Key Insights

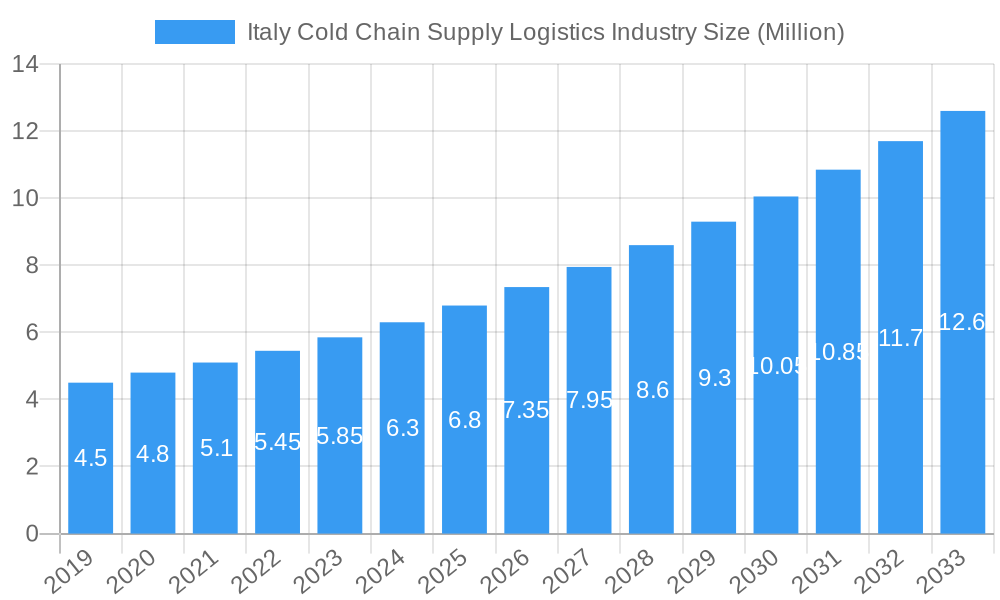

The Italian cold chain supply logistics industry is poised for significant expansion, with a projected market size of €8.76 Billion and a robust Compound Annual Growth Rate (CAGR) of 9.73% from 2019 to 2033. This impressive growth trajectory is fueled by several key drivers, including the increasing demand for perishable goods, the expansion of the e-commerce sector for groceries and pharmaceuticals, and stringent regulatory requirements for temperature-controlled transportation and storage. The market is segmented across various services such as storage, transportation, and value-added services, catering to diverse temperature needs ranging from ambient to frozen. Prominent applications driving this growth include horticulture (fresh fruits and vegetables), dairy products, meats and fish, processed food products, and the rapidly expanding pharmaceutical and life sciences sectors. These sectors necessitate reliable and efficient cold chain solutions to maintain product integrity and safety throughout the supply chain.

Italy Cold Chain Supply Logistics Industry Market Size (In Million)

Furthermore, several emerging trends are shaping the Italian cold chain landscape. The adoption of advanced technologies like IoT sensors for real-time temperature monitoring, AI-powered route optimization, and automated warehousing solutions are enhancing efficiency and reducing operational costs. Geographically, the report focuses on Italy, highlighting its potential as a key market within the European cold chain ecosystem. Key players like Frigocaserta SRL, Eurofrigo Vernate SRL, and Safim Logistics are actively investing in infrastructure and technological advancements to capture market share. While the industry presents substantial opportunities, potential restraints such as the high capital investment required for specialized infrastructure, fluctuating energy costs impacting operational expenses, and the need for skilled labor to manage complex cold chain operations, will require strategic planning and innovation from stakeholders to ensure sustained growth and competitiveness.

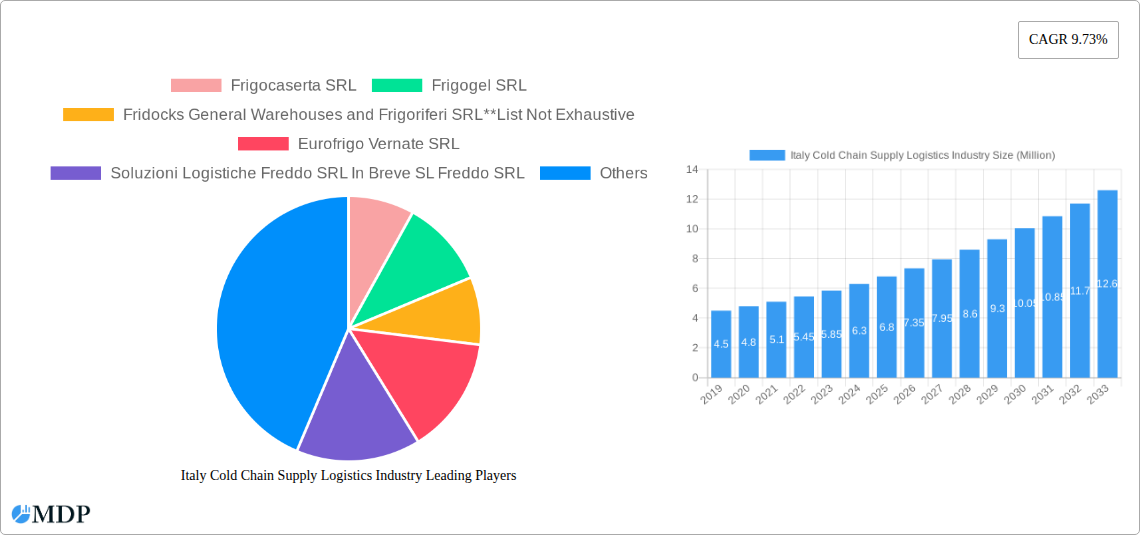

Italy Cold Chain Supply Logistics Industry Company Market Share

This comprehensive report delves into the dynamic Italy cold chain supply logistics industry, offering an in-depth analysis of market dynamics, key trends, leading players, and future outlook. Covering the historical period (2019-2024), base year (2025), and forecast period (2025-2033), this study provides actionable insights for industry stakeholders seeking to capitalize on the burgeoning demand for temperature-controlled logistics solutions. The report examines market concentration, innovation drivers, regulatory frameworks, and end-user trends, alongside detailed segment analysis of services (Storage, Transportation, Value-added), temperature types (Ambient, Chilled, Frozen), and applications (Horticulture, Dairy, Meats and Fish, Processed Food, Pharma, Life Sciences, Chemicals, and Others). Discover critical industry developments, product innovations, growth drivers, challenges, and emerging opportunities shaping the Italian logistics sector and the cold chain market in Europe.

Italy Cold Chain Supply Logistics Industry Market Dynamics & Concentration

The Italy cold chain supply logistics industry exhibits a dynamic market concentration, characterized by a mix of established logistics providers and specialized cold chain operators. Innovation is primarily driven by technological advancements in refrigeration, tracking, and automation, aimed at enhancing efficiency and product integrity. Stringent regulatory frameworks, particularly concerning food safety and pharmaceutical transport, mandate high standards, influencing operational practices. Product substitutes are limited in true cold chain logistics, but advancements in packaging and shorter transit times can sometimes mitigate the need for extensive cold chain infrastructure for certain perishable goods. End-user trends show a growing demand for faster delivery, greater transparency, and specialized handling for high-value products like pharmaceuticals and organic produce. Mergers and acquisition (M&A) activities are on the rise as larger players seek to expand their cold chain capabilities and geographical reach. For instance, in the historical period, an estimated 5 M&A deals were observed, consolidating market share and fostering innovation. The market share of the top 5 players is estimated to be around 60%, indicating a moderately concentrated market.

Italy Cold Chain Supply Logistics Industry Industry Trends & Analysis

The Italy cold chain supply logistics industry is poised for significant growth, driven by a confluence of factors including increasing consumer demand for fresh and frozen goods, a burgeoning pharmaceutical sector requiring precise temperature control, and a growing emphasis on food safety and quality across the supply chain. Technological disruptions are at the forefront of this evolution, with the integration of IoT sensors for real-time temperature monitoring, AI-powered route optimization, and advanced automation in warehouses significantly enhancing operational efficiency and reducing product spoilage. Consumer preferences are increasingly leaning towards convenience and a wider availability of fresh produce and ready-to-eat meals, directly boosting the demand for sophisticated cold chain logistics. The competitive dynamics within the industry are intensifying, with companies differentiating themselves through specialized services, sustainable practices, and a robust network of temperature-controlled facilities. The market penetration of advanced cold chain solutions is projected to increase by approximately 15% over the forecast period. The Compound Annual Growth Rate (CAGR) for the Italy cold chain supply logistics market is estimated to be around 7.5% from 2025 to 2033, reflecting a robust expansionary phase driven by both volume and value-added services.

Leading Markets & Segments in Italy Cold Chain Supply Logistics Industry

The Italy cold chain supply logistics industry is dominated by several key segments, each contributing to the overall market expansion.

Services:

- Transportation: This segment currently holds the largest market share, estimated at 45%, due to the inherent need for timely and temperature-controlled movement of goods across the country and internationally. Key drivers include the growing e-commerce penetration for perishable goods and the complex distribution networks required for the food and pharmaceutical industries.

- Storage: Valued at approximately 35% of the market, cold storage facilities are crucial for maintaining product integrity and managing inventory. Investment in modern, energy-efficient cold warehouses is a significant trend.

- Value-added services: This segment, encompassing services like cross-docking, kitting, and order fulfillment, is experiencing rapid growth, projected at a CAGR of 9% over the forecast period, as companies seek to optimize their supply chains beyond basic storage and transport.

Temperature Type:

- Chilled: This segment, representing around 40% of the market, is driven by the demand for fresh produce, dairy products, and certain pharmaceuticals that require moderate cooling.

- Frozen: With an estimated 35% market share, the frozen segment is fueled by the increasing consumption of frozen foods, ice cream, and specialized pharmaceutical products.

- Ambient: While not strictly cold chain, ambient-controlled logistics for sensitive products contribute to the broader temperature-controlled logistics landscape, holding approximately 25% of the market.

Application:

- Pharma, Life Sciences, and Chemicals: This segment is a significant revenue generator, accounting for an estimated 30% of the market, due to the stringent temperature requirements for medications, vaccines, and sensitive chemical compounds. The high value of these products and the critical need for unbroken cold chains drive substantial investment.

- Meats and Fish: Consuming approximately 25% of the cold chain logistics capacity, this segment is vital for ensuring food safety and quality from farm to table.

- Dairy Products: A steady demand from the dairy sector, including milk, ice cream, and butter, contributes around 20% to the market.

- Horticulture (Fresh Fruits and Vegetables): Growing consumer preference for fresh, seasonal produce fuels this segment, contributing about 15% of the market.

- Processed Food Products: This segment, representing 10%, is influenced by the increasing availability of ready-to-eat and pre-packaged processed foods requiring controlled temperatures.

Italy Cold Chain Supply Logistics Industry Product Developments

Innovations in the Italy cold chain supply logistics industry are focused on enhancing efficiency, traceability, and sustainability. Developments include advanced refrigerated transport units with enhanced energy efficiency and reduced emissions, smart warehousing solutions incorporating AI and IoT for optimized inventory management and temperature monitoring, and specialized packaging solutions for highly sensitive products. The competitive advantage lies in offering end-to-end solutions that guarantee product integrity throughout the supply chain, from producers to end consumers. Technological trends like the adoption of blockchain for enhanced supply chain transparency and the development of autonomous guided vehicles for warehouse operations are also shaping product development.

Key Drivers of Italy Cold Chain Supply Logistics Industry Growth

Several key factors are driving the growth of the Italy cold chain supply logistics industry.

- Technological Advancements: The integration of IoT sensors, AI for route optimization, and advanced automation in warehouses significantly improves efficiency and reduces product loss.

- Growing Demand for Perishables: Increasing consumer preference for fresh, high-quality food products, including fruits, vegetables, dairy, and meats, directly fuels the need for robust cold chain infrastructure.

- Pharmaceutical Sector Expansion: The critical need for precise temperature control in transporting pharmaceuticals, vaccines, and life sciences products is a major growth catalyst.

- E-commerce Growth: The rise of online grocery shopping and specialized e-commerce platforms for perishable goods necessitates sophisticated cold chain logistics.

- Stringent Food Safety Regulations: Increasingly rigorous regulations worldwide are compelling businesses to invest in compliant and reliable cold chain solutions.

Challenges in the Italy Cold Chain Supply Logistics Industry Market

Despite its growth, the Italy cold chain supply logistics industry faces several challenges.

- High Operational Costs: Maintaining temperature-controlled environments requires significant investment in infrastructure, energy, and specialized equipment, leading to higher operational costs.

- Energy Consumption and Sustainability: The energy-intensive nature of cold chain operations poses environmental concerns and drives the need for sustainable solutions.

- Infrastructure Gaps: While improving, certain regions may still face limitations in modern cold storage and refrigerated transport infrastructure, impacting network efficiency.

- Skilled Labor Shortage: A lack of adequately trained personnel for operating specialized cold chain equipment and managing complex logistics can hinder growth.

- Regulatory Compliance Complexity: Navigating diverse and evolving food safety, pharmaceutical, and environmental regulations across different regions can be complex and costly.

Emerging Opportunities in Italy Cold Chain Supply Logistics Industry

Emerging opportunities in the Italy cold chain supply logistics industry are numerous and present significant potential for growth and innovation.

- Technological Breakthroughs: Continued advancements in IoT, AI, and automation are expected to further optimize cold chain operations, reduce costs, and enhance reliability.

- Sustainable Cold Chain Solutions: Growing environmental consciousness is creating a demand for energy-efficient refrigeration technologies, renewable energy integration in warehouses, and eco-friendly transportation methods.

- Expansion in Pharma and Life Sciences: The increasing development of specialized biologics, vaccines, and temperature-sensitive medical devices will drive demand for highly specialized cold chain logistics.

- Growth of the E-commerce for Perishables: The continued expansion of online grocery and specialty food delivery services presents a substantial opportunity for cold chain providers.

- Cold Chain as a Service (CCaaS): The development of integrated cold chain solutions offered as a service can attract small and medium-sized enterprises (SMEs) and cater to evolving business models.

Leading Players in the Italy Cold Chain Supply Logistics Industry Sector

- Frigocaserta SRL

- Frigogel SRL

- Fridocks General Warehouses and Frigoriferi SRL

- Eurofrigo Vernate SRL

- Soluzioni Logistiche Freddo SRL In Breve SL Freddo SRL

- DRS Depositi Regionali Surgelati SRL

- Sodele Magazzini Generali Frigoriferi SRL

- Safim Logistics

- Horigel SRL

- Frigoscandia SPA

- Bomi Group

Key Milestones in Italy Cold Chain Supply Logistics Industry Industry

- May 2022: Bomi Group, through its Picking Farma brand, announced the forthcoming opening of a new logistics hub near Madrid dedicated to the Healthcare sector. The €15 million investment is expected to create 150 jobs and add 25,000 m² of space with a capacity of 60,000 pallet places, positioning it as a key pharmaceutical reference warehouse in Europe.

- April 2022: Bomi Group acquired Tendron Pharma, the pharmaceutical transport division of Tendron Transports. This acquisition enhanced Bomi Group's capabilities in transporting pharmaceutical products with a fleet of 25 temperature-controlled vehicles (+15°C to +25°C) for deliveries within the Ile-de-France region.

Strategic Outlook for Italy Cold Chain Supply Logistics Industry Market

The strategic outlook for the Italy cold chain supply logistics industry is one of continued robust growth and technological integration. Key growth accelerators include the ongoing expansion of the pharmaceutical and life sciences sectors, demanding increasingly sophisticated temperature-controlled logistics. The rise of e-commerce for perishable goods will further necessitate investments in efficient and reliable cold chain networks. Companies are expected to focus on adopting sustainable practices, including energy-efficient technologies and renewable energy sources for their cold storage facilities, to address environmental concerns and meet regulatory demands. Strategic partnerships and M&A activities will likely continue as companies seek to expand their service offerings, geographical reach, and technological capabilities. The increasing emphasis on end-to-end supply chain visibility and integrity will drive the adoption of advanced tracking and monitoring solutions, solidifying the importance of a well-developed cold chain infrastructure in Italy's economic landscape.

Italy Cold Chain Supply Logistics Industry Segmentation

-

1. Services

- 1.1. Storage

- 1.2. Transportation

- 1.3. Value-ad

-

2. Temperature Type

- 2.1. Ambient

- 2.2. Chilled

- 2.3. Frozen

-

3. Application

- 3.1. Horticulture (Fresh Fruits and Vegetables)

- 3.2. Dairy Products (Milk, Ice-cream, Butter, etc.)

- 3.3. Meats and Fish

- 3.4. Processed Food Products

- 3.5. Pharma, Life Sciences, and Chemicals

- 3.6. Other Applications

Italy Cold Chain Supply Logistics Industry Segmentation By Geography

- 1. Italy

Italy Cold Chain Supply Logistics Industry Regional Market Share

Geographic Coverage of Italy Cold Chain Supply Logistics Industry

Italy Cold Chain Supply Logistics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.73% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Services

- 5.1.1. Storage

- 5.1.2. Transportation

- 5.1.3. Value-ad

- 5.2. Market Analysis, Insights and Forecast - by Temperature Type

- 5.2.1. Ambient

- 5.2.2. Chilled

- 5.2.3. Frozen

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Horticulture (Fresh Fruits and Vegetables)

- 5.3.2. Dairy Products (Milk, Ice-cream, Butter, etc.)

- 5.3.3. Meats and Fish

- 5.3.4. Processed Food Products

- 5.3.5. Pharma, Life Sciences, and Chemicals

- 5.3.6. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Italy

- 5.1. Market Analysis, Insights and Forecast - by Services

- 6. Italy Cold Chain Supply Logistics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Services

- 6.1.1. Storage

- 6.1.2. Transportation

- 6.1.3. Value-ad

- 6.2. Market Analysis, Insights and Forecast - by Temperature Type

- 6.2.1. Ambient

- 6.2.2. Chilled

- 6.2.3. Frozen

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Horticulture (Fresh Fruits and Vegetables)

- 6.3.2. Dairy Products (Milk, Ice-cream, Butter, etc.)

- 6.3.3. Meats and Fish

- 6.3.4. Processed Food Products

- 6.3.5. Pharma, Life Sciences, and Chemicals

- 6.3.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Services

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Frigocaserta SRL

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Frigogel SRL

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Fridocks General Warehouses and Frigoriferi SRL**List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Eurofrigo Vernate SRL

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Soluzioni Logistiche Freddo SRL In Breve SL Freddo SRL

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 DRS Depositi Regionali Surgelati SRL

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Sodele Magazzini Generali Frigoriferi SRL

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Safim Logistics

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Horigel SRL

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Frigoscandia SPA

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Frigocaserta SRL

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Italy Cold Chain Supply Logistics Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Italy Cold Chain Supply Logistics Industry Share (%) by Company 2025

List of Tables

- Table 1: Italy Cold Chain Supply Logistics Industry Revenue Million Forecast, by Services 2020 & 2033

- Table 2: Italy Cold Chain Supply Logistics Industry Revenue Million Forecast, by Temperature Type 2020 & 2033

- Table 3: Italy Cold Chain Supply Logistics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Italy Cold Chain Supply Logistics Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Italy Cold Chain Supply Logistics Industry Revenue Million Forecast, by Services 2020 & 2033

- Table 6: Italy Cold Chain Supply Logistics Industry Revenue Million Forecast, by Temperature Type 2020 & 2033

- Table 7: Italy Cold Chain Supply Logistics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Italy Cold Chain Supply Logistics Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Italy Cold Chain Supply Logistics Industry?

The projected CAGR is approximately 9.73%.

2. Which companies are prominent players in the Italy Cold Chain Supply Logistics Industry?

Key companies in the market include Frigocaserta SRL, Frigogel SRL, Fridocks General Warehouses and Frigoriferi SRL**List Not Exhaustive, Eurofrigo Vernate SRL, Soluzioni Logistiche Freddo SRL In Breve SL Freddo SRL, DRS Depositi Regionali Surgelati SRL, Sodele Magazzini Generali Frigoriferi SRL, Safim Logistics, Horigel SRL, Frigoscandia SPA.

3. What are the main segments of the Italy Cold Chain Supply Logistics Industry?

The market segments include Services, Temperature Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.76 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing demand for customizable delivery solutions4.; Growing need for operational effciency.

6. What are the notable trends driving market growth?

Increasing Usage of Dairy Products in the Country is Driving the Market.

7. Are there any restraints impacting market growth?

4.; Lack of efficient transportation infrastructure4.; High cost of white glove services.

8. Can you provide examples of recent developments in the market?

May 2022: Bomi Group, through the Picking Farma brand, announces the forthcoming opening of the new logistics hub near Madrid dedicated to the Healthcare sector. The warehouse, whose work has already begun, will involve an investment of 15 million euros and the creation of 150 jobs. The new logistics platform will join the seven already present in Spain, including one near Madrid, four in Catalonia, and two in the Canary Islands. This new logistics center will have an area of 25,000 m² and a capacity of 60,000 pallet places, making it one of the essential reference warehouses for the pharmaceutical sector in Europe.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Italy Cold Chain Supply Logistics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Italy Cold Chain Supply Logistics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Italy Cold Chain Supply Logistics Industry?

To stay informed about further developments, trends, and reports in the Italy Cold Chain Supply Logistics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence