Key Insights

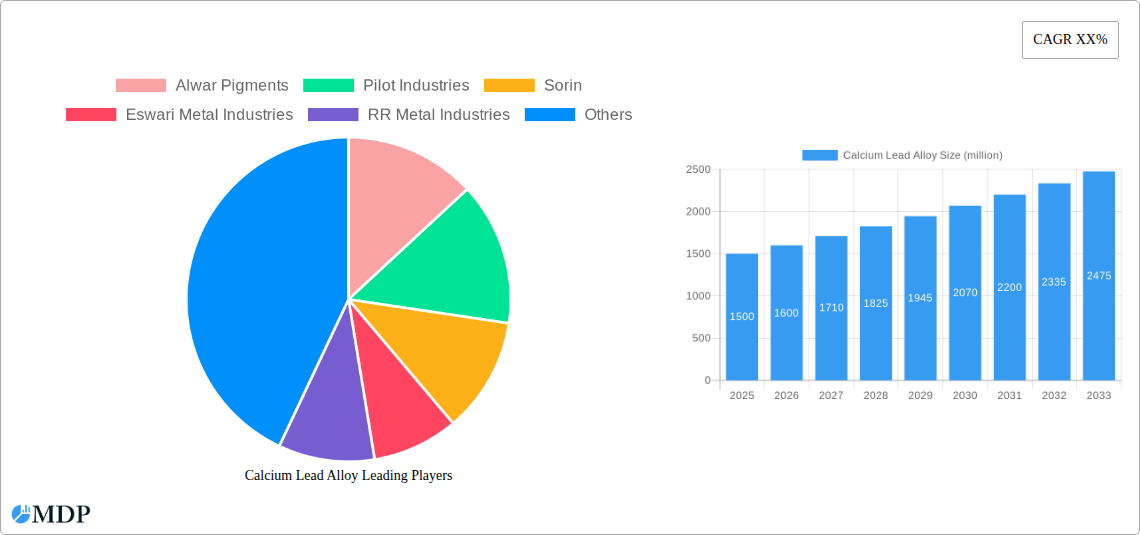

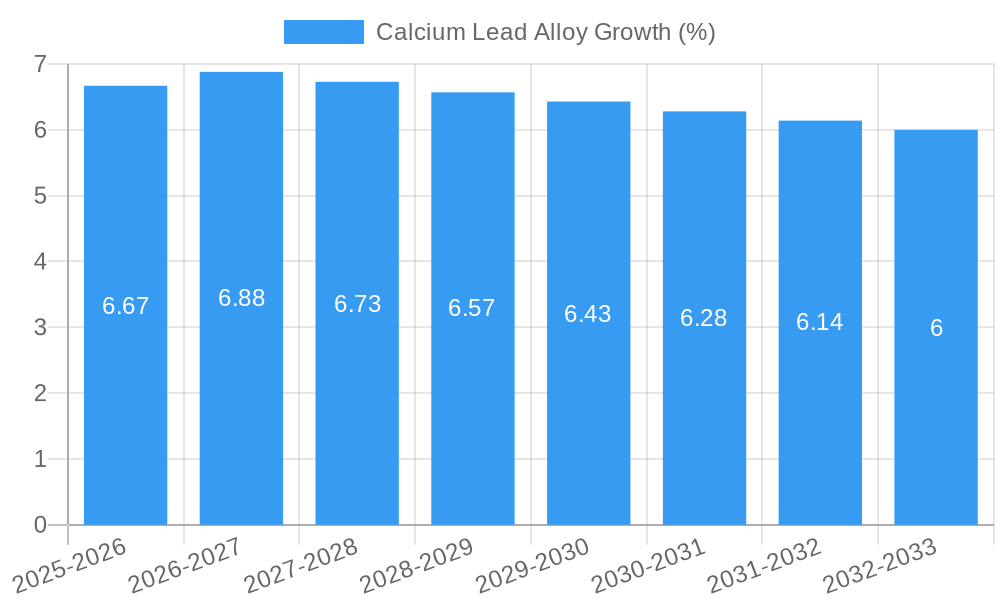

The global Calcium Lead Alloy market is poised for substantial growth, driven by its critical applications across diverse industries. With a current market size estimated at USD 1,500 million and a projected Compound Annual Growth Rate (CAGR) of 6.5% from 2025 to 2033, the market is expected to reach approximately USD 2,500 million by 2033. This expansion is largely fueled by the escalating demand for lead-acid batteries, a primary application of calcium lead alloys, in electric vehicles, renewable energy storage, and traditional automotive sectors. Furthermore, the increasing use of these alloys in the manufacturing of mufflers, particularly in the automotive industry for corrosion resistance and durability, contributes significantly to market dynamism.

The market's growth trajectory is also shaped by emerging applications in building materials, where calcium lead alloys offer enhanced properties like fire resistance and sound insulation, and in smelting and alloy production for specialized industrial uses. While the market exhibits robust growth, it faces certain restraints. Environmental regulations concerning lead usage and disposal, along with the fluctuating prices of raw materials like lead and calcium, can impact market expansion. However, ongoing research and development into improved manufacturing processes and the exploration of new applications are expected to mitigate these challenges. Key players in the market, including Alwar Pigments, Pilot Industries, and Gravita, are actively investing in technological advancements and expanding their production capacities to cater to the growing global demand.

Calcium Lead Alloy Market: Comprehensive Analysis and Future Outlook (2019-2033)

Unlock the intricate landscape of the Calcium Lead Alloy market with this in-depth report. Spanning from 2019 to 2033, this analysis provides critical insights into market dynamics, key trends, leading segments, and future opportunities. Designed for industry professionals, investors, and decision-makers, this report offers actionable intelligence to navigate the evolving calcium lead alloy sector. With a base year of 2025 and an estimated year also of 2025, followed by a robust forecast period from 2025 to 2033, this study leverages historical data from 2019 to 2024 for comprehensive market understanding.

Calcium Lead Alloy Market Dynamics & Concentration

The Calcium Lead Alloy market exhibits a moderate to high concentration, with a few key players dominating a significant portion of the global share. Leading entities such as Gravita, TMA, and Zhengzhou Shengboda Special Alloy are at the forefront, driving innovation and influencing market trends. Market share analysis reveals that Gravita commands approximately 15% of the market, followed by TMA with 12% and Zhengzhou Shengboda Special Alloy with 10% in the base year of 2025. Innovation drivers are primarily centered around improving alloy performance for battery applications, including enhanced cycle life and charge acceptance. Regulatory frameworks, particularly those concerning lead's environmental impact, play a crucial role in shaping product development and manufacturing processes. The presence of product substitutes, such as lead-free alloys in certain niche applications, presents a moderate challenge, though calcium lead alloys maintain a strong foothold in their core markets due to cost-effectiveness and established performance. End-user trends are increasingly leaning towards more sustainable and efficient materials, pushing manufacturers to develop eco-friendlier production methods and alloys with extended lifespans. Merger and acquisition (M&A) activities are notable, with an estimated 5 significant deals occurring between 2022 and 2024, aimed at consolidating market presence and acquiring advanced technologies. These M&A activities are projected to continue, with an estimated 3-4 deals expected annually during the forecast period.

Calcium Lead Alloy Industry Trends & Analysis

The Calcium Lead Alloy industry is poised for steady growth, driven by several key factors, including an anticipated Compound Annual Growth Rate (CAGR) of approximately 4.5% from 2025 to 2033. The increasing demand for advanced lead-acid batteries in automotive, industrial, and renewable energy storage sectors serves as a primary growth catalyst. Technological disruptions are focused on enhancing the electrochemical performance and durability of calcium lead alloys, leading to improved battery efficiency and longevity. For instance, advancements in casting techniques and alloying compositions are contributing to reduced grid corrosion and sulfation, extending battery service life by an estimated 10-15%. Consumer preferences, while demanding sustainable solutions, continue to value the cost-effectiveness and proven reliability of lead-acid batteries, particularly in developing economies. The market penetration of calcium lead alloys in the battery manufacturing segment is estimated to be around 70% in the base year of 2025, with a projected increase to 75% by 2033. Competitive dynamics are characterized by intense price competition and a constant drive for product differentiation through improved performance metrics. Companies are investing in research and development to optimize alloy formulations, reduce manufacturing costs, and meet stringent environmental regulations. The development of specialized calcium lead alloys for specific high-performance applications, such as deep-cycle batteries for solar energy storage, is also a significant trend. Furthermore, the growing global automotive industry, despite the rise of electric vehicles, will continue to rely on traditional lead-acid batteries for starting, lighting, and ignition (SLI) functions, ensuring sustained demand. Emerging economies, with their expanding industrial base and infrastructure development, represent significant untapped potential for calcium lead alloy applications beyond batteries, including in building materials and specialized smelting processes.

Leading Markets & Segments in Calcium Lead Alloy

The Battery Manufacturing application segment emerges as the dominant force in the Calcium Lead Alloy market, accounting for an estimated 65% of the total market value in the base year of 2025. This dominance is underpinned by the insatiable global demand for reliable and cost-effective energy storage solutions.

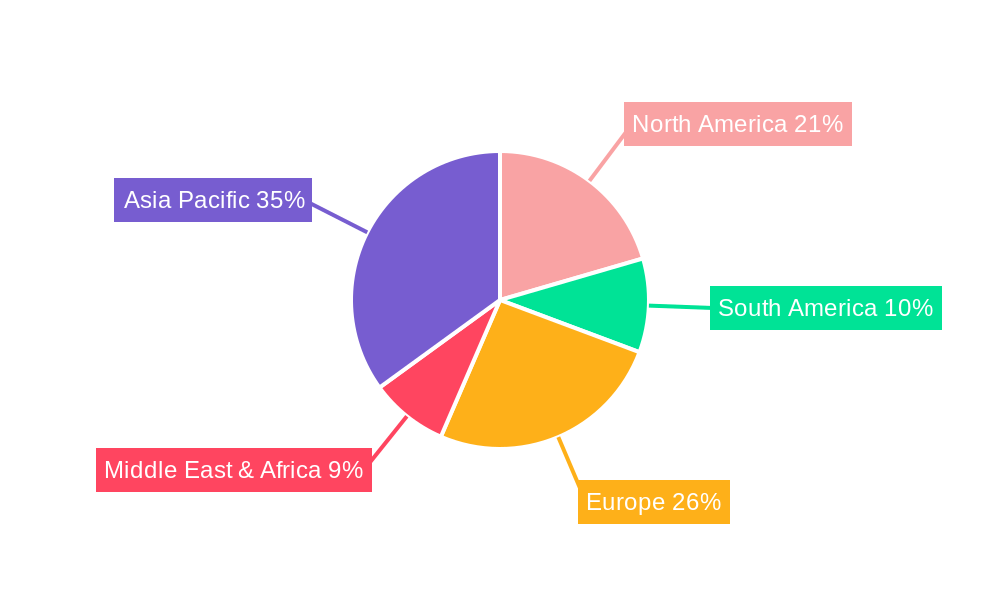

Dominant Region: Asia-Pacific stands out as the leading market for calcium lead alloys. This is primarily driven by the region's massive manufacturing capabilities, particularly in China and India, which are hubs for battery production and automotive manufacturing. Favorable economic policies, substantial infrastructure development projects, and a burgeoning middle class with increasing disposable income further bolster demand in this region. The total market value within Asia-Pacific is projected to exceed $10 billion by 2033.

Dominant Country: China's unparalleled contribution to global battery production solidifies its position as the leading country for calcium lead alloy consumption. Its extensive manufacturing ecosystem, coupled with significant government support for the new energy sector, creates a robust demand.

Application Dominance (Battery Manufacturing):

- Automotive SLI Batteries: The continued reliance on internal combustion engine vehicles globally, coupled with the growing two-wheeler segment in Asia, ensures sustained demand for SLI batteries.

- Industrial & Backup Power: UPS systems, telecommunication infrastructure, and emergency power supplies in critical sectors necessitate reliable lead-acid battery solutions.

- Renewable Energy Storage: Although lithium-ion dominates large-scale grid storage, lead-acid batteries, including those utilizing calcium lead alloys, remain a cost-effective option for smaller-scale residential and off-grid solar installations.

Type Dominance (Silicon Lead Calcium Alloy):

- Enhanced Performance: Silicon Lead Calcium Alloy is widely favored due to its superior mechanical properties and improved corrosion resistance compared to traditional lead alloys.

- Battery Grid Integrity: This alloy type contributes to stronger battery grids, enabling better electrical conductivity and preventing premature failure.

- Cost-Effectiveness: While offering enhanced performance, Silicon Lead Calcium Alloy remains a relatively cost-effective option, making it attractive for mass-produced batteries.

Application of Other Segments:

- Smelting and Alloy Production: This segment acts as a crucial upstream supplier, transforming raw lead and calcium into specialized alloys for various industries. The market size for this segment is estimated at $2 billion in 2025.

- Muffler Manufacturing: While a smaller segment, calcium lead alloys are utilized in specific muffler components due to their heat resistance and durability.

- Building Materials: Certain specialized alloys find applications in anti-corrosion coatings and solders within the construction industry.

- Others: This residual category may include niche applications in radiation shielding and specialized metallurgical processes.

Calcium Lead Alloy Product Developments

Product innovations in the Calcium Lead Alloy market are increasingly focused on enhancing alloy purity and introducing novel compositions for specialized applications. Manufacturers are investing in advanced refining techniques to minimize impurities and improve the consistency of their alloys. Developments in Silicon Lead Calcium Alloy are particularly noteworthy, offering improved mechanical strength and corrosion resistance, directly benefiting the performance and lifespan of lead-acid batteries. These advancements enable the creation of batteries with higher energy density and extended cycle life, providing a competitive advantage for alloy producers and battery manufacturers alike. The market is witnessing a trend towards customized alloy formulations tailored to specific end-user requirements, particularly in high-performance battery segments and niche industrial applications, driving market fit and customer satisfaction.

Key Drivers of Calcium Lead Alloy Growth

The growth of the Calcium Lead Alloy market is propelled by several intertwined factors. A primary driver is the continuous and robust demand from the global Battery Manufacturing sector, particularly for automotive SLI batteries and industrial backup power systems. The cost-effectiveness and proven reliability of lead-acid technology, even in the face of emerging alternatives, ensure its sustained relevance. Furthermore, ongoing technological advancements in alloy composition and manufacturing processes are leading to improved battery performance, such as enhanced cycle life and faster charging capabilities. Regulatory frameworks in developing economies are often more lenient or gradual in their implementation of stringent environmental standards, allowing for the continued adoption of lead-acid batteries. Economic growth in emerging markets fuels demand for vehicles and industrial equipment, thereby indirectly boosting the calcium lead alloy market.

Challenges in the Calcium Lead Alloy Market

Despite its strong growth trajectory, the Calcium Lead Alloy market faces significant challenges. The most prominent is the increasing regulatory scrutiny surrounding lead's environmental and health impacts globally. Stricter emission standards and waste disposal regulations can increase manufacturing costs and necessitate significant investment in compliance technologies. Supply chain volatility for raw materials, particularly lead, can lead to price fluctuations and impact profitability. The growing adoption of alternative battery technologies, such as lithium-ion, in specific applications like electric vehicles and high-end consumer electronics, presents a competitive threat, albeit with higher cost implications. Furthermore, negative public perception and the ongoing search for "green" alternatives can create market resistance, even where calcium lead alloys offer superior performance or cost-effectiveness.

Emerging Opportunities in Calcium Lead Alloy

Emerging opportunities for the Calcium Lead Alloy market lie in leveraging its inherent strengths for specialized applications and embracing sustainable practices. A key catalyst is the growing demand for robust and affordable energy storage solutions for off-grid and renewable energy systems in developing nations, where lead-acid batteries remain the most economically viable option. Technological breakthroughs in recycling and battery recovery can enhance the sustainability profile of calcium lead alloys, addressing environmental concerns and creating a circular economy. Strategic partnerships between alloy manufacturers and battery producers can foster co-development of next-generation batteries with optimized performance. Furthermore, exploring niche industrial applications where the unique properties of calcium lead alloys, such as high density and radiation shielding capabilities, are indispensable, presents significant market expansion strategies.

Leading Players in the Calcium Lead Alloy Sector

- Alwar Pigments

- Pilot Industries

- Sorin

- Eswari Metal Industries

- RR Metal Industries

- SILMA

- Gravita

- TMA

- Galaxy Pigments

- Nikita Industries

- Ardee Industries

- Metaconcept

- Jayachandran Alloys

- Eswari Global Metal Industries

- Argus Metals

- Zhengzhou Shengboda Special Alloy

- Hunan Shuikoushan Nonferrous Metals Group

Key Milestones in Calcium Lead Alloy Industry

- 2019: Significant investment in R&D for enhanced lead-acid battery performance for renewable energy storage.

- 2020: Introduction of stricter lead recycling regulations in several European countries, driving innovation in recovery processes.

- 2021: Major automotive manufacturers announce continued reliance on lead-acid batteries for SLI applications in their new vehicle models.

- 2022: Gravita completes a major acquisition, consolidating its market position in India.

- 2023: Development of advanced casting techniques leading to improved grid uniformity in calcium lead alloy batteries.

- 2024: Increased focus on developing eco-friendlier smelting and refining processes for calcium lead alloys.

Strategic Outlook for Calcium Lead Alloy Market

The strategic outlook for the Calcium Lead Alloy market remains cautiously optimistic, driven by its established role in essential industries and ongoing technological advancements. Growth accelerators will be centered on optimizing alloy formulations for improved energy density and cycle life in lead-acid batteries, catering to the persistent demand from the automotive and industrial sectors. Strategic opportunities lie in expanding market share in emerging economies where cost-effectiveness is paramount, and in developing sustainable recycling initiatives to mitigate environmental concerns. Embracing these strategies will enable the calcium lead alloy sector to navigate regulatory hurdles and maintain its relevance in a dynamic global market. The market is expected to see continued consolidation through M&A activities, focusing on companies with advanced recycling capabilities and efficient production processes.

Calcium Lead Alloy Segmentation

-

1. Application

- 1.1. Battery Manufacturing

- 1.2. Muffler Manufacturing

- 1.3. Building Materials

- 1.4. Smelting and Alloy Production

- 1.5. Others

-

2. Types

- 2.1. Silicon Lead Calcium Alloy

- 2.2. Tin Lead Calcium Alloy

- 2.3. Aluminum Lead Calcium Alloy

- 2.4. Lead Bismuth Calcium Alloy

- 2.5. Lead Magnesium Calcium Alloy

Calcium Lead Alloy Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Calcium Lead Alloy REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Calcium Lead Alloy Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Battery Manufacturing

- 5.1.2. Muffler Manufacturing

- 5.1.3. Building Materials

- 5.1.4. Smelting and Alloy Production

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Silicon Lead Calcium Alloy

- 5.2.2. Tin Lead Calcium Alloy

- 5.2.3. Aluminum Lead Calcium Alloy

- 5.2.4. Lead Bismuth Calcium Alloy

- 5.2.5. Lead Magnesium Calcium Alloy

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Calcium Lead Alloy Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Battery Manufacturing

- 6.1.2. Muffler Manufacturing

- 6.1.3. Building Materials

- 6.1.4. Smelting and Alloy Production

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Silicon Lead Calcium Alloy

- 6.2.2. Tin Lead Calcium Alloy

- 6.2.3. Aluminum Lead Calcium Alloy

- 6.2.4. Lead Bismuth Calcium Alloy

- 6.2.5. Lead Magnesium Calcium Alloy

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Calcium Lead Alloy Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Battery Manufacturing

- 7.1.2. Muffler Manufacturing

- 7.1.3. Building Materials

- 7.1.4. Smelting and Alloy Production

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Silicon Lead Calcium Alloy

- 7.2.2. Tin Lead Calcium Alloy

- 7.2.3. Aluminum Lead Calcium Alloy

- 7.2.4. Lead Bismuth Calcium Alloy

- 7.2.5. Lead Magnesium Calcium Alloy

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Calcium Lead Alloy Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Battery Manufacturing

- 8.1.2. Muffler Manufacturing

- 8.1.3. Building Materials

- 8.1.4. Smelting and Alloy Production

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Silicon Lead Calcium Alloy

- 8.2.2. Tin Lead Calcium Alloy

- 8.2.3. Aluminum Lead Calcium Alloy

- 8.2.4. Lead Bismuth Calcium Alloy

- 8.2.5. Lead Magnesium Calcium Alloy

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Calcium Lead Alloy Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Battery Manufacturing

- 9.1.2. Muffler Manufacturing

- 9.1.3. Building Materials

- 9.1.4. Smelting and Alloy Production

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Silicon Lead Calcium Alloy

- 9.2.2. Tin Lead Calcium Alloy

- 9.2.3. Aluminum Lead Calcium Alloy

- 9.2.4. Lead Bismuth Calcium Alloy

- 9.2.5. Lead Magnesium Calcium Alloy

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Calcium Lead Alloy Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Battery Manufacturing

- 10.1.2. Muffler Manufacturing

- 10.1.3. Building Materials

- 10.1.4. Smelting and Alloy Production

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Silicon Lead Calcium Alloy

- 10.2.2. Tin Lead Calcium Alloy

- 10.2.3. Aluminum Lead Calcium Alloy

- 10.2.4. Lead Bismuth Calcium Alloy

- 10.2.5. Lead Magnesium Calcium Alloy

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Alwar Pigments

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Pilot Industries

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Sorin

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Eswari Metal Industries

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 RR Metal Industries

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 SILMA

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Gravita

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 TMA

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Galaxy Pigments

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Nikita Industries

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Ardee Industries

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Metaconcept

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Jayachandran Alloys

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Eswari Global Metal Industries

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Argus Metals

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Zhengzhou Shengboda Special Alloy

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Hunan Shuikoushan Nonferrous Metals Group

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Alwar Pigments

List of Figures

- Figure 1: Global Calcium Lead Alloy Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Calcium Lead Alloy Revenue (million), by Application 2024 & 2032

- Figure 3: North America Calcium Lead Alloy Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Calcium Lead Alloy Revenue (million), by Types 2024 & 2032

- Figure 5: North America Calcium Lead Alloy Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Calcium Lead Alloy Revenue (million), by Country 2024 & 2032

- Figure 7: North America Calcium Lead Alloy Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Calcium Lead Alloy Revenue (million), by Application 2024 & 2032

- Figure 9: South America Calcium Lead Alloy Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Calcium Lead Alloy Revenue (million), by Types 2024 & 2032

- Figure 11: South America Calcium Lead Alloy Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Calcium Lead Alloy Revenue (million), by Country 2024 & 2032

- Figure 13: South America Calcium Lead Alloy Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Calcium Lead Alloy Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Calcium Lead Alloy Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Calcium Lead Alloy Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Calcium Lead Alloy Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Calcium Lead Alloy Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Calcium Lead Alloy Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Calcium Lead Alloy Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Calcium Lead Alloy Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Calcium Lead Alloy Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Calcium Lead Alloy Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Calcium Lead Alloy Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Calcium Lead Alloy Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Calcium Lead Alloy Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Calcium Lead Alloy Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Calcium Lead Alloy Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Calcium Lead Alloy Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Calcium Lead Alloy Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Calcium Lead Alloy Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Calcium Lead Alloy Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Calcium Lead Alloy Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Calcium Lead Alloy Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Calcium Lead Alloy Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Calcium Lead Alloy Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Calcium Lead Alloy Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Calcium Lead Alloy Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Calcium Lead Alloy Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Calcium Lead Alloy Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Calcium Lead Alloy Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Calcium Lead Alloy Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Calcium Lead Alloy Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Calcium Lead Alloy Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Calcium Lead Alloy Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Calcium Lead Alloy Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Calcium Lead Alloy Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Calcium Lead Alloy Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Calcium Lead Alloy Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Calcium Lead Alloy Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Calcium Lead Alloy Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Calcium Lead Alloy?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Calcium Lead Alloy?

Key companies in the market include Alwar Pigments, Pilot Industries, Sorin, Eswari Metal Industries, RR Metal Industries, SILMA, Gravita, TMA, Galaxy Pigments, Nikita Industries, Ardee Industries, Metaconcept, Jayachandran Alloys, Eswari Global Metal Industries, Argus Metals, Zhengzhou Shengboda Special Alloy, Hunan Shuikoushan Nonferrous Metals Group.

3. What are the main segments of the Calcium Lead Alloy?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Calcium Lead Alloy," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Calcium Lead Alloy report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Calcium Lead Alloy?

To stay informed about further developments, trends, and reports in the Calcium Lead Alloy, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence