Key Insights

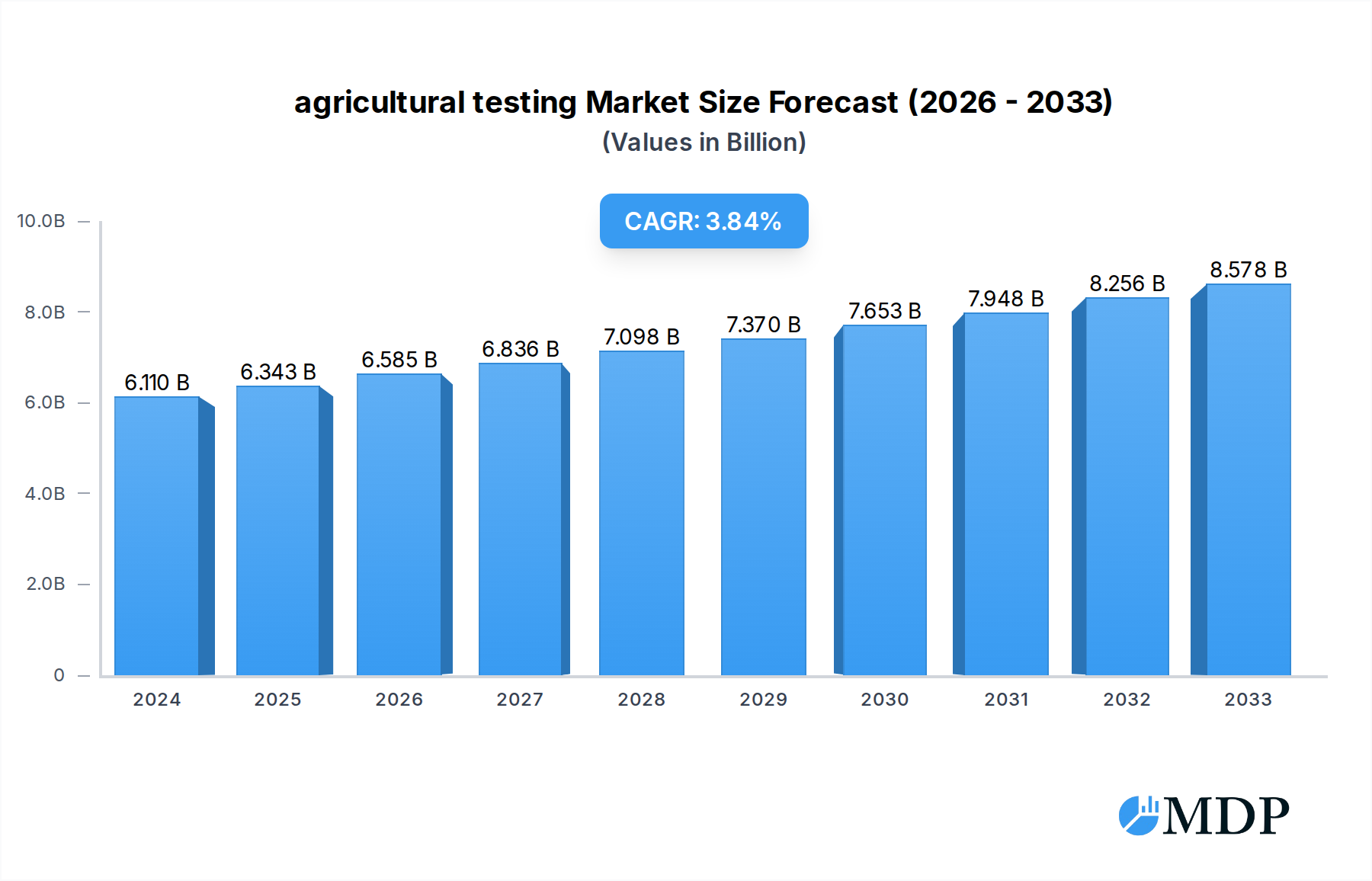

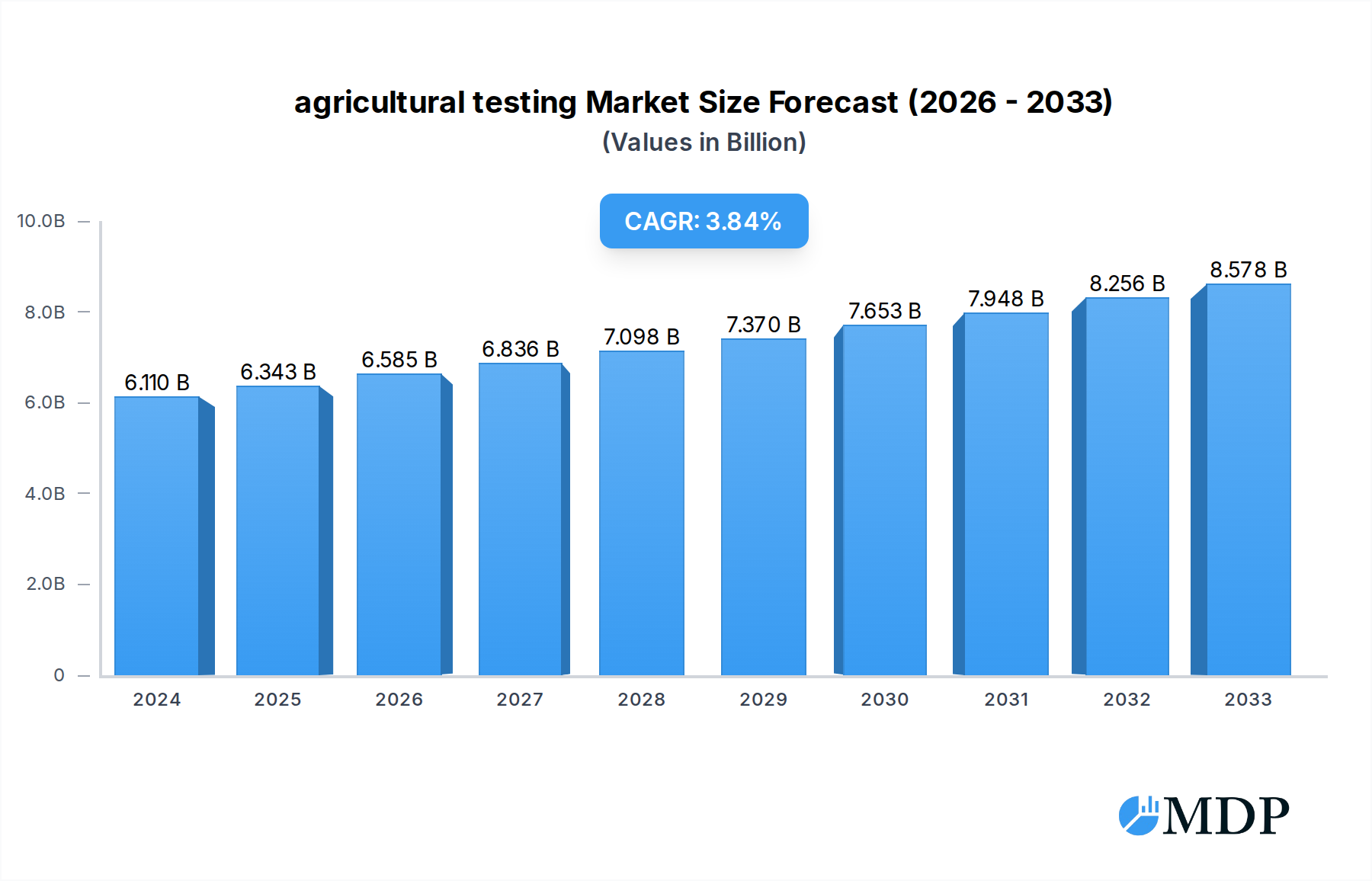

The global agricultural testing market is experiencing robust growth, projected to reach a significant USD 6.11 billion in 2024. This expansion is driven by an increasing emphasis on food safety, quality assurance, and regulatory compliance throughout the agricultural value chain. Farmers, food producers, and regulatory bodies are increasingly relying on comprehensive testing services to ensure the health of crops and livestock, identify contaminants, and verify the nutritional content of agricultural products. This heightened demand for reliable testing is further fueled by growing consumer awareness regarding the origin and safety of their food, leading to stricter standards and a greater need for independent verification. The market's healthy trajectory is further underscored by a projected Compound Annual Growth Rate (CAGR) of 4.07%, indicating sustained momentum in the coming years. This growth is anticipated to be propelled by advancements in testing methodologies, the development of more accurate and faster diagnostic tools, and the expanding scope of agricultural practices, including the rise of precision agriculture and the increasing focus on sustainable farming.

agricultural testing Market Size (In Billion)

The market is segmented by application into farm-level testing, laboratory analysis, and other services, with farm-level applications taking precedence due to the direct need for on-site diagnostics and compliance. Soil and seed testing represent key segments within the types of tests conducted, critical for optimizing crop yields and ensuring healthy plant development. Key industry players such as SGS, Eurofins, and Intertek are actively investing in expanding their service portfolios and geographical reach to cater to the diverse needs of the agricultural sector. Emerging trends include the integration of digital technologies for data management and analysis, the growing demand for testing related to organic and genetically modified (GM) produce, and a greater focus on environmental testing within agriculture. While the market is poised for continued expansion, potential restraints such as high initial investment costs for advanced testing equipment and varying regulatory landscapes across different regions may pose challenges, necessitating strategic adaptation by market participants.

agricultural testing Company Market Share

This in-depth report provides a thorough analysis of the global agricultural testing market, offering critical insights for stakeholders navigating this dynamic sector. With a study period spanning from 2019 to 2033, and a base year of 2025, this report delivers a robust understanding of market trends, growth drivers, leading players, and future opportunities. Explore the intricate market dynamics, technological advancements, and emerging trends that are shaping the future of agricultural testing, from on-farm applications to advanced laboratory diagnostics.

agricultural testing Market Dynamics & Concentration

The agricultural testing market exhibits a moderate to high level of concentration, with a few dominant global players accounting for a significant portion of the market share. Leading companies like SGS (Switzerland), Eurofins (Luxembourg), Intertek (UK), Bureau Veritas (France), and TUV Nord Group (Germany) are actively investing in research and development, driving innovation in areas such as precision agriculture and advanced residue analysis. The market is further characterized by ongoing merger and acquisition (M&A) activities, with an estimated number of over 50 M&A deals recorded during the historical period (2019-2024), indicating strategic consolidation and expansion. Regulatory frameworks, particularly concerning food safety and environmental protection, are significant drivers of market growth, compelling increased adoption of testing services. Product substitutes, while present in some niche areas, are largely unable to replicate the comprehensive and accredited nature of professional agricultural testing services. End-user trends are shifting towards proactive quality management and sustainability practices, with a growing demand for traceable and verified agricultural products.

agricultural testing Industry Trends & Analysis

The agricultural testing industry is experiencing robust growth, propelled by an escalating global population, increasing demand for food security, and a heightened focus on food safety and quality. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 8.5% during the forecast period (2025-2033). Technological disruptions are playing a pivotal role, with advancements in areas such as DNA sequencing for seed testing, high-throughput screening for pesticide residues, and the integration of AI and machine learning for predictive soil health analysis. These innovations are enhancing the speed, accuracy, and scope of agricultural testing services. Consumer preferences are increasingly leaning towards organic, sustainably produced, and ethically sourced food products, creating a demand for comprehensive testing that verifies these claims. The competitive landscape is characterized by a blend of established global giants and specialized regional players, each vying for market share through service differentiation, technological innovation, and strategic partnerships. Market penetration is deepening across developed and developing economies, as regulatory bodies and agricultural stakeholders recognize the indispensable role of accurate testing in ensuring public health and environmental integrity. The increasing adoption of precision agriculture techniques, which rely heavily on detailed soil and crop analysis, is a significant growth catalyst.

Leading Markets & Segments in agricultural testing

The Farm application segment currently holds a dominant position in the agricultural testing market, driven by the direct needs of agricultural producers for on-site analysis and soil health monitoring. Key drivers for this segment’s dominance include the increasing adoption of precision agriculture technologies, where farmers utilize soil tests for optimized nutrient management and irrigation, leading to improved yields and reduced input costs. The economic policies supporting sustainable farming practices and government initiatives promoting soil health further bolster this segment. The Soil Test type is also a leading segment, owing to its fundamental importance in agricultural production. Understanding soil composition, nutrient levels, and potential contaminants is crucial for effective crop planning and management. Infrastructure development in rural areas, facilitating access to testing facilities and services, also contributes to the dominance of this segment. The growing awareness among farmers about the impact of soil health on crop quality and yield directly fuels the demand for regular and comprehensive soil testing. The integration of advanced sensor technologies and data analytics into soil testing further enhances its appeal and effectiveness, solidifying its leadership position.

agricultural testing Product Developments

Product innovation in agricultural testing is rapidly advancing, focusing on enhanced speed, accuracy, and portability of diagnostic tools. Developments include rapid on-site testing kits for pathogen detection, advanced spectroscopic techniques for nutrient analysis, and sophisticated DNA sequencing for seed varietal identification and genetic trait analysis. These innovations offer competitive advantages by reducing turnaround times, improving the precision of results, and enabling earlier detection of potential issues. The market fit for these new products is strong, addressing the growing need for proactive management and compliance in the agricultural supply chain.

Key Drivers of agricultural testing Growth

Several key drivers are propelling the growth of the agricultural testing market. Technologically, advancements in biosensors and automation are enabling faster and more accurate testing. Economically, the rising global demand for food, coupled with increasing consumer awareness regarding food safety, is a significant impetus. Regulatory frameworks, mandating stricter quality control and environmental standards, are also critical growth accelerators, pushing for wider adoption of comprehensive testing services across the entire agricultural value chain.

Challenges in the agricultural testing Market

Despite the positive growth trajectory, the agricultural testing market faces several challenges. Regulatory hurdles can sometimes be complex and vary significantly across different regions, creating compliance complexities for global service providers. Supply chain issues, particularly in remote agricultural areas, can impact the timely collection and delivery of samples. Furthermore, intense competitive pressures among established players and emerging niche providers can affect pricing and profitability, necessitating continuous innovation and service differentiation.

Emerging Opportunities in agricultural testing

Emerging opportunities in the agricultural testing market are primarily driven by technological breakthroughs and strategic market expansion. The rise of digital agriculture, encompassing IoT sensors and data analytics platforms, presents a significant avenue for integrated testing and advisory services. Strategic partnerships between testing laboratories and ag-tech companies are creating new service models. Furthermore, expanding into emerging economies with rapidly growing agricultural sectors offers substantial long-term growth potential.

Leading Players in the agricultural testing Sector

- SGS

- Eurofins

- Intertek

- Bureau Veritas

- TUV Nord Group

- ALS Limited

- Merieux

- AsureQuality

- RJ Hill Laboratories

- Agrifood Technology

- Apal Agricultural Laboratory

- SCS Global

Key Milestones in agricultural testing Industry

- 2019: Launch of advanced next-generation sequencing (NGS) platforms for rapid disease diagnostics.

- 2020: Increased adoption of AI-powered data analytics for soil health and yield prediction.

- 2021: Significant M&A activity, with over 15 major acquisitions aimed at market consolidation and service expansion.

- 2022: Introduction of portable, on-site testing devices for pesticide residue analysis, enhancing farmer accessibility.

- 2023: Development of blockchain-enabled traceability solutions integrated with testing data, boosting consumer trust.

- 2024: Increased focus on sustainability certifications and associated testing protocols.

Strategic Outlook for agricultural testing Market

The strategic outlook for the agricultural testing market remains highly positive, driven by an unwavering demand for safe, high-quality food and sustainable agricultural practices. Growth accelerators include the continuous innovation in analytical technologies, the expansion of precision agriculture, and the increasing stringency of global food safety regulations. Strategic opportunities lie in developing integrated service offerings that combine advanced testing with data-driven advisory, expanding into underserved geographic regions, and fostering collaborations that enhance the efficiency and accessibility of agricultural testing solutions.

agricultural testing Segmentation

-

1. Application

- 1.1. Farm

- 1.2. Laboratory

- 1.3. Other

-

2. Types

- 2.1. Soil Test

- 2.2. Seed Test

- 2.3. Other

agricultural testing Segmentation By Geography

- 1. CA

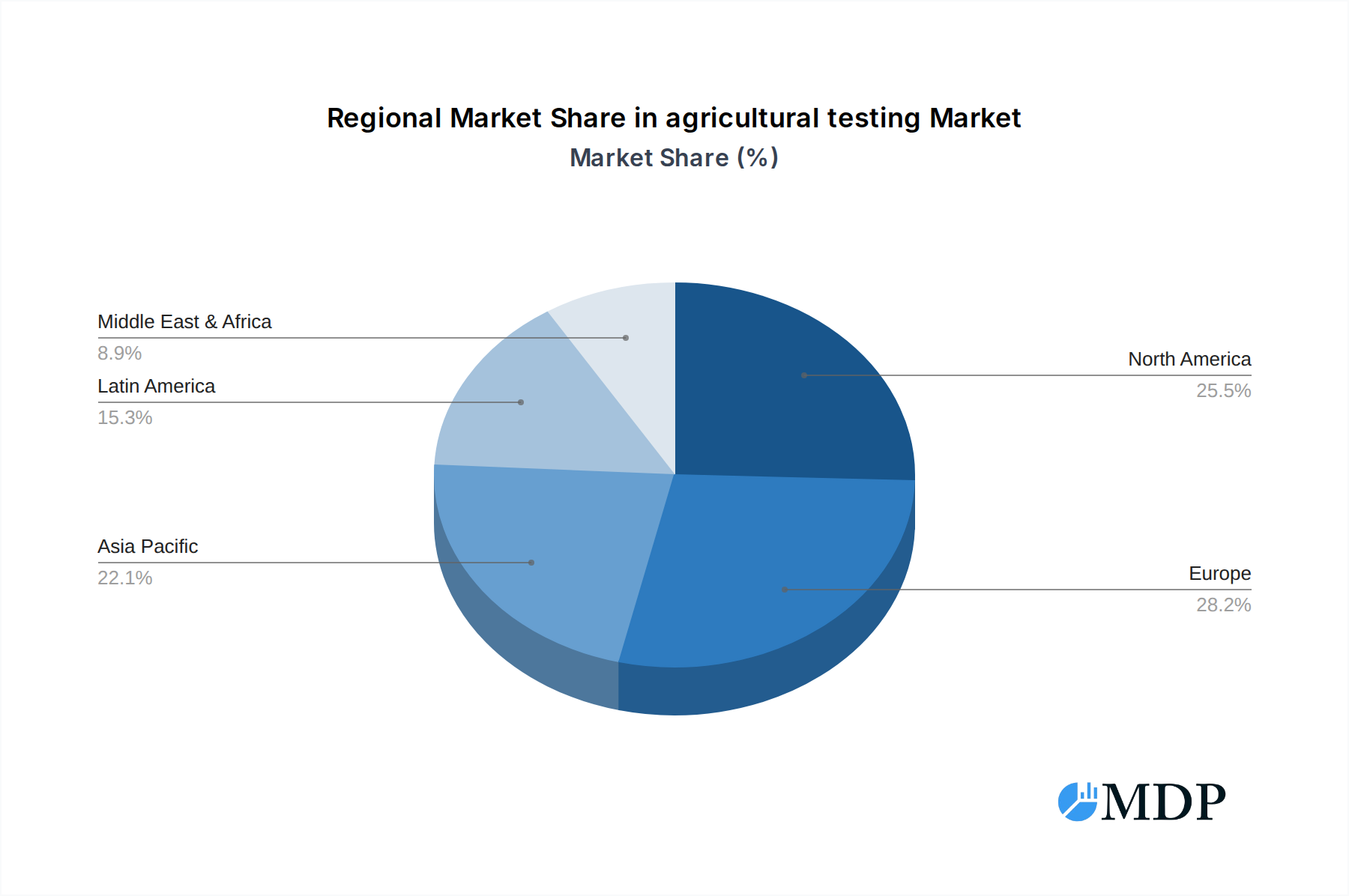

agricultural testing Regional Market Share

Geographic Coverage of agricultural testing

agricultural testing REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.07% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. agricultural testing Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Farm

- 5.1.2. Laboratory

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Soil Test

- 5.2.2. Seed Test

- 5.2.3. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. CA

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 SGS (Switzerland)

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Eurofins (Luxembourg)

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Intertek (UK)

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Bureau Veritas (France)

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 TUV Nord Group (Germany)

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 ALS Limited (Australia)

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Merieux (US)

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 AsureQuality (New Zealand)

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 RJ Hill Laboratories (New Zealand)

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Agrifood Technology (Australia)

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Apal Agricultural Laboratory (Australia)

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 SCS Global (US)

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.1 SGS (Switzerland)

List of Figures

- Figure 1: agricultural testing Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: agricultural testing Share (%) by Company 2025

List of Tables

- Table 1: agricultural testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: agricultural testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: agricultural testing Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: agricultural testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: agricultural testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: agricultural testing Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the agricultural testing?

The projected CAGR is approximately 4.07%.

2. Which companies are prominent players in the agricultural testing?

Key companies in the market include SGS (Switzerland), Eurofins (Luxembourg), Intertek (UK), Bureau Veritas (France), TUV Nord Group (Germany), ALS Limited (Australia), Merieux (US), AsureQuality (New Zealand), RJ Hill Laboratories (New Zealand), Agrifood Technology (Australia), Apal Agricultural Laboratory (Australia), SCS Global (US).

3. What are the main segments of the agricultural testing?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3400.00, USD 5100.00, and USD 6800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "agricultural testing," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the agricultural testing report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the agricultural testing?

To stay informed about further developments, trends, and reports in the agricultural testing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence