Key Insights

The Spanish lubricants market is projected to experience robust growth, with a Compound Annual Growth Rate (CAGR) of 3.5% from 2024 to 2033. The market size was valued at approximately 4 billion Euros in 2024. This expansion is propelled by consistent demand from critical sectors like automotive and heavy machinery. The automotive industry, supported by a recovering new vehicle market and a large existing vehicle base requiring regular maintenance, will remain a significant consumer of engine oils and transmission fluids. The heavy equipment sector, covering construction, mining, and agriculture, will also drive demand for high-performance lubricants to maintain operational efficiency and equipment lifespan. Emerging trends, including the adoption of advanced, long-lasting lubricants that enhance fuel efficiency and minimize waste, are further shaping market dynamics. The increasing demand for specialized industrial lubricants, particularly in metallurgy and metalworking, is contributing to market diversification.

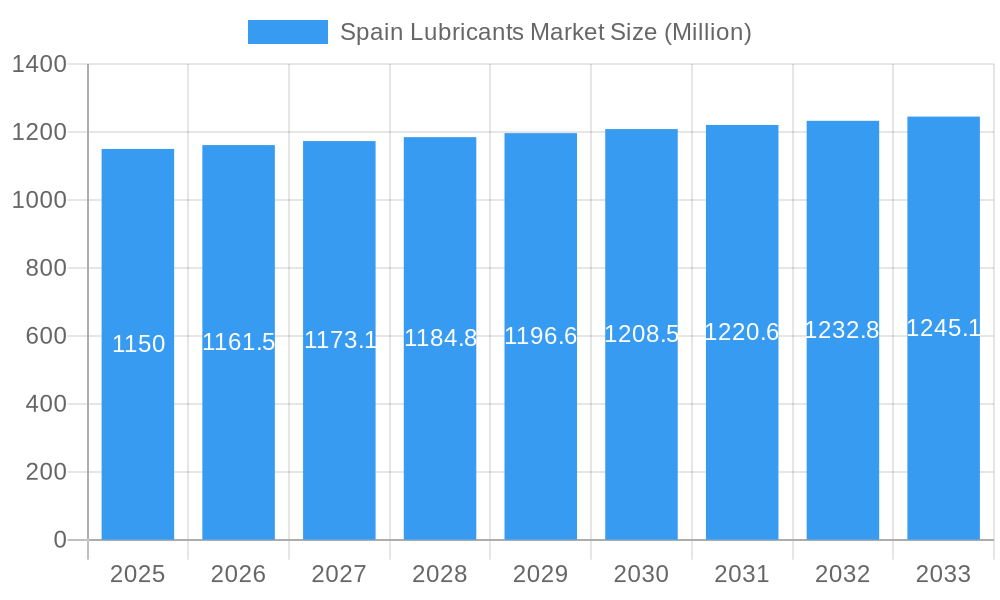

Spain Lubricants Market Market Size (In Billion)

While the Spanish lubricants market shows a positive growth outlook, certain factors may impede its expansion. The growing adoption of electric vehicles (EVs) presents a long-term challenge to traditional engine oil demand. Although widespread EV adoption is still evolving, EVs necessitate specialized fluids. Economic instability and potential price volatility in raw materials, such as base oils derived from crude oil, could impact profitability and consumer spending. Stringent environmental regulations, while fostering the development of sustainable and biodegradable lubricants, can also escalate manufacturing costs. The market features intense competition among major global players including Shell Plc, Exxon Mobil Corporation, and TotalEnergies SE, alongside domestic leaders like Cepsa and Repsol. These companies are competing through product innovation, strategic alliances, and competitive pricing. The forecast period is expected to see continuous product development to align with evolving industry requirements and regulatory frameworks.

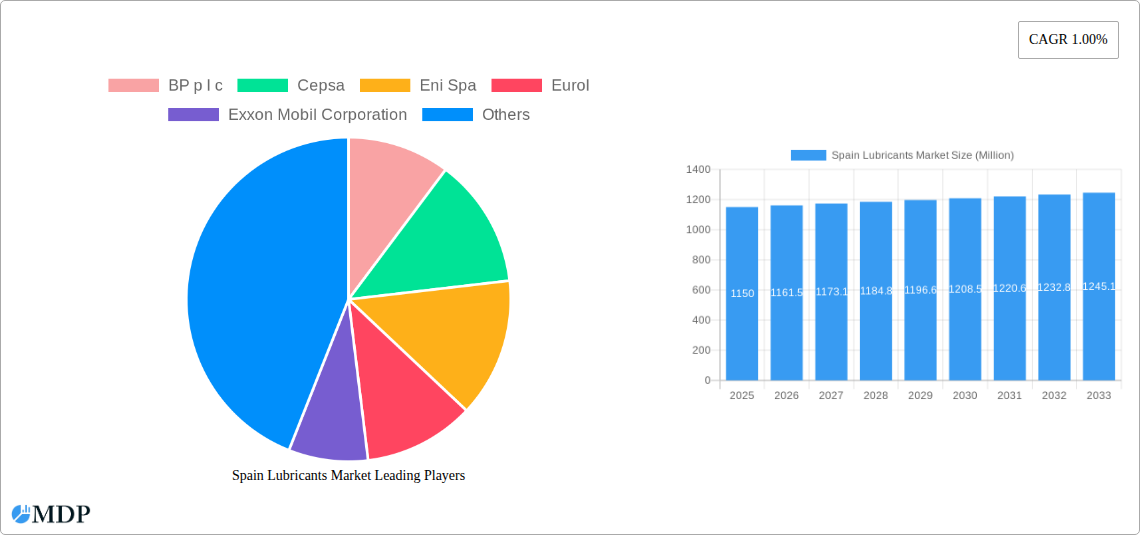

Spain Lubricants Market Company Market Share

Spain Lubricants Market: Comprehensive Growth Analysis and Future Projections (2019-2033)

This in-depth report provides an exhaustive analysis of the Spain Lubricants Market, a vital sector projected to reach a market size of over 12,000 Million by 2025. Delving into historical performance, current trends, and future forecasts from 2019 to 2033, with a base and estimated year of 2025, this study offers actionable insights for industry stakeholders. Explore market dynamics, leading players, segment-specific growth, and strategic opportunities within the rapidly evolving Spanish lubricants industry.

Spain Lubricants Market Market Dynamics & Concentration

The Spain Lubricants Market exhibits a moderately concentrated landscape, with key players like Shell Plc, Repsol, Cepsa, and Exxon Mobil Corporation holding significant market share. Innovation drivers are largely centered around developing high-performance, fuel-efficient, and environmentally friendly lubricants, responding to stringent EU regulations and evolving automotive and industrial demands. Regulatory frameworks, particularly concerning emissions and biodegradability, are shaping product development and market entry. Product substitutes, such as advanced synthetic fluids and greases, are gaining traction, challenging traditional mineral oil-based products. End-user trends highlight a growing preference for specialized lubricants across various sectors, including the robust Automotive and Heavy Equipment industries. Mergers and acquisitions (M&A) activities are expected to continue as companies seek to expand their product portfolios, geographical reach, and technological capabilities. For instance, recent strategic alliances and smaller acquisitions have been observed, totaling approximately 5-7 significant M&A deals in the past five years, aimed at consolidating market presence and acquiring innovative technologies.

Spain Lubricants Market Industry Trends & Analysis

The Spain Lubricants Market is poised for robust growth, driven by a confluence of factors that are reshaping its trajectory. The Spanish economy's recovery and expansion, particularly in the automotive sector, directly translates into increased demand for engine oils and transmission fluids. Furthermore, the burgeoning heavy equipment and metallurgy and metalworking industries, crucial for infrastructure development and manufacturing, are significant consumers of specialized lubricants like hydraulic fluids and metalworking fluids. The power generation sector also presents a consistent demand for high-performance lubricants for turbines and other machinery. A key trend is the increasing adoption of synthetic lubricants, driven by their superior performance characteristics, including better thermal stability, extended drain intervals, and enhanced protection against wear and tear. This shift is particularly evident in the automotive segment, where manufacturers are specifying advanced synthetic formulations for their latest engine technologies.

Technological disruptions are also playing a pivotal role. The development of environmentally friendly lubricants, biodegradable formulations, and those with reduced friction coefficients are gaining significant traction, aligning with sustainability goals and stringent EU regulations. These innovations not only offer environmental benefits but also contribute to improved fuel efficiency and reduced operational costs for end-users. Consumer preferences are evolving towards products that offer longer service life, better protection, and contribute to lower emissions. This is pushing manufacturers to invest heavily in research and development.

The competitive dynamics within the Spain Lubricants Market are characterized by a blend of global majors and strong local players. Companies are increasingly focusing on product differentiation through specialized formulations, advanced additive technologies, and customized solutions for specific industrial applications. The market penetration of advanced lubricants is steadily increasing, moving from niche applications to broader adoption across various sectors. The overall CAGR for the Spain Lubricants Market is projected to be around 3.5% to 4.0% during the forecast period, indicating a healthy and sustained growth trajectory. The market is estimated to reach over 12,000 Million by 2025, with further expansion anticipated through 2033.

Leading Markets & Segments in Spain Lubricants Market

The Spain Lubricants Market is significantly influenced by its dominant segments in both Product Type and End-user Industry.

Dominant Product Types:

- Engine Oils: This segment holds the largest market share, fueled by the extensive automotive sector in Spain, encompassing passenger cars, commercial vehicles, and motorcycles. The increasing vehicle parc, coupled with stringent emission standards that necessitate advanced lubricant formulations, propels the demand for engine oils. Economic policies supporting the automotive industry and infrastructure development contribute to this dominance.

- Hydraulic Fluids: The heavy equipment and metallurgy and metalworking industries are primary drivers for hydraulic fluids. Infrastructure projects, construction activities, and the manufacturing sector's reliance on hydraulic machinery ensure a consistent and substantial demand. Government investments in infrastructure and industrial modernization are key factors supporting this segment.

- Transmission and Gear Oils: Essential for the smooth functioning of vehicles and industrial machinery, this segment benefits from the same growth drivers as engine oils and hydraulic fluids. The need for efficient power transmission and wear protection in a diverse range of applications solidifies its leading position.

Dominant End-user Industries:

- Automotive: As mentioned, this is the cornerstone of the Spain Lubricants Market. The robust fleet of vehicles, coupled with the ongoing technological advancements in engine design, requiring specialized lubricants, makes this the most significant end-user industry.

- Heavy Equipment: This sector, encompassing construction, mining, and agricultural machinery, is a substantial consumer of lubricants. Ongoing infrastructure development projects and the need for reliable machinery operation contribute to its prominent market share.

- Metallurgy and Metalworking: The manufacturing and metal processing industries rely heavily on lubricants for machinery operation, cutting, grinding, and forming processes. Spain's strong industrial base ensures a consistent demand for metalworking fluids and industrial lubricants.

The dominance of these segments is further underscored by factors such as economic policies encouraging industrial activity, investment in infrastructure that drives the need for heavy equipment, and consumer preferences for reliable and long-lasting machinery, all of which necessitate high-quality lubrication solutions. The Other Pr and Other En segments, while smaller, are also experiencing growth due to specialization and emerging industrial applications.

Spain Lubricants Market Product Developments

Product innovation in the Spain Lubricants Market is characterized by a strong focus on enhanced performance, environmental sustainability, and specialized applications. Manufacturers are actively developing advanced engine oils with superior thermal stability and anti-wear properties, contributing to extended engine life and improved fuel efficiency. The development of biodegradable and low-VOC (Volatile Organic Compound) lubricants for hydraulic fluids and metalworking fluids is a key trend, driven by increasing environmental regulations and corporate sustainability initiatives. Innovations in greases are focused on extending service intervals and improving resistance to extreme temperatures and pressures, catering to demanding applications in heavy industries. Competitive advantages are being gained through proprietary additive technologies, customized formulations for specific OEM requirements, and the integration of nanotechnology for enhanced lubrication properties, offering solutions that meet the evolving needs of the automotive, heavy equipment, and metallurgy and metalworking sectors.

Key Drivers of Spain Lubricants Market Growth

The Spain Lubricants Market is propelled by several significant growth drivers. The recovery and continued expansion of the Spanish economy, particularly in the automotive and manufacturing sectors, directly boosts demand for lubricants. Advancements in automotive technology, including the rise of electric and hybrid vehicles (requiring specialized fluids) and more sophisticated internal combustion engines, necessitate the use of high-performance synthetic lubricants. Growing investments in infrastructure development across Spain fuels the demand for heavy equipment and, consequently, the lubricants required for their operation. Furthermore, stringent environmental regulations are pushing the development and adoption of eco-friendly and energy-efficient lubricant formulations, creating a niche for innovative products. Finally, increasing industrial automation and the growth of the metallurgy and metalworking sector continue to drive demand for specialized industrial lubricants.

Challenges in the Spain Lubricants Market Market

Despite the positive growth outlook, the Spain Lubricants Market faces several challenges. The increasing adoption of electric vehicles (EVs) poses a long-term threat to traditional engine oil demand, although EVs still require specialized transmission fluids and coolants. Fluctuations in raw material prices, particularly crude oil, can significantly impact production costs and profit margins. Intense competition from both global and local players, coupled with price sensitivity among some end-users, can lead to margin pressures. Stringent and evolving environmental regulations require continuous investment in R&D for compliant products, which can be costly. Additionally, complexities in the supply chain, including logistics and distribution networks, can present operational challenges. The market also contends with the threat of product counterfeiting, which can damage brand reputation and compromise performance.

Emerging Opportunities in Spain Lubricants Market

Several emerging opportunities are set to shape the future of the Spain Lubricants Market. The continued growth in the automotive aftermarket for maintenance and repair services offers a stable revenue stream. The increasing demand for biodegradable and bio-based lubricants presents a significant opportunity as environmental consciousness rises. Technological advancements in industrial machinery are creating a need for highly specialized lubricants with advanced properties, opening avenues for niche product development. Strategic partnerships and collaborations between lubricant manufacturers and OEMs (Original Equipment Manufacturers) can lead to the development of tailored solutions and secure long-term supply contracts. Furthermore, the expanding renewable energy sector, particularly wind power, requires specialized lubricants for turbines, presenting a growing market segment. The ongoing digitalization of industries also creates opportunities for smart lubricants with diagnostic capabilities.

Leading Players in the Spain Lubricants Market Sector

- BP p l c

- Cepsa

- Eni Spa

- Eurol

- Exxon Mobil Corporation

- FUCHS

- Galp

- LUKOIL

- Motul

- Repsol

- Shell Plc

- TotalEnergies SE

Key Milestones in Spain Lubricants Market Industry

The recent developments about the major players in the market are being covered in the complete study. These developments highlight the industry's dynamic nature and its adaptation to evolving market demands and technological advancements:

- 2023: Shell Plc launched a new range of fuel-efficient engine oils designed to meet the latest Euro 7 emission standards, reinforcing its commitment to sustainability.

- 2023: Repsol announced significant investment in R&D for biodegradable lubricants, focusing on agricultural and marine applications.

- 2022: Cepsa expanded its industrial lubricant portfolio with new formulations for high-temperature metalworking applications, catering to the growing manufacturing sector.

- 2021: Exxon Mobil Corporation introduced advanced synthetic transmission fluids for heavy-duty commercial vehicles, enhancing durability and performance in demanding conditions.

- 2020: TotalEnergies SE acquired a stake in a bio-lubricant production facility, signaling its strategic shift towards sustainable lubricant solutions.

Strategic Outlook for Spain Lubricants Market Market

The strategic outlook for the Spain Lubricants Market indicates a period of sustained growth and innovation. Key accelerators include the ongoing transition towards high-performance synthetic lubricants driven by technological advancements in vehicles and machinery. The increasing focus on sustainability will continue to fuel demand for biodegradable and environmentally friendly formulations, presenting opportunities for companies with strong R&D capabilities in this area. Strategic partnerships with OEMs and participation in emerging sectors like renewable energy will be crucial for market expansion. The market will also benefit from continued government support for industrial development and infrastructure projects. Companies that can adapt to the evolving landscape, particularly the impact of electrification, and offer specialized, high-value solutions are well-positioned for future success in this dynamic market.

Spain Lubricants Market Segmentation

-

1. Product Type

- 1.1. Engine Oils

- 1.2. Greases

- 1.3. Hydraulic Fluids

- 1.4. Metalworking Fluids

- 1.5. Transmission and Gear Oils

- 1.6. Other Pr

-

2. End-user Industry

- 2.1. Automotive

- 2.2. Heavy Equipment

- 2.3. Metallurgy and Metalworking

- 2.4. Power Generation

- 2.5. Other En

Spain Lubricants Market Segmentation By Geography

- 1. Spain

Spain Lubricants Market Regional Market Share

Geographic Coverage of Spain Lubricants Market

Spain Lubricants Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Engine Oils

- 5.1.2. Greases

- 5.1.3. Hydraulic Fluids

- 5.1.4. Metalworking Fluids

- 5.1.5. Transmission and Gear Oils

- 5.1.6. Other Pr

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Automotive

- 5.2.2. Heavy Equipment

- 5.2.3. Metallurgy and Metalworking

- 5.2.4. Power Generation

- 5.2.5. Other En

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Spain Lubricants Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Engine Oils

- 6.1.2. Greases

- 6.1.3. Hydraulic Fluids

- 6.1.4. Metalworking Fluids

- 6.1.5. Transmission and Gear Oils

- 6.1.6. Other Pr

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Automotive

- 6.2.2. Heavy Equipment

- 6.2.3. Metallurgy and Metalworking

- 6.2.4. Power Generation

- 6.2.5. Other En

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 BP p l c

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Cepsa

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Eni Spa

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Eurol

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Exxon Mobil Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 FUCHS

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Galp

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 LUKOIL

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Motul

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Repsol

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Shell Plc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 TotalEnergies SE*List Not Exhaustive

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 BP p l c

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Spain Lubricants Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Spain Lubricants Market Share (%) by Company 2025

List of Tables

- Table 1: Spain Lubricants Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Spain Lubricants Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Spain Lubricants Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Spain Lubricants Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 5: Spain Lubricants Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Spain Lubricants Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Lubricants Market?

The projected CAGR is approximately 3.5%.

2. Which companies are prominent players in the Spain Lubricants Market?

Key companies in the market include BP p l c, Cepsa, Eni Spa, Eurol, Exxon Mobil Corporation, FUCHS, Galp, LUKOIL, Motul, Repsol, Shell Plc, TotalEnergies SE*List Not Exhaustive.

3. What are the main segments of the Spain Lubricants Market?

The market segments include Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 4 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Investments in Power Generation Industry; Growing Demand for Agricultural Machinery; Other Drivers.

6. What are the notable trends driving market growth?

Growing Investments in the Power Generation Industry.

7. Are there any restraints impacting market growth?

Growing Investments in Power Generation Industry; Growing Demand for Agricultural Machinery; Other Drivers.

8. Can you provide examples of recent developments in the market?

The recent developments about the major players in the market are being covered in the complete study.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Lubricants Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Lubricants Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Lubricants Market?

To stay informed about further developments, trends, and reports in the Spain Lubricants Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence