Key Insights

The global Track & Field Equipment market is projected for substantial growth, anticipated to reach $18.7 billion by 2025, with a Compound Annual Growth Rate (CAGR) of approximately 3.7% through 2033. This expansion is fueled by rising global athletic participation, increased health and fitness awareness, and the growing popularity of track and field events across all levels. Increased investment in sports infrastructure and athletic programs by governments and educational institutions globally is creating sustained demand. Technological advancements driving the development of lighter, more durable, and performance-enhancing equipment are also key growth catalysts. Demand is surging for specialized equipment across throwing, jumping, sprinting, and hurdling disciplines.

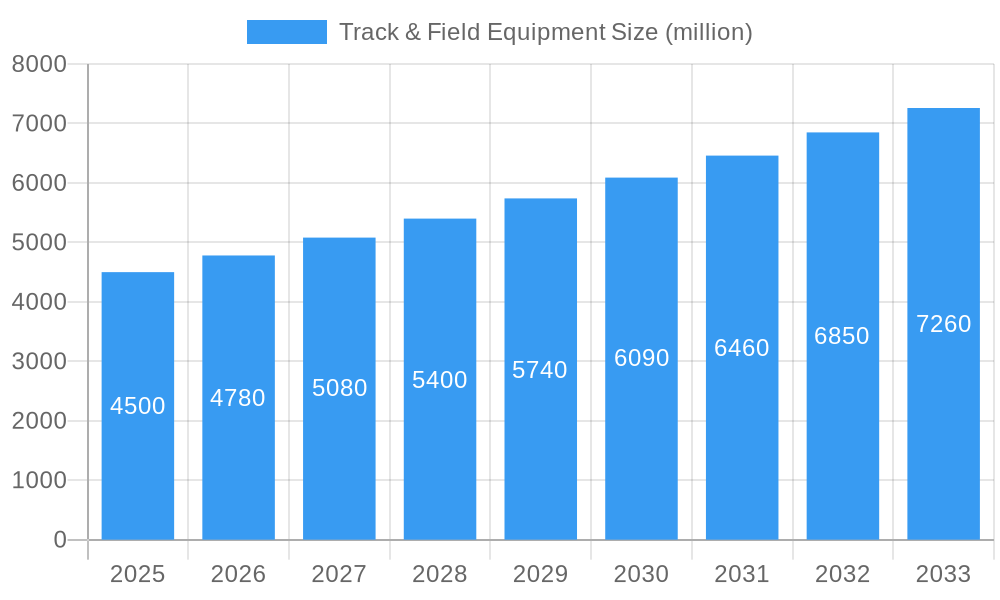

Track & Field Equipment Market Size (In Billion)

The market faces restraints including high manufacturing costs for advanced materials and significant R&D investment requirements. Revenue volatility can also stem from reliance on sponsorships and event funding. However, market challenges are expected to be offset by the increasing commercialization of sports, the rise of professional leagues, and the growing popularity of sports tourism. The Asia Pacific region is a significant growth engine, driven by a rising middle class, increased disposable incomes, and hosting major international sporting events. North America and Europe remain dominant markets due to established sports ecosystems and high consumer spending. The market is segmented by application, serving amateur enthusiasts and professional athletes, with a diverse range of equipment types ensuring broad appeal.

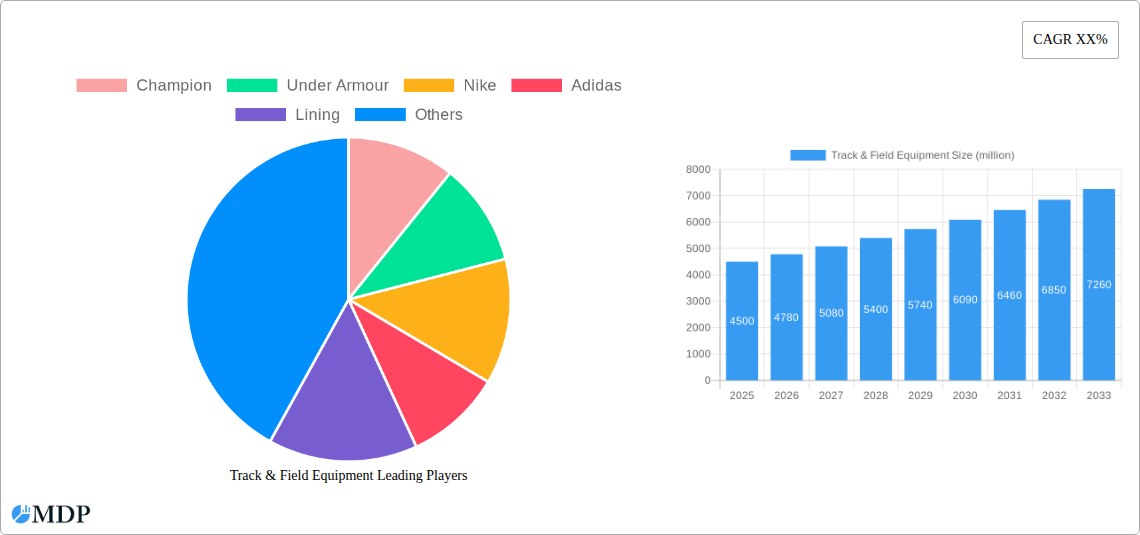

Track & Field Equipment Company Market Share

Track & Field Equipment Market: Comprehensive Analysis & Forecast (2019-2033)

Unlock critical insights into the global track and field equipment market. This in-depth report provides an essential roadmap for stakeholders, covering market dynamics, trends, leading segments, product innovations, growth drivers, challenges, opportunities, and key players from 2019 to 2033. With a base year of 2025 and a forecast period extending to 2033, this analysis leverages historical data from 2019-2024 to offer a robust outlook for industry professionals, investors, and manufacturers.

Track & Field Equipment Market Dynamics & Concentration

The global track and field equipment market exhibits a moderate to high concentration, with major players like Nike, Adidas, and Under Armour dominating a significant portion of the market share, estimated at over 60% of the total market valuation. Emerging brands such as Lining are also carving out significant niches. Innovation remains a key driver, fueled by advancements in material science for lighter and more durable equipment and technology integration for performance analytics. Regulatory frameworks, particularly those set by international sporting federations like World Athletics, are crucial in dictating product standards and safety. Product substitutes, while limited in core track and field disciplines, can arise from multi-sport training equipment that offers partial functionality. End-user trends indicate a growing demand for specialized equipment catering to both amateur athletes and elite professionals, with a surge in participation in recreational athletics. Mergers and acquisitions (M&A) activities, though not at an extremely high volume, have been strategically focused on acquiring niche technologies or expanding geographical reach, with an estimated average of 2-3 significant deals annually in the historical period. The market concentration is influenced by brand loyalty and the significant investment required for R&D and global distribution networks.

Track & Field Equipment Industry Trends & Analysis

The track and field equipment industry is poised for substantial growth, driven by a confluence of factors that are reshaping its landscape. The estimated Compound Annual Growth Rate (CAGR) for the forecast period (2025–2033) is projected to be around 6.8%, reflecting robust market expansion. Key growth drivers include the increasing global participation in athletics, from grassroots school programs to professional competitions. This surge in participation is further amplified by growing health and wellness awareness, encouraging individuals of all ages to engage in athletic pursuits. Technological disruptions are also playing a pivotal role. Innovations in material science have led to the development of lighter, stronger, and more aerodynamic equipment, enhancing athlete performance and safety. For instance, advancements in carbon fiber composites for javelins and pole vaults have significantly improved their performance characteristics. The integration of smart technology into equipment, such as sensors in starting blocks to measure reaction times or advanced materials in hurdles for better flexibility, is another significant trend. Consumer preferences are evolving towards sustainable and ethically produced equipment, prompting manufacturers to adopt eco-friendly materials and manufacturing processes. The competitive dynamics are intense, with established global brands like Nike, Adidas, and Under Armour fiercely competing with specialized manufacturers like Aluminum Athletic Equipment Co. and UCS Spirit. The market penetration of high-performance equipment is increasing, as more amateurs seek to emulate professional athletes and invest in quality gear. Furthermore, the rising popularity of major sporting events like the Olympics and World Athletics Championships acts as a powerful catalyst, inspiring new generations of athletes and driving demand for associated equipment. The market is also seeing increased investment in research and development, focusing on biomechanics and athlete physiology to design equipment that optimizes performance and minimizes injury risk. This continuous innovation cycle ensures the industry remains dynamic and responsive to evolving athlete needs and sporting trends, contributing to a projected market size of over $10 million by 2025 and exceeding $15 million by 2033.

Leading Markets & Segments in Track & Field Equipment

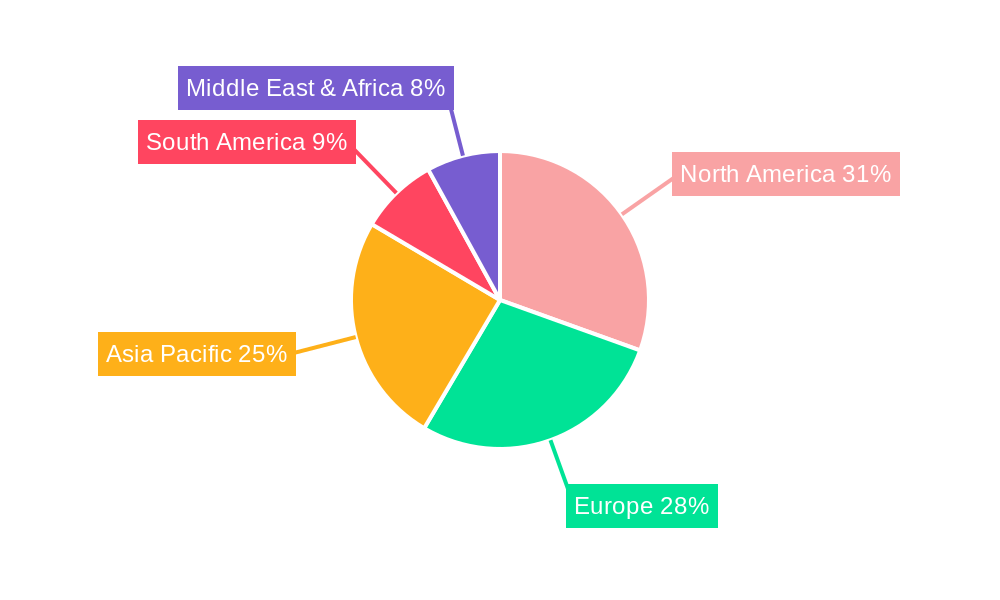

The global track and field equipment market's dominance is multifaceted, with specific regions and product segments exhibiting significant growth and demand. North America currently stands as the leading market, accounting for approximately 35% of the global market share. This leadership is attributed to a strong sporting culture, substantial investment in athletic infrastructure, and the presence of major sporting organizations and educational institutions that consistently drive demand for track and field equipment. Within North America, the United States is the primary contributor, with its extensive school and university athletic programs, professional leagues, and a burgeoning amateur fitness sector.

Key drivers of this regional dominance include:

- Robust Educational Infrastructure: A vast network of high schools and universities with dedicated track and field programs creates a consistent and substantial demand for equipment across all disciplines.

- Government and Private Investment: Significant funding allocated to sports development, including the construction and maintenance of athletic facilities, directly fuels the track and field equipment market.

- High Consumer Spending Power: The affluent consumer base in North America supports the purchase of premium and specialized track and field equipment by both individuals and institutions.

- Major Sporting Events: Hosting and participating in high-profile international and national athletic events stimulates interest and investment in the sport.

In terms of application, the Professionals segment is a significant revenue generator, driven by the demand for cutting-edge, high-performance equipment. However, the Amateurs segment is experiencing the most rapid growth due to increased global participation in fitness and recreational athletics.

Among the equipment types, Starting Blocks and Hurdles represent significant market value due to their essential role in most track and field events and the recurring need for replacements and upgrades. However, the Pole Vaulting and High Jump segments, while more niche, often command higher per-unit prices due to the specialized engineering and advanced materials involved. The Shot Put and Discus segments also maintain steady demand due to their foundational status in athletic programs. The "Others" category, encompassing a range of training aids and specialized equipment, is also showing promising growth as athletes and coaches seek to optimize every aspect of training. Economic policies supporting sports and physical education, alongside infrastructure development for athletic facilities, are critical factors influencing regional and segment growth trajectories. The continued expansion of amateur participation, coupled with the ongoing pursuit of athletic excellence by professionals, ensures sustained demand across these diverse segments.

Track & Field Equipment Product Developments

Product innovations in the track and field equipment market are largely driven by advancements in material science and ergonomic design. Manufacturers are increasingly utilizing advanced composites like carbon fiber and high-tensile polymers to create lighter, more durable, and performance-enhancing equipment. For instance, the development of lighter and more aerodynamic javelins and discus has led to improved athlete performance. Smart technology integration is also a significant trend, with sensors embedded in starting blocks to measure reaction times and pressure plates in landing mats for high jump to provide detailed performance feedback. Competitive advantages are being gained by companies that can offer customized solutions, sustainable product lines, and integrated digital performance tracking. The focus is on optimizing athlete safety, enhancing user experience, and pushing the boundaries of athletic achievement through innovative design and material application.

Key Drivers of Track & Field Equipment Growth

The track and field equipment market is propelled by several robust growth drivers. Technological advancements in material science and product design are creating lighter, more durable, and performance-enhancing equipment, attracting both amateur and professional athletes. The increasing global participation in athletics, fueled by growing health consciousness and the popularity of major sporting events like the Olympics, is a primary economic driver. Furthermore, government initiatives and investments in sports infrastructure worldwide, particularly in developing nations, are expanding access to facilities and consequently, the demand for equipment. The growing trend of "fitness for all" is also broadening the consumer base beyond elite athletes.

Challenges in the Track & Field Equipment Market

Despite the positive growth trajectory, the track and field equipment market faces several challenges. Stringent regulatory standards set by sporting federations can limit innovation and increase production costs as manufacturers must ensure compliance. Supply chain disruptions, as observed in recent global events, can lead to material shortages and increased lead times, impacting production and delivery schedules. High research and development costs associated with advanced materials and smart technology integration present a barrier for smaller players. Intense competition from established brands with significant marketing budgets can make it difficult for new entrants to gain market share. Additionally, economic downturns can reduce discretionary spending on sporting goods, impacting sales, especially for premium products.

Emerging Opportunities in Track & Field Equipment

Emerging opportunities in the track and field equipment market lie in several key areas. The development of sustainable and eco-friendly equipment is a significant untapped market, appealing to environmentally conscious consumers and institutions. The integration of advanced sensor technology and data analytics into equipment offers substantial potential for performance enhancement and personalized training programs, creating a niche for smart track and field gear. Strategic partnerships between equipment manufacturers and sports technology companies can lead to innovative, integrated solutions. Furthermore, market expansion into emerging economies with growing interest in sports and increasing disposable incomes presents a significant long-term growth catalyst. The development of adaptive track and field equipment for athletes with disabilities is also a growing area with significant social and commercial potential.

Leading Players in the Track & Field Equipment Sector

- Nike

- Adidas

- Under Armour

- Lining

- Aluminum Athletic Equipment Co.

- UCS Spirit

- Gill

- SKLZ

- Prism Fitness

- Champro

- Stackhouse

Key Milestones in Track & Field Equipment Industry

- 2019: Introduction of new World Athletics rules for equipment specifications, influencing product design and material choices.

- 2020: Increased demand for home-based training equipment, including portable hurdles and resistance bands, due to global pandemic restrictions.

- 2021: Launch of advanced composite materials for javelins, leading to record-breaking performances and increased sales.

- 2022: Growing adoption of smart technology in starting blocks and timing systems for amateur and collegiate competitions.

- 2023: Increased focus on sustainable manufacturing practices by major brands, with introduction of recycled materials in equipment.

- 2024: Significant investment in R&D for personalized track and field training solutions integrating AI and sensor data.

Strategic Outlook for Track & Field Equipment Market

The strategic outlook for the track and field equipment market is exceptionally promising, driven by continued global interest in athletic pursuits and ongoing technological innovation. Growth accelerators will include the wider adoption of smart track and field equipment, offering data-driven insights for athletes and coaches. The expansion of recreational athletics and the increasing emphasis on holistic wellness will continue to fuel demand from the amateur segment. Manufacturers focusing on sustainable product development and ethical sourcing will likely gain a competitive edge. Strategic partnerships with sports technology firms and a proactive approach to developing equipment for emerging markets will be crucial for sustained growth and market leadership in the coming years.

Track & Field Equipment Segmentation

-

1. Application

- 1.1. Amateurs

- 1.2. Professionals

-

2. Types

- 2.1. Shot Put

- 2.2. Discus

- 2.3. Javelin

- 2.4. Starting Blocks

- 2.5. Hurdles

- 2.6. Pole Vaulting

- 2.7. High Jump

- 2.8. Others

Track & Field Equipment Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Track & Field Equipment Regional Market Share

Geographic Coverage of Track & Field Equipment

Track & Field Equipment REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Track & Field Equipment Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Amateurs

- 5.1.2. Professionals

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Shot Put

- 5.2.2. Discus

- 5.2.3. Javelin

- 5.2.4. Starting Blocks

- 5.2.5. Hurdles

- 5.2.6. Pole Vaulting

- 5.2.7. High Jump

- 5.2.8. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Track & Field Equipment Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Amateurs

- 6.1.2. Professionals

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Shot Put

- 6.2.2. Discus

- 6.2.3. Javelin

- 6.2.4. Starting Blocks

- 6.2.5. Hurdles

- 6.2.6. Pole Vaulting

- 6.2.7. High Jump

- 6.2.8. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Track & Field Equipment Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Amateurs

- 7.1.2. Professionals

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Shot Put

- 7.2.2. Discus

- 7.2.3. Javelin

- 7.2.4. Starting Blocks

- 7.2.5. Hurdles

- 7.2.6. Pole Vaulting

- 7.2.7. High Jump

- 7.2.8. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Track & Field Equipment Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Amateurs

- 8.1.2. Professionals

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Shot Put

- 8.2.2. Discus

- 8.2.3. Javelin

- 8.2.4. Starting Blocks

- 8.2.5. Hurdles

- 8.2.6. Pole Vaulting

- 8.2.7. High Jump

- 8.2.8. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Track & Field Equipment Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Amateurs

- 9.1.2. Professionals

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Shot Put

- 9.2.2. Discus

- 9.2.3. Javelin

- 9.2.4. Starting Blocks

- 9.2.5. Hurdles

- 9.2.6. Pole Vaulting

- 9.2.7. High Jump

- 9.2.8. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Track & Field Equipment Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Amateurs

- 10.1.2. Professionals

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Shot Put

- 10.2.2. Discus

- 10.2.3. Javelin

- 10.2.4. Starting Blocks

- 10.2.5. Hurdles

- 10.2.6. Pole Vaulting

- 10.2.7. High Jump

- 10.2.8. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Champion

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Under Armour

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Nike

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Adidas

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Lining

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Aluminum Athletic Equipment Co.

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 UCS Spirit

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Gill

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 SKLZ

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Prism Fitness

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Champro

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Stackhouse

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Champion

List of Figures

- Figure 1: Global Track & Field Equipment Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Track & Field Equipment Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Track & Field Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Track & Field Equipment Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Track & Field Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Track & Field Equipment Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Track & Field Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Track & Field Equipment Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Track & Field Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Track & Field Equipment Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Track & Field Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Track & Field Equipment Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Track & Field Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Track & Field Equipment Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Track & Field Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Track & Field Equipment Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Track & Field Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Track & Field Equipment Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Track & Field Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Track & Field Equipment Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Track & Field Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Track & Field Equipment Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Track & Field Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Track & Field Equipment Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Track & Field Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Track & Field Equipment Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Track & Field Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Track & Field Equipment Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Track & Field Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Track & Field Equipment Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Track & Field Equipment Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Track & Field Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Track & Field Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Track & Field Equipment Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Track & Field Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Track & Field Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Track & Field Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Track & Field Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Track & Field Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Track & Field Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Track & Field Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Track & Field Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Track & Field Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Track & Field Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Track & Field Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Track & Field Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Track & Field Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Track & Field Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Track & Field Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Track & Field Equipment Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Track & Field Equipment?

The projected CAGR is approximately 3.7%.

2. Which companies are prominent players in the Track & Field Equipment?

Key companies in the market include Champion, Under Armour, Nike, Adidas, Lining, Aluminum Athletic Equipment Co., UCS Spirit, Gill, SKLZ, Prism Fitness, Champro, Stackhouse.

3. What are the main segments of the Track & Field Equipment?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 18.7 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Track & Field Equipment," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Track & Field Equipment report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Track & Field Equipment?

To stay informed about further developments, trends, and reports in the Track & Field Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence