Key Insights

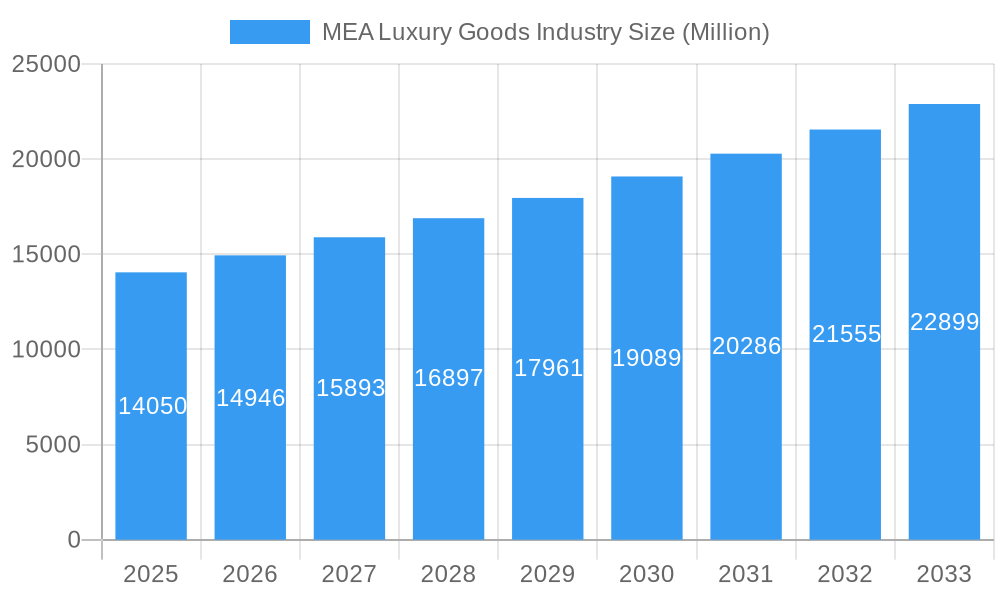

The Middle East and Africa (MEA) luxury goods market, valued at $14.05 billion in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 6.23% from 2025 to 2033. This expansion is fueled by several key factors. A burgeoning affluent population across the region, particularly in the UAE and Saudi Arabia, coupled with increasing disposable incomes and a strong preference for high-end brands, are significant drivers. The rise of e-commerce and the increasing adoption of online luxury retail platforms further contributes to market growth, offering convenience and wider accessibility to luxury goods. Furthermore, strategic brand partnerships, collaborations, and targeted marketing campaigns by luxury brands tailored to the unique preferences of MEA consumers are fostering market expansion. However, economic volatility in certain regions within the MEA and potential global economic downturns represent challenges to consistent market growth.

MEA Luxury Goods Industry Market Size (In Billion)

The market segmentation reveals a diverse landscape. Clothing and apparel dominate the product type segment, followed by footwear, bags, jewelry, and watches. Single-branded stores remain the primary distribution channel, highlighting the importance of brand experience and exclusivity. However, the growing popularity of online retail signifies a shift in consumer behavior, impacting the market share of traditional brick-and-mortar channels. Leading players such as LVMH Moët Hennessy Louis Vuitton, Kering SA, and Richemont, alongside regional players like Alshaya, are intensely competing for market share. This competitive landscape fosters innovation and pushes brands to consistently adapt to the evolving needs and preferences of the luxury consumer within the MEA region. Future growth will likely depend on effectively navigating the evolving economic landscape, leveraging digital channels, and creating personalized brand experiences tailored to the unique cultural contexts within the diverse MEA market.

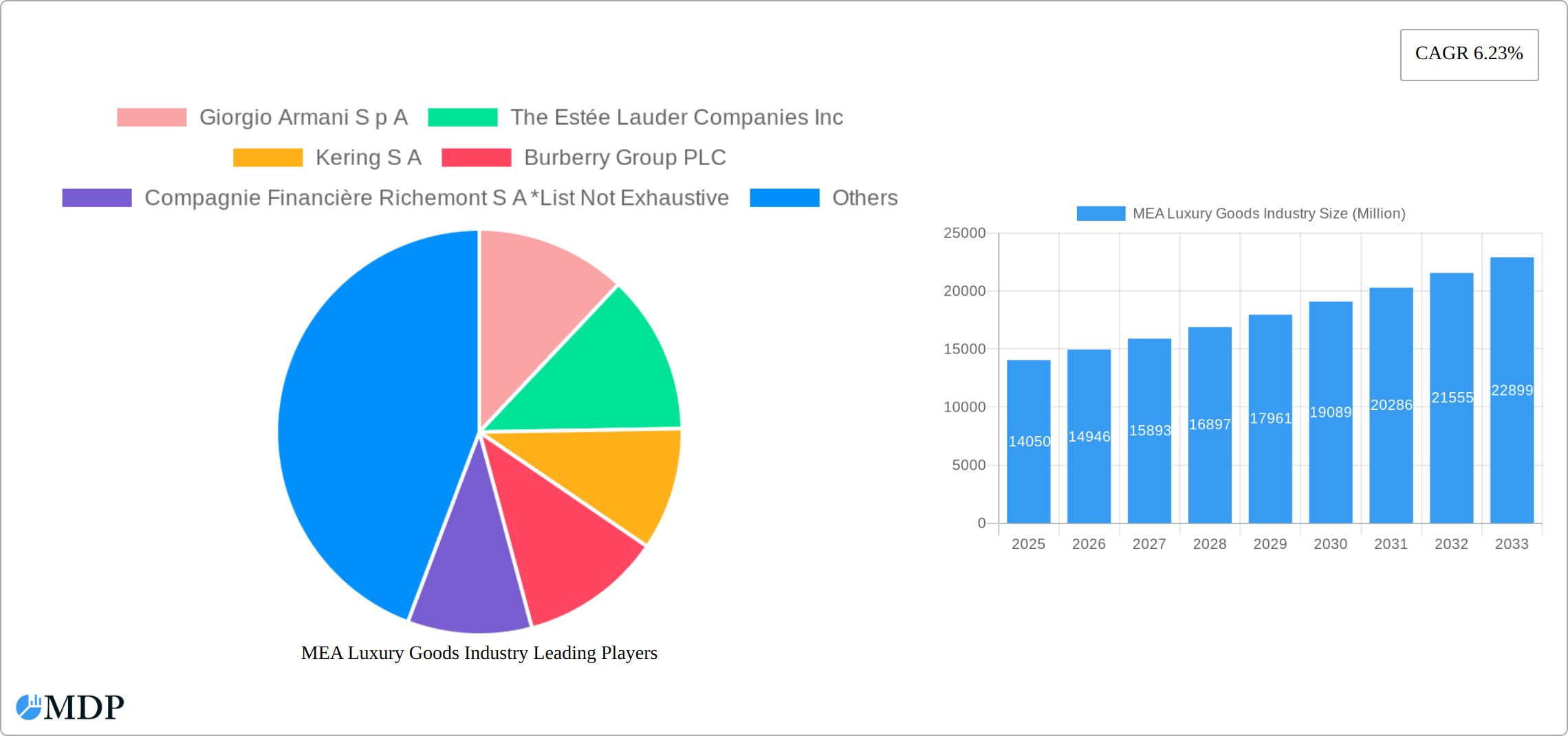

MEA Luxury Goods Industry Company Market Share

MEA Luxury Goods Industry: Market Analysis & Forecast 2019-2033

This comprehensive report provides an in-depth analysis of the Middle East and Africa (MEA) luxury goods industry, offering invaluable insights for stakeholders navigating this dynamic market. With a focus on the period 2019-2033, base year 2025, and forecast period 2025-2033, this report examines market dynamics, leading players, and future growth opportunities. The MEA luxury goods market, valued at $XX Billion in 2024, is projected to reach $XX Billion by 2033, exhibiting a CAGR of XX% during the forecast period. Key players analyzed include Giorgio Armani S p A, The Estée Lauder Companies Inc, Kering S A, Burberry Group PLC, Compagnie Financière Richemont S A, Alshaya franchise group (Tribe of 6 Aerie), Dolce & Gabbana Luxembourg S À R L, Rolex SA, Prada S P A, Roberto Cavalli S P A, Chanel S A, LVMH Moët Hennessy Louis Vuitton, and Chopard Group, though the list is not exhaustive. The report segments the market by product type (Clothing and Apparel, Footwear, Bags, Jewelry, Watches, Other Accessories) and distribution channel (Single-branded Stores, Multi-brand Stores, Online Retail Stores, Other Distribution Channels).

MEA Luxury Goods Industry Market Dynamics & Concentration

The Middle East and Africa (MEA) luxury goods market exhibits a moderately concentrated landscape, dominated by a few key players commanding significant market share. Preliminary 2024 data suggests LVMH Moët Hennessy Louis Vuitton holds approximately [Insert Percentage]%, followed by Kering SA with [Insert Percentage]%, and Richemont with [Insert Percentage]%. However, this established dominance is challenged by a growing number of emerging brands and niche players strategically targeting specific consumer segments with highly curated offerings. Innovation acts as a crucial growth driver, with established luxury houses and newcomers alike continuously introducing novel products, personalized experiences, and leveraging technological advancements to cater to evolving consumer preferences and demands. The regulatory environment, encompassing import duties, taxes, and labeling requirements, significantly influences market dynamics and operational costs, varying considerably across the diverse MEA markets. The presence of both affordable and high-quality product substitutes, especially within apparel and accessories, intensifies competition and necessitates a continuous focus on brand differentiation and value proposition. Crucially, end-user trends, fueled by rising disposable incomes, rapid urbanization, and the expansion of an aspirational middle class, are primary determinants of market demand. The past five years have witnessed [Insert Number] mergers and acquisitions (M&A) deals within the MEA luxury goods sector, primarily focused on expanding market reach, diversifying product portfolios, and securing access to new consumer bases.

- Market Concentration: Moderately concentrated, with the top three players holding approximately [Insert Percentage]% combined market share in 2024.

- Innovation Drivers: New product launches, technological integration in design and manufacturing, personalized customer journeys, and sustainable luxury initiatives.

- Regulatory Framework: Import duties, taxes, and labeling regulations vary significantly across MEA countries, impacting pricing strategies and market access.

- Product Substitutes: The availability of stylish and affordable alternatives exerts competitive pressure, particularly within apparel and accessories segments.

- End-User Trends: Rising disposable incomes, a growing aspirational class, and evolving preferences towards experiences and personalized luxury drive consumption patterns.

- M&A Activity: [Insert Number] M&A deals in the last 5 years reflect strategic expansion and diversification strategies within the industry.

MEA Luxury Goods Industry Industry Trends & Analysis

The MEA luxury goods market is experiencing robust growth, driven by several factors. Rising disposable incomes, particularly in key markets like the UAE and Saudi Arabia, are significantly boosting demand. The increasing influence of social media and digital marketing is also shaping consumer behavior, leading to increased brand awareness and online purchases. Technological disruptions, such as the rise of e-commerce and personalized shopping experiences, are transforming the retail landscape. Consumer preferences are evolving towards sustainable and ethical luxury brands, creating new opportunities for companies committed to responsible practices. Competitive dynamics are intensifying, with established players facing increased competition from both international and regional brands. The market is expected to grow at a CAGR of XX% from 2025 to 2033, with market penetration expected to reach xx% by 2033.

Leading Markets & Segments in MEA Luxury Goods Industry

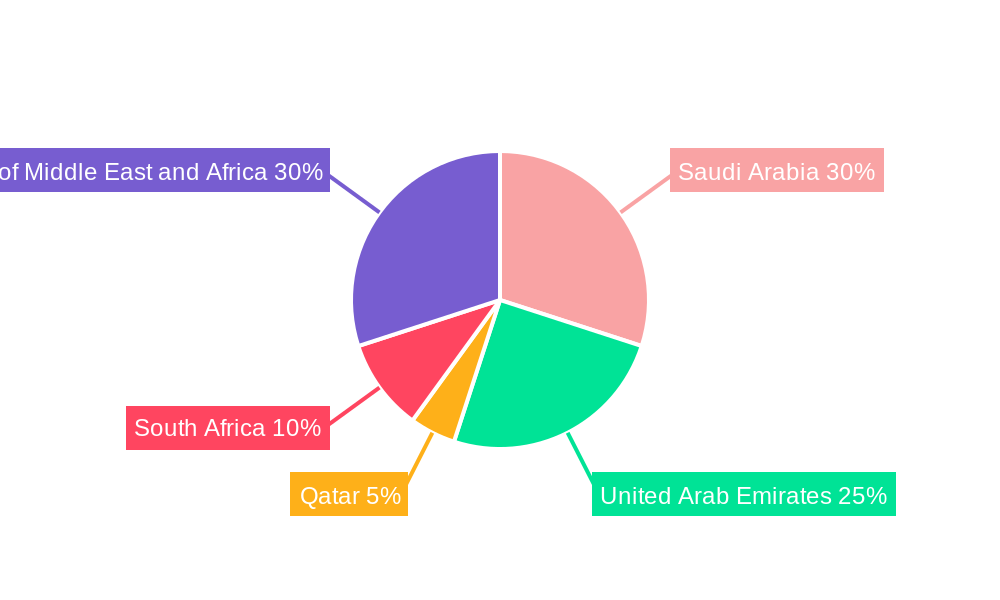

The UAE emerges as the dominant market within the MEA region, driven by its strong economic performance, well-developed retail infrastructure, and high concentration of high-net-worth individuals. Saudi Arabia also holds significant importance, with its growing luxury market propelled by Vision 2030 initiatives. Other key markets include Qatar, Egypt, and South Africa. In terms of product types, watches and jewelry maintain a leading position, followed by bags and apparel. Single-branded stores remain the dominant distribution channel, although online retail is experiencing significant growth.

- Key Drivers for UAE Dominance: Strong economic growth, robust infrastructure, high concentration of affluent consumers, favorable tourism sector.

- Key Drivers for Saudi Arabia Growth: Vision 2030 initiatives, increased tourism, rising disposable incomes among the young population.

- Dominant Product Segments: Watches and Jewelry, Bags, Apparel.

- Dominant Distribution Channels: Single-branded stores, with online retail showing rapid expansion.

MEA Luxury Goods Industry Product Developments

Recent product innovations focus on sustainable materials, personalized customization options, and technological integration. Brands are increasingly leveraging digital technologies to enhance the customer experience, offering virtual try-on features and personalized recommendations. Competitive advantage is achieved through unique design aesthetics, exclusive collaborations, and exceptional craftsmanship. The integration of technology, like NFTs, is also emerging as a trend.

Key Drivers of MEA Luxury Goods Industry Growth

The growth of the MEA luxury goods industry is fueled by several factors:

- Rising Disposable Incomes: A growing middle class with increased spending power is driving demand.

- Tourism: The region's popularity as a tourist destination boosts luxury spending.

- Government Initiatives: Economic diversification policies in various countries stimulate the luxury sector.

- E-commerce Growth: Online platforms expand market reach and accessibility.

Challenges in the MEA Luxury Goods Industry Market

The MEA luxury goods market faces several challenges:

- Economic Volatility: Fluctuations in oil prices and global economic conditions can impact consumer spending.

- Counterfeit Products: The prevalence of counterfeit goods undermines brand value and revenue.

- Supply Chain Disruptions: Global supply chain issues impact product availability and pricing.

- Regulatory Hurdles: Varying regulations across countries create complexities for businesses.

Emerging Opportunities in MEA Luxury Goods Industry

The MEA luxury goods market offers substantial long-term growth potential. The rise of experiential luxury, focusing on unique and personalized services, presents significant opportunities. Strategic partnerships with local businesses can enhance market penetration and brand localization. Expansion into new markets within the MEA region and tapping into the growing demand for sustainable and ethical luxury goods will continue to shape the industry.

Leading Players in the MEA Luxury Goods Industry Sector

- Giorgio Armani S p A

- The Estée Lauder Companies Inc

- Kering S A

- Burberry Group PLC

- Compagnie Financière Richemont S A

- Alshaya franchise group (Tribe of 6 Aerie)

- Dolce & Gabbana Luxembourg S À R L

- Rolex SA

- Prada S P A

- Roberto Cavalli S P A

- Chanel S A

- LVMH Moët Hennessy Louis Vuitton

- Chopard Group

Key Milestones in MEA Luxury Goods Industry Industry

- May 2021: A new Rolex Boutique opened at the Galleria Al Maryah Island in Abu Dhabi, enhancing brand presence and customer experience.

- May 2022: PRADA Tropico launched an exclusive pop-up boutique in Dubai's Mall of Emirates, showcasing innovative retail strategies.

- November 2022: Cartier launched its new Santos de Cartier jewelry collection, introducing innovative designs and expanding product offerings.

Strategic Outlook for MEA Luxury Goods Industry Market

The MEA luxury goods market is poised for continued growth, driven by sustained economic expansion and evolving consumer preferences. Brands that successfully adapt to the changing market dynamics, prioritize personalized experiences, embrace digital technologies, and focus on sustainability will be best positioned to capture significant market share. The focus on creating unique and memorable brand experiences, rather than solely product-centric strategies will be crucial for success.

MEA Luxury Goods Industry Segmentation

-

1. Product Type

- 1.1. Clothing and Apparel

- 1.2. Footwear

- 1.3. Bags

- 1.4. Jewelry

- 1.5. Watches

- 1.6. Other Accessories

-

2. Distribution Channel

- 2.1. Single-branded Stores

- 2.2. Multi-brand Stores

- 2.3. Online Retail Stores

- 2.4. Other Distribution Channels

-

3. Geography

- 3.1. Saudi Arabia

- 3.2. United Arab Emirates

- 3.3. Qatar

- 3.4. South Africa

- 3.5. Rest of Middle East and Africa

MEA Luxury Goods Industry Segmentation By Geography

- 1. Saudi Arabia

- 2. United Arab Emirates

- 3. Qatar

- 4. South Africa

- 5. Rest of Middle East and Africa

MEA Luxury Goods Industry Regional Market Share

Geographic Coverage of MEA Luxury Goods Industry

MEA Luxury Goods Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.23% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Clothing and Apparel

- 5.1.2. Footwear

- 5.1.3. Bags

- 5.1.4. Jewelry

- 5.1.5. Watches

- 5.1.6. Other Accessories

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Single-branded Stores

- 5.2.2. Multi-brand Stores

- 5.2.3. Online Retail Stores

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Saudi Arabia

- 5.3.2. United Arab Emirates

- 5.3.3. Qatar

- 5.3.4. South Africa

- 5.3.5. Rest of Middle East and Africa

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Saudi Arabia

- 5.4.2. United Arab Emirates

- 5.4.3. Qatar

- 5.4.4. South Africa

- 5.4.5. Rest of Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. MEA Luxury Goods Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Clothing and Apparel

- 6.1.2. Footwear

- 6.1.3. Bags

- 6.1.4. Jewelry

- 6.1.5. Watches

- 6.1.6. Other Accessories

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Single-branded Stores

- 6.2.2. Multi-brand Stores

- 6.2.3. Online Retail Stores

- 6.2.4. Other Distribution Channels

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Saudi Arabia

- 6.3.2. United Arab Emirates

- 6.3.3. Qatar

- 6.3.4. South Africa

- 6.3.5. Rest of Middle East and Africa

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Saudi Arabia MEA Luxury Goods Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Clothing and Apparel

- 7.1.2. Footwear

- 7.1.3. Bags

- 7.1.4. Jewelry

- 7.1.5. Watches

- 7.1.6. Other Accessories

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Single-branded Stores

- 7.2.2. Multi-brand Stores

- 7.2.3. Online Retail Stores

- 7.2.4. Other Distribution Channels

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Saudi Arabia

- 7.3.2. United Arab Emirates

- 7.3.3. Qatar

- 7.3.4. South Africa

- 7.3.5. Rest of Middle East and Africa

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. United Arab Emirates MEA Luxury Goods Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Clothing and Apparel

- 8.1.2. Footwear

- 8.1.3. Bags

- 8.1.4. Jewelry

- 8.1.5. Watches

- 8.1.6. Other Accessories

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Single-branded Stores

- 8.2.2. Multi-brand Stores

- 8.2.3. Online Retail Stores

- 8.2.4. Other Distribution Channels

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Saudi Arabia

- 8.3.2. United Arab Emirates

- 8.3.3. Qatar

- 8.3.4. South Africa

- 8.3.5. Rest of Middle East and Africa

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Qatar MEA Luxury Goods Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Clothing and Apparel

- 9.1.2. Footwear

- 9.1.3. Bags

- 9.1.4. Jewelry

- 9.1.5. Watches

- 9.1.6. Other Accessories

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Single-branded Stores

- 9.2.2. Multi-brand Stores

- 9.2.3. Online Retail Stores

- 9.2.4. Other Distribution Channels

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. Saudi Arabia

- 9.3.2. United Arab Emirates

- 9.3.3. Qatar

- 9.3.4. South Africa

- 9.3.5. Rest of Middle East and Africa

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. South Africa MEA Luxury Goods Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Clothing and Apparel

- 10.1.2. Footwear

- 10.1.3. Bags

- 10.1.4. Jewelry

- 10.1.5. Watches

- 10.1.6. Other Accessories

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Single-branded Stores

- 10.2.2. Multi-brand Stores

- 10.2.3. Online Retail Stores

- 10.2.4. Other Distribution Channels

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. Saudi Arabia

- 10.3.2. United Arab Emirates

- 10.3.3. Qatar

- 10.3.4. South Africa

- 10.3.5. Rest of Middle East and Africa

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Rest of Middle East and Africa MEA Luxury Goods Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Clothing and Apparel

- 11.1.2. Footwear

- 11.1.3. Bags

- 11.1.4. Jewelry

- 11.1.5. Watches

- 11.1.6. Other Accessories

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Single-branded Stores

- 11.2.2. Multi-brand Stores

- 11.2.3. Online Retail Stores

- 11.2.4. Other Distribution Channels

- 11.3. Market Analysis, Insights and Forecast - by Geography

- 11.3.1. Saudi Arabia

- 11.3.2. United Arab Emirates

- 11.3.3. Qatar

- 11.3.4. South Africa

- 11.3.5. Rest of Middle East and Africa

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Giorgio Armani S p A

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 The Estée Lauder Companies Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Kering S A

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Burberry Group PLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Compagnie Financière Richemont S A *List Not Exhaustive

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Alshaya franchise group (Tribe of 6 Aerie)

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Dolce & Gabbana Luxembourg S À R L

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Rolex SA

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Prada S P A

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Roberto Cavalli S P A

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Chanel S A

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 LVMH Moët Hennessy Louis Vuitton

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Chopard Group

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Giorgio Armani S p A

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: MEA Luxury Goods Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: MEA Luxury Goods Industry Share (%) by Company 2025

List of Tables

- Table 1: MEA Luxury Goods Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: MEA Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 3: MEA Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 4: MEA Luxury Goods Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: MEA Luxury Goods Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 6: MEA Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 7: MEA Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 8: MEA Luxury Goods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: MEA Luxury Goods Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 10: MEA Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 11: MEA Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 12: MEA Luxury Goods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: MEA Luxury Goods Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 14: MEA Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 15: MEA Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 16: MEA Luxury Goods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: MEA Luxury Goods Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 18: MEA Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 19: MEA Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 20: MEA Luxury Goods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: MEA Luxury Goods Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 22: MEA Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 23: MEA Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 24: MEA Luxury Goods Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the MEA Luxury Goods Industry?

The projected CAGR is approximately 6.23%.

2. Which companies are prominent players in the MEA Luxury Goods Industry?

Key companies in the market include Giorgio Armani S p A, The Estée Lauder Companies Inc, Kering S A, Burberry Group PLC, Compagnie Financière Richemont S A *List Not Exhaustive, Alshaya franchise group (Tribe of 6 Aerie), Dolce & Gabbana Luxembourg S À R L, Rolex SA, Prada S P A, Roberto Cavalli S P A, Chanel S A, LVMH Moët Hennessy Louis Vuitton, Chopard Group.

3. What are the main segments of the MEA Luxury Goods Industry?

The market segments include Product Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.05 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in Tourism Expected to Drive the Market; Robust Luxury Market Infrastructure.

6. What are the notable trends driving market growth?

Rise in Tourism Expected to Drive the Market.

7. Are there any restraints impacting market growth?

Counterfeit Goods Restricting the Market Growth.

8. Can you provide examples of recent developments in the market?

November 2022: Santos de Cartier launched new series of jewelry collections that consists of rings, bracelets, and necklaces. The collection consists of a gold chain in two colors, mounted with a single or double row of coffee beans decorated with diamonds of various sizes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "MEA Luxury Goods Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the MEA Luxury Goods Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the MEA Luxury Goods Industry?

To stay informed about further developments, trends, and reports in the MEA Luxury Goods Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence