Key Insights

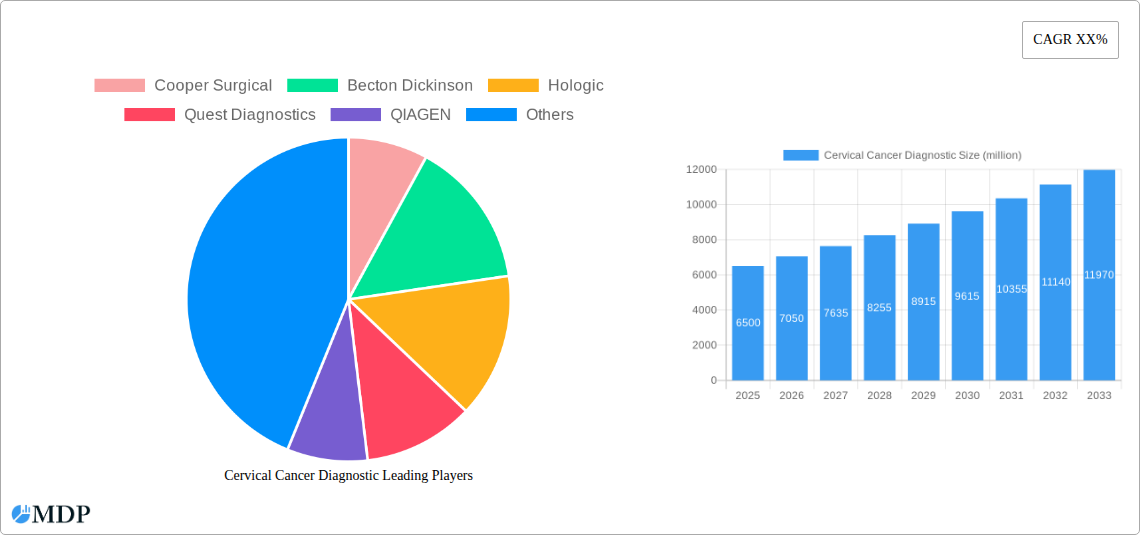

The global Cervical Cancer Diagnostic market is projected to witness robust growth, estimated at approximately $6,500 million in 2025, with a projected Compound Annual Growth Rate (CAGR) of around 8.5% over the forecast period of 2025-2033. This significant expansion is driven by a confluence of factors, including the increasing global incidence of cervical cancer, particularly in developing regions, and a growing awareness among women about the importance of early detection. The market's value is expected to reach over $12,000 million by 2033. Technological advancements in diagnostic tools, such as highly sensitive HPV testing and improved colposcopy techniques, are pivotal drivers. Furthermore, government initiatives and healthcare policies aimed at promoting cervical cancer screening programs are significantly bolstering market demand. The rising adoption of minimally invasive diagnostic procedures also contributes to the market's upward trajectory.

The market is segmented by application, with Cervical Cancer Treatment (encompassing diagnostics as a precursor) holding a dominant share, and by type, where HPV Testing and Pap Testing are leading segments due to their high efficacy and widespread use in routine screening. Colposcopy and Cervical Biopsies are crucial for confirmatory diagnoses, contributing steadily to market value. Key players like Cooper Surgical, Becton Dickinson, Hologic, and Quest Diagnostics are actively involved in research and development, introducing innovative solutions that enhance diagnostic accuracy and patient outcomes. Geographically, North America and Europe currently lead the market, owing to advanced healthcare infrastructure and high screening rates. However, the Asia Pacific region is expected to exhibit the fastest growth, driven by a burgeoning population, increasing healthcare expenditure, and rising awareness campaigns. Restraints include the cost of advanced diagnostic equipment and limited access to screening facilities in some underdeveloped areas, yet the overarching trend of proactive healthcare management and early disease detection is set to propel the market forward.

This comprehensive report, "Cervical Cancer Diagnostic Market Analysis & Forecast 2019–2033," offers an in-depth exploration of the global cervical cancer diagnostic landscape. Spanning the study period of 2019 to 2033, with a base year of 2025 and an extensive forecast period, this analysis provides critical insights for industry stakeholders. The report meticulously examines market dynamics, crucial trends, leading segments, product developments, growth drivers, challenges, and emerging opportunities within this vital healthcare sector. With a focus on high-traffic keywords such as "cervical cancer screening," "HPV testing," "Pap smear," and "colposcopy," this report is optimized for maximum search visibility and engagement among key industry players, including manufacturers, diagnostic service providers, healthcare institutions, and investors.

Cervical Cancer Diagnostic Market Dynamics & Concentration

The cervical cancer diagnostic market exhibits moderate concentration, driven by a blend of established diagnostic giants and emerging innovators. Key players like Cooper Surgical, Becton Dickinson, Hologic, Quest Diagnostics, and QIAGEN hold significant market share, evidenced by their substantial investment in research and development and expansive distribution networks. Innovation in this sector is primarily propelled by advancements in molecular diagnostics, particularly the increasing adoption of HPV testing as a primary screening method, surpassing traditional Pap testing in certain demographics. Regulatory frameworks, such as those established by the FDA and EMA, play a pivotal role in dictating market entry and product approvals, ensuring the safety and efficacy of diagnostic tools. Product substitutes, while present in the form of alternative screening modalities and advanced imaging techniques, are yet to fully displace the established diagnostic pathways. End-user trends reveal a growing preference for minimally invasive and highly accurate diagnostic procedures, pushing for earlier and more precise detection. Mergers and acquisitions (M&A) activities have been instrumental in market consolidation and expansion. Over the historical period (2019-2024), we observed approximately XX M&A deals with an estimated cumulative deal value exceeding $500 million, indicating strategic moves to bolster product portfolios and market reach. Current market share figures indicate that HPV testing accounts for over 60% of the diagnostic market, with Pap testing holding approximately 30%.

Cervical Cancer Diagnostic Industry Trends & Analysis

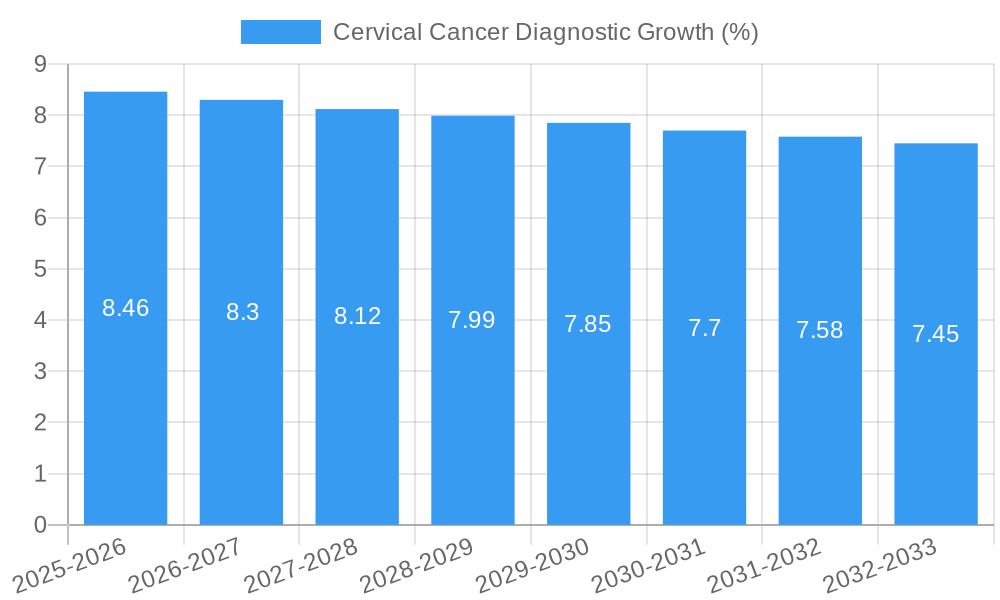

The cervical cancer diagnostic industry is poised for significant expansion, projected to grow at a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033. This robust growth is fueled by a confluence of factors, including increasing global awareness of cervical cancer prevention, rising incidence of HPV infections, and the growing emphasis on early detection by healthcare organizations worldwide. Technological disruptions are a primary catalyst, with the development of highly sensitive and specific HPV DNA and mRNA tests transforming screening protocols. The shift towards self-sampling HPV tests is also gaining momentum, enhancing accessibility and participation, particularly in underserved regions. Consumer preferences are increasingly leaning towards non-invasive and convenient diagnostic methods, which further supports the adoption of advanced HPV testing and molecular diagnostic platforms. Competitive dynamics within the market are characterized by intense innovation and strategic partnerships. Companies are investing heavily in developing next-generation diagnostics that offer faster turnaround times, improved accuracy, and integrated data reporting capabilities. Market penetration of HPV testing as a primary screening tool is projected to exceed 80% in developed nations by 2028. The integration of artificial intelligence (AI) in colposcopy and histopathology analysis is another emerging trend, promising to enhance diagnostic accuracy and streamline workflows. The increasing prevalence of cervical cancer in low- and middle-income countries, coupled with government initiatives to curb its incidence, presents a substantial market opportunity. The global market size for cervical cancer diagnostics is estimated to reach over $15 billion by 2033, up from an estimated $8 billion in 2025.

Leading Markets & Segments in Cervical Cancer Diagnostic

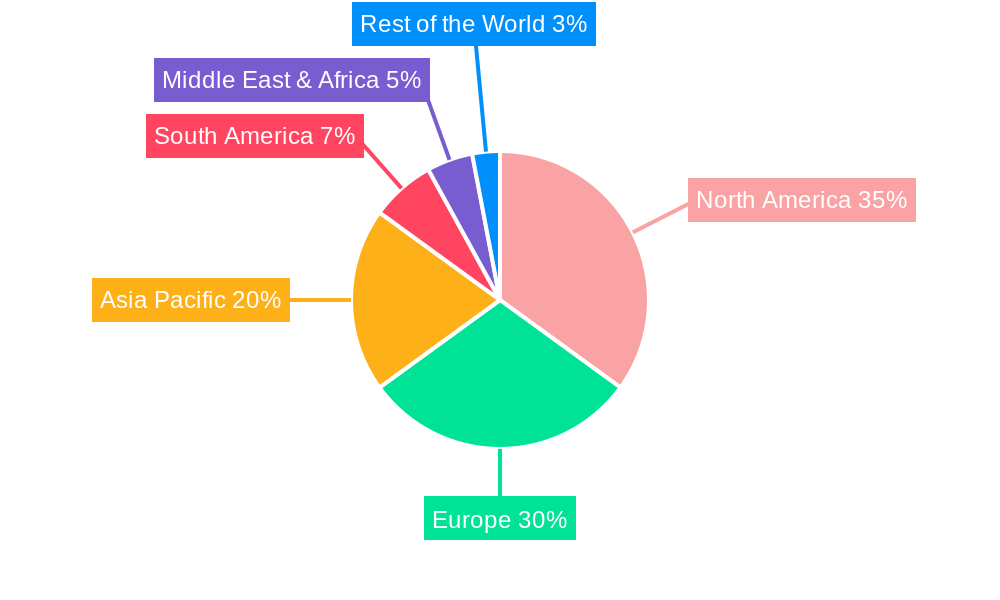

North America and Europe currently dominate the cervical cancer diagnostic market, driven by advanced healthcare infrastructure, high per capita healthcare spending, and proactive government screening programs. The United States, in particular, stands out as a leading country due to the widespread adoption of HPV testing and robust reimbursement policies. Within the Applications segment, Cervical Cancer Treatment is implicitly supported by accurate diagnostics, but the "Others" category, encompassing preventative screening and monitoring, holds the largest share. The most impactful segment by Type is undoubtedly HPV Testing, which has revolutionized screening protocols. Key drivers for the dominance of HPV testing include its superior sensitivity in detecting high-risk HPV types, its efficacy as a primary screening method, and its potential for co-testing with Pap smears or as a standalone test. The economic policies in these leading regions, which prioritize public health initiatives and invest heavily in diagnostic technologies, further solidify their market leadership. Infrastructure development, including well-equipped pathology labs and widespread availability of molecular diagnostic instruments, is crucial.

Dominance of HPV Testing:

- Technological Superiority: Higher sensitivity and specificity in identifying precancerous lesions compared to Pap testing alone.

- Clinical Guidelines: Adoption as a primary screening method by major health organizations (e.g., American Cancer Society, ACOG).

- Cost-Effectiveness: Long-term cost savings due to reduced false positives and improved detection rates.

- Patient Convenience: Potential for self-sampling, increasing accessibility and compliance.

Cervical Cancer Treatment Support: While not a direct diagnostic segment, effective cervical cancer treatment relies heavily on the accuracy and timeliness of diagnostic procedures. The increasing number of diagnoses directly translates to a higher demand for treatment.

Others (Screening & Monitoring): This broad category encompasses the vast majority of diagnostic activities focused on early detection and surveillance, which are the primary drivers of the market.

Colposcopy: Remains a crucial follow-up procedure for abnormal Pap or HPV test results, ensuring precise visualization of cervical tissue.

Cervical Biopsies: Essential for definitive diagnosis and staging when abnormalities are detected during colposcopy.

Pap Testing: While its role is evolving, it remains a significant component, especially in co-testing strategies and in regions where HPV testing is less accessible.

Cystoscopy: Typically used for investigating specific gynecological conditions and can indirectly be part of the broader diagnostic pathway for related issues, though not a primary cervical cancer diagnostic tool.

Cervical Cancer Diagnostic Product Developments

Recent product developments in the cervical cancer diagnostic market are focused on enhancing accuracy, speed, and accessibility. Innovations in multiplex HPV testing allow for the simultaneous detection of multiple high-risk HPV genotypes, providing more comprehensive risk stratification. Companies are also developing point-of-care HPV tests, aiming to deliver results within a single patient visit, thereby reducing turnaround times and improving patient management. Liquid-based cytology continues to evolve, offering improved sample preservation for both cytology and molecular testing. The integration of AI algorithms for analyzing Pap smears and colposcopic images is a significant technological trend, promising to augment the capabilities of pathologists and clinicians. These advancements offer competitive advantages by improving diagnostic yields, reducing false negatives, and enabling personalized screening strategies.

Key Drivers of Cervical Cancer Diagnostic Growth

The cervical cancer diagnostic market is propelled by several key drivers. Firstly, increasing global awareness campaigns and government-backed screening programs are significantly boosting demand for diagnostic tests. Secondly, technological advancements, particularly in molecular diagnostics and the development of highly sensitive HPV tests, are driving the adoption of more effective screening methods. Thirdly, the rising incidence of Human Papillomavirus (HPV) infections, a primary cause of cervical cancer, necessitates robust diagnostic solutions. Fourthly, favorable reimbursement policies and increasing healthcare expenditure, especially in emerging economies, are expanding market access. Finally, the growing trend towards personalized medicine and proactive healthcare further emphasizes the importance of early and accurate cervical cancer detection.

Challenges in the Cervical Cancer Diagnostic Market

Despite its growth potential, the cervical cancer diagnostic market faces several challenges. Regulatory hurdles for novel diagnostic technologies can lead to lengthy approval processes and significant development costs. Supply chain disruptions, particularly for specialized reagents and instruments, can impact the availability and affordability of tests. Competitive pressures from established players and the constant need for innovation to stay ahead can strain R&D budgets. Furthermore, disparities in healthcare access and infrastructure in low- and middle-income countries limit the widespread adoption of advanced diagnostic methods. Socioeconomic factors and cultural barriers in certain regions can also impede screening program participation. The cost of advanced diagnostic technologies can also be a restraint for some healthcare systems.

Emerging Opportunities in Cervical Cancer Diagnostic

Emerging opportunities in the cervical cancer diagnostic market are vast and multifaceted. Technological breakthroughs in areas such as next-generation sequencing (NGS) for comprehensive HPV genotyping and biomarker discovery hold immense potential. Strategic partnerships between diagnostic companies, pharmaceutical firms, and academic research institutions are crucial for accelerating the development and commercialization of innovative solutions. Market expansion into underserved regions, particularly in Asia-Pacific and Africa, presents a significant growth avenue, driven by increasing healthcare investments and disease burden. The development of integrated diagnostic platforms that combine HPV testing, cytology, and other biomarkers for more precise risk stratification and personalized screening strategies will be a key focus. Furthermore, the growing interest in home-based self-sampling kits is opening up new distribution channels and enhancing patient convenience.

Leading Players in the Cervical Cancer Diagnostic Sector

- Cooper Surgical

- Becton Dickinson

- Hologic

- Quest Diagnostics

- QIAGEN

- Guided Therapeutics

- Siemens

- OncoHealth

- Arbor Vita

- Zilico

- Beckman Coulter

Key Milestones in Cervical Cancer Diagnostic Industry

- 2019: FDA approval of new HPV co-testing guidelines, reinforcing the importance of HPV testing in screening.

- 2020: Increased adoption of telemedicine and remote diagnostics, impacting sample collection and consultation workflows.

- 2021: Launch of novel multiplex HPV tests capable of detecting a broader range of high-risk genotypes.

- 2022: Growing research into AI-powered image analysis for Pap smears and colposcopic findings.

- 2023: Expansion of self-sampling HPV testing options in various markets, enhancing accessibility.

- 2024: Significant investment in R&D for biomarker discovery to further refine cervical cancer risk assessment.

Strategic Outlook for Cervical Cancer Diagnostic Market

The strategic outlook for the cervical cancer diagnostic market is exceptionally promising, driven by an unwavering commitment to disease prevention and early detection. Growth accelerators will include the continued refinement and broader adoption of HPV testing as a primary screening modality, coupled with the development of highly accurate, rapid, and cost-effective molecular diagnostic solutions. The integration of AI and machine learning in diagnostic interpretation is expected to further enhance precision and efficiency. Strategic collaborations and partnerships will be critical for market expansion, particularly in emerging economies where the burden of cervical cancer is high. Investment in innovative technologies, such as liquid biopsy and advanced biomarker identification, will unlock new avenues for personalized risk assessment and targeted therapeutic interventions. The market is poised for sustained growth as global health initiatives and technological advancements converge to significantly reduce the incidence and mortality associated with cervical cancer.

Cervical Cancer Diagnostic Segmentation

-

1. Application

- 1.1. Cervical Cancer Treament

- 1.2. Others

-

2. Types

- 2.1. Pap Testing

- 2.2. HPV Testing

- 2.3. Colposcopy

- 2.4. Cervical Biopsies

- 2.5. Cystoscopy

Cervical Cancer Diagnostic Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cervical Cancer Diagnostic REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Cervical Cancer Diagnostic Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Cervical Cancer Treament

- 5.1.2. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Pap Testing

- 5.2.2. HPV Testing

- 5.2.3. Colposcopy

- 5.2.4. Cervical Biopsies

- 5.2.5. Cystoscopy

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Cervical Cancer Diagnostic Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Cervical Cancer Treament

- 6.1.2. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Pap Testing

- 6.2.2. HPV Testing

- 6.2.3. Colposcopy

- 6.2.4. Cervical Biopsies

- 6.2.5. Cystoscopy

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Cervical Cancer Diagnostic Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Cervical Cancer Treament

- 7.1.2. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Pap Testing

- 7.2.2. HPV Testing

- 7.2.3. Colposcopy

- 7.2.4. Cervical Biopsies

- 7.2.5. Cystoscopy

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Cervical Cancer Diagnostic Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Cervical Cancer Treament

- 8.1.2. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Pap Testing

- 8.2.2. HPV Testing

- 8.2.3. Colposcopy

- 8.2.4. Cervical Biopsies

- 8.2.5. Cystoscopy

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Cervical Cancer Diagnostic Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Cervical Cancer Treament

- 9.1.2. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Pap Testing

- 9.2.2. HPV Testing

- 9.2.3. Colposcopy

- 9.2.4. Cervical Biopsies

- 9.2.5. Cystoscopy

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Cervical Cancer Diagnostic Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Cervical Cancer Treament

- 10.1.2. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Pap Testing

- 10.2.2. HPV Testing

- 10.2.3. Colposcopy

- 10.2.4. Cervical Biopsies

- 10.2.5. Cystoscopy

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Cooper Surgical

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Becton Dickinson

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Hologic

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Quest Diagnostics

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 QIAGEN

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Guided Therapeutics

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Siemens

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 OncoHealth

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Arbor Vita

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Zilico

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Beckman Coulter

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Cooper Surgical

List of Figures

- Figure 1: Global Cervical Cancer Diagnostic Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Cervical Cancer Diagnostic Revenue (million), by Application 2024 & 2032

- Figure 3: North America Cervical Cancer Diagnostic Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Cervical Cancer Diagnostic Revenue (million), by Types 2024 & 2032

- Figure 5: North America Cervical Cancer Diagnostic Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Cervical Cancer Diagnostic Revenue (million), by Country 2024 & 2032

- Figure 7: North America Cervical Cancer Diagnostic Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Cervical Cancer Diagnostic Revenue (million), by Application 2024 & 2032

- Figure 9: South America Cervical Cancer Diagnostic Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Cervical Cancer Diagnostic Revenue (million), by Types 2024 & 2032

- Figure 11: South America Cervical Cancer Diagnostic Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Cervical Cancer Diagnostic Revenue (million), by Country 2024 & 2032

- Figure 13: South America Cervical Cancer Diagnostic Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Cervical Cancer Diagnostic Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Cervical Cancer Diagnostic Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Cervical Cancer Diagnostic Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Cervical Cancer Diagnostic Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Cervical Cancer Diagnostic Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Cervical Cancer Diagnostic Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Cervical Cancer Diagnostic Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Cervical Cancer Diagnostic Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Cervical Cancer Diagnostic Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Cervical Cancer Diagnostic Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Cervical Cancer Diagnostic Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Cervical Cancer Diagnostic Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Cervical Cancer Diagnostic Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Cervical Cancer Diagnostic Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Cervical Cancer Diagnostic Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Cervical Cancer Diagnostic Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Cervical Cancer Diagnostic Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Cervical Cancer Diagnostic Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Cervical Cancer Diagnostic Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Cervical Cancer Diagnostic Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Cervical Cancer Diagnostic Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Cervical Cancer Diagnostic Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Cervical Cancer Diagnostic Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Cervical Cancer Diagnostic Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Cervical Cancer Diagnostic Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Cervical Cancer Diagnostic Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Cervical Cancer Diagnostic Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Cervical Cancer Diagnostic Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Cervical Cancer Diagnostic Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Cervical Cancer Diagnostic Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Cervical Cancer Diagnostic Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Cervical Cancer Diagnostic Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Cervical Cancer Diagnostic Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Cervical Cancer Diagnostic Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Cervical Cancer Diagnostic Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Cervical Cancer Diagnostic Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Cervical Cancer Diagnostic Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Cervical Cancer Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cervical Cancer Diagnostic?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Cervical Cancer Diagnostic?

Key companies in the market include Cooper Surgical, Becton Dickinson, Hologic, Quest Diagnostics, QIAGEN, Guided Therapeutics, Siemens, OncoHealth, Arbor Vita, Zilico, Beckman Coulter.

3. What are the main segments of the Cervical Cancer Diagnostic?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cervical Cancer Diagnostic," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cervical Cancer Diagnostic report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cervical Cancer Diagnostic?

To stay informed about further developments, trends, and reports in the Cervical Cancer Diagnostic, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence