Key Insights

The global Fresh Keeping Film for Food market is projected for substantial growth, expected to reach 69.52 billion by the base year: 2025, with a projected Compound Annual Growth Rate (CAGR) of 6.23%. This expansion is driven by heightened consumer demand for convenient, fresh food and increased awareness of food waste reduction. The Household segment is anticipated to lead, fueled by rising disposable incomes and a focus on home cooking and food preservation. Supermarkets and Restaurants are also significant contributors, leveraging the film's ability to improve product presentation, extend shelf life, and maintain food quality. Demand for advanced film technologies offering superior barrier properties, temperature resistance, and enhanced user experience is rising.

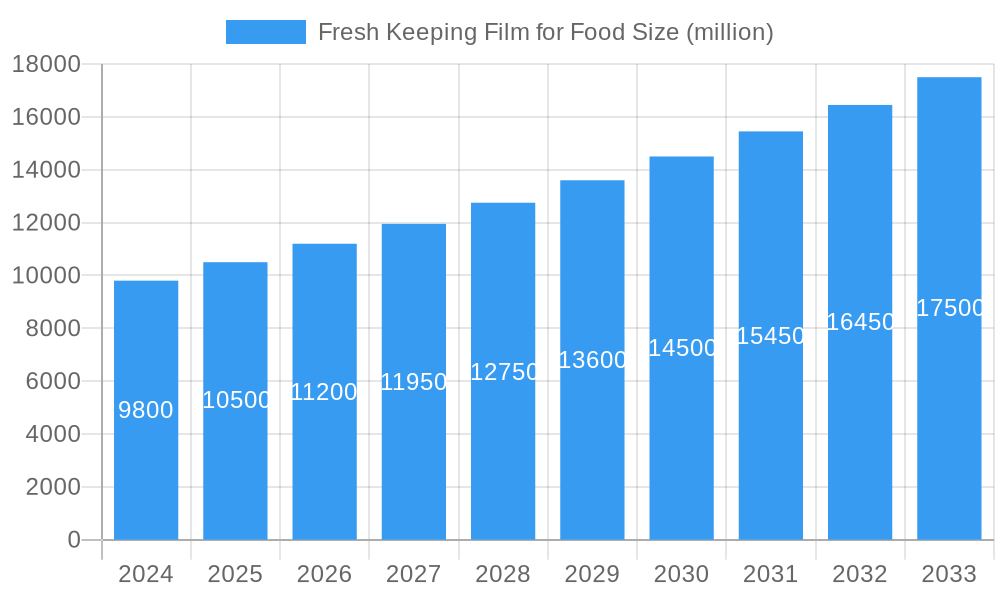

Fresh Keeping Film for Food Market Size (In Billion)

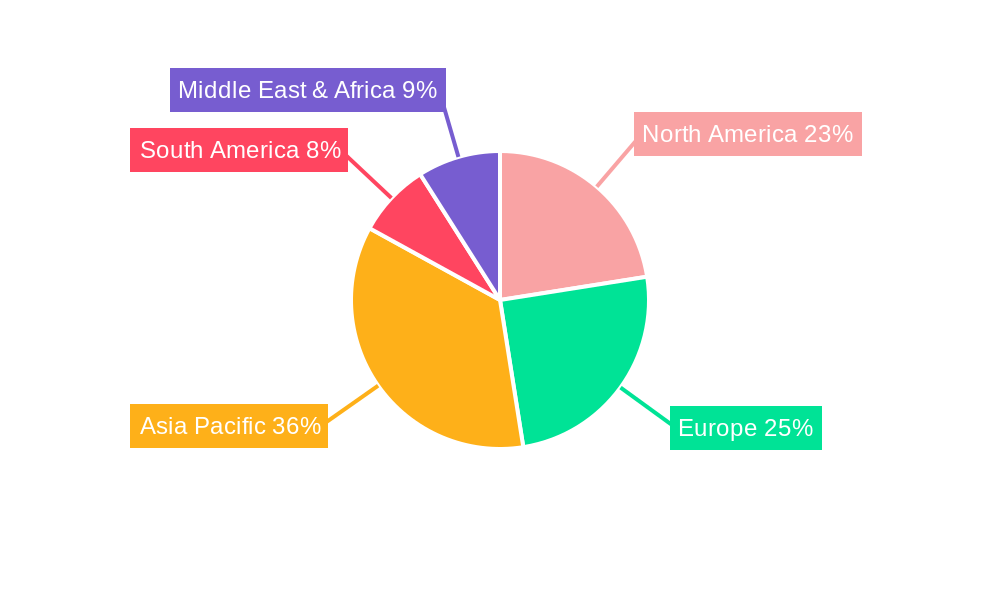

Key market drivers include the growing need for effective food preservation to minimize spoilage and economic losses, alongside evolving consumer preferences for visually appealing and safely packaged foods. The expansion of e-commerce in the food sector further boosts demand for reliable packaging ensuring product integrity during transit. Challenges include fluctuating raw material prices, particularly for PE and PVC, and increased regulatory scrutiny on plastic packaging and its environmental impact. Emerging trends such as biodegradable and compostable films, alongside advancements in recycling technologies, are crucial for addressing these challenges and shaping the future of the fresh keeping film industry. Asia Pacific is expected to dominate due to its large population, rapid urbanization, and a growing middle class with increasing purchasing power for fresh and packaged foods.

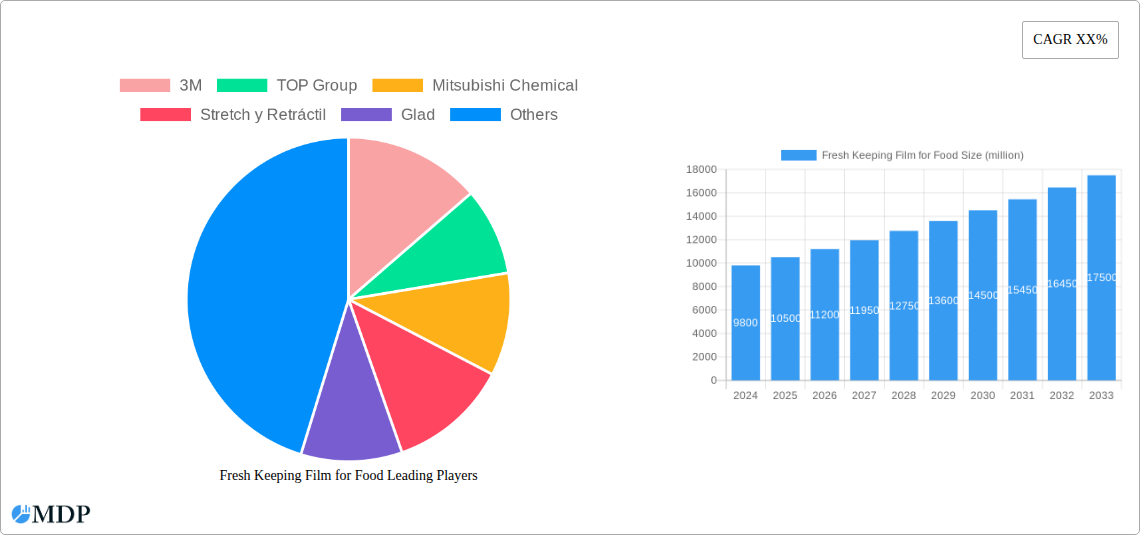

Fresh Keeping Film for Food Company Market Share

Fresh Keeping Film for Food Market: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report provides a strategic overview of the global Fresh Keeping Film for Food market, offering invaluable insights for industry stakeholders, manufacturers, and investors. Covering a comprehensive study period from 2019 to 2033, with a base and estimated year of 2025, this analysis delves into market dynamics, key trends, leading segments, product innovations, growth drivers, challenges, emerging opportunities, and a detailed company and milestone breakdown. The report leverages high-traffic keywords such as "food cling film," "food wrap," "fresh keeping film," "plastic wrap market," and "food packaging film" to ensure maximum visibility.

Fresh Keeping Film for Food Market Dynamics & Concentration

The global Fresh Keeping Film for Food market exhibits moderate to high concentration, with a significant presence of major players dominating market share. Innovation is a key driver, fueled by consumer demand for extended shelf life and reduced food waste. Regulatory frameworks, particularly concerning food contact materials and environmental sustainability, are shaping product development and market entry strategies. Product substitutes, including reusable containers and biodegradable alternatives, present a competitive challenge, influencing market penetration for traditional fresh keeping films. End-user trends show a growing preference for films with enhanced barrier properties and convenience features. Mergers and acquisitions (M&A) activities are observed as companies aim to expand their product portfolios, geographical reach, and technological capabilities, with an estimated xx M&A deals recorded historically. Key players like 3M, TOP Group, and Mitsubishi Chemical are strategically positioned to leverage these dynamics.

Fresh Keeping Film for Food Industry Trends & Analysis

The Fresh Keeping Film for Food industry is poised for robust growth, driven by increasing global population, evolving consumer lifestyles, and a heightened awareness of food preservation. The market is projected to experience a Compound Annual Growth Rate (CAGR) of approximately xx% during the forecast period of 2025–2033. Technological disruptions, such as advancements in polymer science leading to films with superior puncture resistance and better sealing capabilities, are significantly impacting market penetration. Consumer preferences are shifting towards films that offer improved freshness retention, ease of use, and sustainability credentials, including recyclable and compostable options. Competitive dynamics are characterized by intense price competition and continuous product innovation. The penetration of premium, high-performance fresh keeping films is expected to rise, particularly in developed economies. The historical period of 2019–2024 has witnessed a steady increase in demand, reflecting the essential role of these films in modern food supply chains. Leading companies are investing heavily in research and development to stay ahead of these trends, focusing on multi-layer films with specialized barrier properties and the integration of antimicrobial agents.

Leading Markets & Segments in Fresh Keeping Film for Food

The Household application segment currently holds a dominant market share in the Fresh Keeping Film for Food sector, driven by consistent demand for food storage and preservation in homes globally. The Supermarkets segment also represents a significant and growing market, owing to the need for visually appealing and effective food packaging to maintain freshness and extend shelf life for retail display.

- Dominant Region: Asia Pacific is anticipated to emerge as the leading market, propelled by rapid urbanization, a growing middle class, and increasing disposable incomes, which translate to higher consumption of packaged foods.

- Key Drivers in Household Segment:

- Increased awareness of food waste reduction.

- Convenience in everyday food storage.

- Growing adoption of ready-to-eat meals.

- Key Drivers in Supermarkets Segment:

- Demand for extended shelf life and attractive product presentation.

- Stringent food safety and hygiene regulations.

- Growth of organized retail sector.

- Dominant Type: Polyethylene (PE) films are expected to retain their leading position due to their cost-effectiveness, flexibility, and good barrier properties for general food wrapping applications. However, Polyvinylidene Chloride (PVDC) films are gaining traction in niche applications requiring superior barrier performance against oxygen and moisture.

- Key Drivers for PE:

- Cost-effectiveness and wide availability.

- Excellent flexibility and puncture resistance.

- Proven track record in food contact applications.

- Key Drivers for PVDC:

- Superior oxygen and moisture barrier properties.

- Enhanced product freshness and extended shelf life.

- Suitable for sensitive food products.

The Restaurants segment is also a vital contributor, with a focus on hygiene and portion control. The "Others" segment, encompassing institutional catering and food processing units, is expected to grow at a considerable pace, reflecting the expanding food service industry. The market's growth is further influenced by economic policies supporting the food and beverage industry and investments in cold chain infrastructure.

Fresh Keeping Film for Food Product Developments

Recent product developments in the Fresh Keeping Film for Food market are centered on enhancing functionality and sustainability. Innovations include the introduction of bio-based and compostable films derived from renewable resources, addressing environmental concerns. Enhanced barrier technologies, such as multi-layer co-extruded films with improved oxygen and moisture resistance, are being developed to extend food shelf life significantly. Microwave-safe and freezer-friendly films, along with those with improved cling and sealing properties, offer greater convenience to consumers. These advancements aim to provide competitive advantages by meeting evolving consumer demands for performance, safety, and eco-friendliness in food packaging solutions.

Key Drivers of Fresh Keeping Film for Food Growth

The growth of the Fresh Keeping Film for Food market is primarily propelled by several key factors. Firstly, the escalating global demand for convenience foods and ready-to-eat meals necessitates effective packaging solutions that preserve freshness and extend shelf life. Secondly, a growing consumer awareness regarding food waste reduction is driving the adoption of films that can better maintain food quality. Economically, rising disposable incomes in emerging economies are leading to increased per capita consumption of packaged foods. Technologically, advancements in polymer science are enabling the development of films with superior barrier properties, enhanced durability, and improved environmental profiles, such as recyclable or biodegradable options. Furthermore, stringent food safety regulations globally mandate the use of high-quality food contact materials, fostering market expansion for compliant fresh keeping films.

Challenges in the Fresh Keeping Film for Food Market

Despite its growth trajectory, the Fresh Keeping Film for Food market faces several significant challenges. The increasing environmental scrutiny surrounding single-use plastics poses a considerable restraint, leading to regulatory pressures and a growing demand for sustainable alternatives. Supply chain disruptions, including volatility in raw material prices and availability, can impact production costs and market stability. Intense competition among manufacturers, particularly in the commodity film segment, leads to price erosion and reduced profit margins. Furthermore, the development and adoption of innovative, eco-friendly substitutes, such as reusable silicone covers or beeswax wraps, present a competitive threat, potentially diverting market share from conventional plastic films.

Emerging Opportunities in Fresh Keeping Film for Food

Catalysts driving long-term growth in the Fresh Keeping Film for Food market include significant technological breakthroughs in material science, leading to the development of advanced, sustainable film options. Strategic partnerships between film manufacturers and food producers can unlock new market segments and application areas. The growing trend towards personalized nutrition and smaller portion sizes also presents an opportunity for specialized fresh keeping films. Furthermore, market expansion into developing economies with burgeoning middle classes and increasing adoption of modern retail practices offers substantial untapped potential. The development of "smart" films with indicators for spoilage or freshness levels could also create a significant competitive advantage and open new revenue streams.

Leading Players in the Fresh Keeping Film for Food Sector

The global Fresh Keeping Film for Food market is characterized by the presence of numerous established and emerging players. Key companies driving innovation and market growth include:

- 3M

- TOP Group

- Mitsubishi Chemical

- Stretch y Retráctil

- Glad

- Saran

- AEP Industries

- Pragya Flexifilm Industries

- FINO

- UNIQUE PLASTICS CORP

- National Plastics Factory

- SYSPEX

- Polyvinyl Films

- Wrap Film Systems

- Sphere

- Koroplast

- Pro-Pack

- Linpac Packaging

- Melitta

- Comcoplast

- Fora

- Victorgroup

- Wentus Kunststoff

- Shandong Koning Packaging

- Qingdao Longyouru Packing

- Qingdao Zhengdexiang Plastic Packaging

- Shandong Shenghe Plastic-Paper Packaging

- Samyoung Chemical

- Fujian Hengan Group

- Sichuan HongChang Plastics Industrial

- Bursa Pazar

- Sedat Tahir

- Asahi Kasei Home Products

- Cleanwrap

- Nan Ya Plastics

Key Milestones in Fresh Keeping Film for Food Industry

The evolution of the Fresh Keeping Film for Food industry is marked by significant milestones that have shaped its current landscape:

- 2019: Increased consumer focus on sustainability leads to early research into biodegradable plastic alternatives.

- 2020: Heightened awareness of food safety and hygiene drives demand for high-performance cling films in both household and commercial sectors.

- 2021: Introduction of advanced multi-layer PE films offering improved puncture resistance and clingability.

- 2022: Growing regulatory pressures in several regions begin to encourage the development of recyclable and post-consumer recycled content films.

- 2023: Significant investment in R&D for PVDC-free barrier films as part of a broader push towards more environmentally friendly packaging.

- 2024: Emergence of specialized films with anti-microbial properties for enhanced food preservation in critical applications.

- 2025 (Base Year): Market stabilization with a strong focus on balancing performance, cost, and environmental impact.

- 2026-2033 (Forecast Period): Anticipated acceleration in the adoption of bio-based and compostable films, alongside continued innovation in high-barrier PE and other polymer blends.

Strategic Outlook for Fresh Keeping Film for Food Market

The strategic outlook for the Fresh Keeping Film for Food market is one of sustained growth and adaptation. The future will be shaped by a dual focus on enhancing product performance for superior food preservation and addressing growing environmental concerns through sustainable material innovation. Companies that invest in research and development for biodegradable, compostable, and recyclable films, as well as those offering advanced barrier properties and convenience features, are best positioned for long-term success. Strategic partnerships and market expansion into emerging economies will be crucial growth accelerators. The market's ability to navigate regulatory landscapes and respond to evolving consumer preferences for both functionality and eco-consciousness will determine its trajectory in the coming years.

Fresh Keeping Film for Food Segmentation

-

1. Application

- 1.1. Household

- 1.2. Supermarkets

- 1.3. Restaurants

- 1.4. Others

-

2. Types

- 2.1. PE

- 2.2. PVC

- 2.3. PVDC

- 2.4. Others

Fresh Keeping Film for Food Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fresh Keeping Film for Food Regional Market Share

Geographic Coverage of Fresh Keeping Film for Food

Fresh Keeping Film for Food REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.23% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Fresh Keeping Film for Food Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Household

- 5.1.2. Supermarkets

- 5.1.3. Restaurants

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. PE

- 5.2.2. PVC

- 5.2.3. PVDC

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Fresh Keeping Film for Food Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Household

- 6.1.2. Supermarkets

- 6.1.3. Restaurants

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. PE

- 6.2.2. PVC

- 6.2.3. PVDC

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Fresh Keeping Film for Food Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Household

- 7.1.2. Supermarkets

- 7.1.3. Restaurants

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. PE

- 7.2.2. PVC

- 7.2.3. PVDC

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Fresh Keeping Film for Food Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Household

- 8.1.2. Supermarkets

- 8.1.3. Restaurants

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. PE

- 8.2.2. PVC

- 8.2.3. PVDC

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Fresh Keeping Film for Food Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Household

- 9.1.2. Supermarkets

- 9.1.3. Restaurants

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. PE

- 9.2.2. PVC

- 9.2.3. PVDC

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Fresh Keeping Film for Food Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Household

- 10.1.2. Supermarkets

- 10.1.3. Restaurants

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. PE

- 10.2.2. PVC

- 10.2.3. PVDC

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 3M

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 TOP Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Mitsubishi Chemical

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Stretch y Retráctil

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Glad

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Saran

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 AEP Industries

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Pragya Flexifilm Industries

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 FINO

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 UNIQUE PLASTICS CORP

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 National Plastics Factory

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 SYSPEX

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Polyvinyl Films

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Wrap Film Systems

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Sphere

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Koroplast

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Pro-Pack

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Linpac Packaging

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Melitta

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Comcoplast

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Fora

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Victorgroup

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Wentus Kunststoff

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Shandong Koning Packaging

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Qingdao Longyouru Packing

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Qingdao Zhengdexiang Plastic Packaging

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 Shandong Shenghe Plastic-Paper Packaging

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 Samyoung Chemical

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.29 Fujian Hengan Group

- 11.2.29.1. Overview

- 11.2.29.2. Products

- 11.2.29.3. SWOT Analysis

- 11.2.29.4. Recent Developments

- 11.2.29.5. Financials (Based on Availability)

- 11.2.30 Sichuan HongChang Plastics Industrial

- 11.2.30.1. Overview

- 11.2.30.2. Products

- 11.2.30.3. SWOT Analysis

- 11.2.30.4. Recent Developments

- 11.2.30.5. Financials (Based on Availability)

- 11.2.31 Bursa Pazar

- 11.2.31.1. Overview

- 11.2.31.2. Products

- 11.2.31.3. SWOT Analysis

- 11.2.31.4. Recent Developments

- 11.2.31.5. Financials (Based on Availability)

- 11.2.32 Sedat Tahir

- 11.2.32.1. Overview

- 11.2.32.2. Products

- 11.2.32.3. SWOT Analysis

- 11.2.32.4. Recent Developments

- 11.2.32.5. Financials (Based on Availability)

- 11.2.33 Asahi Kasei Home Products

- 11.2.33.1. Overview

- 11.2.33.2. Products

- 11.2.33.3. SWOT Analysis

- 11.2.33.4. Recent Developments

- 11.2.33.5. Financials (Based on Availability)

- 11.2.34 Cleanwrap

- 11.2.34.1. Overview

- 11.2.34.2. Products

- 11.2.34.3. SWOT Analysis

- 11.2.34.4. Recent Developments

- 11.2.34.5. Financials (Based on Availability)

- 11.2.35 Nan Ya Plastics

- 11.2.35.1. Overview

- 11.2.35.2. Products

- 11.2.35.3. SWOT Analysis

- 11.2.35.4. Recent Developments

- 11.2.35.5. Financials (Based on Availability)

- 11.2.1 3M

List of Figures

- Figure 1: Global Fresh Keeping Film for Food Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Fresh Keeping Film for Food Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Fresh Keeping Film for Food Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Fresh Keeping Film for Food Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Fresh Keeping Film for Food Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Fresh Keeping Film for Food Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Fresh Keeping Film for Food Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Fresh Keeping Film for Food Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Fresh Keeping Film for Food Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Fresh Keeping Film for Food Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Fresh Keeping Film for Food Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Fresh Keeping Film for Food Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Fresh Keeping Film for Food Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Fresh Keeping Film for Food Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Fresh Keeping Film for Food Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Fresh Keeping Film for Food Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Fresh Keeping Film for Food Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Fresh Keeping Film for Food Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Fresh Keeping Film for Food Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Fresh Keeping Film for Food Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Fresh Keeping Film for Food Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Fresh Keeping Film for Food Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Fresh Keeping Film for Food Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Fresh Keeping Film for Food Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Fresh Keeping Film for Food Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Fresh Keeping Film for Food Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Fresh Keeping Film for Food Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Fresh Keeping Film for Food Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Fresh Keeping Film for Food Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Fresh Keeping Film for Food Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Fresh Keeping Film for Food Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fresh Keeping Film for Food Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Fresh Keeping Film for Food Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Fresh Keeping Film for Food Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Fresh Keeping Film for Food Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Fresh Keeping Film for Food Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Fresh Keeping Film for Food Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Fresh Keeping Film for Food Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Fresh Keeping Film for Food Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Fresh Keeping Film for Food Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Fresh Keeping Film for Food Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Fresh Keeping Film for Food Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Fresh Keeping Film for Food Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Fresh Keeping Film for Food Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Fresh Keeping Film for Food Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Fresh Keeping Film for Food Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Fresh Keeping Film for Food Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Fresh Keeping Film for Food Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Fresh Keeping Film for Food Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Fresh Keeping Film for Food Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fresh Keeping Film for Food?

The projected CAGR is approximately 6.23%.

2. Which companies are prominent players in the Fresh Keeping Film for Food?

Key companies in the market include 3M, TOP Group, Mitsubishi Chemical, Stretch y Retráctil, Glad, Saran, AEP Industries, Pragya Flexifilm Industries, FINO, UNIQUE PLASTICS CORP, National Plastics Factory, SYSPEX, Polyvinyl Films, Wrap Film Systems, Sphere, Koroplast, Pro-Pack, Linpac Packaging, Melitta, Comcoplast, Fora, Victorgroup, Wentus Kunststoff, Shandong Koning Packaging, Qingdao Longyouru Packing, Qingdao Zhengdexiang Plastic Packaging, Shandong Shenghe Plastic-Paper Packaging, Samyoung Chemical, Fujian Hengan Group, Sichuan HongChang Plastics Industrial, Bursa Pazar, Sedat Tahir, Asahi Kasei Home Products, Cleanwrap, Nan Ya Plastics.

3. What are the main segments of the Fresh Keeping Film for Food?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 69.52 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fresh Keeping Film for Food," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fresh Keeping Film for Food report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fresh Keeping Film for Food?

To stay informed about further developments, trends, and reports in the Fresh Keeping Film for Food, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence