Key Insights

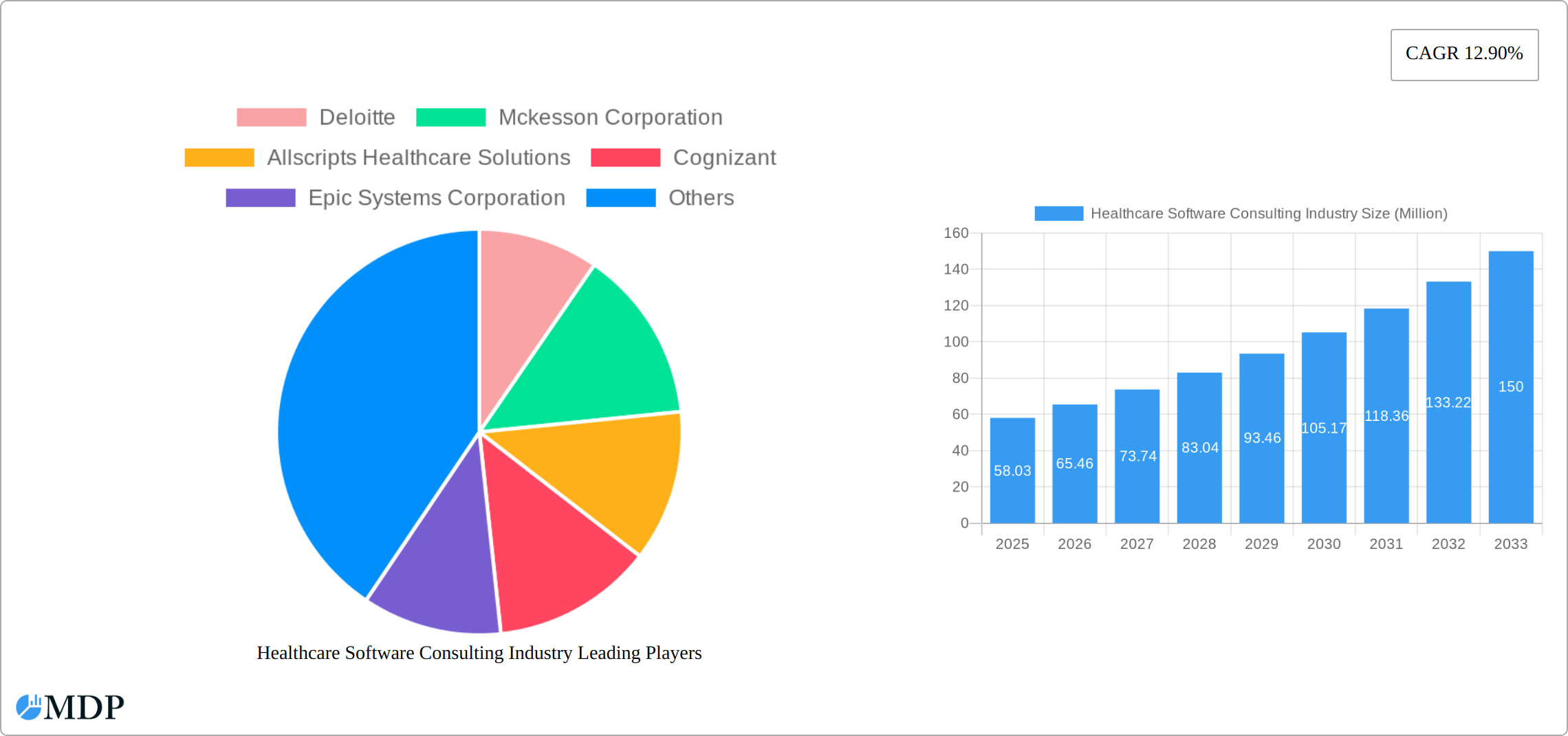

The global healthcare software consulting market, valued at $58.03 million in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 12.90% from 2025 to 2033. This expansion is driven by several key factors. The increasing adoption of electronic health records (EHRs) and other healthcare IT systems necessitates expert consulting services for successful implementation, integration, and optimization. Furthermore, the rising demand for improved healthcare data analytics and business process management, coupled with stringent regulatory compliance requirements (like HIPAA), fuels the need for specialized healthcare software consulting expertise. The market's segmentation reveals significant opportunities across various consulting types, including change management, integration and migration, security set-up and risk assessment, and enterprise reporting and data analytics. Hospitals and ambulatory care centers represent the largest end-user segment, followed by diagnostic and imaging centers and public and private payers. Key players like Deloitte, McKesson, Allscripts, and IBM are leveraging their established presence and expertise to capitalize on this growth. Geographical distribution reveals strong market presence in North America and Europe, with emerging markets in Asia Pacific showing significant potential for future expansion.

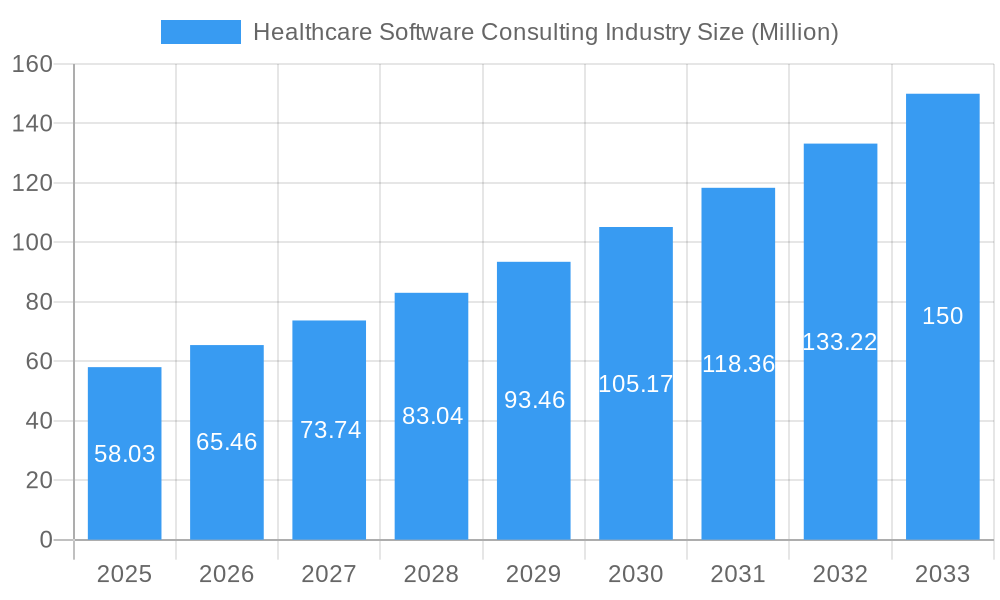

Healthcare Software Consulting Industry Market Size (In Million)

The market's future trajectory is influenced by several trends. The increasing adoption of cloud-based solutions and artificial intelligence (AI) in healthcare is expected to create new avenues for consulting services. However, challenges remain, including the high cost of implementation, the complexity of integrating legacy systems, and the shortage of skilled healthcare IT professionals. Addressing these challenges requires a strategic approach that balances technological advancements with pragmatic implementation strategies. The sustained growth in the global healthcare sector, however, ensures a positive outlook for the healthcare software consulting market in the foreseeable future. Continued investment in healthcare infrastructure and technological upgrades will continue to drive demand for consulting services, offering substantial opportunities for both established players and emerging firms.

Healthcare Software Consulting Industry Company Market Share

Healthcare Software Consulting Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Healthcare Software Consulting industry, projecting a market value of $XX Million by 2033. The study covers the period from 2019 to 2033, with 2025 serving as the base and estimated year. This report is invaluable for industry stakeholders, investors, and strategic decision-makers seeking actionable insights into this rapidly evolving market. The report meticulously examines market dynamics, leading players, emerging trends, and future growth opportunities.

Healthcare Software Consulting Industry Market Dynamics & Concentration

The global Healthcare Software Consulting market is characterized by a dynamic and moderately concentrated landscape, featuring established global leaders alongside specialized niche players. Key contributors such as Deloitte, McKesson Corporation, Allscripts Healthcare Solutions, Cognizant, Epic Systems Corporation, IBM Corporation, Accenture, Cerner Corporation, Siemens Healthineers, and Genpact Limited continue to hold significant influence. The market's robust growth trajectory is underpinned by the escalating adoption of electronic health records (EHRs) and electronic medical records (EMRs), the critical need for advanced data analytics to derive actionable insights from healthcare data, and the imperative to navigate complex and evolving regulatory compliance requirements. Innovation is a pivotal force, driven by breakthroughs in artificial intelligence (AI) for predictive diagnostics and patient risk stratification, machine learning (ML) for optimizing operational efficiencies and treatment pathways, and cloud computing for scalable, secure, and accessible healthcare solutions. This technological evolution fuels the development of sophisticated, value-added consulting services. The industry actively engages in mergers and acquisitions (M&A), with a notable volume of strategic consolidations and expansions occurring. These activities aim to broaden service portfolios, enhance technological capabilities, and extend market reach. The competitive intensity is reflected in the market share distribution among the leading entities. Adherence to stringent regulatory frameworks, including HIPAA in the United States and GDPR in Europe, alongside various regional data privacy and security mandates, fundamentally shapes market operations and drives significant demand for specialized consulting expertise in ensuring compliance. The burgeoning emergence of telehealth platforms and remote patient monitoring technologies presents both transformative opportunities for improved patient access and continuous care, as well as intricate challenges that necessitate agile and forward-thinking consulting strategies. While potential product substitutes, such as robust in-house IT departments and adaptable open-source solutions, exist, the deep domain expertise, strategic guidance, and proven implementation capabilities offered by dedicated consulting firms remain indispensable differentiators. Consequently, end-user trends strongly favor the outsourcing of complex IT projects and strategic initiatives, driven by the pursuit of cost-effectiveness, accelerated project timelines, and access to specialized, in-demand skillsets.

- Market Concentration: Moderately concentrated, with a prominent presence of major global consulting firms and specialized providers, reflecting a competitive yet structured market.

- M&A Activity: Ongoing mergers, acquisitions, and strategic partnerships are a hallmark of the industry, fostering consolidation and the expansion of comprehensive service offerings.

- Key Innovation Drivers: Artificial Intelligence (AI), Machine Learning (ML), Cloud Computing, data analytics, and blockchain technology are spearheading advancements in healthcare software and consulting services.

- Regulatory Frameworks: Strict adherence to and expert guidance on regulations such as HIPAA, GDPR, and other global and regional data privacy and security laws are critical market enablers.

Healthcare Software Consulting Industry Industry Trends & Analysis

The Healthcare Software Consulting industry is experiencing robust growth, with a projected Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025-2033). This growth is fueled by several key factors. The increasing volume and complexity of healthcare data necessitate advanced analytics and reporting capabilities, driving demand for specialized consulting services. Technological disruptions, such as the widespread adoption of cloud-based solutions and the integration of AI/ML in healthcare systems, are reshaping the industry landscape. Consumer preferences are shifting towards personalized and patient-centric healthcare experiences, necessitating improvements in software usability and interoperability. Competitive dynamics are characterized by both collaboration and competition, with firms forming strategic alliances and engaging in M&A activities to expand their market presence and service portfolio. Market penetration of cloud-based healthcare software solutions is estimated to reach XX% by 2033. This trend significantly impacts the demand for consulting services related to cloud migration, integration, and security.

Leading Markets & Segments in Healthcare Software Consulting Industry

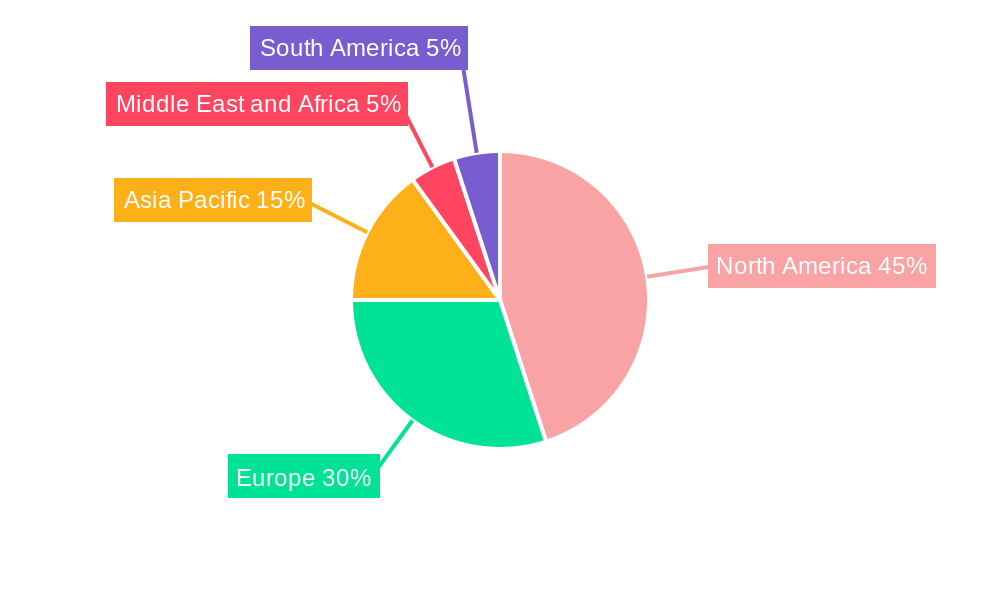

The North American region currently dominates the Healthcare Software Consulting market, driven by factors such as advanced healthcare infrastructure, high technology adoption rates, and stringent regulatory compliance requirements. Within the consulting services segment, HCIT Integration and Migration and Healthcare/Medical System Security Set-Up and Risk Assessment are experiencing the highest growth, driven by the increasing complexity of healthcare IT systems and rising cybersecurity threats. In terms of end-users, Hospitals and Ambulatory Care Centers constitute the largest segment, followed by Diagnostic and Imaging Centers.

- Key Drivers in North America:

- Advanced healthcare infrastructure

- High technology adoption rates

- Stringent regulatory compliance requirements (HIPAA)

- Fastest-Growing Segments:

- HCIT Integration and Migration

- Healthcare/Medical System Security Set-Up and Risk Assessment

- Largest End-User Segment: Hospitals and Ambulatory Care Centers

Healthcare Software Consulting Industry Product Developments

Recent product and service innovations within the Healthcare Software Consulting industry are heavily influenced by cutting-edge technologies aimed at revolutionizing patient care, operational efficiency, and data integrity. A significant focus is placed on AI-powered solutions that enable predictive analytics for disease outbreaks and individual patient risk assessment, sophisticated data security measures to safeguard sensitive health information, and intelligent workflow management systems designed to streamline clinical and administrative processes. These advancements are instrumental in boosting operational efficiency, significantly reducing healthcare expenditures, and ultimately elevating the quality and outcomes of patient care. Consulting firms are differentiating themselves through specialized expertise in niche healthcare domains (e.g., genomics, personalized medicine, medical imaging), fostering strategic alliances with leading technology vendors to integrate best-in-class solutions, and demonstrating a robust portfolio of successful project implementations that deliver tangible value to clients. The integration of blockchain technology is rapidly emerging as a pivotal trend, offering promising applications for enhancing data security, ensuring immutable audit trails, and fostering seamless interoperability across disparate healthcare systems.

Key Drivers of Healthcare Software Consulting Growth

The Healthcare Software Consulting market's growth is propelled by several factors. Technological advancements, particularly in AI, ML, and cloud computing, are driving innovation and creating new opportunities. Increasing government regulations related to data privacy and security are creating a demand for specialized consulting services. The rising adoption of telehealth and remote patient monitoring solutions necessitates robust IT infrastructure and skilled consulting support. Economic factors, such as increasing healthcare spending and the push for cost-effectiveness, also contribute to the market's expansion.

Challenges in the Healthcare Software Consulting Industry Market

The industry faces significant challenges including regulatory complexities and compliance costs, which can hinder market entry and operational efficiency. Supply chain disruptions and talent shortages in specialized skills (e.g., cybersecurity, data analytics) can impact project delivery timelines and overall profitability. Intense competition, both from established players and new entrants, puts pressure on pricing and margins. These factors collectively contribute to approximately XX% reduction in projected profitability for smaller firms.

Emerging Opportunities in Healthcare Software Consulting Industry

The long-term growth of the Healthcare Software Consulting industry is fueled by emerging opportunities in areas like precision medicine, genomics, and personalized healthcare. Strategic partnerships between consulting firms and technology vendors can lead to innovative solutions that address unmet healthcare needs. Expansion into new geographical markets, particularly in developing economies, presents significant growth potential. The integration of advanced technologies, such as blockchain and IoT, offers further opportunities for innovation and value creation.

Leading Players in the Healthcare Software Consulting Industry Sector

Key Milestones in Healthcare Software Consulting Industry Industry

- 2020: Increased adoption of telehealth solutions due to the COVID-19 pandemic.

- 2021: Significant investments in AI and ML-based healthcare solutions by major players.

- 2022: Several large M&A deals consolidating market share.

- 2023: Launch of several new cloud-based healthcare platforms.

- 2024: Growing emphasis on data security and compliance.

Strategic Outlook for Healthcare Software Consulting Market

The Healthcare Software Consulting market is poised for continued growth, driven by technological advancements, increasing healthcare spending, and the growing need for efficient and secure healthcare IT solutions. Strategic opportunities lie in specializing in niche areas, such as AI-powered diagnostics, cybersecurity for healthcare systems, and blockchain-based data management. Companies that can adapt to emerging technologies and effectively address the challenges of regulatory compliance and talent acquisition will be best positioned for success in this dynamic market. The market's long-term potential is significant, with projections indicating substantial growth in the coming decade.

Healthcare Software Consulting Industry Segmentation

-

1. Consulting Type

- 1.1. HCIT Change Management

- 1.2. Healthcare Business Process Management

- 1.3. HCIT Integration and Migration

- 1.4. Healthca

- 1.5. Healthcare Enterprise Reporting and Data Analytics

- 1.6. Other Consulting Types

-

2. End User

- 2.1. Hospitals and Ambulatory Care Centers

- 2.2. Diagnostic and Imaging Centers

- 2.3. Public and Private Payers

- 2.4. Other End Users

Healthcare Software Consulting Industry Segmentation By Geography

-

1. North America

- 1.1. US

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. UK

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Healthcare Software Consulting Industry Regional Market Share

Geographic Coverage of Healthcare Software Consulting Industry

Healthcare Software Consulting Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.90% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Consulting Type

- 5.1.1. HCIT Change Management

- 5.1.2. Healthcare Business Process Management

- 5.1.3. HCIT Integration and Migration

- 5.1.4. Healthca

- 5.1.5. Healthcare Enterprise Reporting and Data Analytics

- 5.1.6. Other Consulting Types

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Hospitals and Ambulatory Care Centers

- 5.2.2. Diagnostic and Imaging Centers

- 5.2.3. Public and Private Payers

- 5.2.4. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Consulting Type

- 6. Global Healthcare Software Consulting Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Consulting Type

- 6.1.1. HCIT Change Management

- 6.1.2. Healthcare Business Process Management

- 6.1.3. HCIT Integration and Migration

- 6.1.4. Healthca

- 6.1.5. Healthcare Enterprise Reporting and Data Analytics

- 6.1.6. Other Consulting Types

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Hospitals and Ambulatory Care Centers

- 6.2.2. Diagnostic and Imaging Centers

- 6.2.3. Public and Private Payers

- 6.2.4. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Consulting Type

- 7. North America Healthcare Software Consulting Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Consulting Type

- 7.1.1. HCIT Change Management

- 7.1.2. Healthcare Business Process Management

- 7.1.3. HCIT Integration and Migration

- 7.1.4. Healthca

- 7.1.5. Healthcare Enterprise Reporting and Data Analytics

- 7.1.6. Other Consulting Types

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Hospitals and Ambulatory Care Centers

- 7.2.2. Diagnostic and Imaging Centers

- 7.2.3. Public and Private Payers

- 7.2.4. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Consulting Type

- 8. Europe Healthcare Software Consulting Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Consulting Type

- 8.1.1. HCIT Change Management

- 8.1.2. Healthcare Business Process Management

- 8.1.3. HCIT Integration and Migration

- 8.1.4. Healthca

- 8.1.5. Healthcare Enterprise Reporting and Data Analytics

- 8.1.6. Other Consulting Types

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Hospitals and Ambulatory Care Centers

- 8.2.2. Diagnostic and Imaging Centers

- 8.2.3. Public and Private Payers

- 8.2.4. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Consulting Type

- 9. Asia Pacific Healthcare Software Consulting Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Consulting Type

- 9.1.1. HCIT Change Management

- 9.1.2. Healthcare Business Process Management

- 9.1.3. HCIT Integration and Migration

- 9.1.4. Healthca

- 9.1.5. Healthcare Enterprise Reporting and Data Analytics

- 9.1.6. Other Consulting Types

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Hospitals and Ambulatory Care Centers

- 9.2.2. Diagnostic and Imaging Centers

- 9.2.3. Public and Private Payers

- 9.2.4. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Consulting Type

- 10. Middle East and Africa Healthcare Software Consulting Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Consulting Type

- 10.1.1. HCIT Change Management

- 10.1.2. Healthcare Business Process Management

- 10.1.3. HCIT Integration and Migration

- 10.1.4. Healthca

- 10.1.5. Healthcare Enterprise Reporting and Data Analytics

- 10.1.6. Other Consulting Types

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Hospitals and Ambulatory Care Centers

- 10.2.2. Diagnostic and Imaging Centers

- 10.2.3. Public and Private Payers

- 10.2.4. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Consulting Type

- 11. South America Healthcare Software Consulting Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Consulting Type

- 11.1.1. HCIT Change Management

- 11.1.2. Healthcare Business Process Management

- 11.1.3. HCIT Integration and Migration

- 11.1.4. Healthca

- 11.1.5. Healthcare Enterprise Reporting and Data Analytics

- 11.1.6. Other Consulting Types

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Hospitals and Ambulatory Care Centers

- 11.2.2. Diagnostic and Imaging Centers

- 11.2.3. Public and Private Payers

- 11.2.4. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Consulting Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Deloitte

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Mckesson Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Allscripts Healthcare Solutions

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Cognizant

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Epic Systems Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 IBM Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Accenture

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Cerner Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Siemens Healthineers*List Not Exhaustive

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Genpact Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Deloitte

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Healthcare Software Consulting Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Healthcare Software Consulting Industry Revenue (Million), by Consulting Type 2025 & 2033

- Figure 3: North America Healthcare Software Consulting Industry Revenue Share (%), by Consulting Type 2025 & 2033

- Figure 4: North America Healthcare Software Consulting Industry Revenue (Million), by End User 2025 & 2033

- Figure 5: North America Healthcare Software Consulting Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America Healthcare Software Consulting Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Healthcare Software Consulting Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Healthcare Software Consulting Industry Revenue (Million), by Consulting Type 2025 & 2033

- Figure 9: Europe Healthcare Software Consulting Industry Revenue Share (%), by Consulting Type 2025 & 2033

- Figure 10: Europe Healthcare Software Consulting Industry Revenue (Million), by End User 2025 & 2033

- Figure 11: Europe Healthcare Software Consulting Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: Europe Healthcare Software Consulting Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Healthcare Software Consulting Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Healthcare Software Consulting Industry Revenue (Million), by Consulting Type 2025 & 2033

- Figure 15: Asia Pacific Healthcare Software Consulting Industry Revenue Share (%), by Consulting Type 2025 & 2033

- Figure 16: Asia Pacific Healthcare Software Consulting Industry Revenue (Million), by End User 2025 & 2033

- Figure 17: Asia Pacific Healthcare Software Consulting Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Asia Pacific Healthcare Software Consulting Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Healthcare Software Consulting Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Healthcare Software Consulting Industry Revenue (Million), by Consulting Type 2025 & 2033

- Figure 21: Middle East and Africa Healthcare Software Consulting Industry Revenue Share (%), by Consulting Type 2025 & 2033

- Figure 22: Middle East and Africa Healthcare Software Consulting Industry Revenue (Million), by End User 2025 & 2033

- Figure 23: Middle East and Africa Healthcare Software Consulting Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Middle East and Africa Healthcare Software Consulting Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East and Africa Healthcare Software Consulting Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Healthcare Software Consulting Industry Revenue (Million), by Consulting Type 2025 & 2033

- Figure 27: South America Healthcare Software Consulting Industry Revenue Share (%), by Consulting Type 2025 & 2033

- Figure 28: South America Healthcare Software Consulting Industry Revenue (Million), by End User 2025 & 2033

- Figure 29: South America Healthcare Software Consulting Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: South America Healthcare Software Consulting Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: South America Healthcare Software Consulting Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Healthcare Software Consulting Industry Revenue Million Forecast, by Consulting Type 2020 & 2033

- Table 2: Global Healthcare Software Consulting Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 3: Global Healthcare Software Consulting Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Healthcare Software Consulting Industry Revenue Million Forecast, by Consulting Type 2020 & 2033

- Table 5: Global Healthcare Software Consulting Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: Global Healthcare Software Consulting Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: US Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Healthcare Software Consulting Industry Revenue Million Forecast, by Consulting Type 2020 & 2033

- Table 11: Global Healthcare Software Consulting Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 12: Global Healthcare Software Consulting Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Germany Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: UK Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Global Healthcare Software Consulting Industry Revenue Million Forecast, by Consulting Type 2020 & 2033

- Table 20: Global Healthcare Software Consulting Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 21: Global Healthcare Software Consulting Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 22: China Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Japan Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Australia Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: South Korea Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Healthcare Software Consulting Industry Revenue Million Forecast, by Consulting Type 2020 & 2033

- Table 29: Global Healthcare Software Consulting Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 30: Global Healthcare Software Consulting Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: GCC Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: South Africa Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Global Healthcare Software Consulting Industry Revenue Million Forecast, by Consulting Type 2020 & 2033

- Table 35: Global Healthcare Software Consulting Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 36: Global Healthcare Software Consulting Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 37: Brazil Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Argentina Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Healthcare Software Consulting Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Healthcare Software Consulting Industry?

The projected CAGR is approximately 12.90%.

2. Which companies are prominent players in the Healthcare Software Consulting Industry?

Key companies in the market include Deloitte, Mckesson Corporation, Allscripts Healthcare Solutions, Cognizant, Epic Systems Corporation, IBM Corporation, Accenture, Cerner Corporation, Siemens Healthineers*List Not Exhaustive, Genpact Limited.

3. What are the main segments of the Healthcare Software Consulting Industry?

The market segments include Consulting Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 58.03 Million as of 2022.

5. What are some drivers contributing to market growth?

Strict Government Regulations in the United States; Rising Need to Improve the Quality of Care and Reduce Healthcare Costs.

6. What are the notable trends driving market growth?

Hospitals and Ambulatory Care Centers Segment Dominates the Market.

7. Are there any restraints impacting market growth?

High Cost of Deployment.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Healthcare Software Consulting Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Healthcare Software Consulting Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Healthcare Software Consulting Industry?

To stay informed about further developments, trends, and reports in the Healthcare Software Consulting Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence