Key Insights

The US luxury market is poised for significant expansion, projected to reach a substantial $274.8 billion by 2025, demonstrating a robust compound annual growth rate (CAGR) of 5.8% through 2033. This impressive trajectory is fueled by a confluence of powerful drivers, including the increasing disposable income of affluent consumers, a growing appetite for unique and personalized luxury experiences, and the aspirational pull of established and emerging luxury brands. The rise of conscious consumerism is also playing a pivotal role, with buyers increasingly seeking ethically sourced and sustainable luxury goods, prompting brands to re-evaluate their production and supply chains. Furthermore, the digital transformation continues to reshape the landscape, with online channels becoming increasingly critical for both discovery and purchase, offering unparalleled convenience and access to a global clientele. This dynamic environment creates fertile ground for innovation and strategic growth within the US luxury sector.

US Luxury Market Market Size (In Billion)

The US luxury market's segmentation reveals a diverse and evolving consumer base. Clothing and apparel, along with footwear, represent core pillars, but significant growth is anticipated in luxury bags, jewelry, and watches, reflecting a desire for statement pieces and enduring investments. The "Other Accessories" segment, encompassing everything from high-end tech gadgets to bespoke home decor, is also showing considerable promise as consumers seek to integrate luxury into all facets of their lives. Distribution channels are similarly multifaceted, with single-brand stores maintaining their exclusivity, multi-brand retailers offering curated selections, and online stores experiencing exponential growth due to their accessibility and targeted marketing capabilities. Leading companies such as LVMH Moët Hennessy Louis Vuitton, Kering, and The Swatch Group are actively navigating these trends, investing in digital infrastructure, sustainable practices, and innovative product development to capture market share. The market's resilience is further underscored by its broad regional penetration across North America, with the United States leading the charge, and a growing influence in other global regions.

US Luxury Market Company Market Share

US Luxury Market: Unveiling Billion-Dollar Trends and Elite Consumer Shifts (2019-2033)

Discover the opulent future of the US luxury market, a dynamic landscape projected to reach multi-billion dollar valuations by 2025. This comprehensive report, spanning from 2019 to 2033, dissects the forces shaping the high-end consumer goods sector, from iconic brands like LVMH Moët Hennessy Louis Vuitton and Kering to emerging digital strategies and evolving consumer desires. Gain unparalleled insights into market dynamics, industry trends, leading segments, and strategic opportunities within this thriving billion-dollar industry. Perfect for investors, brand strategists, and industry stakeholders seeking to navigate the pinnacle of American commerce.

US Luxury Market Market Dynamics & Concentration

The US luxury market is characterized by a sophisticated interplay of high brand equity and intense competition, with market concentration varying across its diverse segments. Dominant players like LVMH Moët Hennessy Louis Vuitton, Compagnie Financière Richemont S.A., and Kering command significant market share, particularly in high-value categories such as leather goods and high fashion. Innovation drivers are propelled by a relentless pursuit of exclusivity, artisanal craftsmanship, and sustainable practices, often spurred by advancements in material science and digital integration. Regulatory frameworks, while generally favorable, focus on intellectual property protection and ethical sourcing, ensuring the integrity of luxury goods. Product substitutes, while not direct competitors in terms of inherent value, emerge from the broader consumer goods market offering aspirational alternatives. End-user trends reveal a growing demand for personalized experiences, provenance, and a conscious shift towards brands that align with personal values, including sustainability and social responsibility. Mergers and acquisitions (M&A) activities are pivotal in consolidating market positions and expanding portfolios, with deal counts often reflecting strategic acquisitions of niche brands or innovative technology providers to enhance omnichannel capabilities. The market's inherent barriers to entry, including brand building costs and established distribution networks, contribute to its concentrated nature.

US Luxury Market Industry Trends & Analysis

The US luxury market is experiencing robust growth, fueled by a confluence of economic prosperity, evolving consumer preferences, and technological advancements. The projected CAGR indicates a sustained upward trajectory, with market penetration deepening as more affluent consumers engage with high-end offerings. Key growth drivers include a burgeoning high-net-worth individual population and a desire for tangible assets that retain or appreciate in value. The historical period (2019-2024) witnessed a significant acceleration in digital adoption, with luxury brands increasingly investing in sophisticated e-commerce platforms and augmented reality (AR) experiences to enhance online shopping. Technological disruptions are not limited to digital interfaces; advancements in sustainable material innovation and bespoke manufacturing processes are redefining product creation and consumer engagement. Consumer preferences are shifting beyond mere brand name to encompass ethical production, unique storytelling, and personalized luxury. This necessitates a hyper-personalized approach to marketing and product development. Competitive dynamics are intensifying, with established behemoths fiercely defending their turf while nimble digital-native luxury brands emerge, challenging traditional retail models. The estimated market value in 2025 underscores the market's resilience and its capacity to adapt to changing economic conditions. The forecast period (2025-2033) anticipates further integration of AI-driven personalization, immersive virtual shopping environments, and a continued emphasis on sustainability as a core brand pillar, driving demand for responsibly sourced and crafted luxury goods.

Leading Markets & Segments in US Luxury Market

The US luxury market's dominance is firmly established within the Clothing and Apparel segment, driven by aspirational fashion trends and the influence of globally recognized designers. This segment, encompassing ready-to-wear, haute couture, and custom garments, consistently attracts substantial consumer spending, reflecting its cultural significance and the desire for self-expression through high-end fashion. Closely following are Bags and Footwear, categories where iconic branding and craftsmanship command premium prices. The Jewelry and Watches segments also represent substantial pillars, characterized by high unit values and a strong emphasis on heritage, precious materials, and intricate artistry.

Distribution Channels play a crucial role in segment performance. Single-brand Stores remain a cornerstone, offering an immersive brand experience and direct control over customer interactions. These flagship locations are essential for reinforcing brand identity and exclusivity. Online Stores have experienced exponential growth, particularly post-pandemic, with luxury brands leveraging sophisticated e-commerce platforms to reach a wider audience and offer personalized digital journeys. The convenience and accessibility of online purchasing have made it a critical component of the luxury retail ecosystem. Multi-brand Stores, while still relevant, are evolving to offer curated selections and exclusive in-store experiences. Other Distribution Channels, including private sales, direct-to-consumer pop-ups, and partnerships with luxury travel and hospitality sectors, are gaining traction as brands seek innovative ways to connect with discerning clientele and create unique consumption moments.

Key drivers for the dominance of these segments include:

- Economic Policies: Favorable tax policies and economic growth in the US bolster disposable income for luxury purchases.

- Infrastructure: Robust retail infrastructure, including prime real estate for flagship stores and advanced logistics for online fulfillment, supports segment growth.

- Consumer Confidence: High levels of consumer confidence directly translate into increased spending on discretionary luxury items.

- Brand Heritage and Storytelling: Iconic brands in clothing, jewelry, and watches benefit from decades of heritage and compelling narratives that resonate deeply with luxury consumers.

- Technological Integration: The successful adoption of digital technologies, from AI-powered recommendations to virtual try-on experiences, significantly boosts online sales across all segments.

US Luxury Market Product Developments

Product developments in the US luxury market are heavily influenced by technological innovation and a heightened consumer demand for sustainability and personalization. Brands are increasingly exploring advanced materials, such as recycled and bio-based fabrics in Clothing and Apparel, and ethically sourced gemstones and lab-grown diamonds in Jewelry. In Watches, miniaturization and smart functionalities are being integrated without compromising traditional craftsmanship. Bags and Other Accessories are seeing innovations in material durability and unique design elements that cater to evolving lifestyle needs. The competitive advantage lies in brands that can seamlessly blend artisanal quality with cutting-edge technology and responsible sourcing, offering products that are not only aesthetically superior but also ethically produced and digitally connected.

Key Drivers of US Luxury Market Growth

The US luxury market's growth is propelled by several interconnected factors. A robust and expanding affluent consumer base, characterized by high disposable income, forms the bedrock of demand. Technological advancements, including AI-driven personalization, virtual reality shopping experiences, and blockchain for authenticity verification, are enhancing consumer engagement and accessibility. Favorable economic conditions, such as steady GDP growth and supportive fiscal policies, contribute to increased consumer confidence and spending power. Furthermore, a growing emphasis on sustainable and ethical practices by brands is resonating with conscious consumers, creating a powerful market differentiator and driving demand for responsibly manufactured luxury goods. The increasing popularity of experiences over material possessions is also influencing growth, with luxury brands expanding into travel, dining, and exclusive events.

Challenges in the US Luxury Market Market

Despite its upward trajectory, the US luxury market faces significant challenges. Intense competition from both established global players and emerging direct-to-consumer brands necessitates continuous innovation and strategic differentiation. Regulatory hurdles, particularly concerning intellectual property protection against counterfeit goods and increasing scrutiny over supply chain transparency and ethical sourcing, require significant compliance efforts. Supply chain disruptions, exacerbated by global events, can impact production timelines and material availability, leading to potential revenue losses. Furthermore, the shift towards digital retail requires substantial investment in e-commerce infrastructure and cybersecurity. Maintaining brand exclusivity and desirability while expanding reach through online channels presents a delicate balancing act, risking brand dilution if not managed effectively.

Emerging Opportunities in US Luxury Market

Emerging opportunities within the US luxury market are abundant, driven by evolving consumer behaviors and technological breakthroughs. The burgeoning demand for sustainable and ethically produced luxury goods presents a significant avenue for growth, rewarding brands committed to transparency and responsible practices. Strategic partnerships, such as collaborations between luxury fashion houses and technology companies for innovative product development or immersive digital experiences, can unlock new revenue streams and customer engagement models. Market expansion strategies, including penetration into underserved demographics or geographical regions, alongside the growing influence of Gen Z and Millennial consumers with their unique purchasing power and values, offer substantial long-term growth potential. The continued rise of the experiential economy also presents opportunities for luxury brands to offer exclusive services, travel, and bespoke events.

Leading Players in the US Luxury Market Sector

- Giorgio Armani S p A

- The Swatch Group

- Kering

- Compagnie Financière Richemont S A

- L'Oreal Luxe

- Rolex SA

- PVH Corp

- The Estee Lauder Companies

- LVMH Moët Hennessy Louis Vuitton

- Burberry

Key Milestones in US Luxury Market Industry

- May 2022: Kering group's brand Gucci collaborated with Adidas in launching their new luxury goods through an online platform along with a few selected stores. This launch focused on hybrid pattern ready-to-wear clothes and accessories.

- March 2022: De Beers, a luxury jewelry house, launched a new haute couture jewelry collection called "The Alchemist of Light," at Miami's St. Regis Bal Harbour, highlighting exclusivity and artistic innovation.

- March 2021: Swatch announced the release of limited-edition designs created in collaboration with The Museum of Modern Art (MoMA) as part of its Museum Journey collection. The wristwatches were sold through Swatch stores globally, Swatch.com, MoMA Design Stores, and store.moma.org, showcasing strategic brand collaborations for wider reach.

Strategic Outlook for US Luxury Market Market

The strategic outlook for the US luxury market is one of continued innovation and adaptation. Growth accelerators include the deepening integration of AI and AR to create hyper-personalized customer journeys, both online and in-store, enhancing engagement and driving conversion rates. The expansion of sustainable luxury offerings, supported by transparent supply chains and ethically sourced materials, will become a critical competitive advantage and a primary driver of consumer loyalty. Strategic partnerships between luxury brands and technology firms, as well as with artists and cultural institutions, will continue to foster creativity and broaden market appeal. Furthermore, a focus on experiential luxury, encompassing exclusive events, personalized services, and curated travel, will cater to the evolving desires of affluent consumers, solidifying the market's billion-dollar trajectory.

US Luxury Market Segmentation

-

1. Type

- 1.1. Clothing and Apparel

- 1.2. Footwear

- 1.3. Bags

- 1.4. Jewelry

- 1.5. Watches

- 1.6. Other Accessories

-

2. Distribution Channel

- 2.1. Single-brand Stores

- 2.2. Multi-brand Stores

- 2.3. Online Stores

- 2.4. Other Distribution Channels

US Luxury Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

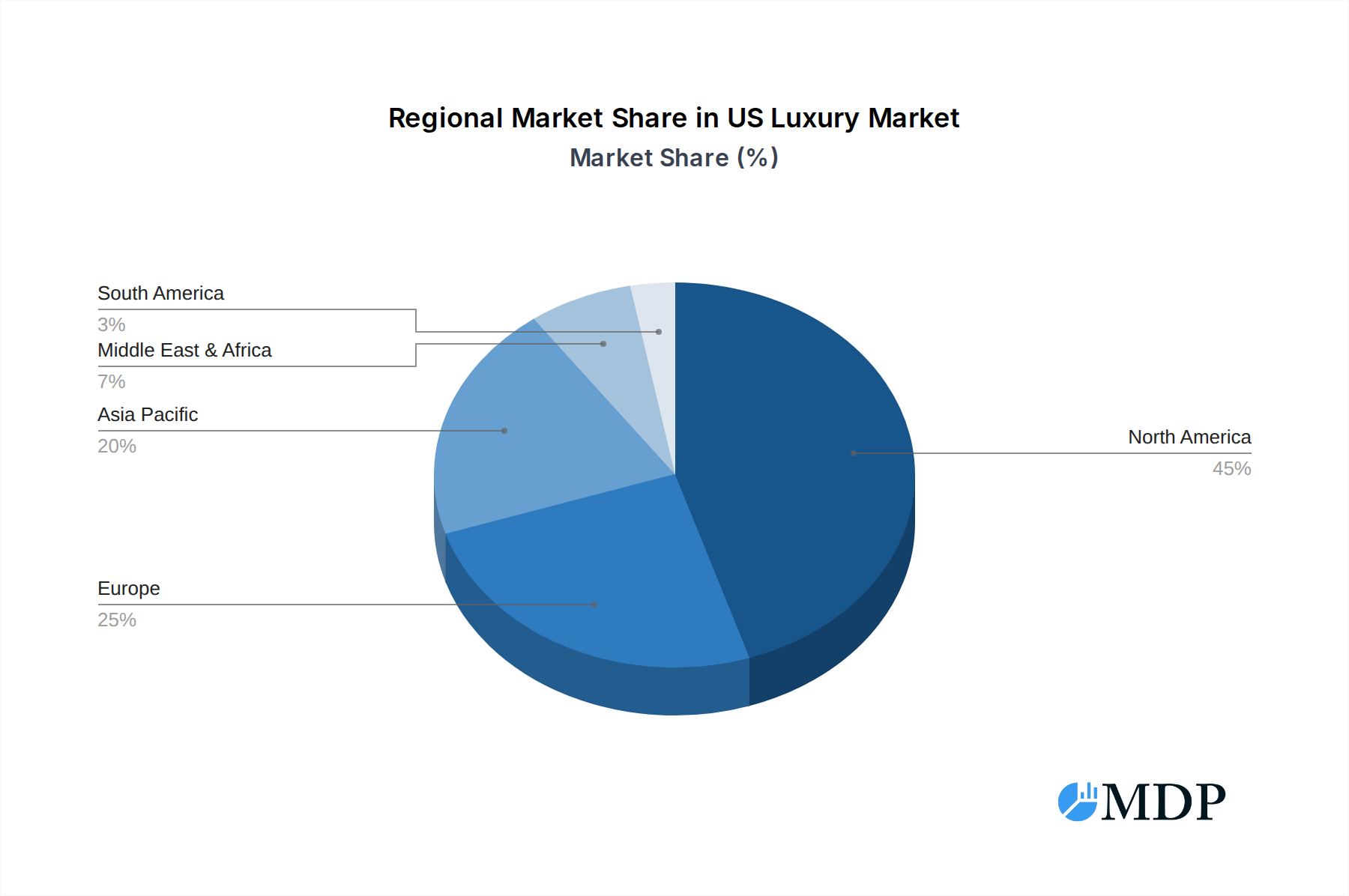

US Luxury Market Regional Market Share

Geographic Coverage of US Luxury Market

US Luxury Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Clothing and Apparel

- 5.1.2. Footwear

- 5.1.3. Bags

- 5.1.4. Jewelry

- 5.1.5. Watches

- 5.1.6. Other Accessories

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Single-brand Stores

- 5.2.2. Multi-brand Stores

- 5.2.3. Online Stores

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global US Luxury Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Clothing and Apparel

- 6.1.2. Footwear

- 6.1.3. Bags

- 6.1.4. Jewelry

- 6.1.5. Watches

- 6.1.6. Other Accessories

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Single-brand Stores

- 6.2.2. Multi-brand Stores

- 6.2.3. Online Stores

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America US Luxury Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Clothing and Apparel

- 7.1.2. Footwear

- 7.1.3. Bags

- 7.1.4. Jewelry

- 7.1.5. Watches

- 7.1.6. Other Accessories

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Single-brand Stores

- 7.2.2. Multi-brand Stores

- 7.2.3. Online Stores

- 7.2.4. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. South America US Luxury Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Clothing and Apparel

- 8.1.2. Footwear

- 8.1.3. Bags

- 8.1.4. Jewelry

- 8.1.5. Watches

- 8.1.6. Other Accessories

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Single-brand Stores

- 8.2.2. Multi-brand Stores

- 8.2.3. Online Stores

- 8.2.4. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe US Luxury Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Clothing and Apparel

- 9.1.2. Footwear

- 9.1.3. Bags

- 9.1.4. Jewelry

- 9.1.5. Watches

- 9.1.6. Other Accessories

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Single-brand Stores

- 9.2.2. Multi-brand Stores

- 9.2.3. Online Stores

- 9.2.4. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East & Africa US Luxury Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Clothing and Apparel

- 10.1.2. Footwear

- 10.1.3. Bags

- 10.1.4. Jewelry

- 10.1.5. Watches

- 10.1.6. Other Accessories

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Single-brand Stores

- 10.2.2. Multi-brand Stores

- 10.2.3. Online Stores

- 10.2.4. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific US Luxury Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Clothing and Apparel

- 11.1.2. Footwear

- 11.1.3. Bags

- 11.1.4. Jewelry

- 11.1.5. Watches

- 11.1.6. Other Accessories

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Single-brand Stores

- 11.2.2. Multi-brand Stores

- 11.2.3. Online Stores

- 11.2.4. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Giorgio Armani S p A

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 The Swatch Group

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Kering

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Compagnie Financière Richemont S A

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 L'Oreal Luxe

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Rolex SA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 PVH Corp

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 The Estee Lauder Companies

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 LVMH Moët Hennessy Louis Vuitton

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Burberry*List Not Exhaustive

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Giorgio Armani S p A

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global US Luxury Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America US Luxury Market Revenue (billion), by Type 2025 & 2033

- Figure 3: North America US Luxury Market Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America US Luxury Market Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 5: North America US Luxury Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 6: North America US Luxury Market Revenue (billion), by Country 2025 & 2033

- Figure 7: North America US Luxury Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America US Luxury Market Revenue (billion), by Type 2025 & 2033

- Figure 9: South America US Luxury Market Revenue Share (%), by Type 2025 & 2033

- Figure 10: South America US Luxury Market Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 11: South America US Luxury Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 12: South America US Luxury Market Revenue (billion), by Country 2025 & 2033

- Figure 13: South America US Luxury Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe US Luxury Market Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe US Luxury Market Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe US Luxury Market Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 17: Europe US Luxury Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 18: Europe US Luxury Market Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe US Luxury Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa US Luxury Market Revenue (billion), by Type 2025 & 2033

- Figure 21: Middle East & Africa US Luxury Market Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East & Africa US Luxury Market Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 23: Middle East & Africa US Luxury Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 24: Middle East & Africa US Luxury Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa US Luxury Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific US Luxury Market Revenue (billion), by Type 2025 & 2033

- Figure 27: Asia Pacific US Luxury Market Revenue Share (%), by Type 2025 & 2033

- Figure 28: Asia Pacific US Luxury Market Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 29: Asia Pacific US Luxury Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Asia Pacific US Luxury Market Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific US Luxury Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global US Luxury Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global US Luxury Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Global US Luxury Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global US Luxury Market Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global US Luxury Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global US Luxury Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global US Luxury Market Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global US Luxury Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 12: Global US Luxury Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global US Luxury Market Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global US Luxury Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 18: Global US Luxury Market Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global US Luxury Market Revenue billion Forecast, by Type 2020 & 2033

- Table 29: Global US Luxury Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 30: Global US Luxury Market Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global US Luxury Market Revenue billion Forecast, by Type 2020 & 2033

- Table 38: Global US Luxury Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 39: Global US Luxury Market Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific US Luxury Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the US Luxury Market?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the US Luxury Market?

Key companies in the market include Giorgio Armani S p A, The Swatch Group, Kering, Compagnie Financière Richemont S A, L'Oreal Luxe, Rolex SA, PVH Corp, The Estee Lauder Companies, LVMH Moët Hennessy Louis Vuitton, Burberry*List Not Exhaustive.

3. What are the main segments of the US Luxury Market?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 274.8 billion as of 2022.

5. What are some drivers contributing to market growth?

Demand for Smartwatches; Popularity of Luxury Watches.

6. What are the notable trends driving market growth?

High Prevalence of Fashion-Conscious Consumers.

7. Are there any restraints impacting market growth?

Presence of Fake Brands in the Market.

8. Can you provide examples of recent developments in the market?

In May 2022, Kering group's brand Gucci collaborated with Adidas in launching their new luxury goods through an online platform along with a few selected stores. With this launch, the brands focused on launching hybrid pattern ready-to-wear clothes and accessories in the region.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "US Luxury Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the US Luxury Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the US Luxury Market?

To stay informed about further developments, trends, and reports in the US Luxury Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence