Key Insights for Automotive Adas Market

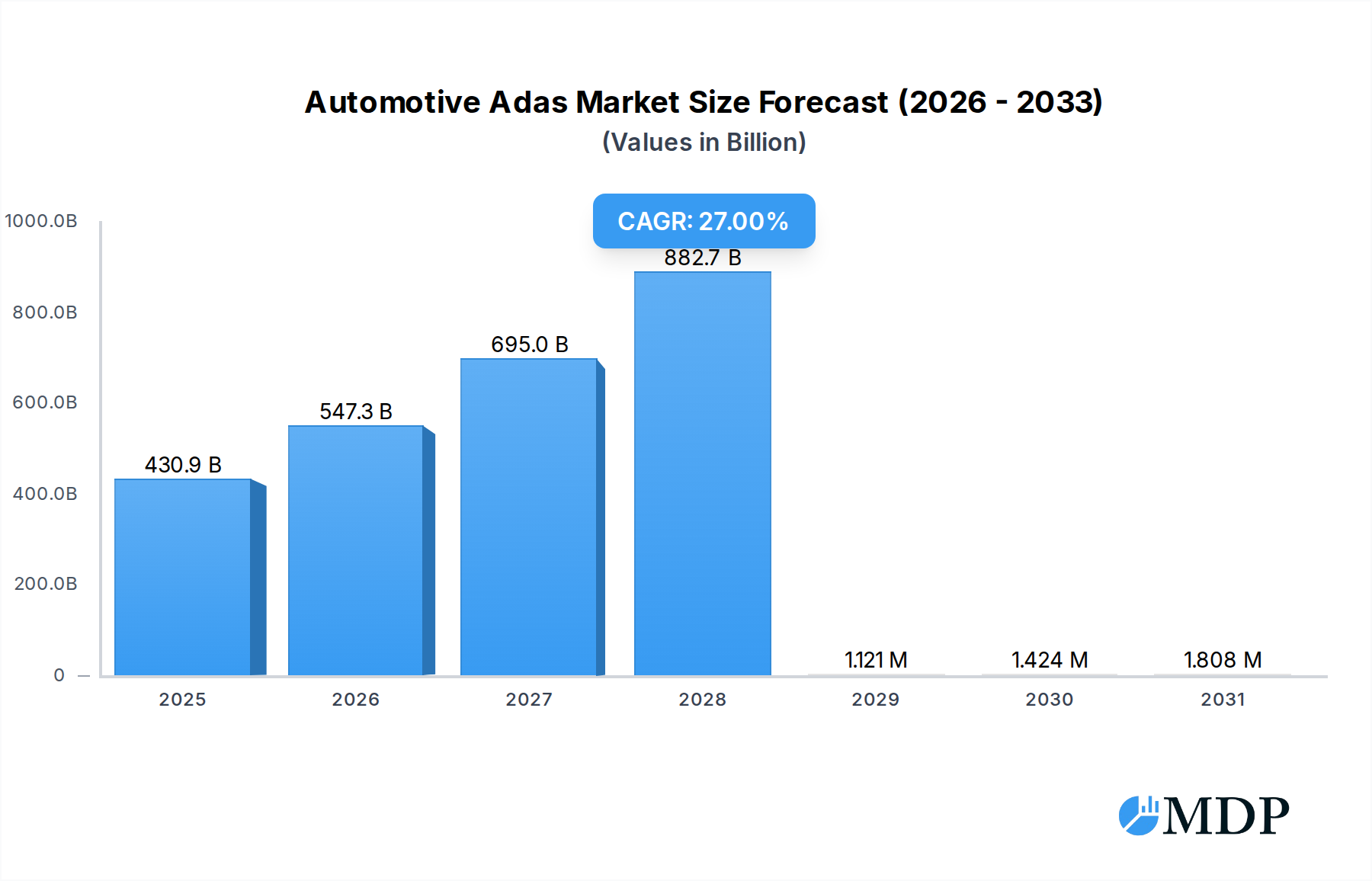

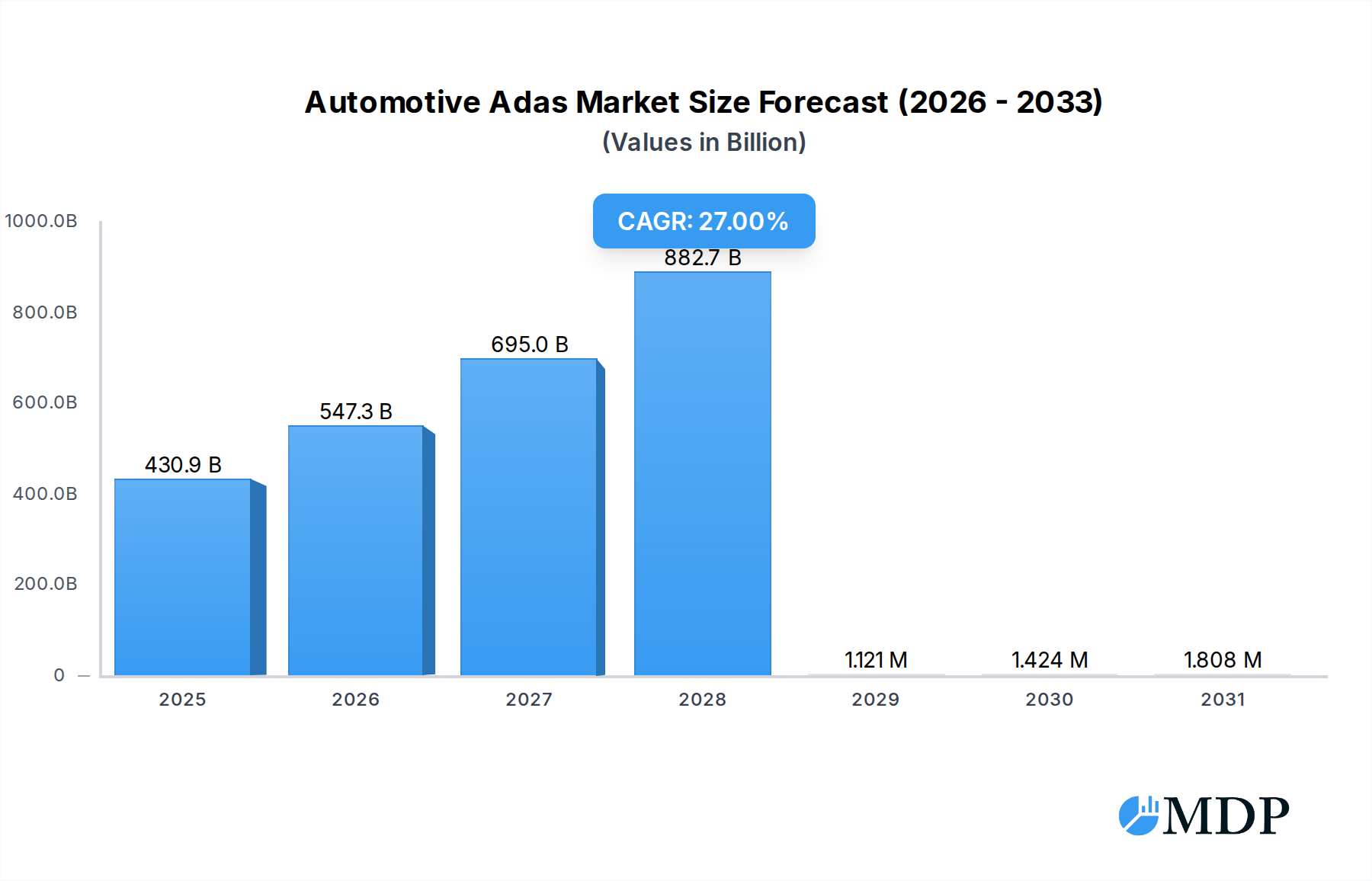

The Global Automotive Adas Market, valued at an estimated $339,300 million in 2024, is poised for exponential expansion, projected to reach approximately $2,250,572 million by 2032, exhibiting a robust Compound Annual Growth Rate (CAGR) of 27% during the forecast period. This significant growth trajectory is underpinned by a confluence of evolving regulatory landscapes, escalating consumer demand for enhanced vehicle safety and convenience, and relentless technological advancements in sensor and processing capabilities. Key demand drivers include global mandates for active safety features, such as Automatic Emergency Braking (AEB) and Lane Departure Warning (LDW) systems, particularly from regulatory bodies like Euro NCAP and NHTSA, which are increasingly integrating ADAS performance into vehicle safety ratings. The growing sophistication of infotainment systems and the proliferation of the Connected Car Market are also synergistically propelling the Automotive Adas Market forward, as these systems often share core technological infrastructure and data streams.

Automotive Adas Market Size (In Billion)

Macroeconomic tailwinds, such as rising disposable incomes in emerging economies and increasing urbanization, contribute to higher new vehicle sales and a greater propensity for consumers to invest in advanced safety features. Furthermore, the decreasing cost of sensor components, including those found in the LiDAR Sensor Market and Radar Sensor Market, is making ADAS technologies more accessible across various vehicle segments. The push towards electrification, evidenced by the burgeoning Electric Vehicle Market, inherently integrates advanced ADAS capabilities, as electric vehicle architectures are often designed with a 'software-first' approach that facilitates sophisticated electronic systems. The Automotive Adas Market is also a foundational pillar for the long-term vision of the Autonomous Vehicle Market, with L2 and L2+ systems serving as critical stepping stones. The outlook remains exceptionally positive, characterized by continuous innovation in sensor fusion, artificial intelligence, and V2X communication, which promise to unlock new levels of automation and safety features, further solidifying the market's dynamic growth trajectory through 2032 and beyond.

Automotive Adas Company Market Share

Level 2 Autonomy Dominance in Automotive Adas Market

The Level 2 (L2) Autonomy segment, within the broader Level of Automation (LOA) classification, currently holds a dominant position in the Automotive Adas Market, and its revenue share is expected to continue its robust expansion over the forecast period. L2 ADAS systems typically combine capabilities like Adaptive Cruise Control (ACC) and Lane Keeping Assist (LKA) to provide both longitudinal and lateral control of the vehicle under specific operating conditions, requiring the driver to remain engaged and ready to intervene. This segment’s dominance stems from its practical balance of enhanced safety, significant convenience, and a high degree of regulatory and consumer acceptance, making it a pivotal stepping stone towards fully autonomous driving.

The widespread adoption of L2 systems is largely attributable to their cost-effectiveness relative to higher automation levels and their ability to address common driving scenarios effectively, thereby improving driver comfort and reducing accident risks. Automakers are increasingly integrating L2 features as standard or optional equipment across a wide range of Passenger Car Market models, responding to both consumer demand and evolving safety regulations that often incentivize or mandate such technologies. The underlying technologies for L2, including advanced camera sensors, radar sensors, and ultrasonic sensors, have matured considerably, allowing for reliable and commercially viable implementation. Many major players in the Automotive Adas Market, such as Robert Bosch Gmbh, Continental Ag, and Denso Corporation, are heavily invested in developing and refining L2+ and L2++ systems, which offer enhanced capabilities beyond basic L2, bridging the gap towards Level 3 autonomy. These companies focus on sensor fusion techniques, advanced perception algorithms, and sophisticated control strategies to optimize L2 performance and reliability.

Furthermore, the growth of the L2 segment is critical for accumulating real-world driving data, which is invaluable for training AI models and validating the safety of more advanced autonomous systems. This data feedback loop accelerates the development cycle for the entire Automotive Adas Market. While higher levels of autonomy (L3, L4, L5) present significant technological and regulatory hurdles, the continuous enhancement and broader deployment of L2 solutions are solidifying its foundational role. The segment is characterized by ongoing innovation, with advancements in sensor resolution, processing power, and software integration constantly pushing the boundaries of what L2 systems can achieve. This sustained focus, coupled with increasing regulatory support for driver assistance features, ensures that L2 autonomy will remain the largest and most dynamic segment, both in terms of revenue and market penetration, for the foreseeable future, serving as a critical enabler for the future of the Autonomous Vehicle Market.

Key Market Drivers & Constraints in Automotive Adas Market

The Automotive Adas Market's trajectory is primarily shaped by a dynamic interplay of potent drivers and inherent constraints, each influencing adoption rates and technological progression. A principal driver is the stringent regulatory landscape and safety mandates across major automotive markets. For instance, the European Union's General Safety Regulation (GSR) mandates several advanced safety features, including Automatic Emergency Braking System Market and Lane Departure Warning System Market, in all new vehicle types introduced from July 2022, significantly bolstering the market. Similar initiatives by the U.S. National Highway Traffic Safety Administration (NHTSA) and the United Nations Economic Commission for Europe (UNECE) actively drive OEM integration of ADAS, directly correlating with improved vehicle safety ratings and consumer purchase decisions.

Another significant driver is the escalating consumer demand for safety and convenience features. A substantial percentage of new car buyers prioritize advanced safety systems, viewing them as essential rather than optional. The integration of advanced features such as adaptive cruise control, blind spot detection, and parking assist systems enhances the driving experience, reduces driver fatigue, and demonstrably lowers accident rates, thereby increasing the intrinsic value proposition for end-users in the Passenger Car Market. The continuous technological advancements in sensor capabilities and processing power serve as a critical enabler. Innovations in the LiDAR Sensor Market and Radar Sensor Market, coupled with sophisticated camera systems and powerful AI-driven processors, allow for more accurate environmental perception and faster decision-making, expanding the functional scope and reliability of ADAS. Moreover, the growing momentum of the Electric Vehicle Market and Autonomous Vehicle Market inherently propels ADAS, as these vehicles are often designed from the ground up with a comprehensive suite of sensors and software that form the core of ADAS capabilities.

Conversely, several constraints temper the market's growth. The high initial cost associated with advanced ADAS features, particularly Level 3 and above, poses a barrier to mass-market adoption. While costs for basic L1/L2 systems are declining, the integration of complex sensor suites and redundant computing platforms for higher automation levels remains expensive, impacting vehicle pricing. Public perception and trust issues represent another significant hurdle; consumers often express concerns regarding system reliability, potential malfunctions, and data privacy, which can slow adoption. Furthermore, complex integration and validation challenges for OEMs, involving diverse suppliers, software platforms, and rigorous testing across myriad driving scenarios, add considerable development time and expense. Lastly, the lack of standardized regulations across different geographies complicates global deployment for manufacturers, necessitating regional adaptations and certifications.

Competitive Ecosystem of Automotive Adas Market

The Automotive Adas Market is characterized by intense competition among a few dominant Tier 1 suppliers, who serve as crucial technology providers to global automotive OEMs. These companies leverage extensive R&D investments, strategic partnerships, and broad product portfolios to maintain their competitive edge. The landscape is also seeing increasing innovation from specialized software and sensor providers.

- Continental Ag: A leading technology company, Continental Ag offers a comprehensive portfolio of ADAS solutions, including radar sensors, camera systems, driver monitoring systems, and advanced software for assisted and automated driving, focusing on integrated safety and enhanced user experience.

- Delphi Automotive PLC: Known for its strong presence in automotive electronics and safety systems, Delphi Automotive PLC (now Aptiv) specializes in advanced sensing, processing platforms, and connectivity solutions critical for ADAS and autonomous driving architectures.

- Robert Bosch Gmbh: As a global leader in automotive technology, Robert Bosch Gmbh provides a vast array of ADAS components and systems, including radar and video sensors, steering systems, braking systems, and software solutions for automated parking, emergency braking, and lane keeping.

- Aisin Seiki Co. Ltd.: A prominent Japanese automotive supplier, Aisin Seiki Co. Ltd. contributes to the ADAS market with its expertise in braking systems, electronic control units, and advanced parking assistance technologies, often integrated into vehicle platforms from major Japanese OEMs.

- Denso Corporation: A global automotive components manufacturer, Denso Corporation offers a wide range of ADAS products, including image sensors, millimeter-wave radar, and various ECUs, with a strong focus on enhancing vehicle safety and contributing to a future of accident-free mobility.

- Trw Automotive Holdings Corp.: Now part of ZF Friedrichshafen AG, Trw Automotive Holdings Corp. was a significant player in active and passive safety systems, providing technologies such as camera and radar systems, occupant safety systems, and steering and braking solutions crucial for ADAS functionality.

- Mobileye NV: A pioneer and leader in computer vision and machine learning for ADAS and autonomous driving, Mobileye NV, an Intel company, specializes in camera-based sensing solutions, mapping, and driving policy technologies, with its EyeQ® chip being a foundational component for many OEMs' ADAS offerings.

Recent Developments & Milestones in Automotive Adas Market

January 2024: Continental Ag announced a strategic partnership with a leading AI software firm to further develop and integrate advanced machine learning algorithms into its ADAS cameras, aiming to enhance object recognition and predictive capabilities for improved driving safety. November 2023: Robert Bosch Gmbh unveiled its next-generation radar sensor technology, designed for Level 3 autonomous driving applications, featuring increased range, higher resolution, and improved weather resilience, slated for production vehicle integration by 2026. September 2023: Mobileye NV introduced its new EyeQ™6L and EyeQ™6H systems-on-chip, engineered to support more complex Level 2+ and Level 3 ADAS features with significantly higher processing power and efficiency for the next wave of advanced driver-assistance systems. July 2023: Denso Corporation commenced mass production of its advanced driver monitoring system (DMS), which utilizes infrared cameras and AI to detect driver distraction and drowsiness, thereby addressing a critical aspect of road safety. May 2023: European Union regulators finalized new standards for cybersecurity in vehicles, including ADAS systems, requiring manufacturers to implement robust protection measures against hacking and data breaches for all new vehicle types by July 2024. March 2023: Several major automotive OEMs, including General Motors and Mercedes-Benz, announced plans to standardize Level 2+ ADAS features, such as enhanced Lane Departure Warning System Market and traffic jam assist, across a broader range of their model lineups starting from 2025. February 2023: A joint venture between a sensor manufacturer and a software developer secured significant funding for the development of solid-state LiDAR Sensor Market technology, targeting a substantial cost reduction and improved reliability for future ADAS and Autonomous Vehicle Market applications.

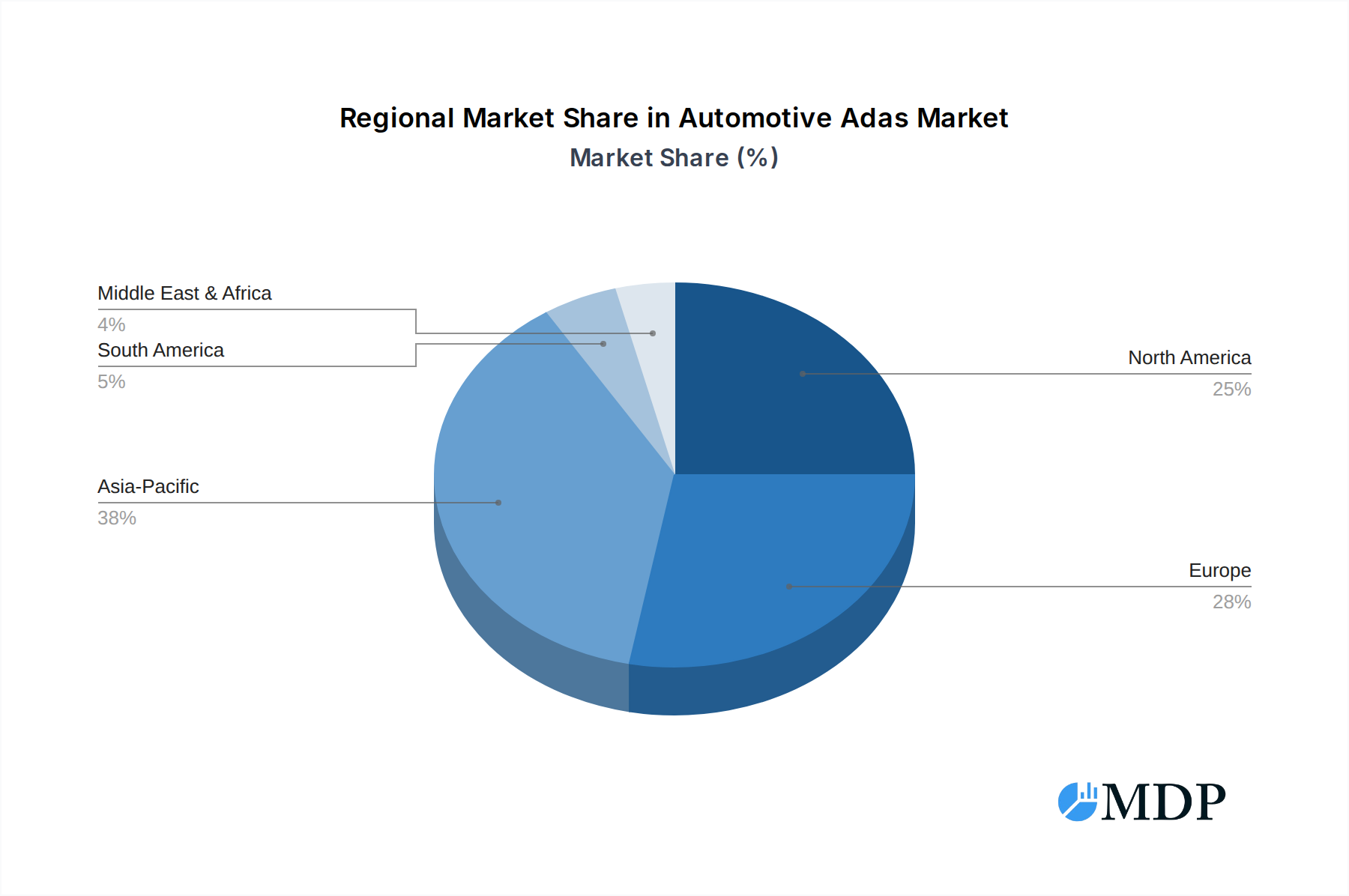

Regional Market Breakdown for Automotive Adas Market

The Global Automotive Adas Market exhibits significant regional disparities in adoption, regulatory impetus, and growth dynamics, primarily segmented across North America, Europe, Asia Pacific, and the Middle East & Africa. These regions collectively showcase a diverse set of drivers and maturity levels, contributing uniquely to the overall market expansion.

Asia Pacific stands out as the fastest-growing region in the Automotive Adas Market. Countries like China, India, Japan, and South Korea are experiencing rapid urbanization, increasing disposable incomes, and a burgeoning middle class, leading to higher vehicle sales and a greater demand for safety features. Regulatory bodies in these nations are increasingly mandating or incentivizing ADAS adoption, mirroring trends in more mature markets. Moreover, the region is a major hub for automotive manufacturing and the Electric Vehicle Market, with domestic players heavily investing in advanced automotive electronics and ADAS development, often with significant government support. The vast consumer base and the increasing penetration of features like parking assist and automatic emergency braking are key demand drivers.

Europe represents a highly mature yet continually growing market for ADAS. Stringent safety regulations, particularly those from Euro NCAP and the European Union's General Safety Regulation, have historically driven the early and widespread adoption of features such as Automatic Emergency Braking System Market and Lane Departure Warning System Market. European consumers are generally well-informed and place a high premium on vehicle safety and technological sophistication. The region is also at the forefront of Autonomous Vehicle Market research and deployment, with significant R&D investments by European OEMs and Tier 1 suppliers. The strong focus on reducing road fatalities and improving traffic efficiency continues to be the primary demand driver.

North America is another mature market, characterized by strong consumer demand for comfort, convenience, and advanced safety features, especially in the Passenger Car Market. The presence of major technology innovators and a robust regulatory framework from NHTSA contribute to continuous ADAS integration. High vehicle ownership rates and a willingness to pay for premium features, alongside a growing interest in the Connected Car Market, fuel sustained demand. The region is also a key testing ground for higher levels of autonomous driving, further bolstering the Automotive Adas Market.

In the Middle East & Africa, the market is still in its nascent stages but is demonstrating considerable potential. Growing economies, increasing automotive sales, and infrastructure development projects are creating new opportunities. While regulatory frameworks are less standardized than in other regions, there is an emerging awareness of road safety and a gradual uptake of advanced vehicle technologies, particularly in the GCC countries. The import of vehicles equipped with modern ADAS features from global manufacturers is a primary driver in this developing region.

Automotive Adas Regional Market Share

Technology Innovation Trajectory in Automotive Adas Market

The Automotive Adas Market is a crucible of technological innovation, constantly evolving with breakthroughs in sensing, perception, and decision-making. Two to three disruptive technologies are currently charting the future trajectory of this domain: Advanced Sensor Fusion Architectures, Artificial Intelligence (AI) and Machine Learning (ML) for Perception, and Solid-State LiDAR Integration.

Advanced Sensor Fusion Architectures are critical for overcoming the limitations of individual sensors. By combining data from radar, camera, ultrasonic, and LiDAR Sensor Market, these architectures create a more robust and comprehensive understanding of the vehicle's surroundings. R&D investments in this area are substantial, focusing on algorithms that can intelligently weigh sensor inputs, handle conflicting data, and ensure redundancy for safety-critical functions. Adoption timelines suggest a gradual shift from basic sensor fusion in L2 systems to highly sophisticated, multi-modal fusion in L3 and L4 vehicles, with widespread implementation expected over the next five to eight years. This technology reinforces incumbent business models of Tier 1 suppliers like Robert Bosch Gmbh and Continental Ag who can offer complete, integrated solutions, while potentially threatening smaller players focused on single-sensor solutions.

Artificial Intelligence and Machine Learning for Perception are revolutionizing how ADAS systems interpret environmental data. AI-powered algorithms enable more accurate object detection, classification, and prediction of pedestrian and vehicle movements, especially in complex scenarios. The development of deep learning models requires massive datasets and significant computational power, leading to high R&D investments from both automotive tech giants and specialized AI startups. AI/ML is increasingly being deployed in features such as Automatic Emergency Braking System Market and Lane Departure Warning System Market to improve reliability and reduce false positives. Adoption is already prevalent in L2 systems and will progressively enhance higher levels of automation, reinforcing the capabilities of established players and driving innovation within the broader Automotive Electronics Market. Companies like Mobileye NV are at the forefront of this AI revolution.

Solid-State LiDAR Integration is emerging as a game-changer. Traditional mechanical LiDARs are expensive, bulky, and prone to wear. Solid-state LiDAR, leveraging semiconductor technology, promises a compact, more durable, and significantly cheaper solution, paving the way for its mass adoption in the Autonomous Vehicle Market. R&D is focused on improving range, resolution, and manufacturing scalability. Adoption is currently in pilot projects and high-end vehicles, but with cost reductions, it is expected to become a standard component in L3/L4 vehicles by the late 2020s to early 2030s. This technology has the potential to disrupt the Radar Sensor Market in certain applications and shift competitive advantage towards companies capable of mastering its integration and cost-effective production, offering a higher fidelity 3D mapping capability essential for complex driving environments.

Export, Trade Flow & Tariff Impact on Automotive Adas Market

The Automotive Adas Market, deeply intertwined with the global automotive supply chain, is significantly influenced by international export, trade flows, and tariff policies. Major trade corridors for ADAS components and systems primarily connect manufacturing hubs in Asia Pacific (Japan, South Korea, China), Europe (Germany, France), and North America (United States, Mexico) with assembly plants worldwide. Leading exporting nations for high-value ADAS components like radar modules, camera sensors, and ECUs include Germany, Japan, and the United States, while importing nations are globally diverse, with large automotive manufacturing bases in China, Mexico, and Central and Eastern Europe.

Trade flows in the Automotive Adas Market are characterized by a complex network of Tier 1 suppliers, who often manufacture components in specialized facilities across different countries and then ship them to global OEMs for integration into vehicles. For example, a Radar Sensor Market component might originate in Germany, be integrated into an ADAS module in Mexico, and then installed in a Passenger Car Market assembled in the U.S. This intricate globalized production necessitates smooth cross-border movement of goods. Non-tariff barriers, such as differing regulatory standards for ADAS features and vehicle homologation processes across regions, often create additional complexities and costs, requiring localized product development and certification efforts.

Recent trade policy impacts, particularly those arising from the US-China trade tensions, have introduced significant challenges. Tariffs imposed on certain electronic components and automotive parts traded between these regions have directly increased the cost of production for ADAS modules, leading to potential price hikes for end consumers or reduced profit margins for manufacturers. For instance, specific tariffs on semiconductors or automotive electronics can escalate the bill of materials for advanced ADAS systems, impacting the competitiveness of vehicles where these tariffs apply. While quantifying the exact cross-border volume impact is complex without granular trade data, general trends indicate that tariff impositions have prompted manufacturers to re-evaluate their supply chain resilience, leading to some diversification of production bases to mitigate future trade risks. The global semiconductor shortage of 2021-2023 also highlighted the vulnerability of the ADAS supply chain to disruptions in critical component flows, irrespective of tariff structures, underscoring the need for robust global sourcing and logistics strategies within the Automotive Adas Market.

Automotive Adas Segmentation

-

1. System Type

- 1.1. Adaptive Cruise Control (ACC)

- 1.2. Automatic Emergency Braking (AEB)

- 1.3. Lane Departure Warning (LDW)

- 1.4. Blind Spot Detection (BSD).

- 1.5. Forward Collision Warning (FCW)

- 1.6. Driver Monitoring System (DMS)

- 1.7. Others

-

2. Sensor Type

- 2.1. Radar Sensors

- 2.2. Camera Sensors

- 2.3. LiDAR Sensors

- 2.4. Ultrasonic Sensors

- 2.5. Infrared Sensors

- 2.6. Others

-

3. LOA

- 3.1. L1

- 3.2. L2

- 3.3. L3

- 3.4. L4

- 3.5. L5

-

4. Sales Channel

- 4.1. Passenger Cars

- 4.2. Light Commercial Vehicles (LCV)

- 4.3. Heavy Commercial Vehicles (HCV)

-

5. Vehicle Type

- 5.1. OEM

- 5.2. Sales Channel

Automotive Adas Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Adas Regional Market Share

Geographic Coverage of Automotive Adas

Automotive Adas REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 27% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by System Type

- 5.1.1. Adaptive Cruise Control (ACC)

- 5.1.2. Automatic Emergency Braking (AEB)

- 5.1.3. Lane Departure Warning (LDW)

- 5.1.4. Blind Spot Detection (BSD).

- 5.1.5. Forward Collision Warning (FCW)

- 5.1.6. Driver Monitoring System (DMS)

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Sensor Type

- 5.2.1. Radar Sensors

- 5.2.2. Camera Sensors

- 5.2.3. LiDAR Sensors

- 5.2.4. Ultrasonic Sensors

- 5.2.5. Infrared Sensors

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by LOA

- 5.3.1. L1

- 5.3.2. L2

- 5.3.3. L3

- 5.3.4. L4

- 5.3.5. L5

- 5.4. Market Analysis, Insights and Forecast - by Sales Channel

- 5.4.1. Passenger Cars

- 5.4.2. Light Commercial Vehicles (LCV)

- 5.4.3. Heavy Commercial Vehicles (HCV)

- 5.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.5.1. OEM

- 5.5.2. Sales Channel

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. South America

- 5.6.3. Europe

- 5.6.4. Middle East & Africa

- 5.6.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by System Type

- 6. Global Automotive Adas Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by System Type

- 6.1.1. Adaptive Cruise Control (ACC)

- 6.1.2. Automatic Emergency Braking (AEB)

- 6.1.3. Lane Departure Warning (LDW)

- 6.1.4. Blind Spot Detection (BSD).

- 6.1.5. Forward Collision Warning (FCW)

- 6.1.6. Driver Monitoring System (DMS)

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Sensor Type

- 6.2.1. Radar Sensors

- 6.2.2. Camera Sensors

- 6.2.3. LiDAR Sensors

- 6.2.4. Ultrasonic Sensors

- 6.2.5. Infrared Sensors

- 6.2.6. Others

- 6.3. Market Analysis, Insights and Forecast - by LOA

- 6.3.1. L1

- 6.3.2. L2

- 6.3.3. L3

- 6.3.4. L4

- 6.3.5. L5

- 6.4. Market Analysis, Insights and Forecast - by Sales Channel

- 6.4.1. Passenger Cars

- 6.4.2. Light Commercial Vehicles (LCV)

- 6.4.3. Heavy Commercial Vehicles (HCV)

- 6.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.5.1. OEM

- 6.5.2. Sales Channel

- 6.1. Market Analysis, Insights and Forecast - by System Type

- 7. North America Automotive Adas Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by System Type

- 7.1.1. Adaptive Cruise Control (ACC)

- 7.1.2. Automatic Emergency Braking (AEB)

- 7.1.3. Lane Departure Warning (LDW)

- 7.1.4. Blind Spot Detection (BSD).

- 7.1.5. Forward Collision Warning (FCW)

- 7.1.6. Driver Monitoring System (DMS)

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Sensor Type

- 7.2.1. Radar Sensors

- 7.2.2. Camera Sensors

- 7.2.3. LiDAR Sensors

- 7.2.4. Ultrasonic Sensors

- 7.2.5. Infrared Sensors

- 7.2.6. Others

- 7.3. Market Analysis, Insights and Forecast - by LOA

- 7.3.1. L1

- 7.3.2. L2

- 7.3.3. L3

- 7.3.4. L4

- 7.3.5. L5

- 7.4. Market Analysis, Insights and Forecast - by Sales Channel

- 7.4.1. Passenger Cars

- 7.4.2. Light Commercial Vehicles (LCV)

- 7.4.3. Heavy Commercial Vehicles (HCV)

- 7.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.5.1. OEM

- 7.5.2. Sales Channel

- 7.1. Market Analysis, Insights and Forecast - by System Type

- 8. South America Automotive Adas Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by System Type

- 8.1.1. Adaptive Cruise Control (ACC)

- 8.1.2. Automatic Emergency Braking (AEB)

- 8.1.3. Lane Departure Warning (LDW)

- 8.1.4. Blind Spot Detection (BSD).

- 8.1.5. Forward Collision Warning (FCW)

- 8.1.6. Driver Monitoring System (DMS)

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Sensor Type

- 8.2.1. Radar Sensors

- 8.2.2. Camera Sensors

- 8.2.3. LiDAR Sensors

- 8.2.4. Ultrasonic Sensors

- 8.2.5. Infrared Sensors

- 8.2.6. Others

- 8.3. Market Analysis, Insights and Forecast - by LOA

- 8.3.1. L1

- 8.3.2. L2

- 8.3.3. L3

- 8.3.4. L4

- 8.3.5. L5

- 8.4. Market Analysis, Insights and Forecast - by Sales Channel

- 8.4.1. Passenger Cars

- 8.4.2. Light Commercial Vehicles (LCV)

- 8.4.3. Heavy Commercial Vehicles (HCV)

- 8.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.5.1. OEM

- 8.5.2. Sales Channel

- 8.1. Market Analysis, Insights and Forecast - by System Type

- 9. Europe Automotive Adas Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by System Type

- 9.1.1. Adaptive Cruise Control (ACC)

- 9.1.2. Automatic Emergency Braking (AEB)

- 9.1.3. Lane Departure Warning (LDW)

- 9.1.4. Blind Spot Detection (BSD).

- 9.1.5. Forward Collision Warning (FCW)

- 9.1.6. Driver Monitoring System (DMS)

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Sensor Type

- 9.2.1. Radar Sensors

- 9.2.2. Camera Sensors

- 9.2.3. LiDAR Sensors

- 9.2.4. Ultrasonic Sensors

- 9.2.5. Infrared Sensors

- 9.2.6. Others

- 9.3. Market Analysis, Insights and Forecast - by LOA

- 9.3.1. L1

- 9.3.2. L2

- 9.3.3. L3

- 9.3.4. L4

- 9.3.5. L5

- 9.4. Market Analysis, Insights and Forecast - by Sales Channel

- 9.4.1. Passenger Cars

- 9.4.2. Light Commercial Vehicles (LCV)

- 9.4.3. Heavy Commercial Vehicles (HCV)

- 9.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.5.1. OEM

- 9.5.2. Sales Channel

- 9.1. Market Analysis, Insights and Forecast - by System Type

- 10. Middle East & Africa Automotive Adas Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by System Type

- 10.1.1. Adaptive Cruise Control (ACC)

- 10.1.2. Automatic Emergency Braking (AEB)

- 10.1.3. Lane Departure Warning (LDW)

- 10.1.4. Blind Spot Detection (BSD).

- 10.1.5. Forward Collision Warning (FCW)

- 10.1.6. Driver Monitoring System (DMS)

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Sensor Type

- 10.2.1. Radar Sensors

- 10.2.2. Camera Sensors

- 10.2.3. LiDAR Sensors

- 10.2.4. Ultrasonic Sensors

- 10.2.5. Infrared Sensors

- 10.2.6. Others

- 10.3. Market Analysis, Insights and Forecast - by LOA

- 10.3.1. L1

- 10.3.2. L2

- 10.3.3. L3

- 10.3.4. L4

- 10.3.5. L5

- 10.4. Market Analysis, Insights and Forecast - by Sales Channel

- 10.4.1. Passenger Cars

- 10.4.2. Light Commercial Vehicles (LCV)

- 10.4.3. Heavy Commercial Vehicles (HCV)

- 10.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.5.1. OEM

- 10.5.2. Sales Channel

- 10.1. Market Analysis, Insights and Forecast - by System Type

- 11. Asia Pacific Automotive Adas Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by System Type

- 11.1.1. Adaptive Cruise Control (ACC)

- 11.1.2. Automatic Emergency Braking (AEB)

- 11.1.3. Lane Departure Warning (LDW)

- 11.1.4. Blind Spot Detection (BSD).

- 11.1.5. Forward Collision Warning (FCW)

- 11.1.6. Driver Monitoring System (DMS)

- 11.1.7. Others

- 11.2. Market Analysis, Insights and Forecast - by Sensor Type

- 11.2.1. Radar Sensors

- 11.2.2. Camera Sensors

- 11.2.3. LiDAR Sensors

- 11.2.4. Ultrasonic Sensors

- 11.2.5. Infrared Sensors

- 11.2.6. Others

- 11.3. Market Analysis, Insights and Forecast - by LOA

- 11.3.1. L1

- 11.3.2. L2

- 11.3.3. L3

- 11.3.4. L4

- 11.3.5. L5

- 11.4. Market Analysis, Insights and Forecast - by Sales Channel

- 11.4.1. Passenger Cars

- 11.4.2. Light Commercial Vehicles (LCV)

- 11.4.3. Heavy Commercial Vehicles (HCV)

- 11.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 11.5.1. OEM

- 11.5.2. Sales Channel

- 11.1. Market Analysis, Insights and Forecast - by System Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Continental Ag

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Delphi Automotive PLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Robert Bosch Gmbh

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Aisin Seiki Co. Ltd.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Denso Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Trw Automotive Holdings Corp.

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Mobileye NV

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 Continental Ag

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Adas Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Adas Revenue (million), by System Type 2025 & 2033

- Figure 3: North America Automotive Adas Revenue Share (%), by System Type 2025 & 2033

- Figure 4: North America Automotive Adas Revenue (million), by Sensor Type 2025 & 2033

- Figure 5: North America Automotive Adas Revenue Share (%), by Sensor Type 2025 & 2033

- Figure 6: North America Automotive Adas Revenue (million), by LOA 2025 & 2033

- Figure 7: North America Automotive Adas Revenue Share (%), by LOA 2025 & 2033

- Figure 8: North America Automotive Adas Revenue (million), by Sales Channel 2025 & 2033

- Figure 9: North America Automotive Adas Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 10: North America Automotive Adas Revenue (million), by Vehicle Type 2025 & 2033

- Figure 11: North America Automotive Adas Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: North America Automotive Adas Revenue (million), by Country 2025 & 2033

- Figure 13: North America Automotive Adas Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Automotive Adas Revenue (million), by System Type 2025 & 2033

- Figure 15: South America Automotive Adas Revenue Share (%), by System Type 2025 & 2033

- Figure 16: South America Automotive Adas Revenue (million), by Sensor Type 2025 & 2033

- Figure 17: South America Automotive Adas Revenue Share (%), by Sensor Type 2025 & 2033

- Figure 18: South America Automotive Adas Revenue (million), by LOA 2025 & 2033

- Figure 19: South America Automotive Adas Revenue Share (%), by LOA 2025 & 2033

- Figure 20: South America Automotive Adas Revenue (million), by Sales Channel 2025 & 2033

- Figure 21: South America Automotive Adas Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 22: South America Automotive Adas Revenue (million), by Vehicle Type 2025 & 2033

- Figure 23: South America Automotive Adas Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 24: South America Automotive Adas Revenue (million), by Country 2025 & 2033

- Figure 25: South America Automotive Adas Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Automotive Adas Revenue (million), by System Type 2025 & 2033

- Figure 27: Europe Automotive Adas Revenue Share (%), by System Type 2025 & 2033

- Figure 28: Europe Automotive Adas Revenue (million), by Sensor Type 2025 & 2033

- Figure 29: Europe Automotive Adas Revenue Share (%), by Sensor Type 2025 & 2033

- Figure 30: Europe Automotive Adas Revenue (million), by LOA 2025 & 2033

- Figure 31: Europe Automotive Adas Revenue Share (%), by LOA 2025 & 2033

- Figure 32: Europe Automotive Adas Revenue (million), by Sales Channel 2025 & 2033

- Figure 33: Europe Automotive Adas Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 34: Europe Automotive Adas Revenue (million), by Vehicle Type 2025 & 2033

- Figure 35: Europe Automotive Adas Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 36: Europe Automotive Adas Revenue (million), by Country 2025 & 2033

- Figure 37: Europe Automotive Adas Revenue Share (%), by Country 2025 & 2033

- Figure 38: Middle East & Africa Automotive Adas Revenue (million), by System Type 2025 & 2033

- Figure 39: Middle East & Africa Automotive Adas Revenue Share (%), by System Type 2025 & 2033

- Figure 40: Middle East & Africa Automotive Adas Revenue (million), by Sensor Type 2025 & 2033

- Figure 41: Middle East & Africa Automotive Adas Revenue Share (%), by Sensor Type 2025 & 2033

- Figure 42: Middle East & Africa Automotive Adas Revenue (million), by LOA 2025 & 2033

- Figure 43: Middle East & Africa Automotive Adas Revenue Share (%), by LOA 2025 & 2033

- Figure 44: Middle East & Africa Automotive Adas Revenue (million), by Sales Channel 2025 & 2033

- Figure 45: Middle East & Africa Automotive Adas Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 46: Middle East & Africa Automotive Adas Revenue (million), by Vehicle Type 2025 & 2033

- Figure 47: Middle East & Africa Automotive Adas Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 48: Middle East & Africa Automotive Adas Revenue (million), by Country 2025 & 2033

- Figure 49: Middle East & Africa Automotive Adas Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Automotive Adas Revenue (million), by System Type 2025 & 2033

- Figure 51: Asia Pacific Automotive Adas Revenue Share (%), by System Type 2025 & 2033

- Figure 52: Asia Pacific Automotive Adas Revenue (million), by Sensor Type 2025 & 2033

- Figure 53: Asia Pacific Automotive Adas Revenue Share (%), by Sensor Type 2025 & 2033

- Figure 54: Asia Pacific Automotive Adas Revenue (million), by LOA 2025 & 2033

- Figure 55: Asia Pacific Automotive Adas Revenue Share (%), by LOA 2025 & 2033

- Figure 56: Asia Pacific Automotive Adas Revenue (million), by Sales Channel 2025 & 2033

- Figure 57: Asia Pacific Automotive Adas Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 58: Asia Pacific Automotive Adas Revenue (million), by Vehicle Type 2025 & 2033

- Figure 59: Asia Pacific Automotive Adas Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 60: Asia Pacific Automotive Adas Revenue (million), by Country 2025 & 2033

- Figure 61: Asia Pacific Automotive Adas Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Adas Revenue million Forecast, by System Type 2020 & 2033

- Table 2: Global Automotive Adas Revenue million Forecast, by Sensor Type 2020 & 2033

- Table 3: Global Automotive Adas Revenue million Forecast, by LOA 2020 & 2033

- Table 4: Global Automotive Adas Revenue million Forecast, by Sales Channel 2020 & 2033

- Table 5: Global Automotive Adas Revenue million Forecast, by Vehicle Type 2020 & 2033

- Table 6: Global Automotive Adas Revenue million Forecast, by Region 2020 & 2033

- Table 7: Global Automotive Adas Revenue million Forecast, by System Type 2020 & 2033

- Table 8: Global Automotive Adas Revenue million Forecast, by Sensor Type 2020 & 2033

- Table 9: Global Automotive Adas Revenue million Forecast, by LOA 2020 & 2033

- Table 10: Global Automotive Adas Revenue million Forecast, by Sales Channel 2020 & 2033

- Table 11: Global Automotive Adas Revenue million Forecast, by Vehicle Type 2020 & 2033

- Table 12: Global Automotive Adas Revenue million Forecast, by Country 2020 & 2033

- Table 13: United States Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Canada Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Mexico Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Adas Revenue million Forecast, by System Type 2020 & 2033

- Table 17: Global Automotive Adas Revenue million Forecast, by Sensor Type 2020 & 2033

- Table 18: Global Automotive Adas Revenue million Forecast, by LOA 2020 & 2033

- Table 19: Global Automotive Adas Revenue million Forecast, by Sales Channel 2020 & 2033

- Table 20: Global Automotive Adas Revenue million Forecast, by Vehicle Type 2020 & 2033

- Table 21: Global Automotive Adas Revenue million Forecast, by Country 2020 & 2033

- Table 22: Brazil Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Argentina Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Rest of South America Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Global Automotive Adas Revenue million Forecast, by System Type 2020 & 2033

- Table 26: Global Automotive Adas Revenue million Forecast, by Sensor Type 2020 & 2033

- Table 27: Global Automotive Adas Revenue million Forecast, by LOA 2020 & 2033

- Table 28: Global Automotive Adas Revenue million Forecast, by Sales Channel 2020 & 2033

- Table 29: Global Automotive Adas Revenue million Forecast, by Vehicle Type 2020 & 2033

- Table 30: Global Automotive Adas Revenue million Forecast, by Country 2020 & 2033

- Table 31: United Kingdom Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Germany Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: France Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: Italy Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: Spain Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Russia Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Benelux Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: Nordics Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 39: Rest of Europe Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Global Automotive Adas Revenue million Forecast, by System Type 2020 & 2033

- Table 41: Global Automotive Adas Revenue million Forecast, by Sensor Type 2020 & 2033

- Table 42: Global Automotive Adas Revenue million Forecast, by LOA 2020 & 2033

- Table 43: Global Automotive Adas Revenue million Forecast, by Sales Channel 2020 & 2033

- Table 44: Global Automotive Adas Revenue million Forecast, by Vehicle Type 2020 & 2033

- Table 45: Global Automotive Adas Revenue million Forecast, by Country 2020 & 2033

- Table 46: Turkey Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 47: Israel Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: GCC Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 49: North Africa Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: South Africa Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 51: Rest of Middle East & Africa Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Global Automotive Adas Revenue million Forecast, by System Type 2020 & 2033

- Table 53: Global Automotive Adas Revenue million Forecast, by Sensor Type 2020 & 2033

- Table 54: Global Automotive Adas Revenue million Forecast, by LOA 2020 & 2033

- Table 55: Global Automotive Adas Revenue million Forecast, by Sales Channel 2020 & 2033

- Table 56: Global Automotive Adas Revenue million Forecast, by Vehicle Type 2020 & 2033

- Table 57: Global Automotive Adas Revenue million Forecast, by Country 2020 & 2033

- Table 58: China Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 59: India Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 60: Japan Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 61: South Korea Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: ASEAN Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 63: Oceania Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Rest of Asia Pacific Automotive Adas Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Adas?

The projected CAGR is approximately 27%.

2. Which companies are prominent players in the Automotive Adas?

Key companies in the market include Continental Ag, Delphi Automotive PLC, Robert Bosch Gmbh, Aisin Seiki Co. Ltd., Denso Corporation, Trw Automotive Holdings Corp., Mobileye NV.

3. What are the main segments of the Automotive Adas?

The market segments include System Type, Sensor Type, LOA, Sales Channel, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 339300 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Adas," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Adas report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Adas?

To stay informed about further developments, trends, and reports in the Automotive Adas, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence