

- 8.2.3. Milo

- 8.2.4. Soybeans

- 8.2.5. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Non Gmo Animal Feed Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Beef Cattle

- 9.1.2. Turkeys

- 9.1.3. Chicken

- 9.1.4. Goats

- 9.1.5. Horses

- 9.1.6. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Field Peas

- 9.2.2. Corn

- 9.2.3. Milo

- 9.2.4. Soybeans

- 9.2.5. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Non Gmo Animal Feed Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Beef Cattle

- 10.1.2. Turkeys

- 10.1.3. Chicken

- 10.1.4. Goats

- 10.1.5. Horses

- 10.1.6. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Field Peas

- 10.2.2. Corn

- 10.2.3. Milo

- 10.2.4. Soybeans

- 10.2.5. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Kraft Heinz

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Givaudan

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Unilever

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ConAgra

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 2 Sisters Food Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Nestle

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 The Hain Celestial Group

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 General Mills

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Dr. Schar

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Epermarket

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Kraft Heinz

List of Figures

- Figure 1: Global Non Gmo Animal Feed Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Non Gmo Animal Feed Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Non Gmo Animal Feed Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Non Gmo Animal Feed Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Non Gmo Animal Feed Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Non Gmo Animal Feed Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Non Gmo Animal Feed Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Non Gmo Animal Feed Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Non Gmo Animal Feed Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Non Gmo Animal Feed Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Non Gmo Animal Feed Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Non Gmo Animal Feed Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Non Gmo Animal Feed Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Non Gmo Animal Feed Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Non Gmo Animal Feed Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Non Gmo Animal Feed Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Non Gmo Animal Feed Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Non Gmo Animal Feed Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Non Gmo Animal Feed Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Non Gmo Animal Feed Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Non Gmo Animal Feed Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Non Gmo Animal Feed Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Non Gmo Animal Feed Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Non Gmo Animal Feed Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Non Gmo Animal Feed Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Non Gmo Animal Feed Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Non Gmo Animal Feed Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Non Gmo Animal Feed Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Non Gmo Animal Feed Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Non Gmo Animal Feed Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Non Gmo Animal Feed Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Non Gmo Animal Feed Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Non Gmo Animal Feed Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Non Gmo Animal Feed Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Non Gmo Animal Feed Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Non Gmo Animal Feed Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Non Gmo Animal Feed Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Non Gmo Animal Feed Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Non Gmo Animal Feed Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Non Gmo Animal Feed Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Non Gmo Animal Feed Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Non Gmo Animal Feed Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Non Gmo Animal Feed Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Non Gmo Animal Feed Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Non Gmo Animal Feed Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Non Gmo Animal Feed Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Non Gmo Animal Feed Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Non Gmo Animal Feed Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Non Gmo Animal Feed Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Non Gmo Animal Feed Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Non Gmo Animal Feed?

The projected CAGR is approximately 7%.

2. Which companies are prominent players in the Non Gmo Animal Feed?

Key companies in the market include Kraft Heinz, Givaudan, Unilever, ConAgra, 2 Sisters Food Group, Nestle, The Hain Celestial Group, General Mills, Dr. Schar, Epermarket.

3. What are the main segments of the Non Gmo Animal Feed?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Non Gmo Animal Feed," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Non Gmo Animal Feed report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Non Gmo Animal Feed?

To stay informed about further developments, trends, and reports in the Non Gmo Animal Feed, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence