Key Insights

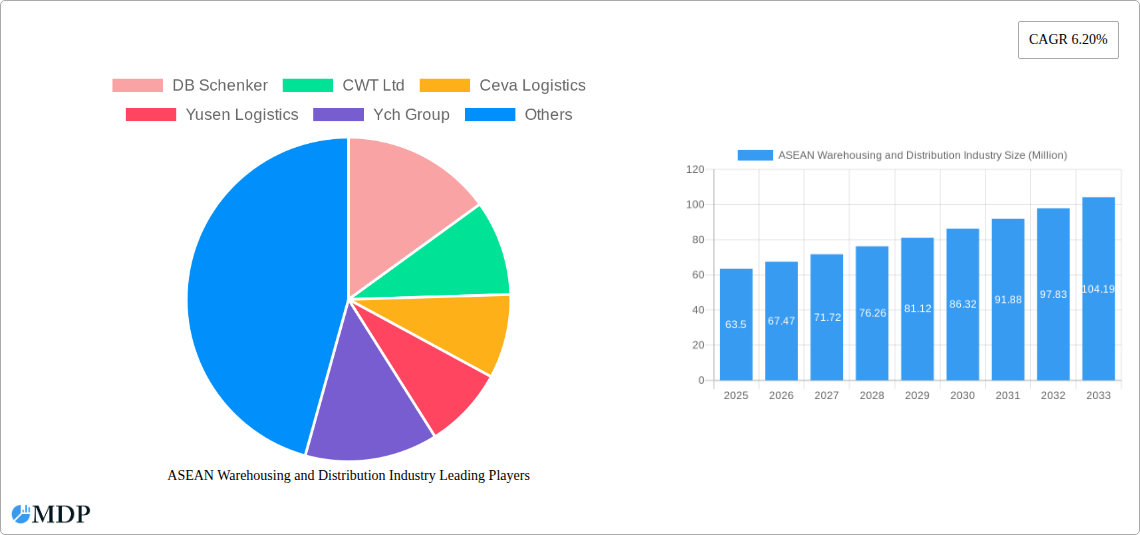

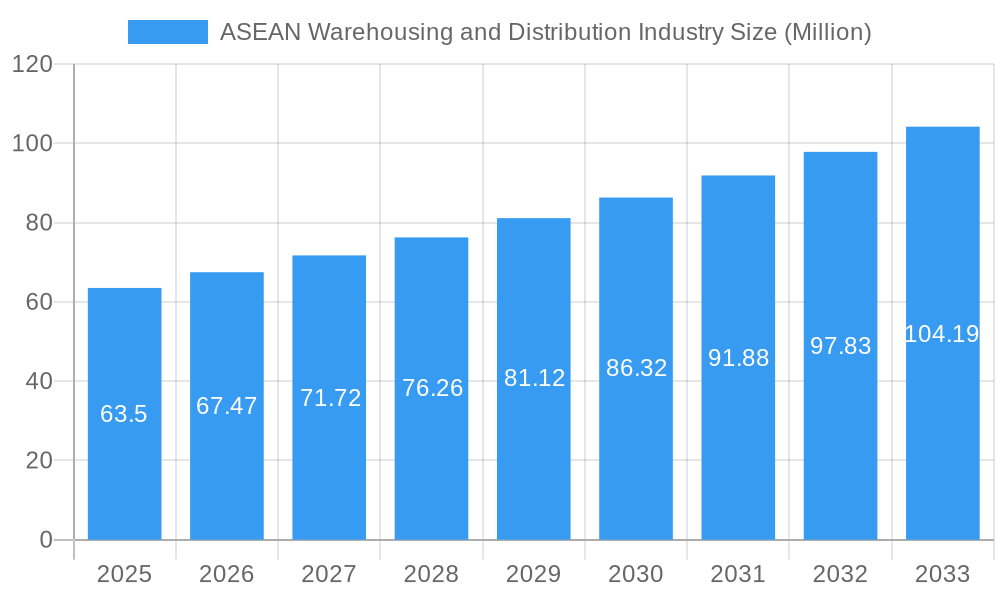

The ASEAN warehousing and distribution industry is experiencing robust growth, driven by the region's expanding e-commerce sector, rising consumer spending, and increasing foreign direct investment. The market, valued at approximately $63.50 million in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 6.20% from 2025 to 2033. This expansion is fueled by several key factors. The rise of e-commerce necessitates efficient warehousing and distribution networks to manage the increased volume of online orders. Furthermore, the growth of manufacturing and FMCG sectors in ASEAN countries creates a high demand for reliable logistics solutions. Value-added services, such as inventory management and packaging, are gaining traction as businesses seek to optimize their supply chains and enhance customer experience. While infrastructure limitations and competition among existing players represent potential challenges, government initiatives to improve infrastructure and logistics efficiency are expected to mitigate these restraints. The industry's segmentation reveals significant opportunities across various service types (warehousing, distribution, value-added services) and end-user industries (retail & e-commerce, automotive, pharmaceutical & healthcare, FMCG, manufacturing, electronics). Major players like DB Schenker, Kuehne + Nagel, and Kerry Logistics are leveraging their expertise and expanding their presence within the region to capture market share.

ASEAN Warehousing and Distribution Industry Market Size (In Million)

The sustained growth of the ASEAN warehousing and distribution market is expected to continue throughout the forecast period (2025-2033). The increasing adoption of advanced technologies like automation and big data analytics will further enhance efficiency and productivity within the industry. Moreover, the focus on sustainability and environmentally friendly logistics practices is gaining momentum, creating opportunities for companies that offer green logistics solutions. However, geopolitical uncertainties and potential economic fluctuations could influence the market's trajectory. Continuous monitoring of these factors is essential for businesses to adapt their strategies and maintain a competitive edge within the dynamic landscape of the ASEAN warehousing and distribution industry. Regional variations in market growth will be influenced by factors like economic development, infrastructure quality, and regulatory frameworks. Countries like Singapore and Indonesia, with their large and growing economies, are expected to contribute significantly to the overall market expansion.

ASEAN Warehousing and Distribution Industry Company Market Share

ASEAN Warehousing and Distribution Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides a detailed analysis of the ASEAN warehousing and distribution industry, covering market dynamics, leading players, and future growth opportunities. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report offers invaluable insights for industry stakeholders, investors, and strategic decision-makers. The report leverages extensive data analysis to provide actionable intelligence, forecasting a market valued at xx Million by 2033.

ASEAN Warehousing and Distribution Industry Market Dynamics & Concentration

This section analyzes the competitive landscape of the ASEAN warehousing and distribution market, examining market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and merger & acquisition (M&A) activities. The ASEAN region showcases a dynamic interplay of established multinational corporations and local players, resulting in a moderately concentrated market.

Market Concentration: The top 10 players account for approximately xx% of the market share in 2025, indicating a moderately consolidated market. This is expected to slightly decrease to xx% by 2033 due to the increasing number of smaller, specialized firms entering the market.

Innovation Drivers: Technological advancements like automation, AI, and IoT are driving innovation, improving efficiency and transparency across the supply chain. This is coupled with growing demand for value-added services such as customized packaging and labeling.

Regulatory Frameworks: Varying regulations across ASEAN nations create complexities for businesses operating across the region. Harmonization efforts are underway, but inconsistencies remain a challenge.

Product Substitutes: The emergence of e-commerce platforms and direct-to-consumer models presents a degree of substitution for traditional warehousing and distribution models.

End-User Trends: The rapid growth of e-commerce, particularly in urban centers, fuels significant demand for warehousing and distribution solutions optimized for speed and last-mile delivery.

M&A Activity: The sector has witnessed significant M&A activity in recent years, exemplified by Maersk’s acquisition of LF Logistics (August 2022) adding 223 warehouses and 9.5 Million square meters of space to its portfolio, and Geodis’s acquisition of Keppel Logistics (April 2022) expanding its footprint in Southeast Asia. We project xx M&A deals within the forecast period.

ASEAN Warehousing and Distribution Industry Industry Trends & Analysis

This section delves into the key trends shaping the ASEAN warehousing and distribution industry, encompassing market growth drivers, technological disruptions, evolving consumer preferences, and competitive dynamics. The industry exhibits a robust CAGR of xx% during the forecast period (2025-2033), driven primarily by burgeoning e-commerce and the rising adoption of advanced technologies. Market penetration of automated warehouse systems is predicted to reach xx% by 2033.

The increasing demand for efficient and reliable delivery systems, coupled with the growth of cross-border e-commerce, is driving the need for sophisticated warehouse management systems and integrated logistics solutions. Furthermore, the growing awareness of supply chain resilience is leading to increased investment in robust and diversified warehousing infrastructure. Competitive dynamics are marked by both collaboration and rivalry, with key players focusing on strategic partnerships, technological innovation, and expansion into new markets to gain a competitive edge.

Leading Markets & Segments in ASEAN Warehousing and Distribution Industry

This section identifies the dominant regions, countries, and segments within the ASEAN warehousing and distribution industry.

Dominant Segments:

By Service Type: Warehousing services currently hold the largest market share, followed by distribution services and value-added services. Value-added services are experiencing the fastest growth rate due to increasing customer demand for customized solutions.

By End-User Industry: The retail & e-commerce sector is the dominant end-user, followed by FMCG, manufacturing, and automotive. The pharmaceutical & healthcare segment exhibits significant growth potential due to stringent regulatory requirements and the need for specialized handling.

Key Drivers by Region/Country: (Using bullet points for brevity)

- Singapore: Robust infrastructure, advanced technology adoption, and strategic location.

- Indonesia: Largest population in ASEAN, rapidly expanding e-commerce sector.

- Thailand: Strong manufacturing base, growing logistics sector.

- Malaysia: Strategic location, improving infrastructure.

- Vietnam: Rapid economic growth, increasing foreign investment.

The detailed dominance analysis shows Singapore and Indonesia as leading markets due to their advanced infrastructure and strong e-commerce growth.

ASEAN Warehousing and Distribution Industry Product Developments

The ASEAN warehousing and distribution industry is witnessing significant product innovations driven by the integration of advanced technologies. Automation, including automated guided vehicles (AGVs) and robotic systems, is improving efficiency and reducing labor costs. The adoption of warehouse management systems (WMS) and transportation management systems (TMS) is enhancing visibility and control across the supply chain. This focus on technological integration leads to significant competitive advantages, improving speed, accuracy, and cost-effectiveness.

Key Drivers of ASEAN Warehousing and Distribution Industry Growth

The growth of the ASEAN warehousing and distribution industry is fueled by several key factors. The exponential growth of e-commerce is a primary driver, increasing the demand for efficient last-mile delivery solutions. Furthermore, government initiatives to improve infrastructure and streamline regulations are creating a more favorable business environment. Technological advancements, such as automation and data analytics, are enhancing efficiency and optimizing supply chain operations.

Challenges in the ASEAN Warehousing and Distribution Industry Market

The ASEAN warehousing and distribution industry faces several challenges. Infrastructure limitations in certain regions, particularly in terms of road networks and port facilities, can lead to logistical bottlenecks and higher transportation costs. The lack of skilled labor can hinder the adoption of advanced technologies and operational efficiency. Furthermore, differing regulatory frameworks across ASEAN countries create complexities for companies operating across the region. These factors collectively influence the overall efficiency and cost of operations. For example, xx Million in annual losses are estimated due to infrastructure limitations.

Emerging Opportunities in ASEAN Warehousing and Distribution Industry

Significant long-term growth opportunities exist for the ASEAN warehousing and distribution industry. The continued expansion of e-commerce, the rise of cross-border trade, and the growing adoption of advanced technologies present substantial potential for market expansion. Strategic partnerships between technology providers and logistics companies can unlock further innovation and efficiency gains. Moreover, investment in sustainable and environmentally friendly warehousing solutions aligns with growing global sustainability goals.

Leading Players in the ASEAN Warehousing and Distribution Industry Sector

- DB Schenker

- CWT Ltd

- Ceva Logistics

- Yusen Logistics

- Ych Group

- Gemadept

- WHA Corporation

- Kuehne + Nagel

- Singapore Post

- Agility

- Kerry Logistics

- CJ Century Logistics

- Tiong Nam Logistics

- Keppel Logistics

- DHL Supply Chain

- [List Not Exhaustive - 6 additional companies with key information/overview are available in the full report]

Key Milestones in ASEAN Warehousing and Distribution Industry Industry

August 2022: Maersk's acquisition of LF Logistics significantly expanded its warehouse network in ASEAN, adding 223 facilities and 9.5 Million square meters of space. This acquisition highlights the consolidation trend within the industry and underscores the growing importance of e-commerce fulfillment capabilities.

April 2022: Geodis's acquisition of Keppel Logistics strengthened its presence in Southeast Asia, particularly in Singapore and Malaysia, enhancing its contract logistics and e-commerce fulfillment services. This acquisition showcases the ongoing strategic expansion of global players in the dynamic ASEAN market.

Strategic Outlook for ASEAN Warehousing and Distribution Industry Market

The ASEAN warehousing and distribution market is poised for substantial growth driven by the region's expanding economies, increasing e-commerce penetration, and the growing adoption of advanced technologies. Strategic partnerships, investments in sustainable infrastructure, and the focus on developing specialized services will be key to success in this dynamic market. The ongoing evolution towards a more interconnected and technology-driven supply chain presents significant opportunities for innovation and expansion. Companies that effectively leverage these trends will be well-positioned to capitalize on the significant market potential within the ASEAN region.

ASEAN Warehousing and Distribution Industry Segmentation

-

1. Geography

- 1.1. Singapore

- 1.2. Thailand

- 1.3. Malaysia

- 1.4. Vietnam

- 1.5. Indonesia

- 1.6. Philippines

- 1.7. Rest of ASEAN

ASEAN Warehousing and Distribution Industry Segmentation By Geography

- 1. Singapore

- 2. Thailand

- 3. Malaysia

- 4. Vietnam

- 5. Indonesia

- 6. Philippines

- 7. Rest of ASEAN

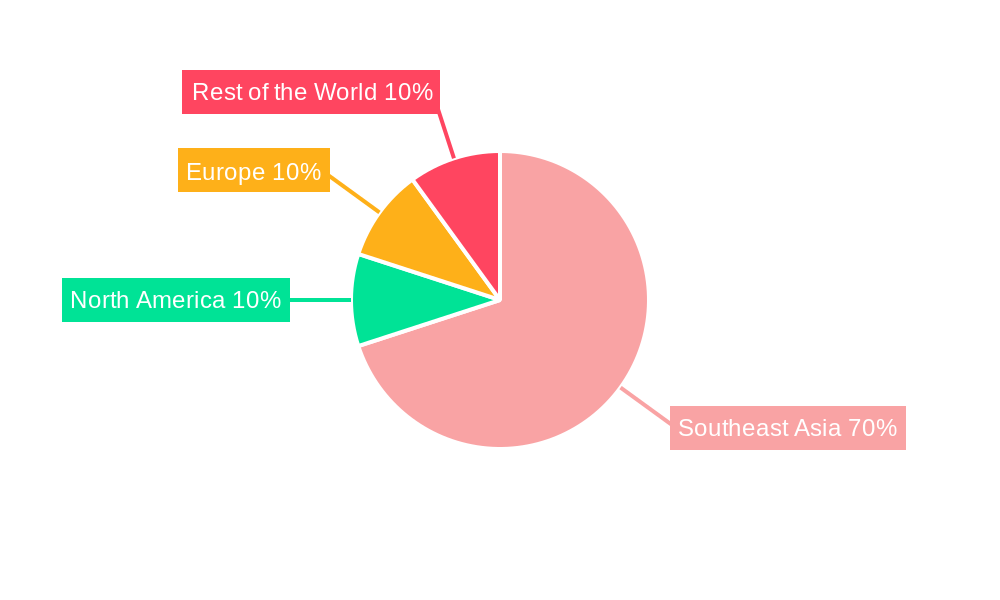

ASEAN Warehousing and Distribution Industry Regional Market Share

Geographic Coverage of ASEAN Warehousing and Distribution Industry

ASEAN Warehousing and Distribution Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Geography

- 5.1.1. Singapore

- 5.1.2. Thailand

- 5.1.3. Malaysia

- 5.1.4. Vietnam

- 5.1.5. Indonesia

- 5.1.6. Philippines

- 5.1.7. Rest of ASEAN

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Singapore

- 5.2.2. Thailand

- 5.2.3. Malaysia

- 5.2.4. Vietnam

- 5.2.5. Indonesia

- 5.2.6. Philippines

- 5.2.7. Rest of ASEAN

- 5.1. Market Analysis, Insights and Forecast - by Geography

- 6. Global ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Geography

- 6.1.1. Singapore

- 6.1.2. Thailand

- 6.1.3. Malaysia

- 6.1.4. Vietnam

- 6.1.5. Indonesia

- 6.1.6. Philippines

- 6.1.7. Rest of ASEAN

- 6.1. Market Analysis, Insights and Forecast - by Geography

- 7. Singapore ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Geography

- 7.1.1. Singapore

- 7.1.2. Thailand

- 7.1.3. Malaysia

- 7.1.4. Vietnam

- 7.1.5. Indonesia

- 7.1.6. Philippines

- 7.1.7. Rest of ASEAN

- 7.1. Market Analysis, Insights and Forecast - by Geography

- 8. Thailand ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Geography

- 8.1.1. Singapore

- 8.1.2. Thailand

- 8.1.3. Malaysia

- 8.1.4. Vietnam

- 8.1.5. Indonesia

- 8.1.6. Philippines

- 8.1.7. Rest of ASEAN

- 8.1. Market Analysis, Insights and Forecast - by Geography

- 9. Malaysia ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Geography

- 9.1.1. Singapore

- 9.1.2. Thailand

- 9.1.3. Malaysia

- 9.1.4. Vietnam

- 9.1.5. Indonesia

- 9.1.6. Philippines

- 9.1.7. Rest of ASEAN

- 9.1. Market Analysis, Insights and Forecast - by Geography

- 10. Vietnam ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Geography

- 10.1.1. Singapore

- 10.1.2. Thailand

- 10.1.3. Malaysia

- 10.1.4. Vietnam

- 10.1.5. Indonesia

- 10.1.6. Philippines

- 10.1.7. Rest of ASEAN

- 10.1. Market Analysis, Insights and Forecast - by Geography

- 11. Indonesia ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Geography

- 11.1.1. Singapore

- 11.1.2. Thailand

- 11.1.3. Malaysia

- 11.1.4. Vietnam

- 11.1.5. Indonesia

- 11.1.6. Philippines

- 11.1.7. Rest of ASEAN

- 11.1. Market Analysis, Insights and Forecast - by Geography

- 12. Philippines ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Geography

- 12.1.1. Singapore

- 12.1.2. Thailand

- 12.1.3. Malaysia

- 12.1.4. Vietnam

- 12.1.5. Indonesia

- 12.1.6. Philippines

- 12.1.7. Rest of ASEAN

- 12.1. Market Analysis, Insights and Forecast - by Geography

- 13. Rest of ASEAN ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Geography

- 13.1.1. Singapore

- 13.1.2. Thailand

- 13.1.3. Malaysia

- 13.1.4. Vietnam

- 13.1.5. Indonesia

- 13.1.6. Philippines

- 13.1.7. Rest of ASEAN

- 13.1. Market Analysis, Insights and Forecast - by Geography

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 DB Schenker

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 CWT Ltd

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 Ceva Logistics

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 Yusen Logistics

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 Ych Group

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 Gemadept

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 WHA Corporation

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 Kuehne + Nagel

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.9 Singapore Post

- 14.1.9.1. Company Overview

- 14.1.9.2. Products

- 14.1.9.3. Company Financials

- 14.1.9.4. SWOT Analysis

- 14.1.10 Agility

- 14.1.10.1. Company Overview

- 14.1.10.2. Products

- 14.1.10.3. Company Financials

- 14.1.10.4. SWOT Analysis

- 14.1.11 Kerry Logistics

- 14.1.11.1. Company Overview

- 14.1.11.2. Products

- 14.1.11.3. Company Financials

- 14.1.11.4. SWOT Analysis

- 14.1.12 CJ Century Logistics

- 14.1.12.1. Company Overview

- 14.1.12.2. Products

- 14.1.12.3. Company Financials

- 14.1.12.4. SWOT Analysis

- 14.1.13 Tiong Nam Logistics

- 14.1.13.1. Company Overview

- 14.1.13.2. Products

- 14.1.13.3. Company Financials

- 14.1.13.4. SWOT Analysis

- 14.1.14 Keppel Logistics**List Not Exhaustive 6 3 Other Companies (Key Information/Overview

- 14.1.14.1. Company Overview

- 14.1.14.2. Products

- 14.1.14.3. Company Financials

- 14.1.14.4. SWOT Analysis

- 14.1.15 DHL Supply Chain

- 14.1.15.1. Company Overview

- 14.1.15.2. Products

- 14.1.15.3. Company Financials

- 14.1.15.4. SWOT Analysis

- 14.1.1 DB Schenker

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: Global ASEAN Warehousing and Distribution Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Singapore ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 3: Singapore ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 4: Singapore ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: Singapore ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Thailand ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 7: Thailand ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 8: Thailand ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Thailand ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Malaysia ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 11: Malaysia ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 12: Malaysia ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Malaysia ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Vietnam ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 15: Vietnam ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 16: Vietnam ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Vietnam ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Indonesia ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 19: Indonesia ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 20: Indonesia ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Indonesia ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Philippines ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 23: Philippines ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 24: Philippines ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Philippines ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of ASEAN ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 27: Rest of ASEAN ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 28: Rest of ASEAN ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 29: Rest of ASEAN ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 2: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 4: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 8: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 10: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 12: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 14: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 16: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the ASEAN Warehousing and Distribution Industry?

The projected CAGR is approximately 6.20%.

2. Which companies are prominent players in the ASEAN Warehousing and Distribution Industry?

Key companies in the market include DB Schenker, CWT Ltd, Ceva Logistics, Yusen Logistics, Ych Group, Gemadept, WHA Corporation, Kuehne + Nagel, Singapore Post, Agility, Kerry Logistics, CJ Century Logistics, Tiong Nam Logistics, Keppel Logistics**List Not Exhaustive 6 3 Other Companies (Key Information/Overview, DHL Supply Chain.

3. What are the main segments of the ASEAN Warehousing and Distribution Industry?

The market segments include Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 63.50 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in the demand for the Air Cargo Capacity; The Rise of E-commerce.

6. What are the notable trends driving market growth?

Increase in Warehousing Space in Thailand.

7. Are there any restraints impacting market growth?

Cargo Restrictions.

8. Can you provide examples of recent developments in the market?

August 2022: A.P. Moller - Maersk (Maersk) announced the successful completion of its acquisition of LF Logistics, a logistics firm with premium capabilities in omnichannel fulfillment services, e-commerce, and inland shipping in the ASEAN region. Following the acquisition, Maersk will expand its warehouse network by adding 223 warehouses to its current network and increasing the total number of facilities, spread across 9.5 million square meters, to 549.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "ASEAN Warehousing and Distribution Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the ASEAN Warehousing and Distribution Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the ASEAN Warehousing and Distribution Industry?

To stay informed about further developments, trends, and reports in the ASEAN Warehousing and Distribution Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence