Key Insights

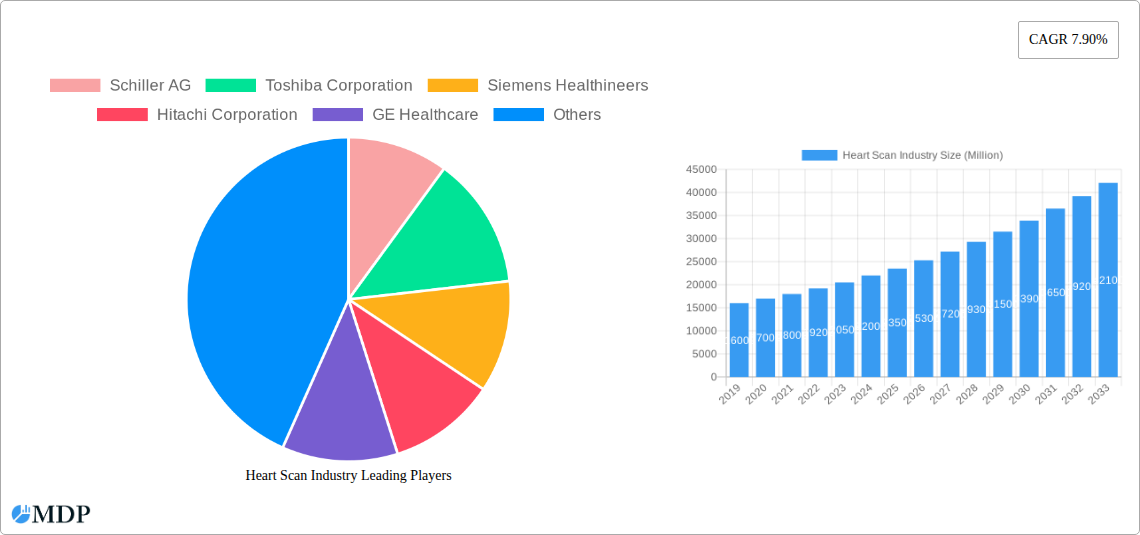

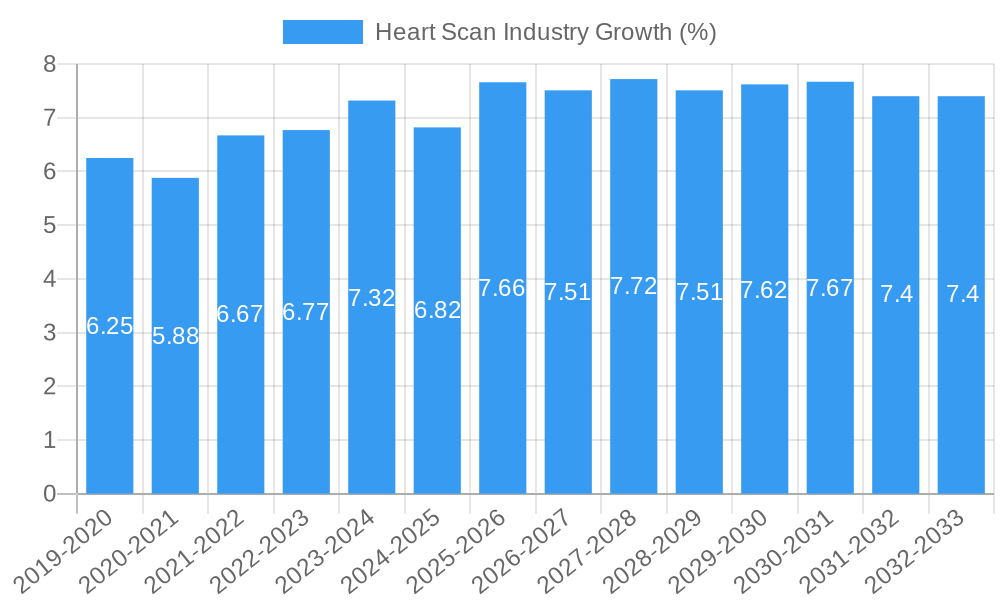

The global Heart Scan Industry is poised for robust growth, projected to reach a market size of approximately $25,000 million by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 7.90% through 2033. This expansion is primarily fueled by the increasing prevalence of cardiovascular diseases (CVDs) worldwide, a growing elderly population susceptible to cardiac issues, and significant advancements in diagnostic imaging technologies. Early detection and preventative care are gaining prominence, driving demand for sophisticated heart scanning solutions. Key drivers include heightened awareness campaigns for CVDs, improved healthcare infrastructure, and increased investment in research and development for more accurate and less invasive diagnostic tools. The integration of artificial intelligence (AI) and machine learning (ML) in interpreting scan results is another transformative trend, enhancing diagnostic precision and efficiency. Furthermore, the growing adoption of these advanced diagnostic tools in both hospital settings and ambulatory surgical centers is contributing to market momentum.

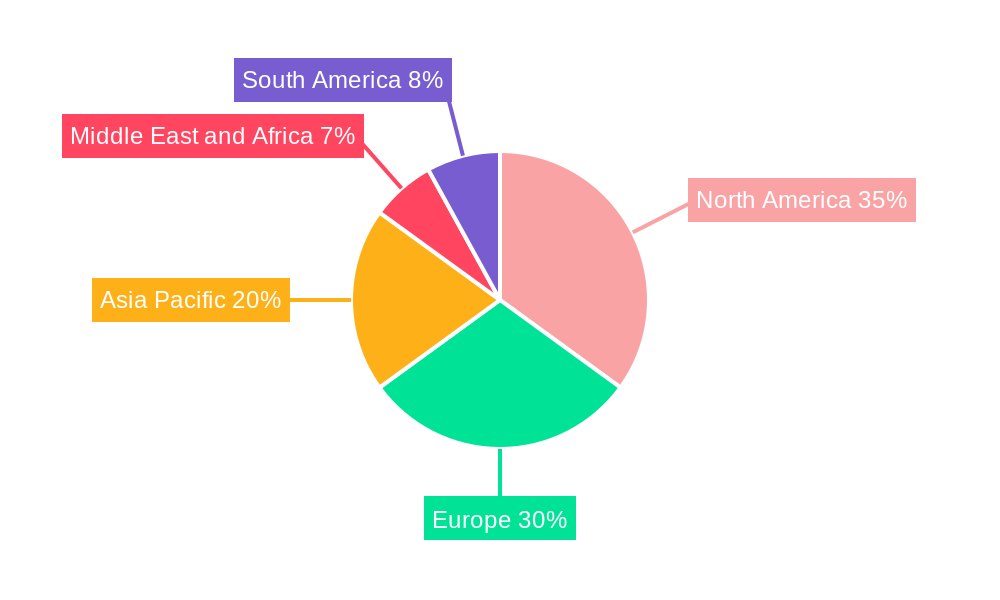

The market, however, faces certain restraints. High costs associated with advanced cardiac imaging equipment and the need for specialized training for healthcare professionals can pose challenges, particularly in developing economies. Stringent regulatory approvals for new medical devices also add to the market entry barriers for new players. Despite these hurdles, the market's segmentation reveals strong performance across various diagnostic tests, with Electrocardiograms (ECG) and Blood Tests remaining foundational, while Angiograms and Computerized Cardiac Tomography (CCT) show significant growth potential due to their advanced diagnostic capabilities. Hospitals are expected to remain the dominant end-user segment, followed closely by diagnostic centers, as the emphasis on accurate and timely cardiac assessment intensifies. Geographically, North America and Europe are leading the market, driven by advanced healthcare systems and high adoption rates of new technologies, while the Asia Pacific region presents a substantial growth opportunity due to its large population and increasing healthcare expenditure.

Heart Scan Industry: Comprehensive Market Analysis, Trends, and Future Outlook (2019-2033)

Unlock critical insights into the burgeoning Heart Scan Industry with this in-depth report. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this analysis provides a detailed examination of market dynamics, technological advancements, key players, and future growth trajectories. Discover the market share of leading companies, the impact of innovative diagnostic tests like Electrocardiograms and advanced Computed Cardiac Tomography, and the evolving preferences of end-users such as Hospitals and Diagnostic Centers. This report is an essential resource for stakeholders seeking to understand and capitalize on the opportunities within the global cardiovascular diagnostics market.

Heart Scan Industry Market Dynamics & Concentration

The Heart Scan Industry is characterized by a moderate to high concentration, with a few dominant players like Siemens Healthineers, GE Healthcare, and Koninklijke Philips NV holding substantial market share. These companies invest heavily in research and development, driving innovation in cardiovascular imaging and diagnostics. The primary innovation drivers include the increasing prevalence of cardiovascular diseases (CVDs), rising healthcare expenditure, and a growing demand for minimally invasive diagnostic procedures. Regulatory frameworks, such as stringent FDA approvals for new diagnostic devices and tests, play a significant role in shaping market entry and product lifecycle. Product substitutes, including traditional risk assessment methods and less advanced imaging techniques, exist but are increasingly being outpaced by the accuracy and efficiency of advanced heart scan technologies. End-user trends reveal a growing preference for integrated diagnostic solutions and point-of-care testing, especially within Hospitals and specialized Diagnostic Centers. Mergers and Acquisitions (M&A) activities are moderately frequent, aimed at consolidating market share, acquiring innovative technologies, and expanding geographic reach. For example, recent M&A deals in the broader medical diagnostics sector have seen private equity firms acquiring smaller players to enhance their portfolio. The overall market share distribution sees Siemens Healthineers at approximately 18%, GE Healthcare at 16%, and Koninklijke Philips NV at 14%, with other key players like Toshiba Corporation and Hitachi Corporation vying for the remaining significant portions. M&A deal counts have averaged around 8-12 significant transactions annually in the last three years, impacting market concentration and competitive landscape.

Heart Scan Industry Industry Trends & Analysis

The Heart Scan Industry is poised for robust growth, driven by a confluence of technological advancements, increasing global healthcare spending, and a growing awareness of cardiovascular health. The Compound Annual Growth Rate (CAGR) for the forecast period (2025-2033) is projected to be approximately 8.5%, reflecting the escalating demand for sophisticated diagnostic tools. Market penetration of advanced heart scan technologies is rapidly increasing, moving beyond specialized cardiology departments into primary care settings and remote diagnostic hubs. Key growth drivers include the escalating global burden of cardiovascular diseases, which remain the leading cause of mortality worldwide, and the subsequent imperative for early detection and intervention. Technological disruptions are at the forefront of this evolution, with innovations in artificial intelligence (AI) for image analysis, machine learning for predictive diagnostics, and miniaturization of imaging devices enabling more accessible and efficient screenings. Consumer preferences are shifting towards proactive health management, leading to a greater uptake of preventative screenings and advanced diagnostic tests even in the absence of overt symptoms. The competitive dynamics are intensifying, with established giants competing against agile startups introducing novel AI-powered solutions. The integration of digital health platforms and telemedicine further enhances the reach and utility of heart scan services, democratizing access to advanced cardiac care. The increasing adoption of non-invasive imaging modalities over traditional angiography is also a significant trend, contributing to patient comfort and reduced recovery times. The global market size for heart scans was estimated to be $12.5 Billion in 2025, with significant growth anticipated. Factors such as an aging global population and the prevalence of lifestyle-related risk factors for heart disease (obesity, diabetes, hypertension) are expected to fuel demand for diagnostic imaging and testing solutions for years to come.

Leading Markets & Segments in Heart Scan Industry

The North American region currently dominates the Heart Scan Industry, largely propelled by high healthcare expenditure, advanced technological adoption, and well-established healthcare infrastructure. Within North America, the United States accounts for the largest market share due to its robust healthcare system and significant investment in cardiovascular research and development. The dominance of the Hospitals end-user segment is undeniable, accounting for an estimated 55% of the market revenue. Hospitals are the primary centers for complex cardiac procedures and diagnostics, investing heavily in state-of-the-art imaging equipment and diagnostic labs.

- Key Drivers for Hospital Dominance:

- Integrated Care Pathways: Hospitals offer a comprehensive approach to cardiac care, from initial screening to complex interventions and rehabilitation, necessitating a wide array of diagnostic tools.

- Technological Investment: Significant capital allocation towards advanced imaging modalities like Computed Cardiac Tomography (CCT) and Magnetic Resonance Imaging (MRI) for detailed cardiac assessment.

- Reimbursement Policies: Favorable reimbursement structures for diagnostic procedures performed within hospital settings.

- Skilled Workforce: Availability of trained cardiologists, radiologists, and technicians to operate and interpret advanced heart scan equipment.

The Computarized Cardiac Tomography (CCT) segment within the "Test" category is a significant growth driver, projected to capture an impressive market share of approximately 30% by 2025. This is due to its superior ability to visualize coronary arteries, assess plaque burden, and detect subtle abnormalities that might be missed by other modalities.

- Key Drivers for CCT Dominance:

- Non-invasiveness and Speed: Offers detailed anatomical and functional information without the need for invasive catheterization in many cases.

- Early Disease Detection: Effective in identifying early signs of atherosclerosis and cardiovascular risk.

- Technological Advancements: Innovations in detector technology, dose reduction techniques, and image reconstruction algorithms enhance diagnostic accuracy and patient safety.

- Increasing Clinical Adoption: Growing evidence supporting the clinical utility of CCT in various patient populations.

Other crucial segments include Diagnostic Centers, which are experiencing rapid expansion as outpatient imaging services become more prevalent, and Ambulatory Surgical Centers, focusing on less invasive procedures requiring pre-operative cardiac assessments. The Electrocardiogram (ECG) remains a fundamental and widely used diagnostic tool, albeit with a mature market share, while Angiogram procedures, though invasive, continue to be vital for interventional cardiology. The "Other Tests" category encompasses emerging technologies and specialized cardiac assessments.

Heart Scan Industry Product Developments

The Heart Scan Industry is witnessing a wave of innovative product developments focused on enhancing diagnostic accuracy, improving patient comfort, and streamlining workflows. Key trends include the integration of artificial intelligence (AI) for automated image analysis and risk prediction, allowing for faster and more precise diagnoses. Advanced spectral imaging technologies in CT scanners are providing richer tissue characterization, while novel ultrasound probes are enabling higher resolution and deeper tissue penetration. Furthermore, the development of portable and point-of-care diagnostic devices is expanding access to cardiac screening, particularly in remote areas and primary care settings. These advancements contribute to a competitive advantage by offering superior clinical insights and improved patient outcomes.

Key Drivers of Heart Scan Industry Growth

The substantial growth in the Heart Scan Industry is propelled by several interconnected factors. Technological advancements are paramount, with innovations in AI, machine learning, and advanced imaging hardware continuously improving diagnostic capabilities. The increasing global prevalence of cardiovascular diseases, driven by an aging population and lifestyle factors, fuels the demand for early and accurate detection. Rising healthcare expenditure worldwide allows for greater investment in advanced medical technologies and diagnostic services. Furthermore, supportive government initiatives and regulatory frameworks promoting early disease detection and preventative healthcare, alongside favorable reimbursement policies for diagnostic procedures, are significant catalysts. The growing awareness among the public regarding the importance of cardiovascular health also contributes to increased utilization of heart scan services.

Challenges in the Heart Scan Industry Market

Despite its strong growth trajectory, the Heart Scan Industry faces several significant challenges. High initial investment costs for advanced imaging equipment can be a barrier, particularly for smaller healthcare providers and in developing economies. Stringent regulatory approval processes for new devices and diagnostic tests, while ensuring safety and efficacy, can lead to lengthy market entry timelines. Data security and privacy concerns are paramount with the increasing digitalization of patient data and the use of cloud-based solutions. Reimbursement complexities and variability across different healthcare systems and regions can impact market access and profitability. Lastly, the shortage of skilled personnel, including trained radiologists and cardiac sonographers, can limit the effective deployment and utilization of advanced heart scan technologies.

Emerging Opportunities in Heart Scan Industry

The Heart Scan Industry is ripe with emerging opportunities driven by ongoing technological breakthroughs and evolving healthcare paradigms. The widespread adoption of artificial intelligence and machine learning algorithms presents a significant opportunity for predictive diagnostics and personalized treatment planning, moving beyond mere detection to proactive risk management. The expansion of telemedicine and remote monitoring solutions offers a pathway to democratize access to advanced cardiac care, reaching underserved populations and improving patient convenience. Strategic partnerships between technology providers, pharmaceutical companies, and healthcare institutions are crucial for developing integrated diagnostic and therapeutic solutions. Furthermore, the growing focus on preventative cardiology and population health management creates a sustained demand for accessible and cost-effective screening tools, opening avenues for novel, user-friendly heart scan devices.

Leading Players in the Heart Scan Industry Sector

- Schiller AG

- Toshiba Corporation

- Siemens Healthineers

- Hitachi Corporation

- GE Healthcare

- F Hoffmann-La Roche Ltd

- Midmark Corporation

- Koninklijke Philips NV

- AstraZeneca PLC

- Welch Allyn Inc

Key Milestones in Heart Scan Industry Industry

- April 2021: Roche launched a series of five new intended uses for two key cardiac biomarkers, highly sensitive cardiac troponin T (cTnT-hs) and N-terminal pro-brain natriuretic peptide test (NT-proBNP), utilizing their Elecsys® technology. This expansion significantly enhances the diagnostic capabilities for a range of cardiac conditions.

- March 2021: The European Union approved the artificial intelligence-based CaRi-Heart Technology. Developed by the British Heart Foundation and Caristo Diagnostics, this groundbreaking technology can detect and predict the risk of severe heart attack years before it occurs, marking a significant advancement in preventative cardiology.

Strategic Outlook for Heart Scan Industry Market

The strategic outlook for the Heart Scan Industry is exceptionally positive, characterized by sustained innovation and expanding market reach. Future growth will be accelerated by the continued integration of AI and machine learning, leading to more predictive and personalized cardiac care. The increasing focus on non-invasive diagnostic modalities and the development of portable, point-of-care devices will broaden accessibility, particularly in emerging markets and primary care settings. Strategic collaborations between technology developers and healthcare providers will be crucial for creating end-to-end solutions, from early screening to sophisticated intervention. The growing emphasis on preventative health and the management of chronic cardiovascular diseases will ensure a consistent demand for advanced diagnostic tools, positioning the Heart Scan Industry for long-term expansion and significant impact on global health outcomes.

Heart Scan Industry Segmentation

-

1. Test

- 1.1. Electrocardiogram

- 1.2. Blood Tests

- 1.3. Angiogram

- 1.4. Computarized Cardiac Tomography

- 1.5. Other Tests

-

2. End User

- 2.1. Hospitals

- 2.2. Ambulatory Surgical Centers

- 2.3. Diagnostic Centers

- 2.4. Other End Users

Heart Scan Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Heart Scan Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.90% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Technological Advancements; Significant Rise in Cardiovascular Diseases; Increase in Quality of Life

- 3.3. Market Restrains

- 3.3.1. Expensive Diagnostics Products; Lack of Skilled Workforce in the Hospitals and Other Areas

- 3.4. Market Trends

- 3.4.1. Rapid Blood Tests like Troponin Expected to Occupy a Significant Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Heart Scan Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Test

- 5.1.1. Electrocardiogram

- 5.1.2. Blood Tests

- 5.1.3. Angiogram

- 5.1.4. Computarized Cardiac Tomography

- 5.1.5. Other Tests

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Hospitals

- 5.2.2. Ambulatory Surgical Centers

- 5.2.3. Diagnostic Centers

- 5.2.4. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Test

- 6. North America Heart Scan Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Test

- 6.1.1. Electrocardiogram

- 6.1.2. Blood Tests

- 6.1.3. Angiogram

- 6.1.4. Computarized Cardiac Tomography

- 6.1.5. Other Tests

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Hospitals

- 6.2.2. Ambulatory Surgical Centers

- 6.2.3. Diagnostic Centers

- 6.2.4. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Test

- 7. Europe Heart Scan Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Test

- 7.1.1. Electrocardiogram

- 7.1.2. Blood Tests

- 7.1.3. Angiogram

- 7.1.4. Computarized Cardiac Tomography

- 7.1.5. Other Tests

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Hospitals

- 7.2.2. Ambulatory Surgical Centers

- 7.2.3. Diagnostic Centers

- 7.2.4. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Test

- 8. Asia Pacific Heart Scan Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Test

- 8.1.1. Electrocardiogram

- 8.1.2. Blood Tests

- 8.1.3. Angiogram

- 8.1.4. Computarized Cardiac Tomography

- 8.1.5. Other Tests

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Hospitals

- 8.2.2. Ambulatory Surgical Centers

- 8.2.3. Diagnostic Centers

- 8.2.4. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Test

- 9. Middle East and Africa Heart Scan Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Test

- 9.1.1. Electrocardiogram

- 9.1.2. Blood Tests

- 9.1.3. Angiogram

- 9.1.4. Computarized Cardiac Tomography

- 9.1.5. Other Tests

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Hospitals

- 9.2.2. Ambulatory Surgical Centers

- 9.2.3. Diagnostic Centers

- 9.2.4. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Test

- 10. South America Heart Scan Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Test

- 10.1.1. Electrocardiogram

- 10.1.2. Blood Tests

- 10.1.3. Angiogram

- 10.1.4. Computarized Cardiac Tomography

- 10.1.5. Other Tests

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Hospitals

- 10.2.2. Ambulatory Surgical Centers

- 10.2.3. Diagnostic Centers

- 10.2.4. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Test

- 11. North America Heart Scan Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 11.1.3 Mexico

- 12. Europe Heart Scan Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 Germany

- 12.1.2 United Kingdom

- 12.1.3 France

- 12.1.4 Italy

- 12.1.5 Spain

- 12.1.6 Rest of Europe

- 13. Asia Pacific Heart Scan Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 China

- 13.1.2 Japan

- 13.1.3 India

- 13.1.4 Australia

- 13.1.5 South Korea

- 13.1.6 Rest of Asia Pacific

- 14. Middle East and Africa Heart Scan Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 GCC

- 14.1.2 South Africa

- 14.1.3 Rest of Middle East and Africa

- 15. South America Heart Scan Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 Brazil

- 15.1.2 Argentina

- 15.1.3 Rest of South America

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Schiller AG

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Toshiba Corporation

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Siemens Healthineers

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Hitachi Corporation

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 GE Healthcare

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 F Hoffmann-La Roche Ltd

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Midmark Corporation

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Koninklijke Philips NV

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Astrazenca PLC

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Welch Allyn Inc

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Schiller AG

List of Figures

- Figure 1: Global Heart Scan Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Heart Scan Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Heart Scan Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Heart Scan Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Heart Scan Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Heart Scan Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Heart Scan Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Middle East and Africa Heart Scan Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Middle East and Africa Heart Scan Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America Heart Scan Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: South America Heart Scan Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Heart Scan Industry Revenue (Million), by Test 2024 & 2032

- Figure 13: North America Heart Scan Industry Revenue Share (%), by Test 2024 & 2032

- Figure 14: North America Heart Scan Industry Revenue (Million), by End User 2024 & 2032

- Figure 15: North America Heart Scan Industry Revenue Share (%), by End User 2024 & 2032

- Figure 16: North America Heart Scan Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America Heart Scan Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Heart Scan Industry Revenue (Million), by Test 2024 & 2032

- Figure 19: Europe Heart Scan Industry Revenue Share (%), by Test 2024 & 2032

- Figure 20: Europe Heart Scan Industry Revenue (Million), by End User 2024 & 2032

- Figure 21: Europe Heart Scan Industry Revenue Share (%), by End User 2024 & 2032

- Figure 22: Europe Heart Scan Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Europe Heart Scan Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Asia Pacific Heart Scan Industry Revenue (Million), by Test 2024 & 2032

- Figure 25: Asia Pacific Heart Scan Industry Revenue Share (%), by Test 2024 & 2032

- Figure 26: Asia Pacific Heart Scan Industry Revenue (Million), by End User 2024 & 2032

- Figure 27: Asia Pacific Heart Scan Industry Revenue Share (%), by End User 2024 & 2032

- Figure 28: Asia Pacific Heart Scan Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Asia Pacific Heart Scan Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: Middle East and Africa Heart Scan Industry Revenue (Million), by Test 2024 & 2032

- Figure 31: Middle East and Africa Heart Scan Industry Revenue Share (%), by Test 2024 & 2032

- Figure 32: Middle East and Africa Heart Scan Industry Revenue (Million), by End User 2024 & 2032

- Figure 33: Middle East and Africa Heart Scan Industry Revenue Share (%), by End User 2024 & 2032

- Figure 34: Middle East and Africa Heart Scan Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Middle East and Africa Heart Scan Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: South America Heart Scan Industry Revenue (Million), by Test 2024 & 2032

- Figure 37: South America Heart Scan Industry Revenue Share (%), by Test 2024 & 2032

- Figure 38: South America Heart Scan Industry Revenue (Million), by End User 2024 & 2032

- Figure 39: South America Heart Scan Industry Revenue Share (%), by End User 2024 & 2032

- Figure 40: South America Heart Scan Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: South America Heart Scan Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Heart Scan Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Heart Scan Industry Revenue Million Forecast, by Test 2019 & 2032

- Table 3: Global Heart Scan Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 4: Global Heart Scan Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Heart Scan Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Heart Scan Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Germany Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: United Kingdom Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: France Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Italy Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Spain Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Rest of Europe Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Global Heart Scan Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: China Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Japan Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: India Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Australia Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: South Korea Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Rest of Asia Pacific Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Global Heart Scan Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: GCC Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: South Africa Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Rest of Middle East and Africa Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Global Heart Scan Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Brazil Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Argentina Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Rest of South America Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Global Heart Scan Industry Revenue Million Forecast, by Test 2019 & 2032

- Table 32: Global Heart Scan Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 33: Global Heart Scan Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: United States Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Canada Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Mexico Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Global Heart Scan Industry Revenue Million Forecast, by Test 2019 & 2032

- Table 38: Global Heart Scan Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 39: Global Heart Scan Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 40: Germany Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: United Kingdom Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: France Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Italy Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Spain Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: Rest of Europe Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Global Heart Scan Industry Revenue Million Forecast, by Test 2019 & 2032

- Table 47: Global Heart Scan Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 48: Global Heart Scan Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 49: China Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Japan Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: India Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 52: Australia Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 53: South Korea Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: Rest of Asia Pacific Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: Global Heart Scan Industry Revenue Million Forecast, by Test 2019 & 2032

- Table 56: Global Heart Scan Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 57: Global Heart Scan Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 58: GCC Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 59: South Africa Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 60: Rest of Middle East and Africa Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 61: Global Heart Scan Industry Revenue Million Forecast, by Test 2019 & 2032

- Table 62: Global Heart Scan Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 63: Global Heart Scan Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 64: Brazil Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 65: Argentina Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 66: Rest of South America Heart Scan Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Heart Scan Industry?

The projected CAGR is approximately 7.90%.

2. Which companies are prominent players in the Heart Scan Industry?

Key companies in the market include Schiller AG, Toshiba Corporation, Siemens Healthineers, Hitachi Corporation, GE Healthcare, F Hoffmann-La Roche Ltd, Midmark Corporation, Koninklijke Philips NV, Astrazenca PLC, Welch Allyn Inc.

3. What are the main segments of the Heart Scan Industry?

The market segments include Test, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Technological Advancements; Significant Rise in Cardiovascular Diseases; Increase in Quality of Life.

6. What are the notable trends driving market growth?

Rapid Blood Tests like Troponin Expected to Occupy a Significant Market Share.

7. Are there any restraints impacting market growth?

Expensive Diagnostics Products; Lack of Skilled Workforce in the Hospitals and Other Areas.

8. Can you provide examples of recent developments in the market?

In April 2021, Roche launched a series of five new intended uses for two key cardiac biomarkers using the Elecsys® technology, i.e., highly sensitive cardiac troponin T (cTnT-hs) and N-terminal pro-brain natriuretic peptide test (NT-proBNP).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Heart Scan Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Heart Scan Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Heart Scan Industry?

To stay informed about further developments, trends, and reports in the Heart Scan Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence