Key Insights

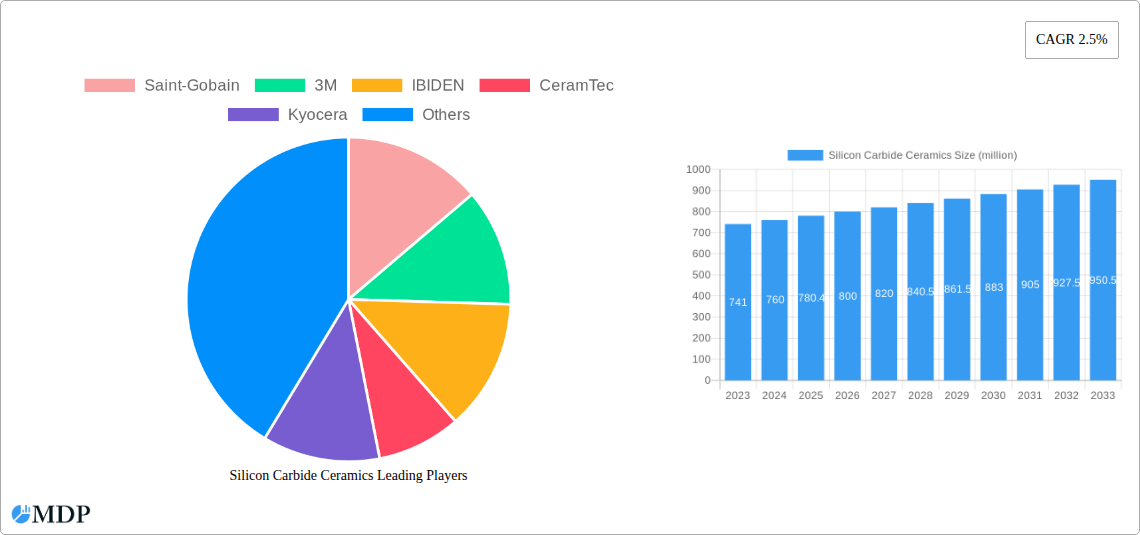

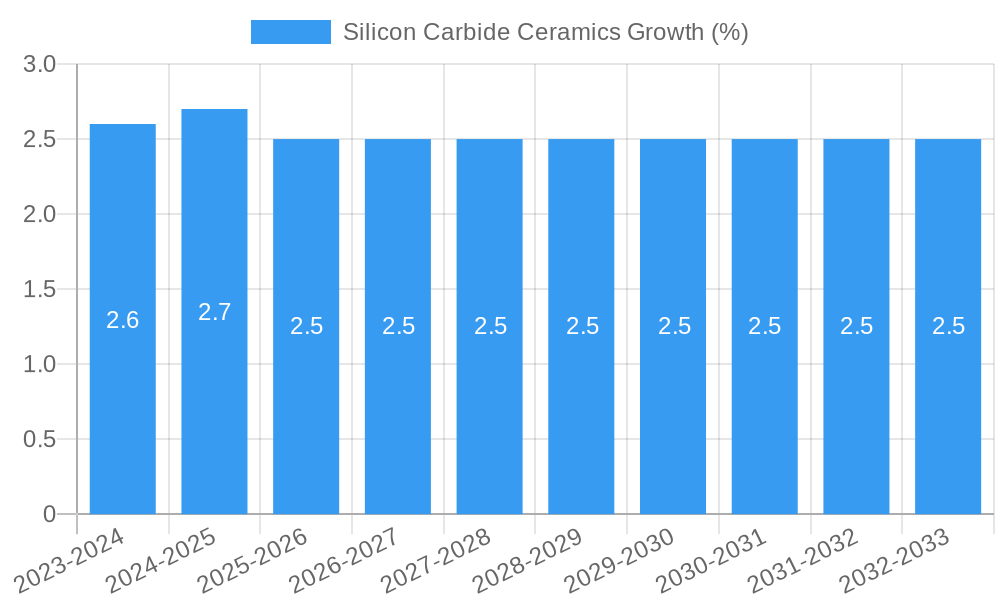

The global Silicon Carbide Ceramics market is poised for steady growth, projected to reach approximately $780.4 million by 2025. This expansion is driven by the inherent superior properties of silicon carbide, including exceptional hardness, thermal conductivity, and chemical resistance. These attributes make it an indispensable material in demanding applications across various industries. Machinery manufacturing, a significant consumer, benefits from silicon carbide's use in wear-resistant components, bearings, and seals, enhancing equipment longevity and performance. The metallurgical industry leverages its high-temperature resistance for furnace linings and crucibles, while chemical engineering utilizes its inertness for corrosive environments. Furthermore, the aerospace & defense sector relies on silicon carbide for lightweight, high-strength components, and the burgeoning semiconductor industry employs it for its thermal management capabilities in advanced electronic devices. This consistent demand, coupled with ongoing technological advancements and material innovation, underpins the projected 2.5% CAGR over the forecast period, indicating a robust and evolving market.

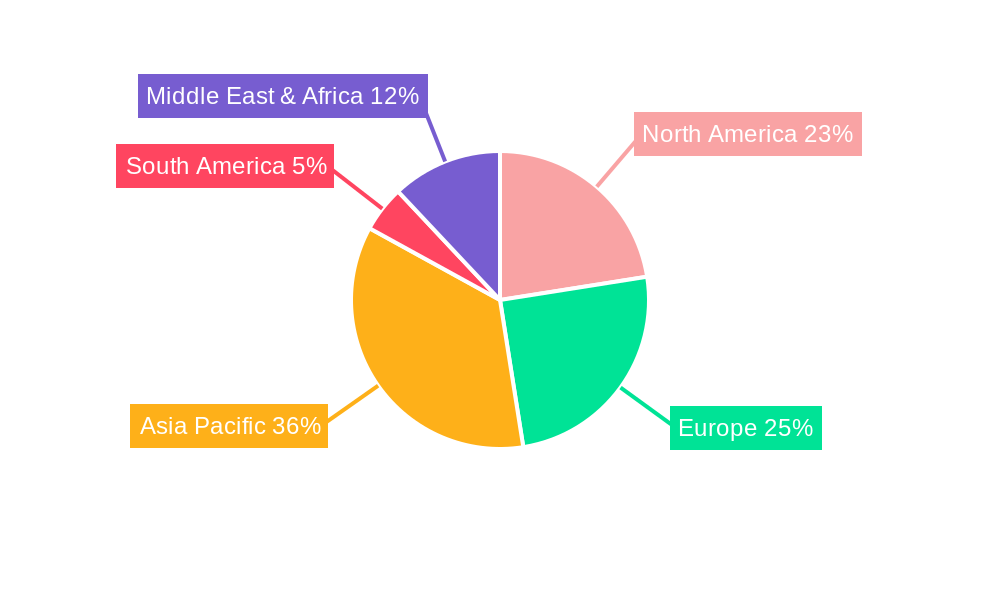

The market's trajectory is further shaped by key trends and the strategic focus of leading companies. The increasing adoption of sintered silicon carbide, known for its high density and mechanical strength, is a notable trend, catering to increasingly stringent performance requirements. Similarly, advancements in reaction-bonded silicon carbide offer cost-effective solutions without significant compromise on properties. As industries push for greater efficiency and sustainability, the demand for high-performance materials like silicon carbide is expected to rise. Geographically, Asia Pacific, particularly China, is emerging as a powerhouse in both production and consumption, fueled by its expansive manufacturing base and rapid technological development. North America and Europe remain significant markets due to their established industrial ecosystems and strong R&D investments. Emerging applications in renewable energy and advanced electronics will continue to fuel innovation and market diversification, presenting both opportunities and challenges for market participants.

Uncover the critical insights and future trajectory of the global Silicon Carbide Ceramics market. This comprehensive report delves into the dynamic forces shaping this high-performance material sector, offering an in-depth analysis of market trends, leading players, and lucrative opportunities. Essential for stakeholders in Machinery Manufacturing, Metallurgical Industry, Chemical Engineering, Aerospace & Defense, Semiconductor, and Automotive sectors.

Silicon Carbide Ceramics Market Dynamics & Concentration

The global Silicon Carbide (SiC) ceramics market is characterized by a moderately concentrated landscape, with a few key players holding significant market share, such as Saint-Gobain, 3M, IBIDEN, CeramTec, and Kyocera. Innovation is a primary driver, fueled by the increasing demand for materials capable of withstanding extreme temperatures, harsh chemical environments, and high mechanical stress. Advancements in manufacturing processes, particularly in sintering techniques and chemical vapor deposition (CVD), are continuously improving material properties and expanding application potential. Regulatory frameworks, while generally supportive of advanced material development, can vary by region, impacting market access and material compliance. Product substitutes, while present in some lower-end applications, often fall short of SiC's superior performance in critical areas like thermal conductivity, hardness, and chemical inertness. End-user trends are strongly influenced by the pursuit of efficiency and longevity in industrial processes, driving adoption across various demanding sectors. Mergers and acquisitions (M&A) activity, while not excessively high, has seen strategic consolidation as companies aim to expand their product portfolios and geographical reach. For instance, historical M&A deal counts in the advanced ceramics sector typically range from xx to xx annually, reflecting a strategic approach to growth.

Silicon Carbide Ceramics Industry Trends & Analysis

The Silicon Carbide ceramics industry is poised for robust growth, driven by an increasing demand for high-performance materials across a multitude of industrial applications. The projected Compound Annual Growth Rate (CAGR) for the SiC ceramics market is estimated to be approximately 6.8%, reaching a market size of over $XX million by 2033. This expansion is propelled by several key market growth drivers. Firstly, the burgeoning semiconductor industry's reliance on SiC substrates for advanced power electronics and LEDs, due to their superior electrical and thermal properties compared to silicon, represents a significant demand catalyst. Secondly, the aerospace and defense sectors are increasingly adopting SiC ceramics for their lightweight, high-strength, and thermal resistance capabilities in critical components like turbine blades, engine parts, and armor plating. The automotive industry's push towards electric vehicles (EVs) and enhanced fuel efficiency also contributes substantially, as SiC power semiconductors enable more efficient inverters and on-board chargers, reducing energy loss and extending battery range.

Technological disruptions are central to the industry's evolution. Innovations in manufacturing techniques, including advanced sintering methods for enhanced density and purity, and the refinement of CVD processes for precise coating applications, are continuously improving material performance and enabling new use cases. Research into nanostructured SiC and composite materials is also opening avenues for even greater strength and thermal management capabilities. Consumer preferences are indirectly influencing the market by demanding more durable, efficient, and sustainable products, which SiC ceramics directly enable through their longevity and contribution to energy savings. Competitive dynamics are intense, with leading players like Saint-Gobain, 3M, IBIDEN, CeramTec, and Kyocera investing heavily in R&D and strategic partnerships to maintain their market leadership. The market penetration of SiC ceramics is steadily increasing, moving beyond niche applications into mainstream industrial adoption.

Leading Markets & Segments in Silicon Carbide Ceramics

The Aerospace & Defense segment is emerging as a dominant force within the Silicon Carbide Ceramics market, driven by its unparalleled ability to meet stringent performance requirements.

Dominant Application: Aerospace & Defense

- Key Drivers:

- Extreme Performance Demands: The inherent properties of SiC ceramics, including exceptional thermal shock resistance, high hardness, and chemical inertness, are critical for components operating in high-temperature and corrosive environments found in aircraft engines, missile systems, and satellite technology.

- Lightweighting Initiatives: The aerospace industry's continuous drive to reduce aircraft weight for improved fuel efficiency and payload capacity makes SiC ceramics an attractive alternative to heavier metallic alloys. This contributes to significant cost savings over the lifecycle of aircraft.

- Ballistic Protection: The superior hardness and strength of SiC ceramics make them a key material in the development of advanced body armor and vehicle protection systems, offering a significant improvement in protection-to-weight ratio.

- Technological Advancements in Propulsion Systems: The development of next-generation jet engines and rocket propulsion systems necessitates materials that can withstand extreme thermal loads and erosive forces. SiC's resilience directly addresses these challenges.

- Key Drivers:

Dominant Type: Sintered Silicon Carbide

- Detailed Dominance Analysis: Sintered Silicon Carbide (SSiC) holds a commanding position within the SiC ceramics market due to its excellent mechanical properties, high purity, and versatility. The sintering process allows for precise control over microstructure, leading to superior hardness, wear resistance, and thermal conductivity. This makes SSiC the material of choice for a wide array of demanding applications. Its widespread adoption in mechanical seals, bearings, and pump components within the chemical and machinery manufacturing industries underscores its dominance. The ability to achieve high densities through advanced sintering techniques further enhances its reliability and performance in critical applications. The cost-effectiveness and scalability of SSiC production also contribute to its market leadership.

Leading Regions and Countries:

- North America and Europe: These regions exhibit strong demand due to their well-established aerospace and defense industries, as well as significant investments in advanced manufacturing and research and development. Stringent regulations on material performance and a focus on technological innovation drive the adoption of high-performance SiC ceramics.

- Asia-Pacific: This region, particularly China, is experiencing rapid growth driven by its expanding semiconductor manufacturing capabilities and increasing investments in aerospace and automotive sectors. Local manufacturers like Shandong Huamei New Material Technology and Jinhong New Material are contributing to market expansion.

Silicon Carbide Ceramics Product Developments

Recent product developments in Silicon Carbide ceramics are focused on enhancing thermal management, increasing mechanical strength, and improving manufacturing efficiency. Innovations include advanced SiC composites with enhanced fracture toughness and the development of novel coating technologies for improved wear and corrosion resistance. CVD Silicon Carbide is being utilized for highly complex geometries in semiconductor manufacturing equipment. These advancements offer significant competitive advantages by enabling components to operate reliably under more extreme conditions, extending product lifespans, and reducing maintenance requirements. Market fit is being broadened as SiC ceramics move into more mainstream applications due to these performance enhancements.

Key Drivers of Silicon Carbide Ceramics Growth

The growth of the Silicon Carbide ceramics market is primarily driven by technological advancements in material science and manufacturing processes, leading to superior performance characteristics like extreme hardness, high thermal conductivity, and chemical inertness. Economically, the increasing demand for energy efficiency across industries, particularly in the automotive sector with the rise of electric vehicles and in industrial machinery, is a major catalyst. Regulatory mandates pushing for higher emission standards and more durable industrial equipment indirectly favor the adoption of long-lasting and efficient SiC components. For example, the semiconductor industry's reliance on SiC for next-generation power electronics is a prime illustration of these interconnected drivers.

Challenges in the Silicon Carbide Ceramics Market

Despite its advantages, the Silicon Carbide ceramics market faces several challenges. High manufacturing costs associated with the complex and energy-intensive production processes, especially for high-purity grades, can be a significant barrier. Brittleness, while improving with advanced techniques, remains a inherent characteristic that requires careful design and handling. Supply chain complexities and raw material availability, particularly for specific precursor materials, can lead to price volatility and lead time issues. Furthermore, established adoption of alternative materials in certain applications, coupled with the need for specialized expertise in processing and implementation, can slow down market penetration. For instance, the cost premium over traditional ceramics can hinder adoption in price-sensitive markets.

Emerging Opportunities in Silicon Carbide Ceramics

Emerging opportunities for Silicon Carbide ceramics are abundant, driven by accelerating technological breakthroughs and expanding application frontiers. The continued evolution of the semiconductor industry, with its insatiable demand for advanced power devices and substrates, presents a substantial growth avenue. Strategic partnerships between SiC manufacturers and end-users, such as those involving companies like IBIDEN and semiconductor giants, are fostering tailored material solutions. Market expansion into renewable energy sectors, including solar inverters and wind turbine components, where SiC’s durability and efficiency are paramount, offers significant long-term growth potential. Furthermore, advancements in additive manufacturing for SiC ceramics could unlock new design possibilities and streamline production for complex geometries, opening up previously inaccessible markets.

Leading Players in the Silicon Carbide Ceramics Sector

- Saint-Gobain

- 3M

- IBIDEN

- CeramTec

- Kyocera

- CoorsTek

- Morgan Advanced Materials

- Schunk

- Mersen

- IPS Ceramics

- Ortech

- ASUZAC

- Fraunhofer IKTS

- Shandong Huamei New Material Technology

- Jinhong New Material

- Sanzer New Materials Technology

- Shantian Abrasive

- SSACC China

- Zhejiang Dongxin New Material Technology

- Ningbo FLK Technology

- Shaanxi UDC

- FCT(Tangshan) New Materials

- Joint Power Shanghai Seals

- Luoyang Pengfei Wear Resistant Materials

- Weifang Zhida Special Ceramics

Key Milestones in Silicon Carbide Ceramics Industry

- 2019: Increased focus on SiC substrates for 5G infrastructure and electric vehicle power electronics.

- 2020: Significant R&D investments by major players to scale up SiC wafer production capacity.

- 2021: Launch of new SiC-based power modules with improved efficiency and reliability for EVs.

- 2022: Growing adoption of SiC ceramics in aerospace for lightweight and high-temperature resistant components.

- 2023: advancements in CVD silicon carbide technology for wafer handling and processing equipment.

- 2024: Expansion of SiC applications into industrial automation and harsh environment machinery.

Strategic Outlook for Silicon Carbide Ceramics Market

The strategic outlook for the Silicon Carbide ceramics market is exceptionally positive, driven by sustained technological innovation and expanding application horizons. The market is expected to witness continued growth acceleration due to the insatiable demand for high-performance materials in sectors like semiconductors, electric vehicles, and aerospace. Key growth accelerators include further advancements in SiC wafer technology, the development of more cost-effective manufacturing processes, and strategic collaborations aimed at customizing material solutions for specific end-user needs. The increasing emphasis on sustainability and energy efficiency globally will further bolster the demand for SiC ceramics, positioning them as critical enablers of future technological advancements.

Silicon Carbide Ceramics Segmentation

-

1. Application

- 1.1. Machinery Manufacturing

- 1.2. Metallurgical Industry

- 1.3. Chemical Engineering

- 1.4. Aerospace & Defense

- 1.5. Semiconductor

- 1.6. Automobile

- 1.7. Others

-

2. Types

- 2.1. Sintered Silicon Carbide

- 2.2. Reaction Bonded Silicon Carbide

- 2.3. Recrystallized Silicon Carbide

- 2.4. CVD Silicon Carbide

- 2.5. Others

Silicon Carbide Ceramics Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Silicon Carbide Ceramics REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.5% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Silicon Carbide Ceramics Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Machinery Manufacturing

- 5.1.2. Metallurgical Industry

- 5.1.3. Chemical Engineering

- 5.1.4. Aerospace & Defense

- 5.1.5. Semiconductor

- 5.1.6. Automobile

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Sintered Silicon Carbide

- 5.2.2. Reaction Bonded Silicon Carbide

- 5.2.3. Recrystallized Silicon Carbide

- 5.2.4. CVD Silicon Carbide

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Silicon Carbide Ceramics Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Machinery Manufacturing

- 6.1.2. Metallurgical Industry

- 6.1.3. Chemical Engineering

- 6.1.4. Aerospace & Defense

- 6.1.5. Semiconductor

- 6.1.6. Automobile

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Sintered Silicon Carbide

- 6.2.2. Reaction Bonded Silicon Carbide

- 6.2.3. Recrystallized Silicon Carbide

- 6.2.4. CVD Silicon Carbide

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Silicon Carbide Ceramics Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Machinery Manufacturing

- 7.1.2. Metallurgical Industry

- 7.1.3. Chemical Engineering

- 7.1.4. Aerospace & Defense

- 7.1.5. Semiconductor

- 7.1.6. Automobile

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Sintered Silicon Carbide

- 7.2.2. Reaction Bonded Silicon Carbide

- 7.2.3. Recrystallized Silicon Carbide

- 7.2.4. CVD Silicon Carbide

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Silicon Carbide Ceramics Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Machinery Manufacturing

- 8.1.2. Metallurgical Industry

- 8.1.3. Chemical Engineering

- 8.1.4. Aerospace & Defense

- 8.1.5. Semiconductor

- 8.1.6. Automobile

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Sintered Silicon Carbide

- 8.2.2. Reaction Bonded Silicon Carbide

- 8.2.3. Recrystallized Silicon Carbide

- 8.2.4. CVD Silicon Carbide

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Silicon Carbide Ceramics Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Machinery Manufacturing

- 9.1.2. Metallurgical Industry

- 9.1.3. Chemical Engineering

- 9.1.4. Aerospace & Defense

- 9.1.5. Semiconductor

- 9.1.6. Automobile

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Sintered Silicon Carbide

- 9.2.2. Reaction Bonded Silicon Carbide

- 9.2.3. Recrystallized Silicon Carbide

- 9.2.4. CVD Silicon Carbide

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Silicon Carbide Ceramics Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Machinery Manufacturing

- 10.1.2. Metallurgical Industry

- 10.1.3. Chemical Engineering

- 10.1.4. Aerospace & Defense

- 10.1.5. Semiconductor

- 10.1.6. Automobile

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Sintered Silicon Carbide

- 10.2.2. Reaction Bonded Silicon Carbide

- 10.2.3. Recrystallized Silicon Carbide

- 10.2.4. CVD Silicon Carbide

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Saint-Gobain

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 3M

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 IBIDEN

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 CeramTec

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Kyocera

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 CoorsTek

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Morgan Advanced Materials

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Schunk

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Mersen

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 IPS Ceramics

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Ortech

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 ASUZAC

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Fraunhofer IKTS

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Shandong Huamei New Material Technology

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Jinhong New Material

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Sanzer New Materials Technology

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Shantian Abrasive

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 SSACC China

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Zhejiang Dongxin New Material Technology

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Ningbo FLK Technology

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Shaanxi UDC

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 FCT(Tangshan) New Materials

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Joint Power Shanghai Seals

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Luoyang Pengfei Wear Resistant Materials

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Weifang Zhida Special Ceramics

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.1 Saint-Gobain

List of Figures

- Figure 1: Global Silicon Carbide Ceramics Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Silicon Carbide Ceramics Revenue (million), by Application 2024 & 2032

- Figure 3: North America Silicon Carbide Ceramics Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Silicon Carbide Ceramics Revenue (million), by Types 2024 & 2032

- Figure 5: North America Silicon Carbide Ceramics Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Silicon Carbide Ceramics Revenue (million), by Country 2024 & 2032

- Figure 7: North America Silicon Carbide Ceramics Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Silicon Carbide Ceramics Revenue (million), by Application 2024 & 2032

- Figure 9: South America Silicon Carbide Ceramics Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Silicon Carbide Ceramics Revenue (million), by Types 2024 & 2032

- Figure 11: South America Silicon Carbide Ceramics Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Silicon Carbide Ceramics Revenue (million), by Country 2024 & 2032

- Figure 13: South America Silicon Carbide Ceramics Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Silicon Carbide Ceramics Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Silicon Carbide Ceramics Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Silicon Carbide Ceramics Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Silicon Carbide Ceramics Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Silicon Carbide Ceramics Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Silicon Carbide Ceramics Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Silicon Carbide Ceramics Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Silicon Carbide Ceramics Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Silicon Carbide Ceramics Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Silicon Carbide Ceramics Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Silicon Carbide Ceramics Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Silicon Carbide Ceramics Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Silicon Carbide Ceramics Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Silicon Carbide Ceramics Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Silicon Carbide Ceramics Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Silicon Carbide Ceramics Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Silicon Carbide Ceramics Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Silicon Carbide Ceramics Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Silicon Carbide Ceramics Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Silicon Carbide Ceramics Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Silicon Carbide Ceramics Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Silicon Carbide Ceramics Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Silicon Carbide Ceramics Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Silicon Carbide Ceramics Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Silicon Carbide Ceramics Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Silicon Carbide Ceramics Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Silicon Carbide Ceramics Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Silicon Carbide Ceramics Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Silicon Carbide Ceramics Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Silicon Carbide Ceramics Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Silicon Carbide Ceramics Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Silicon Carbide Ceramics Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Silicon Carbide Ceramics Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Silicon Carbide Ceramics Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Silicon Carbide Ceramics Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Silicon Carbide Ceramics Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Silicon Carbide Ceramics Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Silicon Carbide Ceramics Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Silicon Carbide Ceramics?

The projected CAGR is approximately 2.5%.

2. Which companies are prominent players in the Silicon Carbide Ceramics?

Key companies in the market include Saint-Gobain, 3M, IBIDEN, CeramTec, Kyocera, CoorsTek, Morgan Advanced Materials, Schunk, Mersen, IPS Ceramics, Ortech, ASUZAC, Fraunhofer IKTS, Shandong Huamei New Material Technology, Jinhong New Material, Sanzer New Materials Technology, Shantian Abrasive, SSACC China, Zhejiang Dongxin New Material Technology, Ningbo FLK Technology, Shaanxi UDC, FCT(Tangshan) New Materials, Joint Power Shanghai Seals, Luoyang Pengfei Wear Resistant Materials, Weifang Zhida Special Ceramics.

3. What are the main segments of the Silicon Carbide Ceramics?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 780.4 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Silicon Carbide Ceramics," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Silicon Carbide Ceramics report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Silicon Carbide Ceramics?

To stay informed about further developments, trends, and reports in the Silicon Carbide Ceramics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence