Key Insights

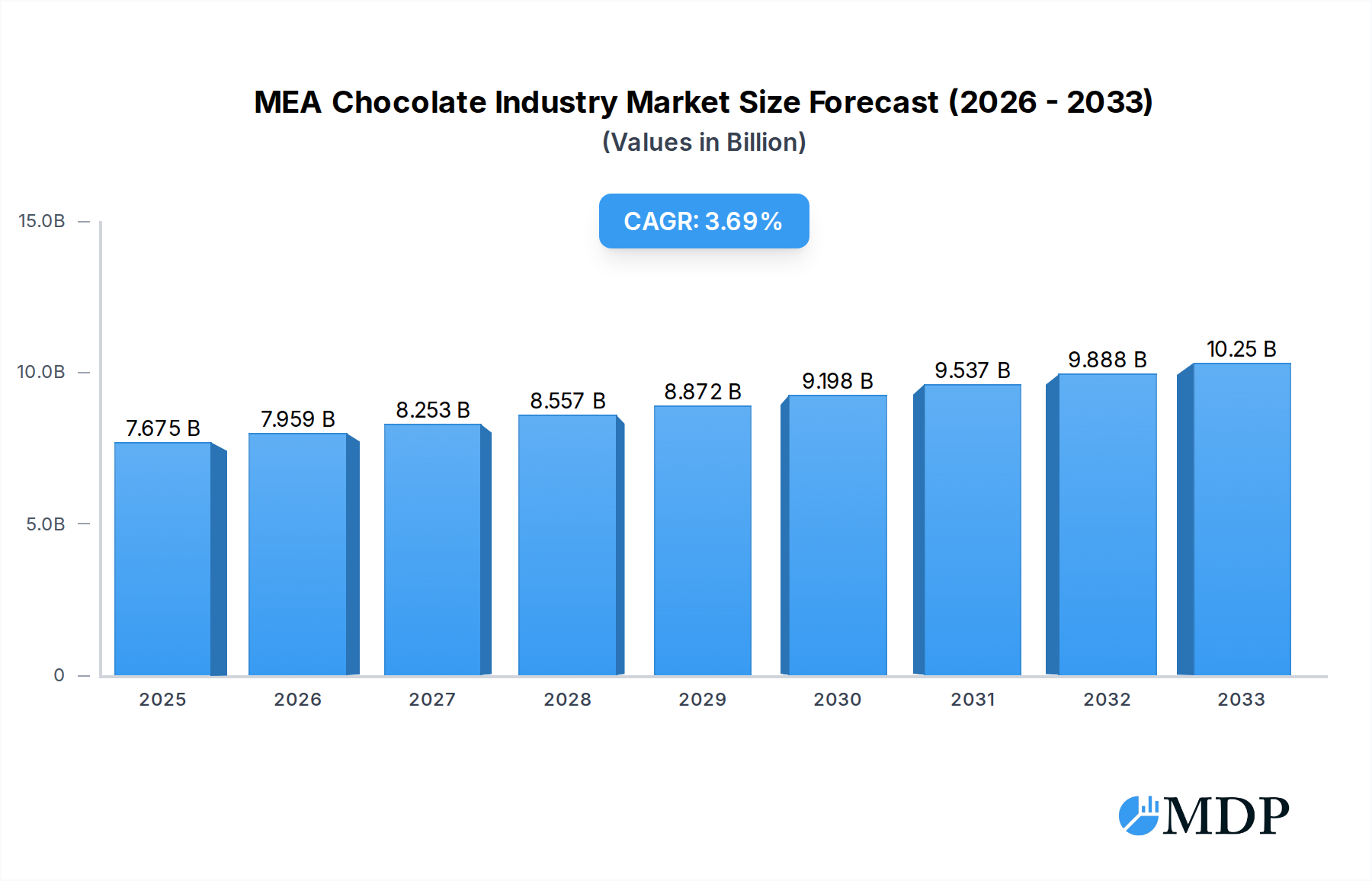

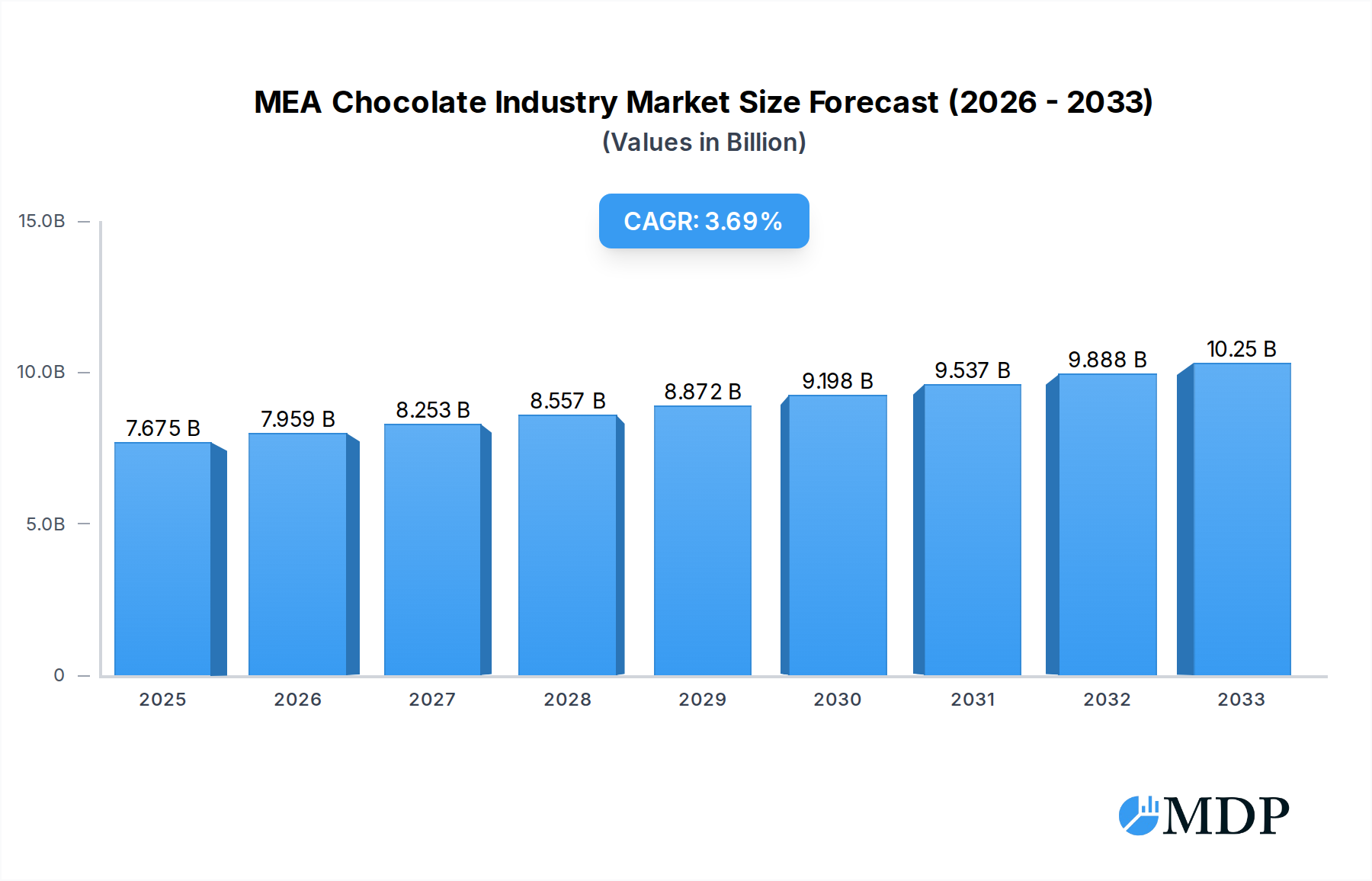

The Middle East and Africa (MEA) chocolate market is poised for robust growth, with an estimated market size of USD 7675.3 million in 2025, expanding at a Compound Annual Growth Rate (CAGR) of 3.7% from 2019 to 2033. This steady expansion is primarily driven by evolving consumer preferences towards premium and indulgence products, coupled with a growing demand for dark chocolate varieties due to perceived health benefits. The increasing disposable income across key economies within the region further fuels this demand. Distribution channels are also undergoing transformation, with online retail stores emerging as a significant growth avenue, complementing traditional channels like supermarkets and hypermarkets. The market is characterized by a diverse product landscape, encompassing boxed assortments, countlines, and seasonal chocolates, catering to a wide array of consumer occasions and preferences.

MEA Chocolate Industry Market Size (In Billion)

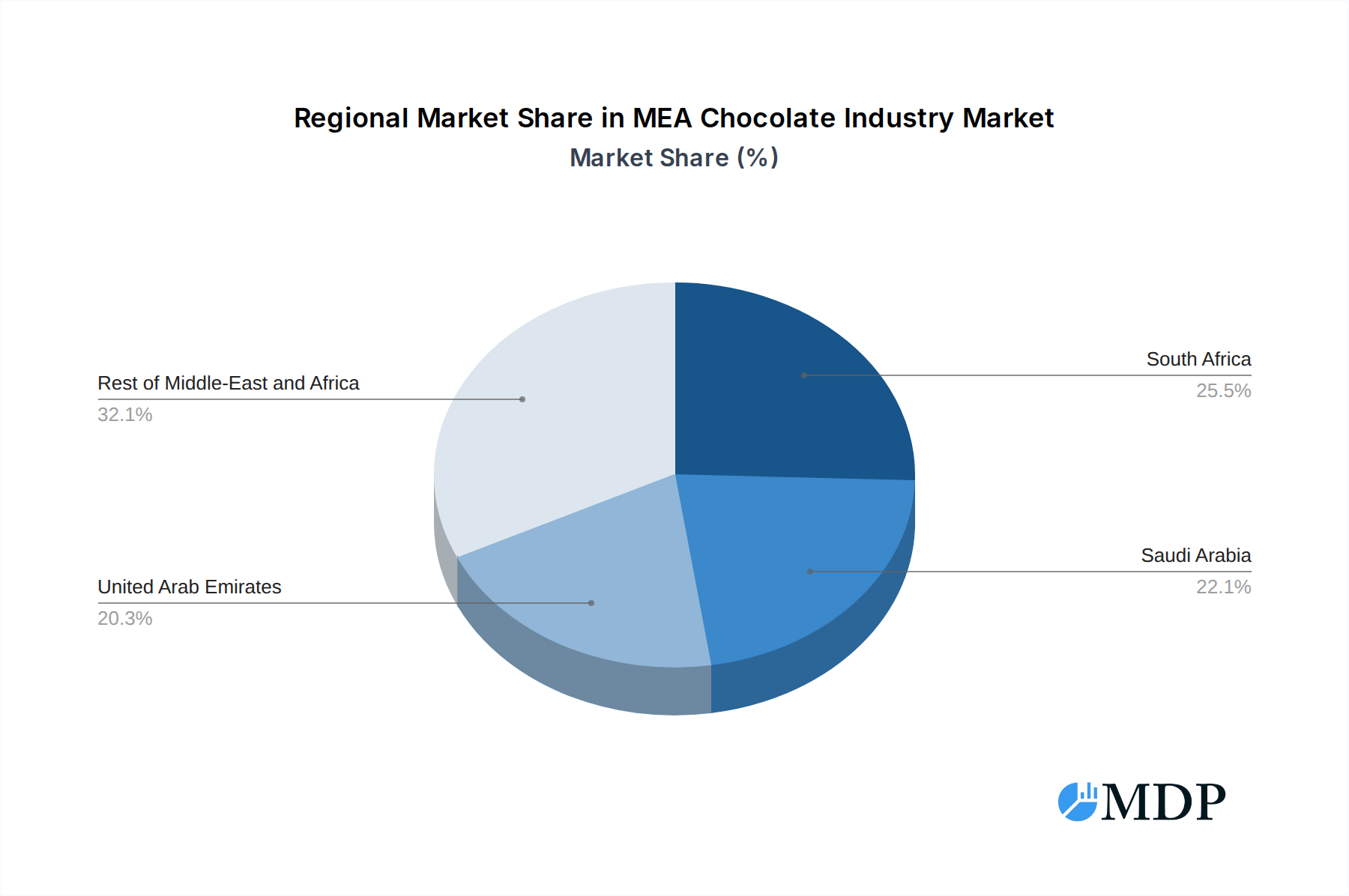

Key growth drivers for the MEA chocolate market include the rising popularity of gifting occasions, increased urbanization, and a growing expatriate population with established chocolate consumption habits. However, challenges such as fluctuating cocoa prices, intense competition, and varying economic conditions across the diverse MEA landscape present potential restraints. The market segments show a significant demand for milk/white chocolate alongside dark chocolate, indicating a preference for a broader taste profile. Geographically, South Africa and the United Arab Emirates are projected to lead market expansion, driven by higher consumer spending and a more developed retail infrastructure. The competitive landscape is dominated by major global players alongside strong local manufacturers, all vying for market share through product innovation and strategic distribution.

MEA Chocolate Industry Company Market Share

MEA Chocolate Industry Report: Market Dynamics, Trends, and Leading Players (2019-2033)

This comprehensive report offers an in-depth analysis of the Middle East and Africa (MEA) chocolate industry, a rapidly evolving market projected to reach xx million by 2033. With a robust CAGR of xx% during the forecast period (2025-2033), the MEA chocolate market is characterized by increasing consumer demand for premium and novel chocolate experiences, driven by rising disposable incomes and a growing awareness of health-conscious options. This report delves into market dynamics, key industry trends, leading segments, product developments, growth drivers, challenges, emerging opportunities, and the strategies of key players, providing actionable insights for stakeholders. The study covers the historical period of 2019-2024, with 2025 serving as both the base and estimated year, and projects growth through 2033.

MEA Chocolate Industry Market Dynamics & Concentration

The MEA chocolate industry exhibits a dynamic market concentration, with a growing emphasis on innovation as a key differentiator. Key players are strategically investing in product development and market penetration to capture a larger share of the burgeoning demand. The regulatory landscape, while varied across countries, is generally supportive of market growth, with a focus on food safety and quality standards. Product substitutes, such as confectionery and other sweet treats, pose a moderate competitive threat, yet the intrinsic appeal of chocolate continues to drive its popularity. End-user trends are notably shifting towards premiumization, with a significant appetite for artisanal, ethically sourced, and healthier chocolate options. Mergers and acquisitions (M&A) activities are expected to remain a significant aspect of market evolution, with xx M&A deals anticipated between 2025 and 2033, aimed at consolidating market presence and expanding product portfolios. Market share is fragmented, with leading companies holding approximately xx% of the total market.

- Market Concentration: Moderately concentrated, with key international players and emerging regional brands vying for market dominance.

- Innovation Drivers: Growing consumer demand for premium, artisanal, and health-conscious chocolate products, alongside technological advancements in chocolate manufacturing.

- Regulatory Frameworks: Generally favorable, with increasing focus on food safety, ingredient transparency, and sustainable sourcing practices.

- Product Substitutes: Confectionery, baked goods, and other sweet snacks.

- End-User Trends: Shift towards premiumization, demand for darker chocolates, sugar-free options, and novel flavor profiles.

- M&A Activities: Expected to rise as companies seek to expand their geographical reach and product offerings.

MEA Chocolate Industry Industry Trends & Analysis

The MEA chocolate industry is on an upward trajectory, fueled by a confluence of evolving consumer preferences and economic development across the region. The increasing disposable incomes in key markets like the United Arab Emirates and Saudi Arabia are directly translating into higher spending on premium and indulgence products, with chocolate being a prime beneficiary. A significant trend is the growing adoption of healthier chocolate options, including dark chocolate with higher cocoa content and products with reduced sugar or natural sweeteners. This aligns with a broader wellness movement sweeping across the region. Technological disruptions are also playing a pivotal role, with advancements in processing, packaging, and online retail enhancing accessibility and consumer experience. The competitive landscape is intensifying, characterized by aggressive product launches, strategic marketing campaigns, and a focus on unique flavor innovations to capture consumer attention. Market penetration for chocolate products is steadily increasing, particularly in urban centers and emerging economies within MEA. The CAGR of xx% underscores the robust growth potential, with the market size projected to expand significantly in the coming years. Companies are investing in sustainable sourcing and ethical practices, recognizing their importance in building brand loyalty and meeting consumer expectations. The proliferation of online retail channels has further democratized access to a wider range of chocolate products, including niche and imported brands, thereby contributing to market expansion.

Leading Markets & Segments in MEA Chocolate Industry

The MEA chocolate industry is experiencing robust growth across various segments, with certain geographical regions and product categories demonstrating exceptional dominance. South Africa continues to be a mature yet significant market, driven by established retail infrastructure and a substantial consumer base. However, the United Arab Emirates (UAE) and Saudi Arabia are emerging as high-growth hotspots, fueled by burgeoning tourism, significant expatriate populations, and a strong demand for premium and luxury goods. The "Rest of Middle-East and Africa" encompasses a vast and diverse set of markets, many of which are in earlier stages of development but represent substantial untapped potential.

In terms of Product categories, Milk/White Chocolate remains the largest segment due to its broad appeal and accessibility. However, Dark Chocolate is witnessing rapid growth, driven by increasing health consciousness and a growing appreciation for complex flavors among consumers. The Type of chocolate product is also evolving, with Boxed Assortments and Seasonal Chocolates maintaining strong appeal for gifting occasions and holidays, while Countlines and Molded Chocolates cater to everyday consumption. The emergence of novel and artisanal chocolate types is also a notable trend.

The Distribution Channel landscape is dominated by Supermarkets/Hypermarkets, which offer wide availability and convenience. Online Retail Stores are rapidly gaining traction, providing consumers with access to a broader selection of products and the convenience of home delivery, especially in urbanized areas. Specialty Stores cater to the premium segment, offering artisanal and niche chocolate brands.

- Dominant Geography: United Arab Emirates and Saudi Arabia are projected to exhibit the highest growth rates due to their strong economies and increasing consumer spending power on premium products. South Africa remains a key market with established players.

- Leading Product Segments: Milk/White Chocolate leads in volume, with Dark Chocolate experiencing the fastest growth.

- Key Product Types: Boxed Assortments and Seasonal Chocolates are significant for gifting, while Countlines and Molded Chocolates drive everyday consumption.

- Dominant Distribution Channels: Supermarkets/Hypermarkets are key for mass distribution, with Online Retail Stores showing rapid expansion, particularly for premium and niche products.

MEA Chocolate Industry Product Developments

Product development in the MEA chocolate industry is characterized by a strong emphasis on innovation driven by consumer preferences for healthier, premium, and unique offerings. Companies are increasingly launching chocolates with reduced sugar content, utilizing natural sweeteners, and incorporating functional ingredients such as antioxidants and probiotics. The demand for dark chocolate with higher cocoa percentages is on the rise, appealing to health-conscious consumers and those seeking sophisticated flavor profiles. Furthermore, there is a significant push towards artisanal and craft chocolates, featuring exotic ingredients, novel flavor combinations, and ethically sourced cocoa. Packaging innovations are also crucial, with a focus on sustainable materials and visually appealing designs that enhance the premium perception of the product. These developments aim to differentiate brands in a competitive market and cater to a discerning consumer base seeking quality and novelty.

Key Drivers of MEA Chocolate Industry Growth

Several interconnected factors are propelling the growth of the MEA chocolate industry. Economically, rising disposable incomes and a growing middle class across key nations like Saudi Arabia and the UAE are significantly increasing consumer spending on premium and indulgence products. Technological advancements in chocolate manufacturing and processing are leading to more efficient production, higher quality products, and the development of novel taste profiles. Furthermore, a growing health and wellness consciousness among consumers is driving demand for dark chocolate, sugar-free options, and chocolates with natural ingredients. E-commerce expansion provides greater accessibility to a wider range of chocolate products, including niche and international brands. Government initiatives promoting foreign investment and economic diversification in many MEA countries also contribute to a more favorable business environment for the chocolate industry.

Challenges in the MEA Chocolate Industry Market

Despite its strong growth potential, the MEA chocolate industry faces several significant challenges. Fluctuations in the price and availability of raw materials, particularly cocoa beans, can impact production costs and profit margins. Supply chain disruptions, exacerbated by logistical complexities and infrastructure limitations in certain regions, can affect product distribution and lead to increased costs. Intense competition from both established global brands and emerging local players necessitates continuous innovation and aggressive marketing strategies. Regulatory hurdles and varying import duties across different MEA countries can also pose challenges for market entry and expansion. Consumer price sensitivity, especially in less affluent markets, can limit the adoption of premium-priced chocolate products.

Emerging Opportunities in MEA Chocolate Industry

The MEA chocolate industry is ripe with emerging opportunities for growth and expansion. The burgeoning demand for premium and artisanal chocolates presents a significant avenue for brands focusing on unique flavors, high-quality ingredients, and appealing storytelling. The increasing consumer awareness regarding health and wellness is creating a substantial market for sugar-free, dark chocolate, and functional chocolate products. Strategic partnerships with local distributors and retailers can unlock access to untapped markets within the vast African continent and the Middle East. Furthermore, the development of e-commerce platforms and direct-to-consumer (DTC) models offers a direct channel to reach a wider customer base and gather valuable consumer insights. Investment in sustainable sourcing practices and ethical production can build brand loyalty and appeal to a growing segment of socially conscious consumers.

Leading Players in the MEA Chocolate Industry Sector

- Nestle SA

- Tiger Brands Limited

- Barry Callebaut

- Ferrero Group

- Chocoladefabriken Lindt & Sprungli AG

- Mars Incorporated

- Mondelez International Inc

- Cocoa Processing Company Limited

- Kees Beyers Chocolate CC

- The Hershey Company

Key Milestones in MEA Chocolate Industry Industry

- March 2022: Barry Callebaut launched its line of whole-fruit chocolates under the Cacao Barry brand in the United Arab Emirates. This product, containing 40% less sugar and made from 100% pure cacao fruit, was a result of a partnership with Cabosse Naturals, focusing on upcycled cacao fruit pulp and peels from Ecuador, highlighting innovation in sustainable ingredients.

- February 2022: Made By Two, a Dubai-based artisanal chocolate boutique, unveiled its collection of glazed luxury chocolates. Influenced by art and design, these chocolates featured novel flavors, vibrant colors, and intricate craftsmanship, catering to the premium segment of the market.

- October 2021: Barry Callebaut inaugurated a new Chocolate Academy at the foot of Burj Khalifa in Dubai, United Arab Emirates. This facility, the 24th globally, serves as a crucial platform for chefs and artisans to enhance their skills and foster innovation, responding to a shift in consumer preference towards premium and diverse chocolate varieties.

Strategic Outlook for MEA Chocolate Industry Market

The strategic outlook for the MEA chocolate industry is exceptionally positive, driven by sustained economic growth and evolving consumer preferences. Key growth accelerators include the continued demand for premium and artisanal chocolates, alongside a rising interest in healthier alternatives like dark chocolate and sugar-free options. Companies are expected to leverage technological advancements in production and distribution, with e-commerce playing an increasingly vital role in market penetration. Strategic partnerships and potential mergers and acquisitions will be crucial for consolidating market share and expanding product portfolios. Focus on sustainable sourcing and ethical practices will be paramount in building brand equity and appealing to the modern consumer. The untapped potential within various African markets presents significant long-term growth opportunities, necessitating tailored market entry strategies.

MEA Chocolate Industry Segmentation

-

1. Product

- 1.1. Dark Chocolate

- 1.2. Milk/ White Chocolate

-

2. Type

- 2.1. Boxed Assortments

- 2.2. Countlines

- 2.3. Seasonal Chocolates

- 2.4. Molded Chocolates

- 2.5. Other Product Types

-

3. Distribution Channel

- 3.1. Supermarkets/ Hypermarkets

- 3.2. Specialty Stores

- 3.3. Convenience/Grocery Stores

- 3.4. Online Retail Stores

- 3.5. Other Distribution Channels

-

4. Geography

- 4.1. South Africa

- 4.2. Saudi Arabia

- 4.3. United Arab Emirates

- 4.4. Rest of Middle-East and Africa

MEA Chocolate Industry Segmentation By Geography

- 1. South Africa

- 2. Saudi Arabia

- 3. United Arab Emirates

- 4. Rest of Middle East and Africa

MEA Chocolate Industry Regional Market Share

Geographic Coverage of MEA Chocolate Industry

MEA Chocolate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Dark Chocolate

- 5.1.2. Milk/ White Chocolate

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Boxed Assortments

- 5.2.2. Countlines

- 5.2.3. Seasonal Chocolates

- 5.2.4. Molded Chocolates

- 5.2.5. Other Product Types

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Supermarkets/ Hypermarkets

- 5.3.2. Specialty Stores

- 5.3.3. Convenience/Grocery Stores

- 5.3.4. Online Retail Stores

- 5.3.5. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. South Africa

- 5.4.2. Saudi Arabia

- 5.4.3. United Arab Emirates

- 5.4.4. Rest of Middle-East and Africa

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. South Africa

- 5.5.2. Saudi Arabia

- 5.5.3. United Arab Emirates

- 5.5.4. Rest of Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global MEA Chocolate Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Dark Chocolate

- 6.1.2. Milk/ White Chocolate

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Boxed Assortments

- 6.2.2. Countlines

- 6.2.3. Seasonal Chocolates

- 6.2.4. Molded Chocolates

- 6.2.5. Other Product Types

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Supermarkets/ Hypermarkets

- 6.3.2. Specialty Stores

- 6.3.3. Convenience/Grocery Stores

- 6.3.4. Online Retail Stores

- 6.3.5. Other Distribution Channels

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. South Africa

- 6.4.2. Saudi Arabia

- 6.4.3. United Arab Emirates

- 6.4.4. Rest of Middle-East and Africa

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. South Africa MEA Chocolate Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Dark Chocolate

- 7.1.2. Milk/ White Chocolate

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Boxed Assortments

- 7.2.2. Countlines

- 7.2.3. Seasonal Chocolates

- 7.2.4. Molded Chocolates

- 7.2.5. Other Product Types

- 7.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.3.1. Supermarkets/ Hypermarkets

- 7.3.2. Specialty Stores

- 7.3.3. Convenience/Grocery Stores

- 7.3.4. Online Retail Stores

- 7.3.5. Other Distribution Channels

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. South Africa

- 7.4.2. Saudi Arabia

- 7.4.3. United Arab Emirates

- 7.4.4. Rest of Middle-East and Africa

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Saudi Arabia MEA Chocolate Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Dark Chocolate

- 8.1.2. Milk/ White Chocolate

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Boxed Assortments

- 8.2.2. Countlines

- 8.2.3. Seasonal Chocolates

- 8.2.4. Molded Chocolates

- 8.2.5. Other Product Types

- 8.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.3.1. Supermarkets/ Hypermarkets

- 8.3.2. Specialty Stores

- 8.3.3. Convenience/Grocery Stores

- 8.3.4. Online Retail Stores

- 8.3.5. Other Distribution Channels

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. South Africa

- 8.4.2. Saudi Arabia

- 8.4.3. United Arab Emirates

- 8.4.4. Rest of Middle-East and Africa

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. United Arab Emirates MEA Chocolate Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Dark Chocolate

- 9.1.2. Milk/ White Chocolate

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Boxed Assortments

- 9.2.2. Countlines

- 9.2.3. Seasonal Chocolates

- 9.2.4. Molded Chocolates

- 9.2.5. Other Product Types

- 9.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.3.1. Supermarkets/ Hypermarkets

- 9.3.2. Specialty Stores

- 9.3.3. Convenience/Grocery Stores

- 9.3.4. Online Retail Stores

- 9.3.5. Other Distribution Channels

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. South Africa

- 9.4.2. Saudi Arabia

- 9.4.3. United Arab Emirates

- 9.4.4. Rest of Middle-East and Africa

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Rest of Middle East and Africa MEA Chocolate Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Dark Chocolate

- 10.1.2. Milk/ White Chocolate

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Boxed Assortments

- 10.2.2. Countlines

- 10.2.3. Seasonal Chocolates

- 10.2.4. Molded Chocolates

- 10.2.5. Other Product Types

- 10.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.3.1. Supermarkets/ Hypermarkets

- 10.3.2. Specialty Stores

- 10.3.3. Convenience/Grocery Stores

- 10.3.4. Online Retail Stores

- 10.3.5. Other Distribution Channels

- 10.4. Market Analysis, Insights and Forecast - by Geography

- 10.4.1. South Africa

- 10.4.2. Saudi Arabia

- 10.4.3. United Arab Emirates

- 10.4.4. Rest of Middle-East and Africa

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Nestle SA

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Tiger Brands Limited

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Barry Callebaut

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Ferrero Group

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Chocoladefabriken Lindt & Sprungli AG

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Mars Incorporated

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Mondelez International Inc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Cocoa Processing Company Limited

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Kees Beyers Chocolate CC*List Not Exhaustive

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 The Hershey Company

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Nestle SA

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global MEA Chocolate Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: South Africa MEA Chocolate Industry Revenue (billion), by Product 2025 & 2033

- Figure 3: South Africa MEA Chocolate Industry Revenue Share (%), by Product 2025 & 2033

- Figure 4: South Africa MEA Chocolate Industry Revenue (billion), by Type 2025 & 2033

- Figure 5: South Africa MEA Chocolate Industry Revenue Share (%), by Type 2025 & 2033

- Figure 6: South Africa MEA Chocolate Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 7: South Africa MEA Chocolate Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 8: South Africa MEA Chocolate Industry Revenue (billion), by Geography 2025 & 2033

- Figure 9: South Africa MEA Chocolate Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 10: South Africa MEA Chocolate Industry Revenue (billion), by Country 2025 & 2033

- Figure 11: South Africa MEA Chocolate Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Saudi Arabia MEA Chocolate Industry Revenue (billion), by Product 2025 & 2033

- Figure 13: Saudi Arabia MEA Chocolate Industry Revenue Share (%), by Product 2025 & 2033

- Figure 14: Saudi Arabia MEA Chocolate Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Saudi Arabia MEA Chocolate Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Saudi Arabia MEA Chocolate Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 17: Saudi Arabia MEA Chocolate Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 18: Saudi Arabia MEA Chocolate Industry Revenue (billion), by Geography 2025 & 2033

- Figure 19: Saudi Arabia MEA Chocolate Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 20: Saudi Arabia MEA Chocolate Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Saudi Arabia MEA Chocolate Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: United Arab Emirates MEA Chocolate Industry Revenue (billion), by Product 2025 & 2033

- Figure 23: United Arab Emirates MEA Chocolate Industry Revenue Share (%), by Product 2025 & 2033

- Figure 24: United Arab Emirates MEA Chocolate Industry Revenue (billion), by Type 2025 & 2033

- Figure 25: United Arab Emirates MEA Chocolate Industry Revenue Share (%), by Type 2025 & 2033

- Figure 26: United Arab Emirates MEA Chocolate Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 27: United Arab Emirates MEA Chocolate Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 28: United Arab Emirates MEA Chocolate Industry Revenue (billion), by Geography 2025 & 2033

- Figure 29: United Arab Emirates MEA Chocolate Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 30: United Arab Emirates MEA Chocolate Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: United Arab Emirates MEA Chocolate Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Rest of Middle East and Africa MEA Chocolate Industry Revenue (billion), by Product 2025 & 2033

- Figure 33: Rest of Middle East and Africa MEA Chocolate Industry Revenue Share (%), by Product 2025 & 2033

- Figure 34: Rest of Middle East and Africa MEA Chocolate Industry Revenue (billion), by Type 2025 & 2033

- Figure 35: Rest of Middle East and Africa MEA Chocolate Industry Revenue Share (%), by Type 2025 & 2033

- Figure 36: Rest of Middle East and Africa MEA Chocolate Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 37: Rest of Middle East and Africa MEA Chocolate Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 38: Rest of Middle East and Africa MEA Chocolate Industry Revenue (billion), by Geography 2025 & 2033

- Figure 39: Rest of Middle East and Africa MEA Chocolate Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 40: Rest of Middle East and Africa MEA Chocolate Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Rest of Middle East and Africa MEA Chocolate Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global MEA Chocolate Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 2: Global MEA Chocolate Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global MEA Chocolate Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: Global MEA Chocolate Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 5: Global MEA Chocolate Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global MEA Chocolate Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 7: Global MEA Chocolate Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global MEA Chocolate Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 9: Global MEA Chocolate Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 10: Global MEA Chocolate Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Global MEA Chocolate Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 12: Global MEA Chocolate Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 13: Global MEA Chocolate Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 14: Global MEA Chocolate Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 15: Global MEA Chocolate Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global MEA Chocolate Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 17: Global MEA Chocolate Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global MEA Chocolate Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 19: Global MEA Chocolate Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 20: Global MEA Chocolate Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Global MEA Chocolate Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 22: Global MEA Chocolate Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 23: Global MEA Chocolate Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 24: Global MEA Chocolate Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 25: Global MEA Chocolate Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the MEA Chocolate Industry?

The projected CAGR is approximately 4.9%.

2. Which companies are prominent players in the MEA Chocolate Industry?

Key companies in the market include Nestle SA, Tiger Brands Limited, Barry Callebaut, Ferrero Group, Chocoladefabriken Lindt & Sprungli AG, Mars Incorporated, Mondelez International Inc, Cocoa Processing Company Limited, Kees Beyers Chocolate CC*List Not Exhaustive, The Hershey Company.

3. What are the main segments of the MEA Chocolate Industry?

The market segments include Product, Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 127.1 billion as of 2022.

5. What are some drivers contributing to market growth?

Government Initiatives and E-commerce Penetration.

6. What are the notable trends driving market growth?

Countlines and Premium Dark Chocolates Hold a Major Market Share.

7. Are there any restraints impacting market growth?

Detrimental Health Impact of Caffeine Intake.

8. Can you provide examples of recent developments in the market?

In March 2022, Barry Callebaut launched its line of whole-fruit chocolates under the Cacao Barry brand in the United Arab Emirates. The product has 40% less sugar than conventional dark chocolate and is made from 100% pure cacao fruit. The company partnered with Cabosse Naturals, who work closely with local cacao fruit farmers in Ecuador, to source the upcycled cacao fruit pulp and peels for the product.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "MEA Chocolate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the MEA Chocolate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the MEA Chocolate Industry?

To stay informed about further developments, trends, and reports in the MEA Chocolate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence