Key Insights

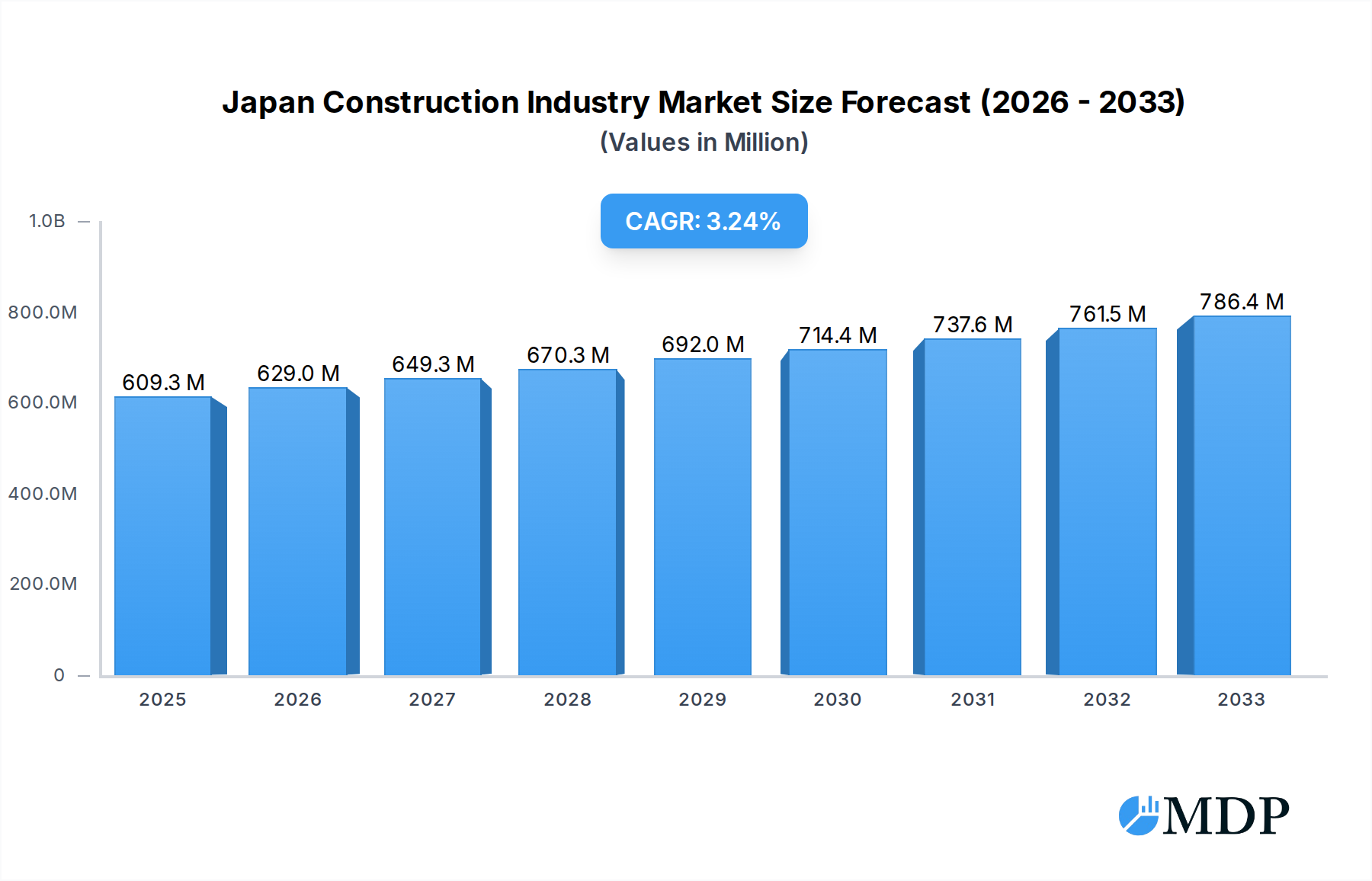

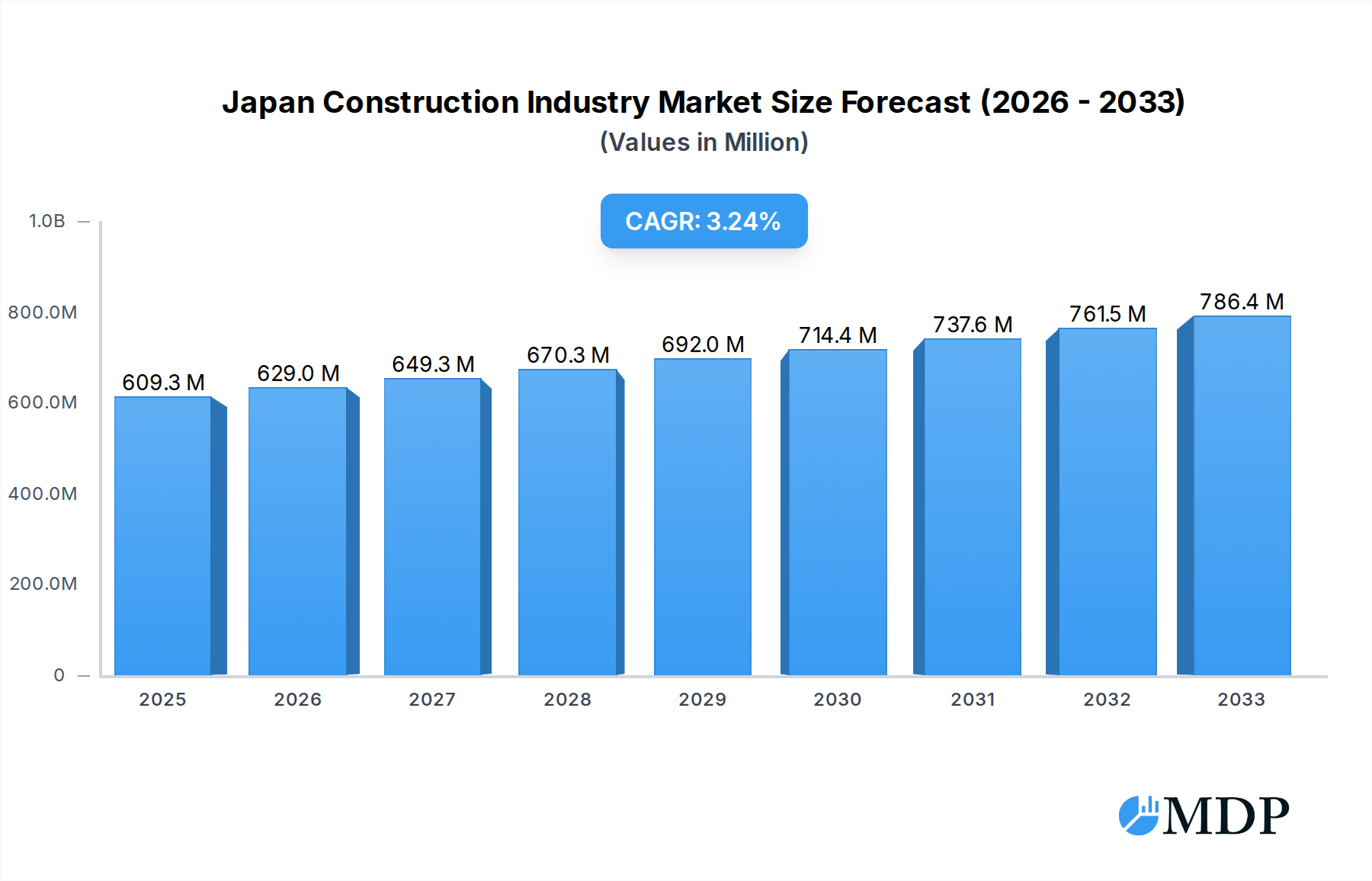

The Japan construction industry is poised for steady growth, with a current market size estimated at 609.27 Million in 2025. This expansion is underpinned by a projected Compound Annual Growth Rate (CAGR) of 3.30% from 2019 to 2033. Key drivers propelling this market include significant investments in infrastructure development, particularly in transportation networks, to address aging facilities and accommodate future needs. Furthermore, ongoing urban regeneration projects and the demand for sustainable, energy-efficient buildings across residential, commercial, and industrial sectors are contributing to sustained momentum. The government's focus on rebuilding and modernizing after natural disasters, alongside a growing emphasis on smart city initiatives, also presents substantial opportunities for growth and innovation within the sector.

Japan Construction Industry Market Size (In Million)

Despite the positive outlook, the industry faces certain restraints. An aging workforce and a potential shortage of skilled labor could pose challenges to meeting the increasing demand. Additionally, stringent environmental regulations and the rising costs of raw materials might influence project timelines and profitability. Nevertheless, emerging trends such as the adoption of advanced construction technologies, including Building Information Modeling (BIM) and prefabrication, are expected to enhance efficiency and mitigate some of these challenges. The increasing focus on green construction and the development of resilient infrastructure in response to climate change further shape the landscape, creating a dynamic environment for key players like Obayashi Corp, Shimizu Corp, and Sumitomo Mitsui Construction Co Ltd. The market segmentation reveals a balanced distribution across residential, commercial, industrial, infrastructure (transportation), and energy & utilities, with each segment contributing to the overall market vitality.

Japan Construction Industry Company Market Share

This comprehensive report delves into the dynamic Japan Construction Industry, offering an in-depth analysis of market dynamics, key trends, leading players, and future opportunities. Spanning a study period from 2019 to 2033, with a base and estimated year of 2025, this report provides actionable insights for stakeholders navigating the evolving landscape of Japanese construction. We explore critical sectors including Residential, Commercial, Industrial, Infrastructure (Transportation), and Energy and Utilities, highlighting major industry developments and their impact.

Japan Construction Industry Market Dynamics & Concentration

The Japan Construction Industry exhibits a moderate to high market concentration, with a few dominant players like Obayashi Corp, Shimizu Corp, and Kajima Corp holding significant market share. For instance, Obayashi Corp is estimated to hold a market share of approximately 8%, with Shimizu Corp and Kajima Corp close behind. The Zenitaka Corp and Sumitomo Mitsui Construction Co Ltd also command substantial portions of the market. Innovation drivers are primarily fueled by the demand for advanced earthquake-resistant technologies, sustainable building practices, and smart city integration, pushing companies to invest in R&D. Regulatory frameworks, particularly those concerning safety standards and environmental compliance, are stringent and play a crucial role in shaping market entry and operational strategies. Product substitutes are gradually emerging in the form of pre-fabricated and modular construction methods, offering faster build times and cost efficiencies, although traditional on-site construction remains dominant. End-user trends are shifting towards energy-efficient buildings, smart homes, and adaptable commercial spaces. Mergers and acquisition (M&A) activities, while not at peak levels, are observed as companies seek to consolidate their market position, acquire new technologies, or expand their service offerings. The number of significant M&A deals in the past five years is estimated to be around 35-45, with deal values often in the hundreds of millions of dollars.

Japan Construction Industry Industry Trends & Analysis

The Japan Construction Industry is experiencing robust growth, driven by a confluence of economic, technological, and demographic factors. The Compound Annual Growth Rate (CAGR) for the forecast period (2025–2033) is projected to be around 4.5%. This growth is underpinned by significant government investment in infrastructure development, particularly in transportation networks and disaster resilience measures, a direct response to historical events and the nation's geographic vulnerabilities. The Residential sector is witnessing a sustained demand for new housing, coupled with a growing emphasis on renovation and retrofitting of existing properties to meet higher energy efficiency standards and accommodate an aging population. Smart home technology integration is rapidly increasing, boosting market penetration for advanced construction materials and integrated systems. In the Commercial sector, there's a noticeable trend towards mixed-use developments and the modernization of office spaces to attract a hybrid workforce, leading to increased demand for flexible and technologically advanced building solutions. The Industrial sector is being shaped by the resurgence of manufacturing and the growing need for advanced logistics and data centers, requiring specialized construction expertise. Technological disruptions are profoundly impacting the industry, with the adoption of Building Information Modeling (BIM) becoming standard practice, enhancing design accuracy, collaboration, and project management. Robotics and automation are being increasingly employed in construction sites to improve efficiency, safety, and address labor shortages. Furthermore, the push for sustainability is driving innovation in green building materials, modular construction, and energy-efficient designs, significantly influencing consumer preferences and regulatory mandates. Competitive dynamics are characterized by intense rivalry among established giants and the growing influence of specialized technology providers and material suppliers. The market penetration of sustainable construction practices is estimated to reach 60% by 2030.

Leading Markets & Segments in Japan Construction Industry

The Infrastructure (Transportation) segment stands out as a dominant force within the Japan Construction Industry, propelled by substantial government initiatives and ongoing urban development projects. This dominance is further amplified by the nation's strategic focus on enhancing its transportation networks for both domestic connectivity and international trade. Key drivers include the continuous need for high-speed rail expansion, the modernization of airports and seaports, and the implementation of smart traffic management systems. Economic policies that prioritize infrastructure renewal and expansion, particularly in preparation for and recovery from natural disasters, directly fuel investments in this segment. For instance, the Japanese government's commitment to rebuilding and reinforcing infrastructure post-earthquakes and typhoons translates into billions of dollars of construction contracts annually.

- Infrastructure (Transportation): This segment is projected to account for approximately 35% of the total market value during the forecast period. The development of the Chuo Shinkansen (Maglev) line is a prime example of a mega-project significantly boosting this sector.

- Residential Sector: While stable, it experiences fluctuations based on demographic shifts and housing demand. Renovation and retrofitting of existing homes, driven by an aging population and sustainability mandates, contribute significantly.

- Commercial Sector: Characterized by urban redevelopment and the growth of mixed-use properties, particularly in major metropolitan areas like Tokyo and Osaka. The demand for flexible and technologically advanced office spaces is a key trend.

- Industrial Sector: Driven by the demand for advanced manufacturing facilities, logistics hubs, and data centers, reflecting Japan's technological prowess and evolving supply chain needs.

- Energy and Utilities: This segment is experiencing growth due to investments in renewable energy sources and the modernization of existing power infrastructure, aligning with national decarbonization goals.

Japan Construction Industry Product Developments

Product innovation in the Japan Construction Industry is heavily influenced by the pursuit of safety, sustainability, and efficiency. Advanced earthquake-resistant materials, self-healing concrete, and modular construction systems are gaining traction, offering enhanced structural integrity and reduced environmental impact. Smart building technologies, including integrated IoT sensors for environmental monitoring and energy management, are becoming standard, creating competitive advantages through improved building performance and occupant comfort. The application of these innovations spans all sectors, from resilient residential homes to energy-efficient commercial spaces and robust industrial facilities.

Key Drivers of Japan Construction Industry Growth

The Japan Construction Industry is propelled by several significant growth drivers. Technological advancements, such as the widespread adoption of Building Information Modeling (BIM) and the increasing use of robotics and AI in construction, are enhancing efficiency and safety. Favorable economic policies, including substantial government investment in infrastructure renewal and disaster preparedness, create consistent demand. Regulatory frameworks that promote sustainable building practices and energy efficiency encourage innovation in green construction materials and techniques. Furthermore, demographic shifts, including an aging population and urbanization, drive demand for specialized housing solutions and urban redevelopment projects.

Challenges in the Japan Construction Industry Market

Despite robust growth, the Japan Construction Industry faces several challenges. A persistent labor shortage, exacerbated by an aging workforce and declining birth rates, is a critical restraint, potentially increasing labor costs and project timelines. Stringent regulatory hurdles and the complex approval processes for new construction projects can also lead to delays and increased administrative burdens. Supply chain disruptions, particularly for specialized materials and equipment, can impact project schedules and costs. Competitive pressures from both domestic and international players, especially in large-scale infrastructure projects, necessitate continuous innovation and cost optimization strategies. The estimated impact of labor shortages on project completion timelines can range from 10% to 20%.

Emerging Opportunities in Japan Construction Industry

Emerging opportunities within the Japan Construction Industry are centered on technological innovation and the growing demand for sustainable and resilient infrastructure. The push towards carbon neutrality is creating significant demand for green building solutions, renewable energy installations, and energy-efficient retrofitting projects. The ongoing digital transformation, including the wider adoption of AI, IoT, and advanced analytics in construction, presents opportunities for improved project management, predictive maintenance, and enhanced building performance. Strategic partnerships between traditional construction firms and technology providers are likely to accelerate the development and deployment of cutting-edge solutions. Furthermore, the development of smart cities and the continuous need for urban regeneration projects offer substantial long-term growth potential.

Leading Players in the Japan Construction Industry Sector

- Obayashi Corp

- The Zenitaka Corp

- Shimizu Corp

- Toshiba Corp

- Takada Corporation

- Kajima Corp

- Nippon Concrete Industries

- Sumitomo Mitsui Construction Co Ltd

- Mori Building Co Ltd

- Mitsubishi Heavy Industries Ltd

Key Milestones in Japan Construction Industry Industry

- 2019: Increased government focus on infrastructure resilience and disaster preparedness following a series of natural disasters, leading to increased project funding.

- 2020: Accelerated adoption of BIM and digital construction technologies due to the need for remote collaboration and enhanced efficiency during the COVID-19 pandemic.

- 2021: Growing investment in renewable energy infrastructure, driven by national climate targets and a push for energy independence.

- 2022: Introduction of new regulations promoting energy-efficient building standards, spurring innovation in sustainable construction materials and practices.

- 2023: Significant progress in the development of smart city initiatives and smart infrastructure projects, integrating IoT and AI technologies.

- 2024: Continued emphasis on retrofitting and renovating existing buildings to meet modern safety and sustainability standards, addressing an aging building stock.

Strategic Outlook for Japan Construction Industry Market

The strategic outlook for the Japan Construction Industry is characterized by sustained growth, driven by a commitment to technological advancement, sustainability, and robust infrastructure development. The industry is poised to benefit from continued government investment in transportation, disaster resilience, and renewable energy. The increasing integration of digital technologies, such as AI and robotics, will be crucial for enhancing productivity and addressing labor challenges. Companies that focus on developing and implementing green building solutions, smart infrastructure, and innovative modular construction techniques will be well-positioned for future success. Strategic collaborations and a proactive approach to regulatory changes will be key accelerators for market expansion and long-term profitability.

Japan Construction Industry Segmentation

-

1. Sector

- 1.1. Residential

- 1.2. Commercial

- 1.3. Industrial

- 1.4. Infrastruture (Transportation)

- 1.5. Energy and Utilities

Japan Construction Industry Segmentation By Geography

- 1. Japan

Japan Construction Industry Regional Market Share

Geographic Coverage of Japan Construction Industry

Japan Construction Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.30% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Residential

- 5.1.2. Commercial

- 5.1.3. Industrial

- 5.1.4. Infrastruture (Transportation)

- 5.1.5. Energy and Utilities

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Japan Construction Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 6.1.1. Residential

- 6.1.2. Commercial

- 6.1.3. Industrial

- 6.1.4. Infrastruture (Transportation)

- 6.1.5. Energy and Utilities

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Obayashi Corp

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 The Zenitaka Corp

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Shimizu Corp **List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Toshiba Corp

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Takada Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Kajima Corp

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Nippon Concrete Industries

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Sumitomo Mitsui Construction Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Mori Building Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Mitsubishi Heavy Industries Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Obayashi Corp

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Japan Construction Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Japan Construction Industry Share (%) by Company 2025

List of Tables

- Table 1: Japan Construction Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 2: Japan Construction Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Japan Construction Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 4: Japan Construction Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Construction Industry?

The projected CAGR is approximately 3.30%.

2. Which companies are prominent players in the Japan Construction Industry?

Key companies in the market include Obayashi Corp, The Zenitaka Corp, Shimizu Corp **List Not Exhaustive, Toshiba Corp, Takada Corporation, Kajima Corp, Nippon Concrete Industries, Sumitomo Mitsui Construction Co Ltd, Mori Building Co Ltd, Mitsubishi Heavy Industries Ltd.

3. What are the main segments of the Japan Construction Industry?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 609.27 Million as of 2022.

5. What are some drivers contributing to market growth?

Growth of Education Sector; Rising Demand for Quality Accomodation.

6. What are the notable trends driving market growth?

Increase in Infrastructure Developments Boosting the Market.

7. Are there any restraints impacting market growth?

Enrolment Fluctuations.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Construction Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Construction Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Construction Industry?

To stay informed about further developments, trends, and reports in the Japan Construction Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence