Key Insights

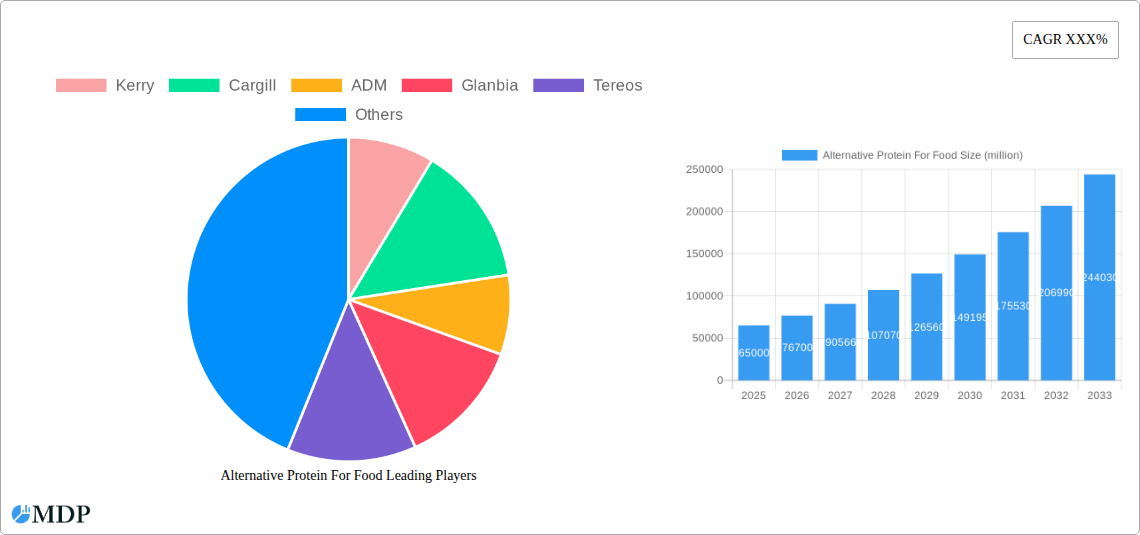

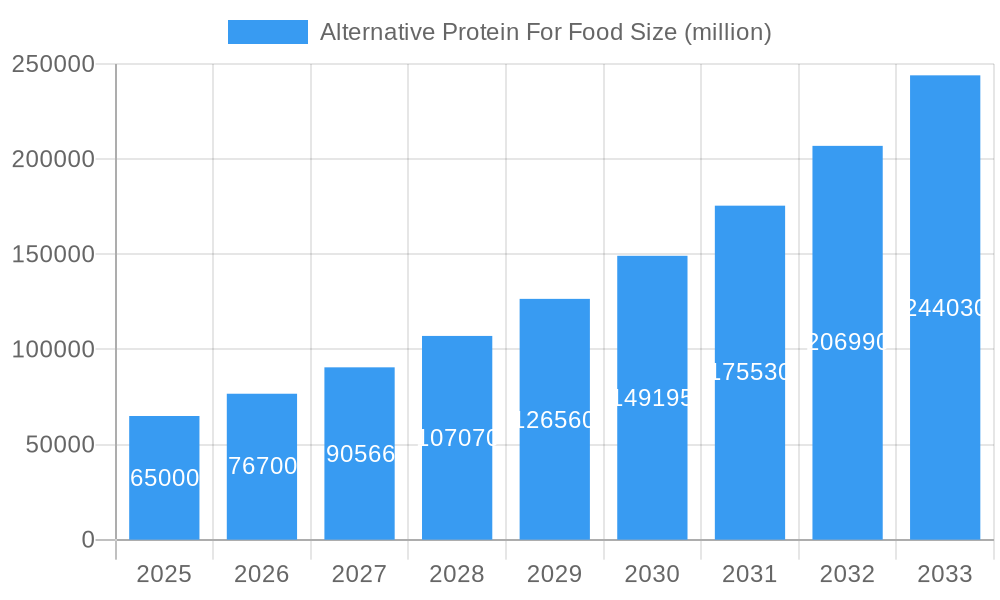

The global Alternative Protein for Food market is projected to witness substantial growth, estimated at approximately $65,000 million in 2025, with a robust Compound Annual Growth Rate (CAGR) of around 15-18% anticipated through 2033. This dynamic expansion is primarily driven by a confluence of factors including escalating consumer demand for healthier and more sustainable food options, increasing awareness of the environmental impact of traditional animal agriculture, and advancements in food technology enabling the development of palatable and nutritious plant-based and other alternative protein sources. Key applications span across various consumer segments, with "Patient" needs for specialized diets, "Religious Believers" adhering to specific dietary restrictions, and "Environmental Advocates" seeking sustainable choices forming significant demand drivers. The market is segmented by type into plant protein, algae protein, and others, with plant-based proteins currently dominating due to their wider availability and established consumer acceptance.

Alternative Protein For Food Market Size (In Billion)

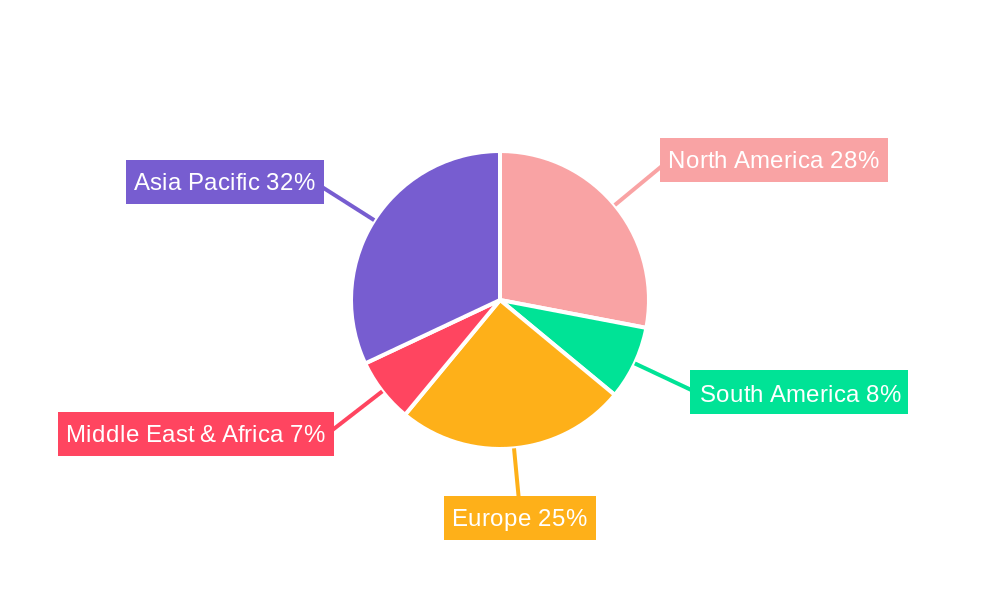

The market's upward trajectory is further supported by significant investments in research and development by leading companies such as Kerry, Cargill, ADM, and Glanbia, who are actively innovating to improve taste, texture, and nutritional profiles of alternative protein products. Emerging trends include the rise of cultivated meat and fermentation-derived proteins, promising to diversify the alternative protein landscape. However, the market faces certain restraints, including high production costs for some alternative protein types, regulatory hurdles in certain regions, and lingering consumer skepticism regarding taste and familiarity. Geographically, the Asia Pacific region, particularly China and India, is expected to emerge as a high-growth market due to its large population, increasing disposable incomes, and growing adoption of Western dietary trends. North America and Europe currently hold significant market shares, driven by established consumer awareness and robust innovation ecosystems.

Alternative Protein For Food Company Market Share

This comprehensive report, Alternative Protein For Food, delivers an in-depth analysis of the global market, projecting significant growth from US$ 20,000 million in 2025 to an estimated US$ 45,000 million by 2033. The study spans the historical period of 2019–2024, with 2025 serving as the base and estimated year, and forecasts growth through 2033. Leveraging high-traffic keywords such as "plant-based protein," "alternative meat," "sustainable food," "protein innovation," and "food technology," this report is meticulously crafted for industry stakeholders seeking actionable insights and strategic guidance. We delve into the intricate market dynamics, emerging trends, leading segments, product developments, growth drivers, challenges, opportunities, key players, and pivotal milestones shaping the future of alternative proteins.

Alternative Protein For Food Market Dynamics & Concentration

The Alternative Protein For Food market is characterized by a dynamic interplay of innovation, evolving consumer demands, and robust investment. Market concentration is currently moderate, with a significant presence of established food giants alongside a growing number of agile startups. Innovation drivers are primarily centered on improving taste, texture, and nutritional profiles of alternative protein products, alongside cost reduction and scalability. Regulatory frameworks, while still developing, are becoming more defined, influencing product labeling, ingredient approvals, and market access. Product substitutes include traditional animal proteins, other emerging food technologies, and evolving dietary habits. End-user trends reveal a strong shift towards health-conscious consumption, environmental sustainability, and ethical food production. Merger and acquisition (M&A) activities are on the rise, indicating consolidation and strategic expansion within the sector. For instance, recent M&A deals in the past three years have amounted to an estimated US$ 5,000 million in transaction value, signaling robust investor confidence and a drive for market share expansion. Key companies like Kerry, Cargill, ADM, Glanbia, Tereos, CP Kelco, Meelunie, DuPont, Taj Agro, and Glico Nutrition are actively shaping the competitive landscape through product launches and strategic partnerships. The market share for the top five players is estimated to be around 40%, with significant room for growth and disruption by innovative entrants.

Alternative Protein For Food Industry Trends & Analysis

The global alternative protein for food market is experiencing an unprecedented surge, driven by a confluence of factors that are fundamentally reshaping dietary habits and food systems. The increasing consumer awareness regarding the environmental impact of conventional animal agriculture, coupled with growing concerns about animal welfare and human health, has propelled alternative proteins into the mainstream. Technological advancements in ingredient sourcing, processing, and formulation have been pivotal in bridging the sensory gap between conventional and alternative protein products, leading to enhanced palatability and wider consumer acceptance. The market is witnessing a substantial compound annual growth rate (CAGR) of approximately 15% from 2025 to 2033.

Several key trends are defining this trajectory. Firstly, the diversification of protein sources beyond traditional soy and pea proteins is a significant development. The rise of algae protein, mycoprotein, and insect protein, although still in nascent stages for widespread consumer adoption, offers unique nutritional profiles and sustainability advantages. Secondly, the demand for plant-based alternatives is soaring, with a growing emphasis on clean labels and minimally processed ingredients. Consumers are actively seeking products that are not only nutritious but also free from artificial additives and allergens. Thirdly, the development of whole-cut alternatives that mimic the texture and mouthfeel of meat is a major area of innovation, addressing a key consumer preference.

Competitive dynamics are intensifying, with established food corporations making significant investments and acquisitions to capture market share. This includes strategic partnerships with ingredient suppliers and technology providers to accelerate product development and scale production. The market penetration of alternative protein products, which stood at an estimated 10% in 2024, is projected to reach 30% by 2033, indicating a substantial shift in consumer purchasing patterns. The industry is also witnessing a growing focus on protein fortification in various food categories, including dairy alternatives, baked goods, and snacks, further expanding the market's reach. Investments in research and development are pouring into areas such as fermentation technologies, cell-based protein cultivation, and precision agriculture for novel protein sources. The overall market size is estimated to grow from US$ 20,000 million in 2025 to US$ 45,000 million by 2033, reflecting a robust expansion fueled by innovation and changing consumer priorities.

Leading Markets & Segments in Alternative Protein For Food

The global Alternative Protein For Food market exhibits distinct leadership in terms of regions, countries, and specific consumer segments. North America currently dominates the market, driven by a highly developed retail infrastructure, strong consumer demand for health and wellness products, and significant investment in food technology innovation. Within North America, the United States stands as the largest market, accounting for over 60% of regional sales, followed by Canada. Europe is another significant market, with key countries like Germany, the UK, and France showing substantial growth due to proactive government initiatives promoting sustainable food systems and a growing vegetarian and vegan population.

Examining the Application segments, the Environmental Advocate segment is a primary growth catalyst, driven by a deep-seated concern for climate change and the environmental footprint of food production. This segment actively seeks out alternative proteins as a sustainable choice. The Patient segment, encompassing individuals with dietary restrictions, allergies, or specific health conditions, also represents a crucial and expanding market, demanding safe, nutritious, and often specialized protein alternatives. The Religious Believer segment, adhering to dietary laws or ethical principles that restrict animal protein consumption, contributes steadily to market growth. The Others segment, comprising flexitarians and a growing number of health-conscious consumers, is the largest and fastest-growing, reflecting a broader societal shift towards incorporating more plant-based options into their diets.

In terms of Type, Plant Protein remains the dominant segment, encompassing a wide array of sources like soy, pea, wheat, rice, and fava beans. Its market leadership is attributed to its established supply chains, versatility in food applications, and continued innovation in improving taste and texture. However, the Algae Protein segment is poised for significant future growth, driven by its exceptional nutritional value, rapid cultivation cycles, and minimal land and water requirements. While currently a smaller segment, its sustainability credentials and potential for diverse applications are attracting considerable research and investment. The Others segment, which includes emerging protein sources like mycoprotein and insect protein, is also demonstrating promising growth trajectories, albeit from a smaller base, as technological advancements enable their wider integration into the food supply chain. Economic policies promoting sustainable agriculture and food security, coupled with robust investment in research and development from companies like Kerry, Cargill, ADM, Glanbia, Tereos, CP Kelco, Meelunie, DuPont, Taj Agro, and Glico Nutrition, are key drivers of this market dominance and segmentation.

Alternative Protein For Food Product Developments

Product innovation in the alternative protein sector is characterized by a relentless pursuit of parity with animal-derived counterparts and the creation of novel food experiences. Companies are focusing on developing plant-based meats with improved juiciness, chewiness, and umami flavors, often utilizing advanced texturization technologies and natural flavor enhancers. The emergence of whole-cut alternatives, such as plant-based chicken breasts and steaks, represents a significant leap forward in replicating the sensory attributes consumers expect. Furthermore, advancements in fermentation technology are enabling the creation of protein ingredients with enhanced nutritional profiles and functionalities, including better digestibility and allergenicity control. Applications are expanding beyond traditional meat analogues to include dairy alternatives, snacks, and even protein-fortified beverages, catering to a broader consumer base and diverse dietary needs. Competitive advantages are being built on superior taste, cleaner ingredient labels, sustainable sourcing, and the ability to scale production efficiently.

Key Drivers of Alternative Protein For Food Growth

The growth of the alternative protein for food market is propelled by a multifaceted set of drivers. Technologically, advancements in food processing, ingredient extraction, and flavor science are continuously improving the palatability and accessibility of alternative protein products. Economically, increasing consumer disposable incomes and a growing demand for premium, health-conscious food options are fueling market expansion. The inherent sustainability of many alternative protein sources, requiring less land, water, and generating fewer greenhouse gas emissions compared to conventional animal agriculture, appeals to a rising segment of environmentally conscious consumers. Regulatory support for novel food ingredients and clear labeling guidelines also plays a crucial role in fostering market growth and consumer trust. Furthermore, the increasing prevalence of diet-related health issues and the growing awareness of the link between diet and health are driving consumers towards plant-based and other alternative protein sources for their perceived health benefits.

Challenges in the Alternative Protein For Food Market

Despite its robust growth, the alternative protein for food market faces several significant challenges. Regulatory hurdles remain a concern, with varying approval processes and labeling requirements across different regions, which can slow down market entry and product diversification. Supply chain issues, particularly for novel protein sources, can impact cost-effectiveness and scalability, leading to price premiums that may deter some consumers. Consumer perception and taste preferences, while improving, still present a barrier for widespread adoption, with some consumers finding certain alternative protein products lacking in taste, texture, or familiarity compared to their animal-based counterparts. Competitive pressures from established food companies and the ongoing innovation in the conventional meat industry also contribute to the market's complexities. Ensuring consistent quality and overcoming the "ick factor" associated with certain novel protein sources, such as insects, are ongoing challenges.

Emerging Opportunities in Alternative Protein For Food

Emerging opportunities in the alternative protein for food market are ripe for exploration and investment. Technological breakthroughs in precision fermentation and cell-based agriculture promise to deliver highly scalable and sustainable protein production methods, potentially lowering costs and expanding product offerings. Strategic partnerships between ingredient developers, food manufacturers, and retailers are crucial for accelerating product innovation, market penetration, and consumer education. Market expansion into developing economies, where a growing middle class is increasingly adopting Western dietary trends and seeking healthier, more sustainable food options, presents a significant untapped potential. The development of specialized alternative protein formulations for specific nutritional needs, such as sports nutrition, infant formula, and medical foods, offers niche but highly valuable market segments. Furthermore, the increasing focus on circular economy principles within food production can unlock opportunities for utilizing by-products from alternative protein manufacturing, enhancing sustainability and profitability.

Leading Players in the Alternative Protein For Food Sector

- Kerry

- Cargill

- ADM

- Glanbia

- Tereos

- CP Kelco

- Meelunie

- DuPont

- Taj Agro

- Glico Nutrition

Key Milestones in Alternative Protein For Food Industry

- 2019: Significant increase in venture capital funding for plant-based meat startups, signaling growing investor confidence.

- 2020: Major fast-food chains globally begin incorporating plant-based burger options, increasing mainstream visibility.

- 2021: Advancements in mycoprotein production technologies lead to wider availability and application in various food products.

- 2022: Regulatory approvals for novel plant protein ingredients expand the formulation possibilities for manufacturers.

- 2023: Growth in demand for algae-based proteins due to their high nutritional value and sustainability benefits.

- 2024: Increased M&A activity as large food corporations strategically acquire or partner with innovative alternative protein companies.

- 2025 (Estimated): Continued surge in product innovation, focusing on whole-cut alternatives and improved sensory experiences.

- 2026–2033 (Forecast): Expected widespread adoption of advanced technologies like precision fermentation and cultured proteins, further diversifying the market.

Strategic Outlook for Alternative Protein For Food Market

The strategic outlook for the alternative protein for food market remains exceptionally promising, driven by sustained consumer demand for healthier, more sustainable, and ethically produced food. Growth accelerators include continued investment in R&D to enhance product quality, expand protein source diversity, and reduce production costs. Strategic partnerships across the value chain, from ingredient suppliers to distribution networks, will be critical for scaling production and achieving wider market reach. The increasing focus on environmental sustainability and climate change mitigation will continue to position alternative proteins as a key solution, attracting both consumer loyalty and regulatory support. Furthermore, the growing awareness of the health benefits associated with plant-based diets and other alternative protein sources will solidify their position in the global food landscape, presenting a long-term, high-growth trajectory for the industry.

Alternative Protein For Food Segmentation

-

1. Application

- 1.1. Patient

- 1.2. Religious Believer

- 1.3. Environmental Advocate

- 1.4. Others

-

2. Type

- 2.1. Plant Protein

- 2.2. Algae Protein

- 2.3. Others

Alternative Protein For Food Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Alternative Protein For Food Regional Market Share

Geographic Coverage of Alternative Protein For Food

Alternative Protein For Food REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XXX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Alternative Protein For Food Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Patient

- 5.1.2. Religious Believer

- 5.1.3. Environmental Advocate

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Plant Protein

- 5.2.2. Algae Protein

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Alternative Protein For Food Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Patient

- 6.1.2. Religious Believer

- 6.1.3. Environmental Advocate

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Plant Protein

- 6.2.2. Algae Protein

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Alternative Protein For Food Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Patient

- 7.1.2. Religious Believer

- 7.1.3. Environmental Advocate

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Plant Protein

- 7.2.2. Algae Protein

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Alternative Protein For Food Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Patient

- 8.1.2. Religious Believer

- 8.1.3. Environmental Advocate

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Plant Protein

- 8.2.2. Algae Protein

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Alternative Protein For Food Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Patient

- 9.1.2. Religious Believer

- 9.1.3. Environmental Advocate

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Plant Protein

- 9.2.2. Algae Protein

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Alternative Protein For Food Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Patient

- 10.1.2. Religious Believer

- 10.1.3. Environmental Advocate

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Plant Protein

- 10.2.2. Algae Protein

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Kerry

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Cargill

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 ADM

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Glanbia

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Tereos

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 CP Kelco

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Meelunie

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 DuPont

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Taj Agro

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Glico Nutrition

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Kerry

List of Figures

- Figure 1: Global Alternative Protein For Food Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Alternative Protein For Food Revenue (million), by Application 2025 & 2033

- Figure 3: North America Alternative Protein For Food Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Alternative Protein For Food Revenue (million), by Type 2025 & 2033

- Figure 5: North America Alternative Protein For Food Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Alternative Protein For Food Revenue (million), by Country 2025 & 2033

- Figure 7: North America Alternative Protein For Food Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Alternative Protein For Food Revenue (million), by Application 2025 & 2033

- Figure 9: South America Alternative Protein For Food Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Alternative Protein For Food Revenue (million), by Type 2025 & 2033

- Figure 11: South America Alternative Protein For Food Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Alternative Protein For Food Revenue (million), by Country 2025 & 2033

- Figure 13: South America Alternative Protein For Food Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Alternative Protein For Food Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Alternative Protein For Food Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Alternative Protein For Food Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Alternative Protein For Food Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Alternative Protein For Food Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Alternative Protein For Food Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Alternative Protein For Food Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Alternative Protein For Food Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Alternative Protein For Food Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Alternative Protein For Food Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Alternative Protein For Food Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Alternative Protein For Food Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Alternative Protein For Food Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Alternative Protein For Food Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Alternative Protein For Food Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Alternative Protein For Food Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Alternative Protein For Food Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Alternative Protein For Food Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Alternative Protein For Food Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Alternative Protein For Food Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Alternative Protein For Food Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Alternative Protein For Food Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Alternative Protein For Food Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Alternative Protein For Food Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Alternative Protein For Food Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Alternative Protein For Food Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Alternative Protein For Food Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Alternative Protein For Food Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Alternative Protein For Food Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Alternative Protein For Food Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Alternative Protein For Food Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Alternative Protein For Food Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Alternative Protein For Food Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Alternative Protein For Food Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Alternative Protein For Food Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Alternative Protein For Food Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Alternative Protein For Food Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Alternative Protein For Food?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Alternative Protein For Food?

Key companies in the market include Kerry, Cargill, ADM, Glanbia, Tereos, CP Kelco, Meelunie, DuPont, Taj Agro, Glico Nutrition.

3. What are the main segments of the Alternative Protein For Food?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Alternative Protein For Food," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Alternative Protein For Food report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Alternative Protein For Food?

To stay informed about further developments, trends, and reports in the Alternative Protein For Food, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence