Key Insights

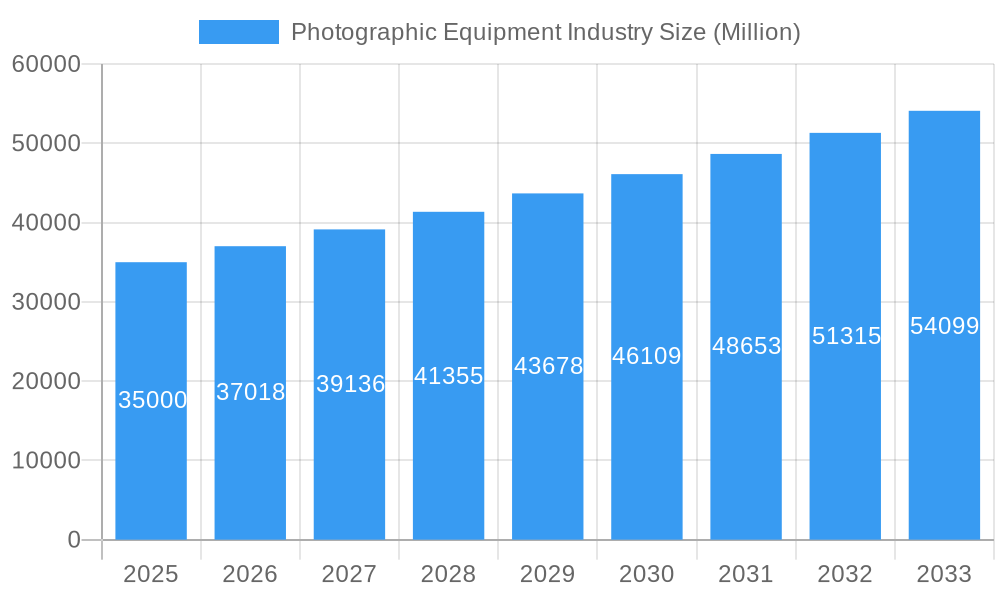

The global photographic equipment market is projected to experience significant expansion, reaching an estimated market size of USD 6.5 billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of 7.1% through 2033. This robust growth is propelled by escalating consumer demand for premium imaging solutions, rapid technological advancements, and the enduring human desire to document and share experiences. The industry is characterized by continuous innovation, with manufacturers actively developing advanced cameras and lenses for both professionals and enthusiasts. Key technological drivers include the rising adoption of mirrorless cameras, the increasing prevalence of high-resolution sensors, and sophisticated autofocus systems. The proliferation of content creation platforms and social media further fuels demand for professional-grade equipment.

Photographic Equipment Industry Market Size (In Billion)

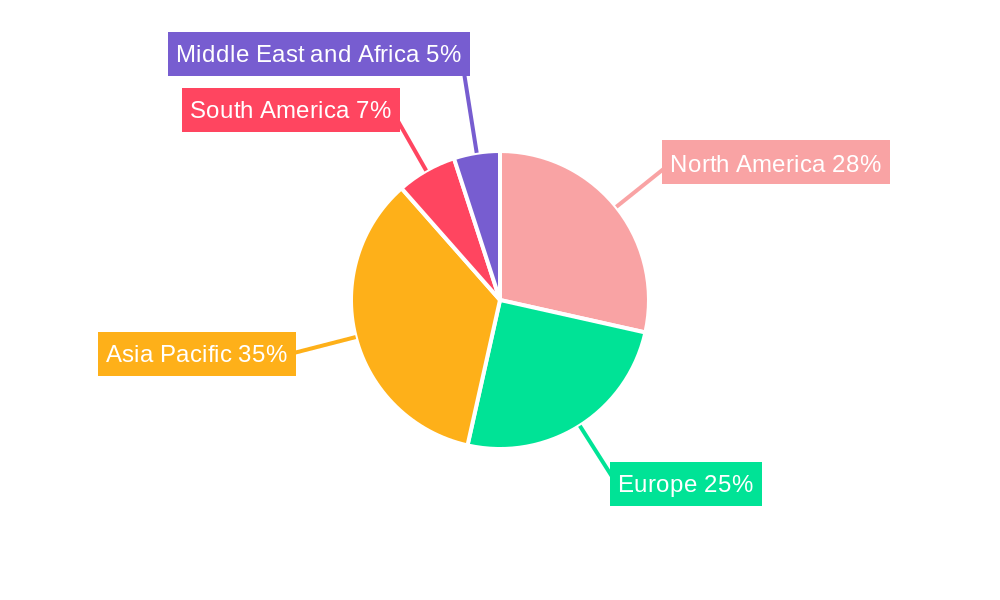

The market's segmentation reveals a diverse landscape. While cameras and lenses are primary categories, the "Others" segment, comprising accessories, lighting, and imaging software, is also growing as users seek integrated solutions. Both online and offline retail channels are vital, offering convenience and wider selection online, and hands-on experience in physical stores. Geographically, the Asia Pacific region, led by China and India, is anticipated to be a major growth driver due to its large population, rising disposable incomes, and a burgeoning digital photography culture. North America and Europe remain critical, mature markets supported by established professional photography sectors and a strong consumer base for advanced imaging technology. Leading companies such as Canon, Nikon, and Sony are instrumental in shaping the market through ongoing product development and strategic initiatives.

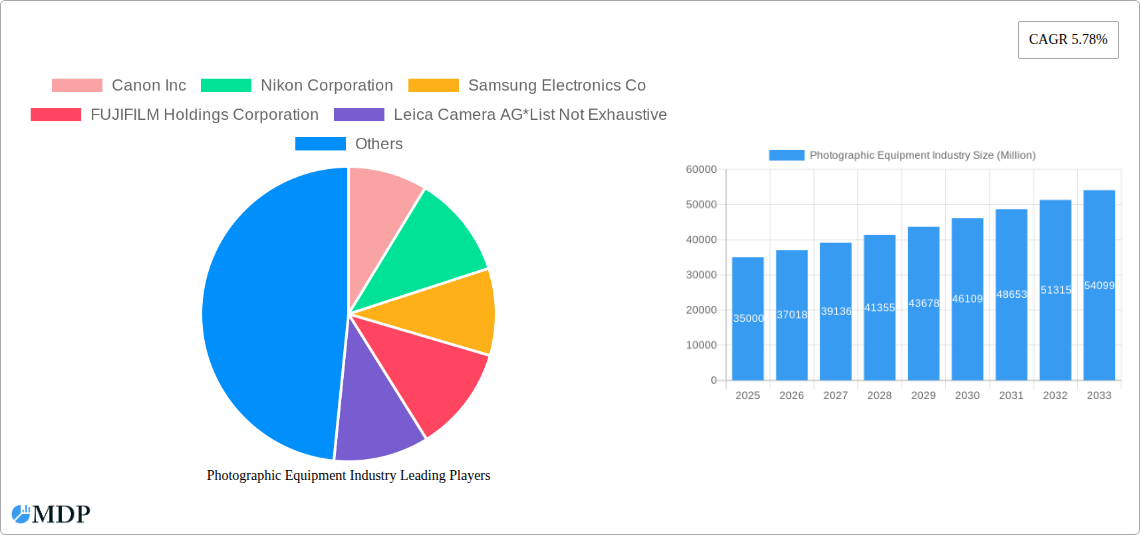

Photographic Equipment Industry Company Market Share

Unveiling the Future of Visual Storytelling: Photographic Equipment Industry Market Report (2019-2033)

This comprehensive report delves into the dynamic and rapidly evolving photographic equipment industry, offering unparalleled insights for stakeholders aiming to navigate its complexities and capitalize on emerging opportunities. From high-end professional cameras and lenses to consumer-grade devices, this analysis provides a deep dive into market dynamics, key trends, leading segments, and strategic outlooks, supported by robust data and expert analysis.

Photographic Equipment Industry Market Dynamics & Concentration

The photographic equipment industry exhibits a moderate market concentration, with a few dominant players holding significant market share. Canon Inc. and Nikon Corporation, stalwarts in the DSLR and mirrorless camera segments, collectively command an estimated 45% market share. Sony Corporation, with its strong presence in mirrorless technology and sensor manufacturing, holds a substantial 20% market share. FUJIFILM Holdings Corporation is a key player, particularly in the mirrorless and instant camera segments, with an estimated 12% market share. Samsung Electronics Co. maintains a presence, especially in the smartphone camera component market, contributing approximately 8%. Leica Camera AG, though a niche player, commands a premium segment with an estimated 5% market share in high-end cameras. Panasonic Corporation also contributes to the market, particularly with its Lumix line, holding an estimated 7% market share. The remaining market share is fragmented among smaller players and specialized manufacturers.

Innovation remains the primary driver of market growth, fueled by advancements in sensor technology, artificial intelligence for image processing, and miniaturization of components. Regulatory frameworks, while generally favorable, can impact import/export duties and environmental standards for manufacturing. Product substitutes, primarily advanced smartphone cameras, continue to pose a challenge, particularly in the entry-level and mid-range segments, though professional and enthusiast markets remain resilient. End-user trends indicate a growing demand for mirrorless cameras, compact yet powerful lenses, and integrated imaging solutions. Merger and acquisition activities have been relatively modest in recent years, with a few strategic acquisitions focused on technology integration, such as acquisitions in the AI imaging or drone photography space. The number of M&A deals over the study period is estimated to be around 20-30, with transaction values varying significantly based on the target company's IP and market position.

Photographic Equipment Industry Industry Trends & Analysis

The photographic equipment industry is poised for sustained growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 5.5% during the forecast period of 2025–2033. This growth is primarily propelled by a confluence of technological advancements, shifting consumer preferences, and expanding application areas. The increasing adoption of mirrorless camera technology, offering superior image quality, faster autofocus, and greater flexibility compared to traditional DSLRs, is a significant market driver. Innovations in sensor technology, including larger pixel counts, enhanced low-light performance, and improved dynamic range, continue to elevate image capture capabilities, appealing to both professional photographers and advanced hobbyists. The integration of artificial intelligence (AI) and machine learning (ML) in camera firmware and software is revolutionizing image processing, offering intelligent scene recognition, automatic image optimization, and advanced editing features, making professional-quality results more accessible to a broader audience.

The proliferation of content creation platforms, such as YouTube, Instagram, and TikTok, has fueled a demand for high-quality imaging equipment among influencers, vloggers, and aspiring content creators. This demographic seeks portable, versatile, and feature-rich cameras that can produce professional-looking videos and stills. Furthermore, the burgeoning demand for visual content in sectors like e-commerce, real estate, and tourism necessitates advanced photographic tools. The market penetration of high-resolution cameras and advanced lens systems is expected to deepen as these industries recognize the impact of compelling visuals on customer engagement and sales.

Competitive dynamics are characterized by intense innovation and product differentiation. Leading companies are investing heavily in research and development to introduce next-generation cameras and lenses that push the boundaries of imaging technology. This includes advancements in computational photography, faster processing speeds, enhanced video recording capabilities (e.g., 8K resolution, higher frame rates), and improved connectivity features for seamless sharing and remote operation. The shift towards mirrorless systems has intensified competition among established players and has also opened avenues for new entrants with innovative technologies. The offline retail segment, while still significant for hands-on product evaluation and expert advice, is increasingly complemented by robust online sales channels, offering wider product selections and competitive pricing. The market penetration of advanced imaging solutions is estimated to reach 70% by 2033, up from approximately 55% in the base year of 2025.

Leading Markets & Segments in Photographic Equipment Industry

The Asia-Pacific region is projected to be the dominant market for photographic equipment, driven by its vast population, rapidly growing middle class, and increasing disposable incomes, particularly in countries like China, India, and South Korea. Economic policies that support manufacturing and innovation, coupled with robust infrastructure development, further bolster the region's lead. Within this region, China stands out as a leading country due to its massive consumer base, thriving e-commerce ecosystem, and a strong appetite for new technology. The country's burgeoning content creation scene and the increasing adoption of professional photography by small and medium-sized enterprises contribute significantly to this dominance.

In terms of Product Type, the Camera segment is expected to maintain its leading position, driven by continuous innovation in mirrorless technology and the demand for advanced features for both professional and enthusiast users. The Lens segment, closely following the camera market, is also experiencing robust growth as photographers increasingly invest in specialized lenses to achieve specific creative effects and enhance image quality. The "Others" category, encompassing accessories, lighting equipment, and imaging software, will see steady growth, driven by the need for a comprehensive photographic workflow.

The Online Retail distribution channel is projected to witness the fastest growth and capture a larger market share. This is attributed to the convenience of online shopping, competitive pricing, wider product availability, and the ease of accessing product reviews and comparisons. E-commerce platforms have become crucial touchpoints for consumers to research, compare, and purchase photographic equipment. Key drivers for the dominance of online retail include the widespread adoption of smartphones for online browsing and purchasing, efficient logistics and delivery networks, and the increasing trust consumers place in online marketplaces. While the Offline Retail segment will continue to be important for experiential purchasing, product demonstrations, and personalized customer service, its market share will gradually be influenced by the expanding reach and convenience of online platforms. The market share of online retail is estimated to grow from approximately 58% in 2025 to 70% by 2033, while offline retail will see a corresponding decline from 42% to 30%.

Photographic Equipment Industry Product Developments

Product developments in the photographic equipment industry are characterized by a relentless pursuit of technological excellence and enhanced user experience. Key innovations include the widespread adoption of advanced AI-powered image processing, enabling superior low-light performance and intelligent subject tracking. Mirrorless camera technology continues to evolve, offering smaller form factors, faster burst shooting rates, and improved in-body image stabilization. The development of high-resolution sensors and sophisticated lens coatings contributes to exceptional image clarity and color accuracy. Furthermore, the integration of advanced video capabilities, such as 8K recording and professional-grade codecs, is expanding the utility of photographic equipment for videographers and content creators. These advancements provide competitive advantages by meeting the growing demand for professional-quality visuals across various applications, from artistic photography to commercial content creation.

Key Drivers of Photographic Equipment Industry Growth

The photographic equipment industry's growth is propelled by several key factors. Technological Advancements are paramount, with continuous innovation in sensor technology, artificial intelligence for image processing, and mirrorless camera systems driving demand. The Exponential Growth of Content Creation across social media platforms and professional multimedia sectors fuels the need for high-quality imaging tools. Rising Disposable Incomes in emerging economies translate to increased consumer spending on premium photographic equipment. The Expanding Application of Visuals in industries like e-commerce, real estate, and tourism necessitates advanced photographic solutions. Finally, Government Initiatives supporting technological innovation and digital infrastructure development indirectly contribute to market expansion by fostering a conducive environment for businesses.

Challenges in the Photographic Equipment Industry Market

Despite its robust growth, the photographic equipment industry faces several challenges. Intense Competition from Smartphone Cameras continues to be a significant restraint, particularly in the entry-level and mid-range segments, as smartphone camera quality rapidly improves. Supply Chain Disruptions, exacerbated by global geopolitical events and manufacturing complexities, can lead to production delays and increased costs. The High Cost of Advanced Equipment can be a barrier for aspiring professionals and hobbyists, limiting market penetration in price-sensitive regions. Rapid Technological Obsolescence requires continuous investment in R&D and marketing to stay competitive, putting pressure on profit margins. The estimated impact of smartphone competition on the interchangeable lens camera market is a reduction of 15-20% in potential unit sales over the forecast period.

Emerging Opportunities in Photographic Equipment Industry

Catalysts driving long-term growth in the photographic equipment industry are numerous. The continued evolution and adoption of AI in image processing present opportunities for enhanced creative tools and automated workflows. The growing demand for specialized imaging solutions in niche markets such as astrophotography, wildlife photography, and industrial inspection opens new avenues for product development and market expansion. Strategic partnerships between camera manufacturers and software developers for integrated editing and sharing platforms can create seamless user experiences. Furthermore, the exploration of augmented reality (AR) and virtual reality (VR) integration within camera functionalities and viewing platforms could unlock novel applications and consumer engagement models, offering a projected market potential of over $5 Billion by 2033.

Leading Players in the Photographic Equipment Industry Sector

- Canon Inc.

- Nikon Corporation

- Samsung Electronics Co.

- FUJIFILM Holdings Corporation

- Leica Camera AG

- Panasonic Corporation

- Sony Corporation

Key Milestones in Photographic Equipment Industry Industry

- 2019: Introduction of advanced AI-powered autofocus systems in mirrorless cameras, significantly improving subject tracking capabilities.

- 2020: Launch of high-resolution 8K video recording capabilities in professional-grade mirrorless cameras, catering to the growing demand for ultra-high-definition content.

- 2021: Increased market penetration of computational photography features in both dedicated cameras and smartphone-integrated imaging solutions.

- 2022: Significant advancements in in-body image stabilization (IBIS) technology, enabling sharper handheld shots in challenging lighting conditions.

- 2023: Growing interest and development in drone photography and videography, integrating advanced camera technologies into aerial platforms.

- 2024: Focus on sustainable manufacturing practices and eco-friendly product designs within the photographic equipment industry.

Strategic Outlook for Photographic Equipment Industry Market

The strategic outlook for the photographic equipment industry is overwhelmingly positive, driven by ongoing technological innovation and expanding market applications. The industry's future growth will be accelerated by the continued refinement of AI in image capture and processing, leading to more intelligent and user-friendly devices. The expansion of mirrorless technology and the development of versatile, high-performance lenses will remain central to product strategies. Furthermore, tapping into emerging markets and catering to the evolving needs of content creators and specialized professional segments will be crucial for sustained success. Embracing digitalization in distribution and customer engagement, alongside strategic collaborations to enhance the overall imaging ecosystem, will position key players for continued market leadership and profitability. The projected market potential for new imaging applications is estimated to exceed $10 Billion by 2033, presenting a significant opportunity for forward-thinking companies.

Photographic Equipment Industry Segmentation

-

1. Product Type

- 1.1. Camera

- 1.2. Lens

- 1.3. Others

-

2. Distribution Channel

- 2.1. Online Retail

- 2.2. Offline Retail

Photographic Equipment Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Italy

- 2.5. Russia

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. Saudi Arabia

- 5.3. Rest of Middle East and Africa

Photographic Equipment Industry Regional Market Share

Geographic Coverage of Photographic Equipment Industry

Photographic Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Camera

- 5.1.2. Lens

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Online Retail

- 5.2.2. Offline Retail

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Photographic Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Camera

- 6.1.2. Lens

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Online Retail

- 6.2.2. Offline Retail

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Photographic Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Camera

- 7.1.2. Lens

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Online Retail

- 7.2.2. Offline Retail

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Photographic Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Camera

- 8.1.2. Lens

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Online Retail

- 8.2.2. Offline Retail

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Pacific Photographic Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Camera

- 9.1.2. Lens

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Online Retail

- 9.2.2. Offline Retail

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. South America Photographic Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Camera

- 10.1.2. Lens

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Online Retail

- 10.2.2. Offline Retail

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Middle East and Africa Photographic Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Camera

- 11.1.2. Lens

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Online Retail

- 11.2.2. Offline Retail

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Canon Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Nikon Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Samsung Electronics Co

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 FUJIFILM Holdings Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Leica Camera AG*List Not Exhaustive

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Panasonic Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Sony Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 Canon Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Photographic Equipment Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Photographic Equipment Industry Volume Breakdown (K Units, %) by Region 2025 & 2033

- Figure 3: North America Photographic Equipment Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 4: North America Photographic Equipment Industry Volume (K Units), by Product Type 2025 & 2033

- Figure 5: North America Photographic Equipment Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Photographic Equipment Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 7: North America Photographic Equipment Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 8: North America Photographic Equipment Industry Volume (K Units), by Distribution Channel 2025 & 2033

- Figure 9: North America Photographic Equipment Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 10: North America Photographic Equipment Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 11: North America Photographic Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Photographic Equipment Industry Volume (K Units), by Country 2025 & 2033

- Figure 13: North America Photographic Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Photographic Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Photographic Equipment Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 16: Europe Photographic Equipment Industry Volume (K Units), by Product Type 2025 & 2033

- Figure 17: Europe Photographic Equipment Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 18: Europe Photographic Equipment Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 19: Europe Photographic Equipment Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 20: Europe Photographic Equipment Industry Volume (K Units), by Distribution Channel 2025 & 2033

- Figure 21: Europe Photographic Equipment Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 22: Europe Photographic Equipment Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 23: Europe Photographic Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: Europe Photographic Equipment Industry Volume (K Units), by Country 2025 & 2033

- Figure 25: Europe Photographic Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Photographic Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Photographic Equipment Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 28: Asia Pacific Photographic Equipment Industry Volume (K Units), by Product Type 2025 & 2033

- Figure 29: Asia Pacific Photographic Equipment Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 30: Asia Pacific Photographic Equipment Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 31: Asia Pacific Photographic Equipment Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 32: Asia Pacific Photographic Equipment Industry Volume (K Units), by Distribution Channel 2025 & 2033

- Figure 33: Asia Pacific Photographic Equipment Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 34: Asia Pacific Photographic Equipment Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 35: Asia Pacific Photographic Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 36: Asia Pacific Photographic Equipment Industry Volume (K Units), by Country 2025 & 2033

- Figure 37: Asia Pacific Photographic Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Photographic Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: South America Photographic Equipment Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 40: South America Photographic Equipment Industry Volume (K Units), by Product Type 2025 & 2033

- Figure 41: South America Photographic Equipment Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 42: South America Photographic Equipment Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 43: South America Photographic Equipment Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 44: South America Photographic Equipment Industry Volume (K Units), by Distribution Channel 2025 & 2033

- Figure 45: South America Photographic Equipment Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 46: South America Photographic Equipment Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 47: South America Photographic Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: South America Photographic Equipment Industry Volume (K Units), by Country 2025 & 2033

- Figure 49: South America Photographic Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: South America Photographic Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Photographic Equipment Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 52: Middle East and Africa Photographic Equipment Industry Volume (K Units), by Product Type 2025 & 2033

- Figure 53: Middle East and Africa Photographic Equipment Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 54: Middle East and Africa Photographic Equipment Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 55: Middle East and Africa Photographic Equipment Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 56: Middle East and Africa Photographic Equipment Industry Volume (K Units), by Distribution Channel 2025 & 2033

- Figure 57: Middle East and Africa Photographic Equipment Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 58: Middle East and Africa Photographic Equipment Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 59: Middle East and Africa Photographic Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 60: Middle East and Africa Photographic Equipment Industry Volume (K Units), by Country 2025 & 2033

- Figure 61: Middle East and Africa Photographic Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Middle East and Africa Photographic Equipment Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Photographic Equipment Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Global Photographic Equipment Industry Volume K Units Forecast, by Product Type 2020 & 2033

- Table 3: Global Photographic Equipment Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: Global Photographic Equipment Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 5: Global Photographic Equipment Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Photographic Equipment Industry Volume K Units Forecast, by Region 2020 & 2033

- Table 7: Global Photographic Equipment Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Global Photographic Equipment Industry Volume K Units Forecast, by Product Type 2020 & 2033

- Table 9: Global Photographic Equipment Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 10: Global Photographic Equipment Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 11: Global Photographic Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Photographic Equipment Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 13: United States Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 15: Canada Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 17: Mexico Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 19: Rest of North America Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Rest of North America Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 21: Global Photographic Equipment Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 22: Global Photographic Equipment Industry Volume K Units Forecast, by Product Type 2020 & 2033

- Table 23: Global Photographic Equipment Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 24: Global Photographic Equipment Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 25: Global Photographic Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Global Photographic Equipment Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 27: United Kingdom Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: United Kingdom Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 29: Germany Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Germany Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 31: France Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: France Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 33: Italy Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Italy Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 35: Russia Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Russia Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 37: Rest of Europe Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Rest of Europe Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 39: Global Photographic Equipment Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 40: Global Photographic Equipment Industry Volume K Units Forecast, by Product Type 2020 & 2033

- Table 41: Global Photographic Equipment Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 42: Global Photographic Equipment Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 43: Global Photographic Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 44: Global Photographic Equipment Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 45: China Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: China Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 47: Japan Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Japan Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 49: India Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: India Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 51: Australia Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Australia Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 53: Rest of Asia Pacific Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Asia Pacific Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 55: Global Photographic Equipment Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 56: Global Photographic Equipment Industry Volume K Units Forecast, by Product Type 2020 & 2033

- Table 57: Global Photographic Equipment Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 58: Global Photographic Equipment Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 59: Global Photographic Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Photographic Equipment Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 61: Brazil Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Brazil Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 63: Argentina Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Argentina Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 65: Rest of South America Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: Rest of South America Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 67: Global Photographic Equipment Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 68: Global Photographic Equipment Industry Volume K Units Forecast, by Product Type 2020 & 2033

- Table 69: Global Photographic Equipment Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 70: Global Photographic Equipment Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 71: Global Photographic Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 72: Global Photographic Equipment Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 73: South Africa Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 74: South Africa Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 75: Saudi Arabia Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 76: Saudi Arabia Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 77: Rest of Middle East and Africa Photographic Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 78: Rest of Middle East and Africa Photographic Equipment Industry Volume (K Units) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Photographic Equipment Industry?

The projected CAGR is approximately 7.1%.

2. Which companies are prominent players in the Photographic Equipment Industry?

Key companies in the market include Canon Inc, Nikon Corporation, Samsung Electronics Co, FUJIFILM Holdings Corporation, Leica Camera AG*List Not Exhaustive, Panasonic Corporation, Sony Corporation.

3. What are the main segments of the Photographic Equipment Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Fast Fashion Trend; Inflating Income Level of Individuals.

6. What are the notable trends driving market growth?

Increasing sale of Photography Equipment’s from Online Retailing Channels.

7. Are there any restraints impacting market growth?

The Presence Of Counterfeit Products.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Photographic Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Photographic Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Photographic Equipment Industry?

To stay informed about further developments, trends, and reports in the Photographic Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence