Key Insights

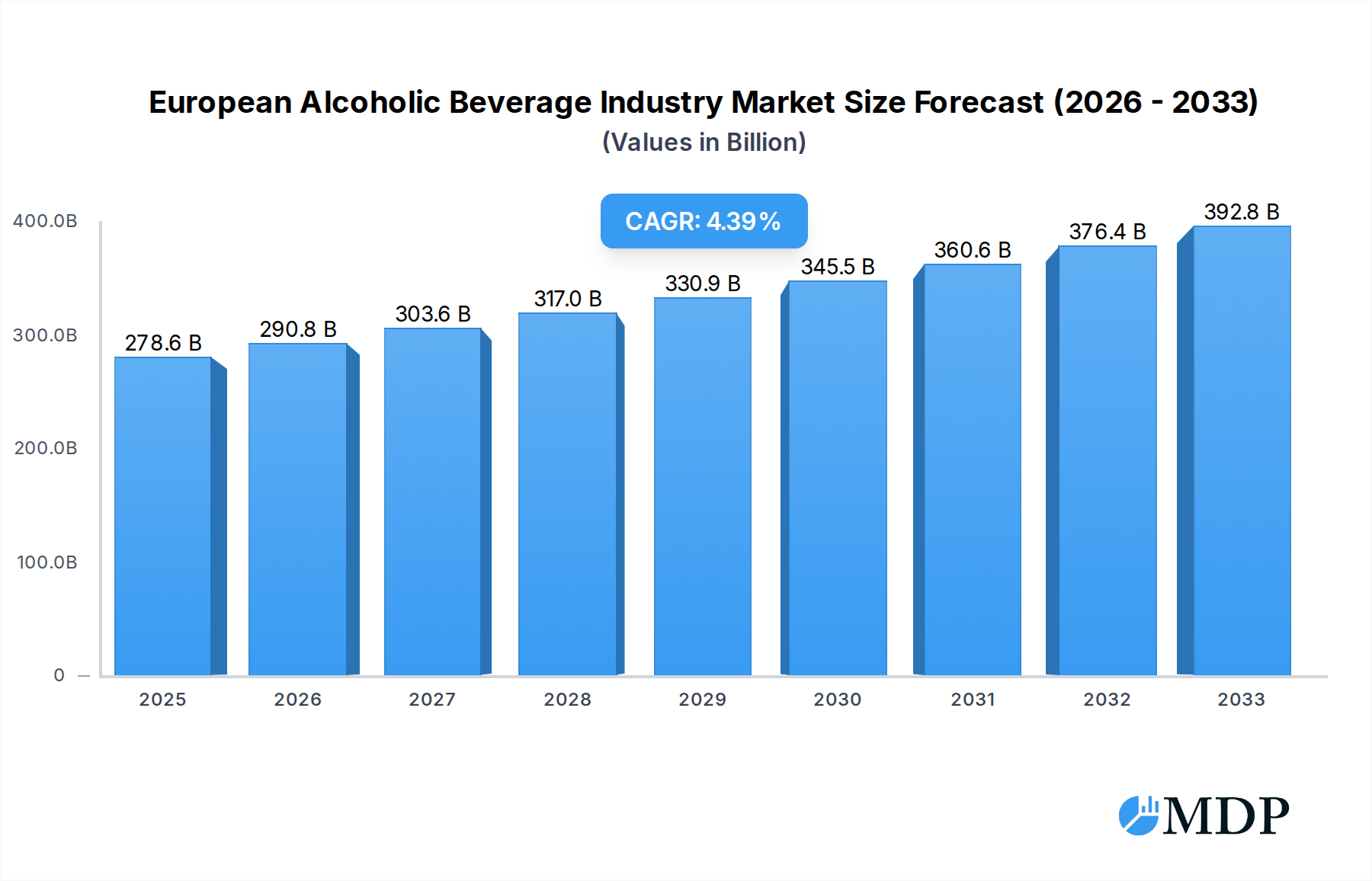

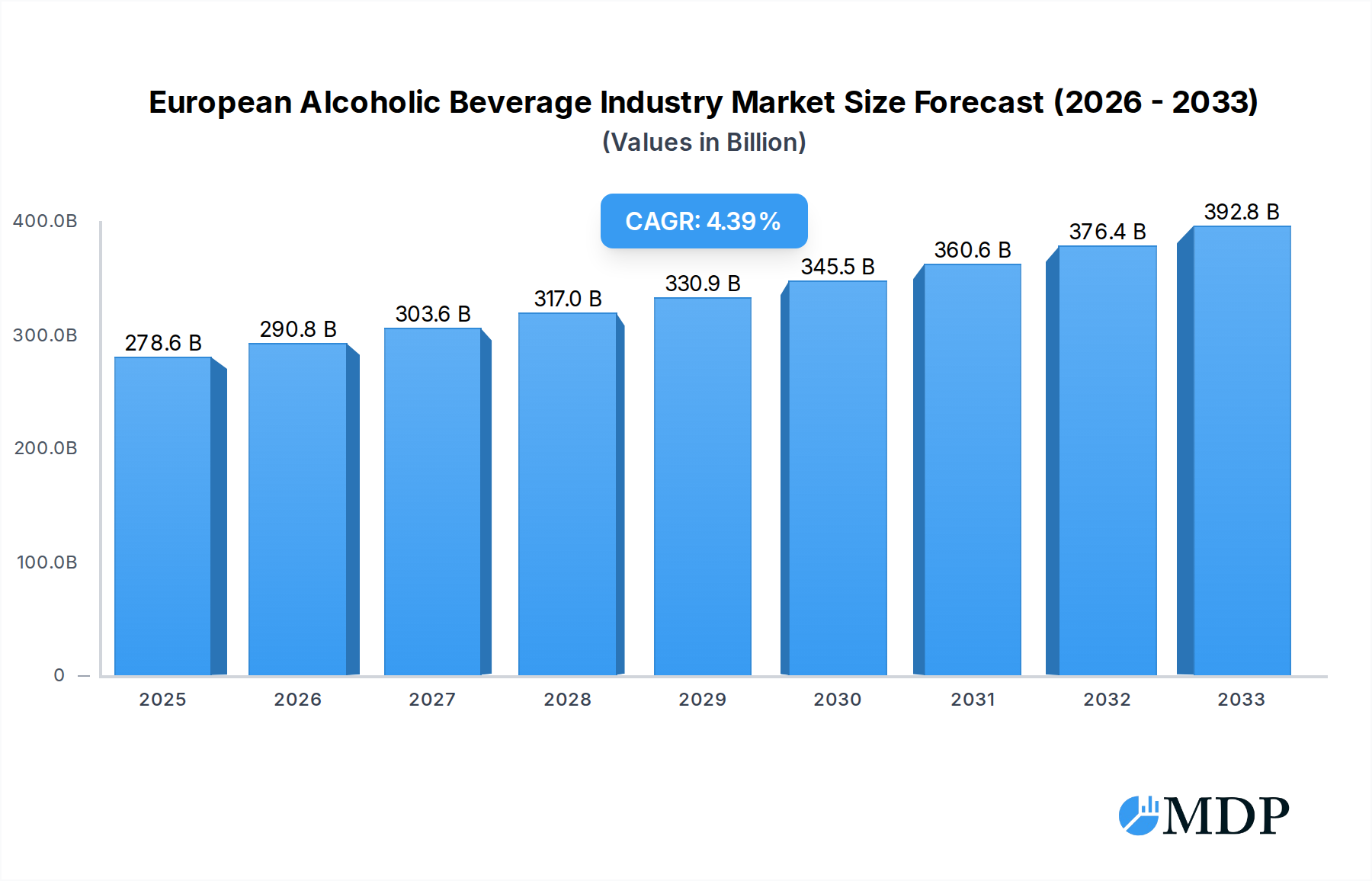

The European Alcoholic Beverage Industry is poised for robust growth, projected to reach $278.56 billion in 2025. The market is anticipated to expand at a Compound Annual Growth Rate (CAGR) of 4.48% from 2025 to 2033, indicating a dynamic and evolving landscape. This substantial market size is fueled by a confluence of evolving consumer preferences, the increasing prominence of premium and craft offerings across Beer, Wine, and Spirits segments, and strategic expansion in distribution channels. The "on-trade" sector, encompassing bars, restaurants, and hotels, continues to be a significant contributor, while the "off-trade" segment, particularly online retail and specialist stores, is experiencing accelerated growth due to convenience and wider product accessibility. Key players like Pernod Ricard SA, Heineken Holding NV, and Anheuser-Busch InBev SA/NV are instrumental in shaping this market through innovation, mergers, and strategic acquisitions, further solidifying the industry's upward trajectory.

European Alcoholic Beverage Industry Market Size (In Billion)

Several factors are driving this expansion within the European alcoholic beverage market. A growing demand for artisanal and specialty products, including craft beers, premium wines, and unique spirit formulations, is a significant trend. Consumers are increasingly seeking quality over quantity, leading to a premiumization of the market. Furthermore, the digital transformation has profoundly impacted distribution, with online retail channels becoming increasingly vital for reaching a broader customer base and offering specialized selections. While challenges related to stringent regulations, fluctuating raw material costs, and evolving health consciousness among consumers do exist, the overall outlook remains strongly positive. The industry's adaptability, coupled with continuous innovation in product development and marketing strategies, is expected to sustain its growth momentum throughout the forecast period, particularly in key European markets like the United Kingdom, Germany, and France.

European Alcoholic Beverage Industry Company Market Share

Here's an SEO-optimized, engaging report description for the European Alcoholic Beverage Industry, designed for maximum visibility and stakeholder attraction:

European Alcoholic Beverage Industry Market Analysis & Forecast (2019-2033): Unveiling Trends, Growth Drivers, and Leading Players

Dive deep into the dynamic European alcoholic beverage market with this comprehensive report. Covering beer, wine, and spirits, this analysis navigates the intricate landscape of on-trade and off-trade distribution channels, including supermarkets, hypermarkets, specialist stores, and the burgeoning online retail sector. With an estimated market size projected to reach several hundred billion by 2025, this report provides unparalleled insights into market dynamics, concentration, and future trajectory. Leveraging high-traffic keywords such as "European alcohol market," "wine industry Europe," "beer market growth," "spirits trends," and "alcoholic beverage forecast," this study is essential for distributors, manufacturers, investors, and industry stakeholders seeking to capitalize on emerging opportunities and understand the competitive environment. Our detailed analysis spans the historical period (2019-2024), base year (2025), and forecast period (2025-2033), offering a robust outlook for strategic decision-making. Discover key developments from March 2022: Heineken launched Heineken Silver, February 2022: Anheuser-Busch InBev launched Stella Artois Unfiltered, and March 2021: Heineken launched Pure Piraña hard seltzer, alongside an in-depth examination of leading companies like Pernod Ricard SA, Heineken Holding NV, E & J Gallo Winery, Bacardi Limited, Bronco Wine Company, Carlsberg Breweries A/S, Anheuser-Busch InBev SA/NV, Molson Coors Brewing Company, LVMH Moët Hennessy Louis Vuitton, and Diageo PLC. This report is your definitive guide to the European alcoholic beverage industry.

European Alcoholic Beverage Industry Market Dynamics & Concentration

The European alcoholic beverage market is characterized by a moderate to high degree of concentration, with a few dominant multinational corporations holding significant market share across various product categories. Innovation drivers are largely influenced by evolving consumer preferences for premiumization, low-alcohol/alcohol-free options, and sustainable production practices. Regulatory frameworks, including excise duties, marketing restrictions, and labeling requirements, play a crucial role in shaping market access and product development across different European nations. Product substitutes, ranging from non-alcoholic beverages to craft alternatives, continuously challenge established market players, necessitating agile product portfolios and marketing strategies. End-user trends highlight a growing demand for experiential consumption, personalized offerings, and a greater emphasis on health and wellness, impacting both product innovation and distribution strategies. Mergers and acquisitions (M&A) activities remain a significant feature of the industry, driven by a desire to expand geographical reach, acquire new brands, and achieve economies of scale. For instance, numerous multi-million billion dollar deals have been recorded in the historical period, reflecting strategic consolidation and portfolio diversification efforts by leading entities. M&A deal counts in the past five years have consistently remained in the double digits, indicating ongoing strategic realignment. Key players often engage in acquisitions to bolster their presence in specific segments or capitalize on niche market opportunities, further influencing overall market concentration.

European Alcoholic Beverage Industry Industry Trends & Analysis

The European alcoholic beverage industry is experiencing robust growth, driven by a confluence of factors including increasing disposable incomes, a thriving tourism sector, and a dynamic shift in consumer preferences. The CAGR for the forecast period is projected to be between XX% and XX%, reflecting a healthy expansion trajectory. Market penetration for premium and craft alcoholic beverages continues to rise, as consumers increasingly seek unique and high-quality drinking experiences. Technological disruptions are revolutionizing production, distribution, and consumer engagement. Innovations in brewing, fermentation, and distillation processes are leading to the development of novel products with enhanced flavor profiles and reduced environmental impact. E-commerce platforms and direct-to-consumer (DTC) models are reshaping distribution channels, offering greater convenience and personalized offerings. Consumer preferences are leaning towards healthier options, with a significant surge in demand for low-alcohol and alcohol-free beverages, as well as hard seltzers and ready-to-drink (RTD) cocktails. This trend is particularly pronounced among younger demographics, Gen Y and Gen Z, who are more health-conscious and open to exploring new beverage categories. Competitive dynamics are intensifying, with traditional beverage giants facing increasing pressure from agile craft producers and emerging brands. The focus is shifting from sheer volume to value-added products and sustainable practices. Companies are investing heavily in R&D to cater to these evolving demands, leading to a more diverse and competitive market landscape. The overall market value is expected to reach well over several hundred billion in the coming years, underscoring the industry's substantial economic significance. The penetration of premium segments is estimated to increase by XX% by 2033.

Leading Markets & Segments in European Alcoholic Beverage Industry

The European alcoholic beverage industry exhibits significant regional and segmental variations. Geographically, Western Europe, encompassing countries like Germany, France, Spain, and the United Kingdom, remains the dominant market due to its mature consumer base, high disposable incomes, and established distribution networks. However, Eastern European markets are showing accelerated growth, driven by increasing urbanization and a rising middle class. Within product types, Beer consistently holds the largest market share, fueled by its widespread popularity and diverse range of sub-segments, from lagers to craft ales. Wine maintains a strong presence, with significant consumption in countries with rich viticultural heritage, while Spirits are experiencing robust growth, particularly in the premium and super-premium categories, driven by cocktail culture and niche artisanal offerings.

Distribution channels are also experiencing a significant evolution. Off-trade channels, especially Supermarkets/Hypermarkets, continue to dominate in terms of volume due to their accessibility and promotional activities. The Online Retail Stores segment, however, is witnessing the most rapid expansion, driven by convenience, wider product selection, and targeted marketing capabilities. This channel is projected to capture a substantial share of the market by the end of the forecast period.

- Key Drivers of Dominance:

- Economic Policies: Favorable tax structures and trade agreements in key European nations bolster market growth.

- Infrastructure: Advanced logistics and supply chain networks ensure efficient product distribution across the continent.

- Consumer Demographics: A large and diverse consumer base with varying purchasing power and preferences sustains demand.

- Cultural Significance: Deep-rooted traditions and cultural associations with alcoholic beverages, particularly wine and beer, contribute to sustained consumption.

- Technological Adoption: The rapid uptake of e-commerce and digital marketing strategies is transforming how consumers access and purchase beverages.

The dominance of certain segments is further amplified by targeted marketing campaigns and product innovation. For instance, the rising popularity of hard seltzers and RTD cocktails has led to increased product development and promotional focus within these niche segments, capturing a growing share of the younger consumer market. The premiumization trend is evident across all product categories, with consumers willing to pay more for perceived quality, unique origins, and artisanal production methods.

European Alcoholic Beverage Industry Product Developments

Product development in the European alcoholic beverage industry is increasingly focused on meeting evolving consumer demands for healthier, more convenient, and premium options. Innovations such as low-alcohol and alcohol-free alternatives, hard seltzers, and ready-to-drink (RTD) cocktails are gaining significant traction, driven by the growing health and wellness trend. Companies are also investing in sustainable packaging solutions and ethically sourced ingredients to appeal to environmentally conscious consumers. Technological advancements in brewing and distillation are enabling the creation of novel flavor profiles and unique product experiences. The competitive advantage for brands lies in their ability to innovate rapidly, adapt to changing consumer preferences, and effectively communicate their product's unique selling propositions, whether it's origin, craftsmanship, or health benefits.

Key Drivers of European Alcoholic Beverage Industry Growth

Several key drivers are propelling the growth of the European alcoholic beverage industry. Technological advancements in production processes, such as improved fermentation techniques and novel flavoring agents, are leading to the development of innovative products that cater to niche tastes. Economic factors, including rising disposable incomes across several European nations and a rebound in tourism, are boosting consumer spending on alcoholic beverages, particularly premium and imported brands. Favorable regulatory shifts, in some regions, that encourage responsible consumption and support for local producers can also stimulate market expansion. Furthermore, the growing consumer interest in health and wellness is creating significant demand for low-alcohol and non-alcoholic alternatives, opening up new market segments. The expanding online retail sector for alcoholic beverages provides a crucial channel for reaching a wider audience and offering convenient purchasing options.

Challenges in the European Alcoholic Beverage Industry Market

The European alcoholic beverage industry faces several significant challenges. Stringent and often fragmented regulatory hurdles across different EU member states, including varying excise duties, advertising restrictions, and labeling requirements, can impede market access and increase operational complexity. Supply chain disruptions, exacerbated by global events and logistical complexities, can impact the availability and cost of raw materials and finished goods. Intense competitive pressures from both established global players and agile craft producers necessitate continuous innovation and strategic marketing. Additionally, growing public health concerns and a societal shift towards mindful consumption are leading to increased demand for lower-alcohol and non-alcoholic options, requiring companies to adapt their product portfolios. The rising cost of raw materials, such as grains and grapes, also presents a significant challenge to profitability.

Emerging Opportunities in European Alcoholic Beverage Industry

Emerging opportunities within the European alcoholic beverage industry are significant and diverse. The burgeoning demand for low-alcohol and alcohol-free beverages presents a substantial growth avenue, with consumers actively seeking healthier alternatives without compromising on taste and experience. The expansion of e-commerce and direct-to-consumer (DTC) sales channels offers brands unprecedented reach and the ability to build direct relationships with consumers, fostering loyalty and personalized marketing. Technological breakthroughs in brewing, distillation, and packaging are enabling the creation of innovative products with unique flavor profiles and enhanced sustainability. Strategic partnerships between beverage companies and other industries, such as hospitality and food service, can unlock new consumption occasions and revenue streams. Furthermore, market expansion into underserved regions within Eastern Europe and the development of premium and super-premium offerings to cater to the discerning European palate represent significant long-term growth catalysts.

Leading Players in the European Alcoholic Beverage Industry Sector

- Pernod Ricard SA

- Heineken Holding NV

- E & J Gallo Winery

- Bacardi Limited

- Bronco Wine Company

- Carlsberg Breweries A/S

- Anheuser-Busch InBev SA/NV

- Molson Coors Brewing Company

- LVMH Moët Hennessy Louis Vuitton

- Diageo PLC

Key Milestones in European Alcoholic Beverage Industry Industry

- March 2022: Heineken launched Heineken Silver, a premium lager aimed at Gen Y and Z drinkers in the United Kingdom and European Union. The new lager (4% ABV) is available in 4x330ml bottles, 12x330ml bottles, and 6x330ml slim-line cans, offering a premium and modern packaging design.

- February 2022: The United Kingdom division of Anheuser-Busch InBev launched Stella Artois Unfiltered lager beer in the country. Standard Stella Artois has a 4.6% abv available in six- and 12-packs of 33cl cans and 66cl individual cans.

- March 2021: Heineken launched Pure Piraña hard seltzer in Europe following a successful trial in Mexico and New Zealand. The hard seltzer is initially available in Austria, Ireland, Netherlands, Portugal, and Spain.

Strategic Outlook for European Alcoholic Beverage Industry Market

The strategic outlook for the European alcoholic beverage market is characterized by continued evolution and adaptation to consumer trends. Growth accelerators will likely stem from the persistent demand for premiumization, driven by consumers' willingness to spend on high-quality and artisanal products across beer, wine, and spirits. The expansion of the low-alcohol and alcohol-free segment presents a significant opportunity for innovation and market penetration, catering to health-conscious demographics. Strategic investments in e-commerce and direct-to-consumer channels will be crucial for enhancing market reach and customer engagement. Furthermore, companies that prioritize sustainability in their sourcing, production, and packaging will likely gain a competitive edge. The market's future potential is also tied to navigating regulatory landscapes effectively and embracing digital transformation to optimize operations and marketing efforts.

(Note: All monetary values are represented in billions. Predicted values for CAGR and market penetration are indicated by 'XX' as per instructions where specific figures were not provided for the context.)

European Alcoholic Beverage Industry Segmentation

-

1. Product Type

- 1.1. Beer

- 1.2. Wine

- 1.3. Spirits

-

2. Distribution Channel

- 2.1. On-trade

-

2.2. Off-trade

- 2.2.1. Supermarkets/Hypermarkets

- 2.2.2. Specialist Stores

- 2.2.3. Online Retail Stores

- 2.2.4. Other Off-trade Channels

European Alcoholic Beverage Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

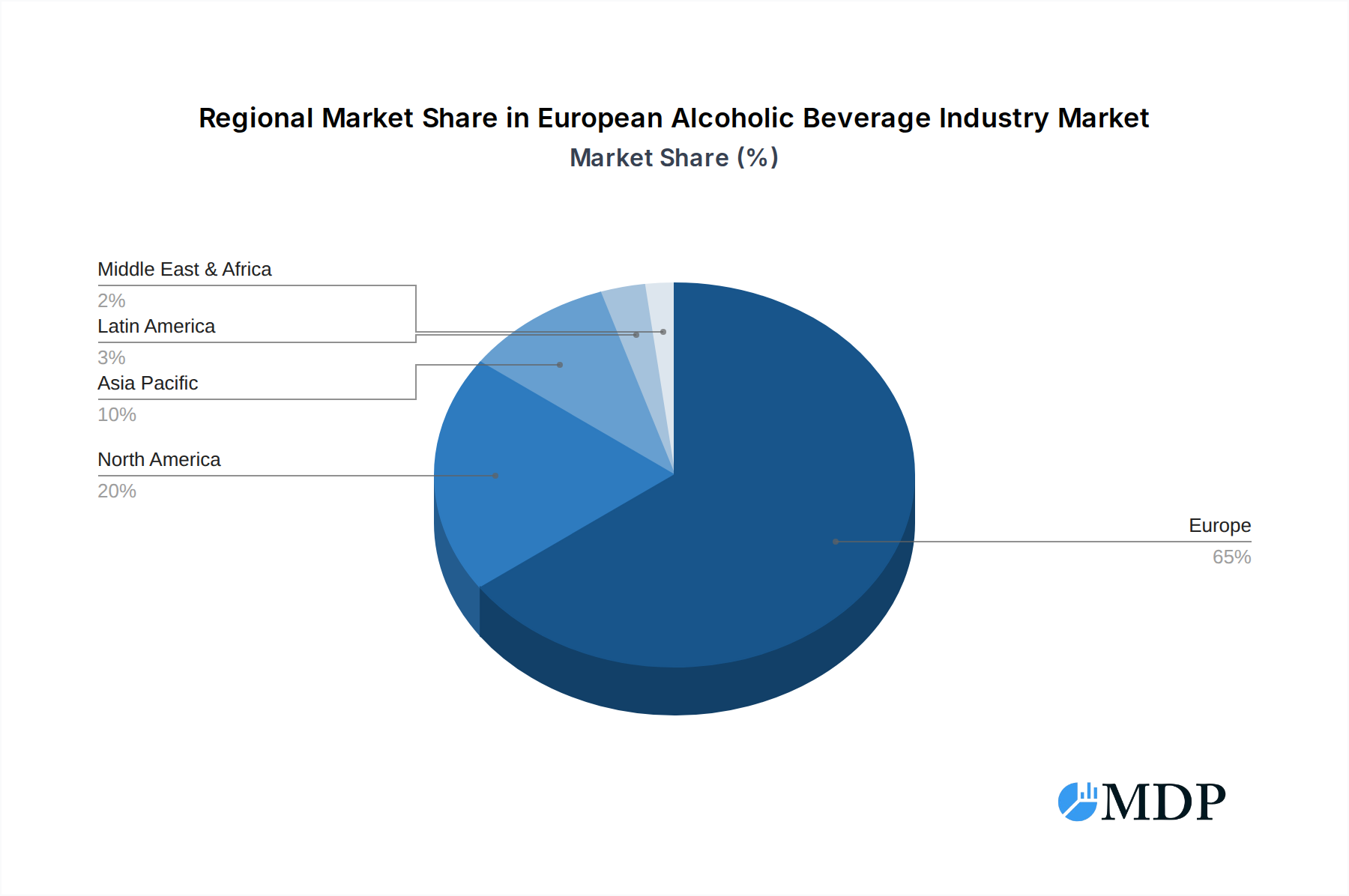

European Alcoholic Beverage Industry Regional Market Share

Geographic Coverage of European Alcoholic Beverage Industry

European Alcoholic Beverage Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.48% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Beer

- 5.1.2. Wine

- 5.1.3. Spirits

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. On-trade

- 5.2.2. Off-trade

- 5.2.2.1. Supermarkets/Hypermarkets

- 5.2.2.2. Specialist Stores

- 5.2.2.3. Online Retail Stores

- 5.2.2.4. Other Off-trade Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. European Alcoholic Beverage Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Beer

- 6.1.2. Wine

- 6.1.3. Spirits

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. On-trade

- 6.2.2. Off-trade

- 6.2.2.1. Supermarkets/Hypermarkets

- 6.2.2.2. Specialist Stores

- 6.2.2.3. Online Retail Stores

- 6.2.2.4. Other Off-trade Channels

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Pernod Ricard SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Heineken Holding NV

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 E & J Gallo Winery

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Bacardi Limited

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Bronco Wine Company*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Carlsberg Breweries A/S

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Anheuser-Busch InBev SA/NV

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Molson Coors Brewing Company

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 LVMH Moët Hennessy Louis Vuitton

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Diageo PLC

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Pernod Ricard SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: European Alcoholic Beverage Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: European Alcoholic Beverage Industry Share (%) by Company 2025

List of Tables

- Table 1: European Alcoholic Beverage Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: European Alcoholic Beverage Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: European Alcoholic Beverage Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: European Alcoholic Beverage Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 5: European Alcoholic Beverage Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: European Alcoholic Beverage Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United Kingdom European Alcoholic Beverage Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Germany European Alcoholic Beverage Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: France European Alcoholic Beverage Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Italy European Alcoholic Beverage Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Spain European Alcoholic Beverage Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Netherlands European Alcoholic Beverage Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Belgium European Alcoholic Beverage Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Sweden European Alcoholic Beverage Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Norway European Alcoholic Beverage Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Poland European Alcoholic Beverage Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Denmark European Alcoholic Beverage Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Alcoholic Beverage Industry?

The projected CAGR is approximately 4.48%.

2. Which companies are prominent players in the European Alcoholic Beverage Industry?

Key companies in the market include Pernod Ricard SA, Heineken Holding NV, E & J Gallo Winery, Bacardi Limited, Bronco Wine Company*List Not Exhaustive, Carlsberg Breweries A/S, Anheuser-Busch InBev SA/NV, Molson Coors Brewing Company, LVMH Moët Hennessy Louis Vuitton, Diageo PLC.

3. What are the main segments of the European Alcoholic Beverage Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 278.56 billion as of 2022.

5. What are some drivers contributing to market growth?

Convenience Offered By Online Food Delivery Services; Attractive Offers And Memberships Along With Advertisements And Marketing By Players.

6. What are the notable trends driving market growth?

Increased Demand for Craft Beer.

7. Are there any restraints impacting market growth?

Consumers Desire For Fine Dining Experience.

8. Can you provide examples of recent developments in the market?

March 2022: Heineken launched Heineken Silver, a premium lager aimed at Gen Y and Z drinkers in the United Kingdom and European Union. The new lager (4% ABV) is available in 4x330ml bottles, 12x330ml bottles, and 6x330ml slim-line cans. The range offers a premium and modern packaging design.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Alcoholic Beverage Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Alcoholic Beverage Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Alcoholic Beverage Industry?

To stay informed about further developments, trends, and reports in the European Alcoholic Beverage Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence