Key Insights

The global Soy-Based Foods market is experiencing robust growth, projected to reach a significant valuation by 2033. Driven by increasing consumer demand for plant-based alternatives, health-conscious eating, and ethical considerations regarding animal agriculture, the market is poised for expansion. The rising awareness of soy's nutritional benefits, including its protein content and potential to lower cholesterol, further fuels this demand. Furthermore, innovations in food technology are leading to more appealing and diverse soy-based products, from flavorful meat substitutes that mimic traditional textures to creamy, dairy-free ice creams and cheeses. This product diversification is crucial in attracting a wider consumer base, including flexitarians and those with lactose intolerance or dairy allergies. The convenience offered by readily available soy products in various retail channels, from hypermarkets to online platforms, also contributes to market penetration and accessibility.

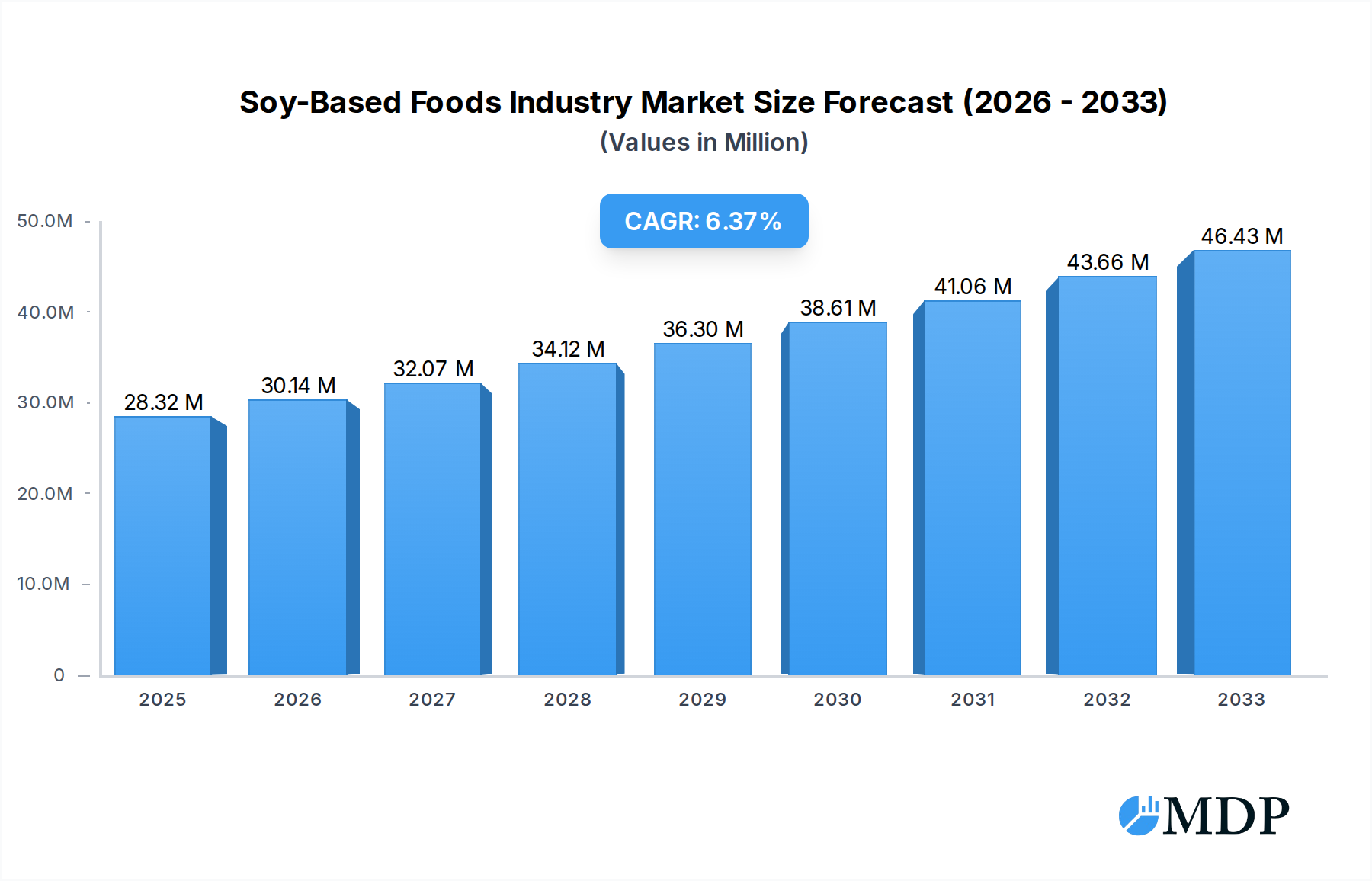

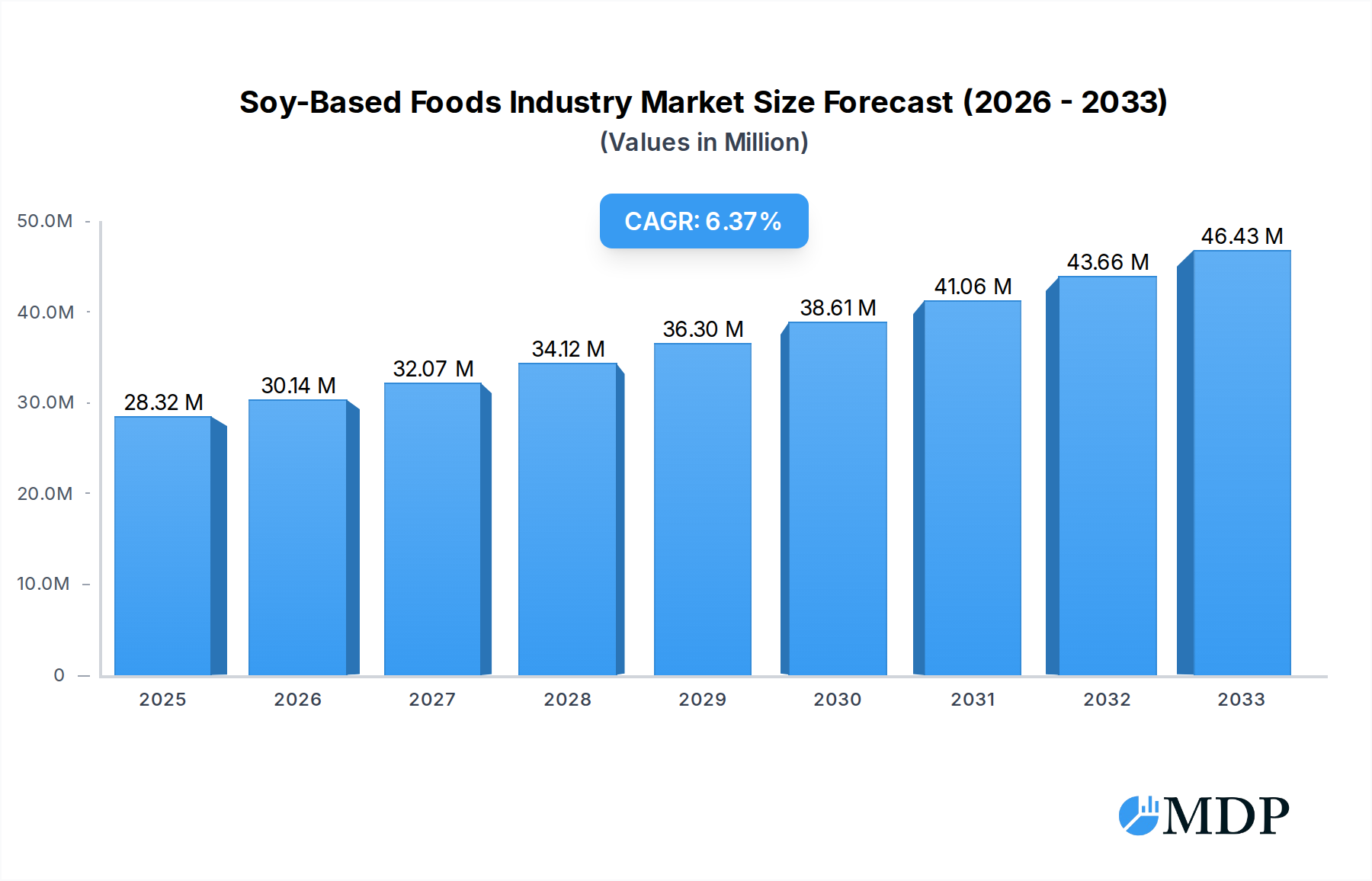

Soy-Based Foods Industry Market Size (In Million)

The market size of the Soy-Based Foods industry is estimated at $28.32 million in 2025, exhibiting a compelling Compound Annual Growth Rate (CAGR) of 6.45% throughout the forecast period of 2025-2033. This impressive growth trajectory is propelled by a confluence of factors, including the expanding vegan and vegetarian populations globally, a growing concern for environmental sustainability, and the increasing availability of a wide array of soy-based products. Key market drivers include the perceived health benefits associated with soy consumption, such as its rich protein profile and potential for cardiovascular health, alongside its versatility in culinary applications. Emerging trends like the development of novel soy protein isolates and textured soy protein for enhanced taste and texture in meat alternatives are shaping consumer preferences. However, potential market restraints, such as fluctuating raw material prices and consumer perceptions regarding genetically modified soy, necessitate strategic management by industry players. The market is segmented into distinct product categories, with Meat Substitutes, Non-Dairy Ice Cream, Non-Dairy Cheese, Non-Dairy Yogurt, and Non-Dairy Spreads each contributing to the overall market dynamism. Distribution channels like Hypermarkets/Supermarkets, Convenience Stores, and Online Retail Stores are instrumental in reaching a broad consumer base across key regions like North America, Europe, and Asia Pacific.

Soy-Based Foods Industry Company Market Share

Soy-Based Foods Industry Report: Comprehensive Market Analysis & Forecast 2019-2033

This in-depth report provides a panoramic view of the global Soy-Based Foods Industry, offering critical insights for stakeholders seeking to navigate this dynamic and rapidly expanding market. Spanning the historical period from 2019 to 2024, with a base year of 2025 and a forecast extending to 2033, this analysis delves into market dynamics, key trends, leading segments, product innovations, growth drivers, challenges, and emerging opportunities. With an estimated market size of over $XX Million in 2025, projected to reach $XX Million by 2033, and a Compound Annual Growth Rate (CAGR) of approximately XX%, this report is an indispensable resource for manufacturers, suppliers, investors, and policymakers.

Soy-Based Foods Industry Market Dynamics & Concentration

The Soy-Based Foods Industry is characterized by moderate to high market concentration, with several key players dominating significant market shares. Innovation drivers are primarily fueled by increasing consumer demand for plant-based alternatives, driven by health consciousness and environmental concerns. Regulatory frameworks, particularly concerning food labeling and ingredient transparency, play a crucial role in shaping market entry and product development. Product substitutes, including other plant-based proteins like pea and almond, pose a competitive challenge. End-user trends reveal a growing preference for convenient, ready-to-eat soy-based products and a significant uptake in online retail channels. Mergers and acquisitions (M&A) activities are present, with companies seeking to expand their product portfolios and market reach. For instance, there have been approximately XX M&A deals recorded between 2019 and 2024, aiming to consolidate market position and acquire innovative technologies. Major companies hold substantial market shares, with Nestle SA and Vitasoy International Holdings Ltd often leading in specific product categories.

Soy-Based Foods Industry Industry Trends & Analysis

The Soy-Based Foods Industry is witnessing robust growth, propelled by a confluence of factors including rising health awareness, environmental sustainability concerns, and dietary shifts towards plant-based eating. The market penetration of soy-based products is steadily increasing, with consumers actively seeking alternatives to traditional animal-based proteins. Technological disruptions are at the forefront, with advancements in processing techniques enhancing the texture, flavor, and nutritional profile of soy-based foods, making them more appealing to a wider consumer base. For example, extrusion technology has significantly improved the meat-like texture of Textured Vegetable Protein (TVP). Consumer preferences are evolving, with a growing demand for organic, non-GMO, and minimally processed soy-based options. Competitive dynamics are intensifying, with both established food giants and agile startups vying for market share. The CAGR of XX% over the forecast period underscores the industry's strong upward trajectory. Key market growth drivers include the rising prevalence of veganism and vegetarianism, coupled with the growing acceptance of flexitarian diets. The perceived health benefits of soy, such as its protein content and potential for cholesterol reduction, continue to attract health-conscious consumers. Furthermore, increasing government initiatives promoting healthy eating and sustainable food production indirectly benefit the soy-based foods sector. The development of novel soy-based products, such as those mimicking the taste and texture of traditional meats more closely, is also a significant trend. The global market is estimated to be valued at over $XX Million in the base year of 2025.

Leading Markets & Segments in Soy-Based Foods Industry

The global Soy-Based Foods Industry is segmented across various product types and distribution channels, with each segment exhibiting distinct growth patterns and market dominance.

Product Type Dominance:

- Meat Substitutes: This segment, encompassing Textured Vegetable Protein (TVP), Tofu, and Tempeh, is a significant driver of the industry's growth. The increasing demand for plant-based protein due to health and ethical reasons has propelled this category to the forefront. TVP, in particular, benefits from its versatility and affordability in mimicking meat textures.

- Key Drivers:

- Growing vegan and vegetarian populations worldwide.

- Rising awareness of the environmental impact of meat consumption.

- Innovations in creating more palatable and texturally diverse meat analogues.

- Influence of flexitarian diets.

- Key Drivers:

- Non-Dairy Ice Cream: This segment has experienced substantial growth due to lactose intolerance and a preference for plant-based desserts. The availability of diverse flavors and textures is crucial for its market penetration.

- Key Drivers:

- Increasing disposable incomes in emerging economies.

- Expansion of flavor profiles and artisanal offerings.

- Availability of soy milk as a stable and cost-effective base.

- Key Drivers:

- Non-Dairy Cheese: While still a developing segment, non-dairy cheese is gaining traction as consumers seek dairy-free alternatives. Product innovation is key to overcoming taste and meltability challenges.

- Key Drivers:

- Growing demand for vegan and dairy-free options in processed foods.

- Improvements in manufacturing processes for better texture and flavor.

- Key Drivers:

- Non-Dairy Yogurt: This segment is well-established, offering a healthier alternative to dairy yogurt for consumers with lactose intolerance or those pursuing plant-based diets.

- Key Drivers:

- Probiotic fortification and perceived health benefits.

- Wide variety of flavors and fruit inclusions.

- Key Drivers:

- Non-Dairy Spread: This category, including soy-based margarines and butter alternatives, benefits from the overall trend towards plant-based diets and a reduction in saturated fats.

- Key Drivers:

- Health benefits associated with reduced cholesterol.

- Versatility in culinary applications.

- Key Drivers:

Distribution Channel Dominance:

- Hypermarkets/Supermarkets: These remain the primary distribution channel for soy-based foods, offering wide product availability and competitive pricing. The extensive reach and consumer traffic make them crucial for market penetration.

- Key Drivers:

- Convenience and one-stop shopping experience.

- Promotional activities and discounts.

- Shelf space and visibility for product discovery.

- Key Drivers:

- Online Retail Stores: The e-commerce segment is rapidly growing, driven by consumer convenience, wider selection, and the ability to access niche or specialty soy-based products.

- Key Drivers:

- Increasing internet penetration and smartphone usage.

- Growth of online grocery delivery services.

- Personalized recommendations and subscription models.

- Key Drivers:

- Convenience Stores: These cater to impulse purchases and on-the-go consumption, with a growing presence of ready-to-eat soy-based snacks and meals.

- Key Drivers:

- Strategic locations in high-traffic areas.

- Demand for quick meal solutions.

- Key Drivers:

- Other Distribution Channels: This includes specialty food stores, health food stores, and food service providers, which cater to specific consumer segments and offer premium or niche soy-based products.

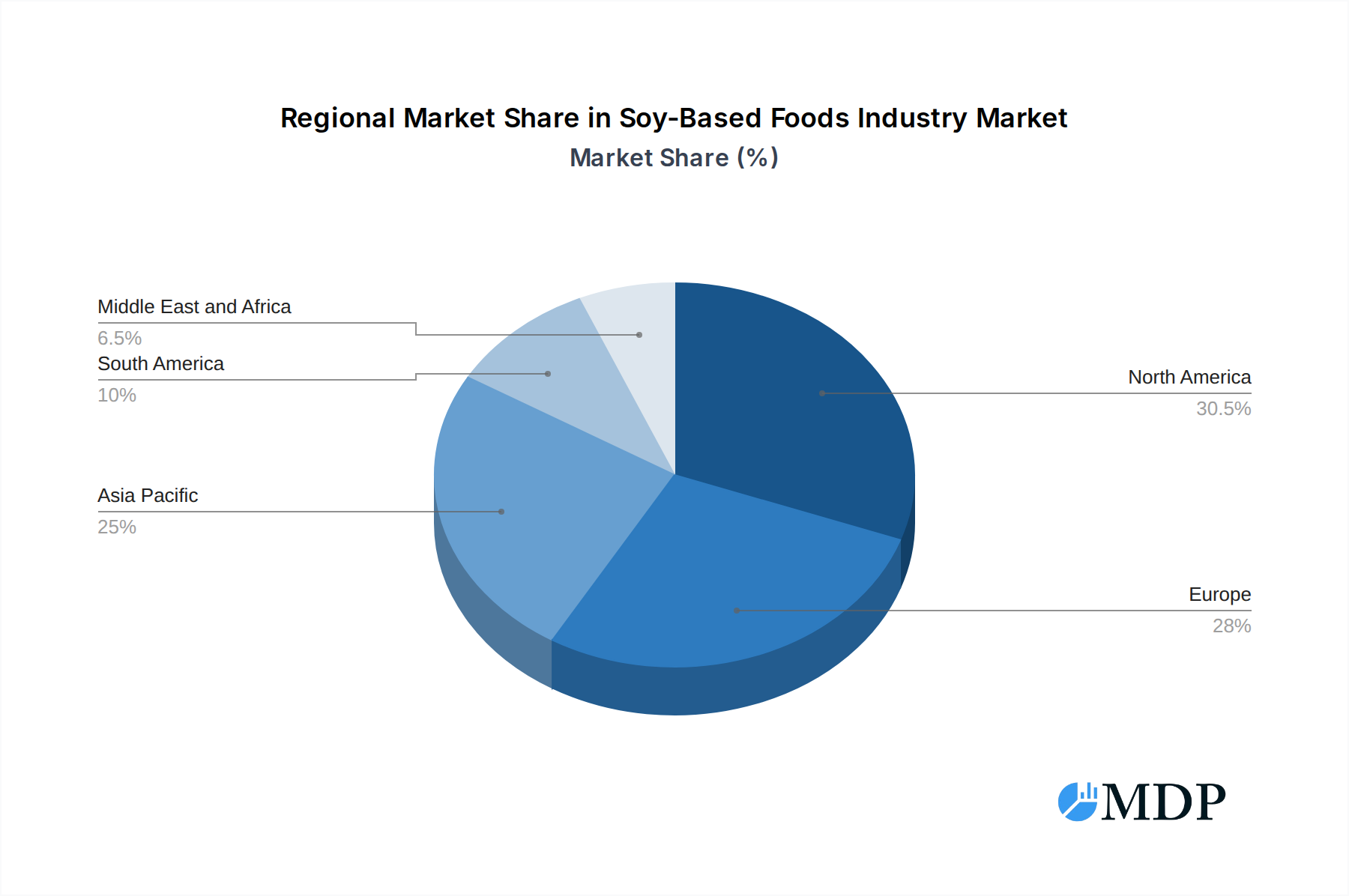

The dominant region for soy-based foods is Asia-Pacific, owing to its traditional consumption of soy products, followed by North America and Europe, which are experiencing rapid growth driven by increasing adoption of plant-based diets.

Soy-Based Foods Industry Product Developments

Product innovation in the Soy-Based Foods Industry focuses on enhancing sensory attributes, nutritional profiles, and convenience. Companies are investing in advanced texturization technologies to create meat substitutes that closely mimic the taste, texture, and cooking experience of animal proteins. The development of novel ingredients derived from soy, such as fermented soy products with improved digestibility and enhanced umami flavors, is a key trend. Furthermore, the market is witnessing a rise in fortified soy-based products, incorporating essential vitamins and minerals to meet specific dietary needs. These advancements, driven by consumer demand for healthier and more sustainable food options, provide significant competitive advantages and expand the applicability of soy-based ingredients across various food categories.

Key Drivers of Soy-Based Foods Industry Growth

The Soy-Based Foods Industry's growth is propelled by several critical factors. Technologically, advancements in food processing, particularly in texturization and flavor encapsulation, are creating more appealing and versatile soy-based products. Economically, the rising disposable incomes in emerging markets and a growing awareness of the cost-effectiveness of plant-based proteins contribute significantly. Regulatory factors, such as government initiatives promoting healthy eating and sustainable agriculture, indirectly foster the adoption of soy-based foods. Consumer demand for healthier alternatives to animal protein, driven by concerns about chronic diseases and ethical considerations, is a paramount driver.

Challenges in the Soy-Based Foods Industry Market

Despite its strong growth, the Soy-Based Foods Industry faces several challenges. Regulatory hurdles, including complex labeling requirements and differing food safety standards across regions, can impede market entry and product diversification. Supply chain issues, such as ensuring consistent quality and availability of non-GMO soybeans and managing price volatility, can impact production costs. Competitive pressures are intense, with a growing array of plant-based alternatives from other sources like peas, almonds, and oats, as well as conventional food manufacturers entering the market. Furthermore, consumer perception regarding taste and texture, though improving, can still be a barrier for widespread adoption.

Emerging Opportunities in Soy-Based Foods Industry

Emerging opportunities in the Soy-Based Foods Industry are significant and diverse. Technological breakthroughs in fermentation and precision agriculture are paving the way for novel soy-derived ingredients with enhanced nutritional benefits and unique functionalities. Strategic partnerships between ingredient suppliers, food manufacturers, and retailers are crucial for expanding product reach and consumer education. Market expansion into untapped geographical regions, particularly those with a growing middle class and increasing interest in health and sustainability, presents substantial growth potential. Furthermore, the development of soy-based products catering to specific dietary needs, such as allergen-free formulations and high-protein, low-carbohydrate options, will capture niche market segments.

Leading Players in the Soy-Based Foods Industry Sector

- Nestle SA

- Vitasoy International Holdings Ltd

- The Amy's Kitche

- Unilever PLC

- Conagra Brands Inc

- Danone SA

- Monde Nissin Corporation

- Impossible Foods Inc

- Hain Celestial Group

- Good Catch Foods

Key Milestones in Soy-Based Foods Industry Industry

- 2019: Increased investment in plant-based food R&D by major food corporations.

- 2020: Significant surge in consumer demand for plant-based alternatives due to health and environmental concerns.

- 2021: Expansion of retail availability for a wider range of soy-based meat and dairy alternatives.

- 2022: Introduction of next-generation soy-based meat substitutes with improved texture and flavor profiles.

- 2023: Growing focus on sustainable sourcing and transparent labeling of soy-based products.

- 2024: Further development in fermentation technologies for enhanced soy ingredient functionality.

Strategic Outlook for Soy-Based Foods Industry Market

The strategic outlook for the Soy-Based Foods Industry market is overwhelmingly positive, fueled by persistent consumer trends and ongoing innovation. Growth accelerators include the continued demand for plant-based diets, driven by health, ethical, and environmental considerations. The industry will witness further investment in product development to enhance taste, texture, and nutritional value, making soy-based options more competitive with traditional animal products. Expansion into emerging markets and the development of specialized product lines targeting diverse consumer needs, such as sports nutrition and convenience foods, will also drive growth. Strategic collaborations and acquisitions are expected to continue as companies seek to consolidate their market position and access new technologies and distribution networks. The integration of AI and advanced analytics in understanding consumer preferences will further refine product offerings and marketing strategies, ensuring sustained market expansion.

Soy-Based Foods Industry Segmentation

-

1. Product Type

-

1.1. Meat Substitutes

- 1.1.1. Textured Vegetable Protein

- 1.1.2. Tofu

- 1.1.3. Tempeh

- 1.2. Non-Dairy Ice Cream

- 1.3. Non-Dairy Cheese

- 1.4. Non-Dairy Yogurt

- 1.5. Non-Dairy Spread

-

1.1. Meat Substitutes

-

2. Distribution Channel

- 2.1. Hypermarkets/Supermarkets

- 2.2. Convenience Stores

- 2.3. Online Retail Stores

- 2.4. Other Distribution Channel

Soy-Based Foods Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Russia

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. Japan

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. Saudi Arabia

- 5.3. Rest of Middle East and Africa

Soy-Based Foods Industry Regional Market Share

Geographic Coverage of Soy-Based Foods Industry

Soy-Based Foods Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.45% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Meat Substitutes

- 5.1.1.1. Textured Vegetable Protein

- 5.1.1.2. Tofu

- 5.1.1.3. Tempeh

- 5.1.2. Non-Dairy Ice Cream

- 5.1.3. Non-Dairy Cheese

- 5.1.4. Non-Dairy Yogurt

- 5.1.5. Non-Dairy Spread

- 5.1.1. Meat Substitutes

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Hypermarkets/Supermarkets

- 5.2.2. Convenience Stores

- 5.2.3. Online Retail Stores

- 5.2.4. Other Distribution Channel

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Soy-Based Foods Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Meat Substitutes

- 6.1.1.1. Textured Vegetable Protein

- 6.1.1.2. Tofu

- 6.1.1.3. Tempeh

- 6.1.2. Non-Dairy Ice Cream

- 6.1.3. Non-Dairy Cheese

- 6.1.4. Non-Dairy Yogurt

- 6.1.5. Non-Dairy Spread

- 6.1.1. Meat Substitutes

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Hypermarkets/Supermarkets

- 6.2.2. Convenience Stores

- 6.2.3. Online Retail Stores

- 6.2.4. Other Distribution Channel

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Soy-Based Foods Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Meat Substitutes

- 7.1.1.1. Textured Vegetable Protein

- 7.1.1.2. Tofu

- 7.1.1.3. Tempeh

- 7.1.2. Non-Dairy Ice Cream

- 7.1.3. Non-Dairy Cheese

- 7.1.4. Non-Dairy Yogurt

- 7.1.5. Non-Dairy Spread

- 7.1.1. Meat Substitutes

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Hypermarkets/Supermarkets

- 7.2.2. Convenience Stores

- 7.2.3. Online Retail Stores

- 7.2.4. Other Distribution Channel

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Soy-Based Foods Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Meat Substitutes

- 8.1.1.1. Textured Vegetable Protein

- 8.1.1.2. Tofu

- 8.1.1.3. Tempeh

- 8.1.2. Non-Dairy Ice Cream

- 8.1.3. Non-Dairy Cheese

- 8.1.4. Non-Dairy Yogurt

- 8.1.5. Non-Dairy Spread

- 8.1.1. Meat Substitutes

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Hypermarkets/Supermarkets

- 8.2.2. Convenience Stores

- 8.2.3. Online Retail Stores

- 8.2.4. Other Distribution Channel

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Pacific Soy-Based Foods Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Meat Substitutes

- 9.1.1.1. Textured Vegetable Protein

- 9.1.1.2. Tofu

- 9.1.1.3. Tempeh

- 9.1.2. Non-Dairy Ice Cream

- 9.1.3. Non-Dairy Cheese

- 9.1.4. Non-Dairy Yogurt

- 9.1.5. Non-Dairy Spread

- 9.1.1. Meat Substitutes

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Hypermarkets/Supermarkets

- 9.2.2. Convenience Stores

- 9.2.3. Online Retail Stores

- 9.2.4. Other Distribution Channel

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. South America Soy-Based Foods Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Meat Substitutes

- 10.1.1.1. Textured Vegetable Protein

- 10.1.1.2. Tofu

- 10.1.1.3. Tempeh

- 10.1.2. Non-Dairy Ice Cream

- 10.1.3. Non-Dairy Cheese

- 10.1.4. Non-Dairy Yogurt

- 10.1.5. Non-Dairy Spread

- 10.1.1. Meat Substitutes

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Hypermarkets/Supermarkets

- 10.2.2. Convenience Stores

- 10.2.3. Online Retail Stores

- 10.2.4. Other Distribution Channel

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Middle East and Africa Soy-Based Foods Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Meat Substitutes

- 11.1.1.1. Textured Vegetable Protein

- 11.1.1.2. Tofu

- 11.1.1.3. Tempeh

- 11.1.2. Non-Dairy Ice Cream

- 11.1.3. Non-Dairy Cheese

- 11.1.4. Non-Dairy Yogurt

- 11.1.5. Non-Dairy Spread

- 11.1.1. Meat Substitutes

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Hypermarkets/Supermarkets

- 11.2.2. Convenience Stores

- 11.2.3. Online Retail Stores

- 11.2.4. Other Distribution Channel

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Nestle SA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Vitasoy International Holdings Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 The Amy's Kitche

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Unilever PLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Conagra Brands Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Danone SA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Monde Nissin Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Impossible Foods Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Hain Celestial Group

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Good Catch Foods

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Nestle SA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Soy-Based Foods Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Soy-Based Foods Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 3: North America Soy-Based Foods Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: North America Soy-Based Foods Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 5: North America Soy-Based Foods Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 6: North America Soy-Based Foods Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Soy-Based Foods Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Soy-Based Foods Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 9: Europe Soy-Based Foods Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 10: Europe Soy-Based Foods Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 11: Europe Soy-Based Foods Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 12: Europe Soy-Based Foods Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Soy-Based Foods Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Soy-Based Foods Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 15: Asia Pacific Soy-Based Foods Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Asia Pacific Soy-Based Foods Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 17: Asia Pacific Soy-Based Foods Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 18: Asia Pacific Soy-Based Foods Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Soy-Based Foods Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Soy-Based Foods Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 21: South America Soy-Based Foods Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: South America Soy-Based Foods Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 23: South America Soy-Based Foods Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 24: South America Soy-Based Foods Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: South America Soy-Based Foods Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Soy-Based Foods Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 27: Middle East and Africa Soy-Based Foods Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Middle East and Africa Soy-Based Foods Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 29: Middle East and Africa Soy-Based Foods Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Middle East and Africa Soy-Based Foods Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Soy-Based Foods Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Soy-Based Foods Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Soy-Based Foods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 3: Global Soy-Based Foods Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Soy-Based Foods Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 5: Global Soy-Based Foods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global Soy-Based Foods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Rest of North America Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Global Soy-Based Foods Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 12: Global Soy-Based Foods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 13: Global Soy-Based Foods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 14: Germany Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: United Kingdom Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: France Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Russia Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Spain Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Rest of Europe Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Global Soy-Based Foods Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 21: Global Soy-Based Foods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 22: Global Soy-Based Foods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 23: China Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Japan Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Japan Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Australia Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Soy-Based Foods Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 29: Global Soy-Based Foods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 30: Global Soy-Based Foods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Brazil Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Argentina Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Rest of South America Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Global Soy-Based Foods Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 35: Global Soy-Based Foods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 36: Global Soy-Based Foods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 37: South Africa Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Saudi Arabia Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Rest of Middle East and Africa Soy-Based Foods Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Soy-Based Foods Industry?

The projected CAGR is approximately 6.45%.

2. Which companies are prominent players in the Soy-Based Foods Industry?

Key companies in the market include Nestle SA, Vitasoy International Holdings Ltd, The Amy's Kitche, Unilever PLC, Conagra Brands Inc, Danone SA, Monde Nissin Corporation, Impossible Foods Inc, Hain Celestial Group, Good Catch Foods.

3. What are the main segments of the Soy-Based Foods Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 28.32 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Rising Prevalence of Lactose Intolerant Population.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Soy-Based Foods Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Soy-Based Foods Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Soy-Based Foods Industry?

To stay informed about further developments, trends, and reports in the Soy-Based Foods Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence