Key Insights

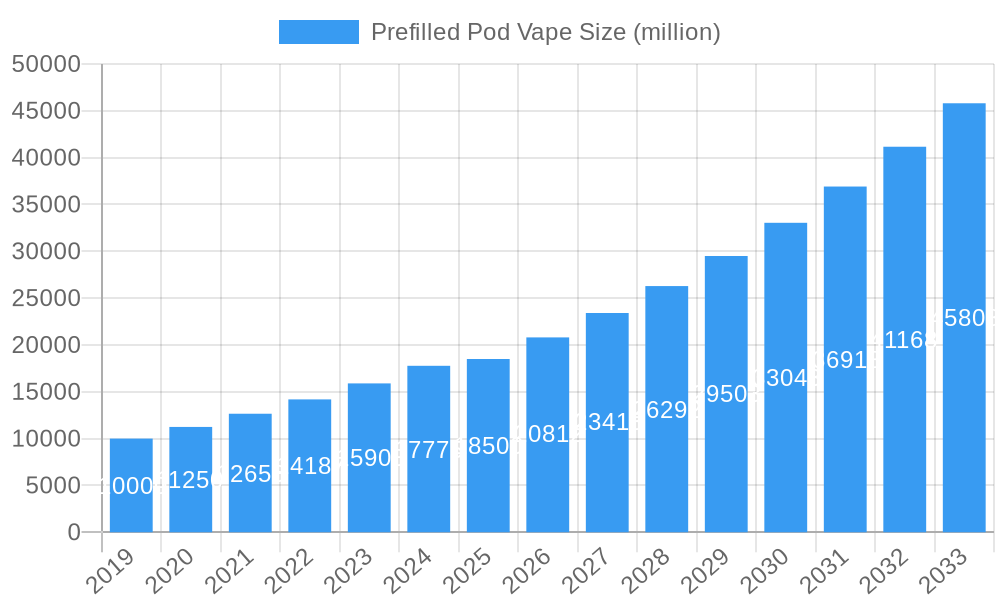

The Prefilled Pod Vape market is experiencing significant growth, projected to reach an estimated market size of USD 18,500 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 12.5% anticipated through 2033. This expansion is primarily fueled by the increasing consumer preference for convenient and user-friendly vaping devices, coupled with the rising global adoption of e-cigarettes as alternatives to traditional tobacco products. Key drivers include evolving lifestyle trends, a growing awareness of the potential harm reduction offered by vaping compared to smoking, and innovative product development by leading manufacturers such as BAT, Altria Group, and SMOORE. The market segmentation reveals a strong inclination towards larger capacity devices, with the ">10,000 Puffs" category showing substantial traction due to enhanced user experience and reduced frequency of replacements. Online sales channels are also playing a pivotal role, offering wider accessibility and competitive pricing.

Prefilled Pod Vape Market Size (In Billion)

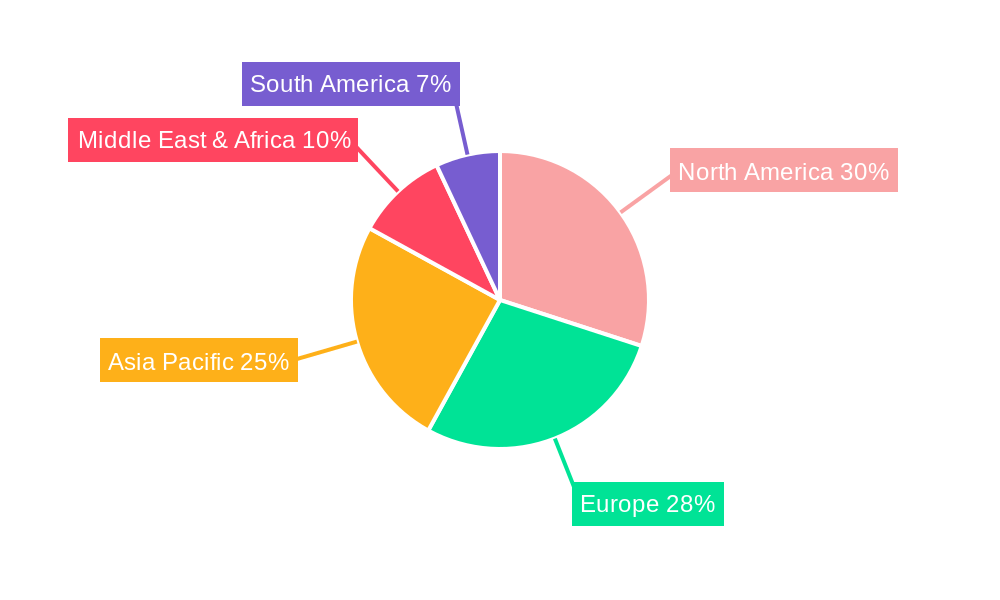

Despite the promising outlook, the market faces certain restraints, including stringent regulatory frameworks and potential health concerns associated with vaping, particularly concerning long-term effects and youth accessibility. However, the industry is actively responding by investing in research and development for safer formulations and advocating for responsible marketing practices. The Asia Pacific region, led by China and India, is emerging as a significant growth engine, driven by a burgeoning young population and increasing disposable incomes. North America and Europe continue to be dominant markets, characterized by a mature consumer base and a strong presence of established players. Future trends are expected to focus on further technological advancements, improved flavor profiles, and enhanced device customization, all contributing to sustained market expansion.

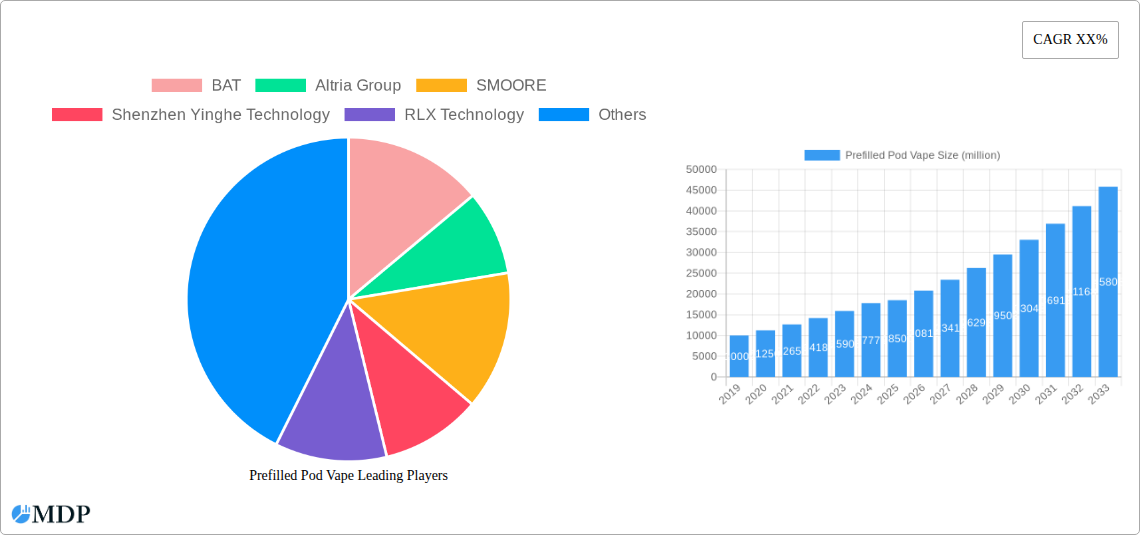

Prefilled Pod Vape Company Market Share

This comprehensive report delves into the burgeoning Prefilled Pod Vape market, offering deep insights and actionable intelligence for industry stakeholders. Spanning the study period of 2019–2033, with a base year of 2025 and a forecast period of 2025–2033, this analysis leverages historical data from 2019–2024 to provide an unparalleled understanding of market dynamics, trends, and future potential. We explore leading companies, innovative product developments, crucial growth drivers, and emerging opportunities within this rapidly evolving sector. This report is essential for businesses aiming to capitalize on the projected market expansion and navigate the competitive landscape effectively.

Prefilled Pod Vape Market Dynamics & Concentration

The Prefilled Pod Vape market exhibits moderate concentration, with key players like BAT, Altria Group, and SMOORE holding significant market share. Innovation drivers are predominantly fueled by advancements in battery technology, flavor profiles, and device ergonomics, responding to evolving consumer preferences. Regulatory frameworks, particularly concerning nicotine content and marketing restrictions, represent a crucial external factor shaping market accessibility and product development. The threat of product substitutes, such as traditional cigarettes and other alternative nicotine delivery systems, is present but mitigated by the convenience and user-friendliness of prefilled pod vapes. End-user trends indicate a strong inclination towards convenient, disposable, and diverse flavor options. Merger and acquisition activities are anticipated to increase, with an estimated xx number of deals projected within the forecast period, aiming to consolidate market positions and expand product portfolios. The M&A deal value is projected to reach an impressive xx million.

- Market Concentration: Moderate, with established players and emerging innovators.

- Innovation Drivers: Battery efficiency, flavor diversity, user experience enhancement.

- Regulatory Impact: Significant, influencing product composition and market entry.

- Product Substitutes: Traditional cigarettes, other e-cigarette types.

- End-User Trends: Convenience, portability, wide flavor selection.

- M&A Activity: Projected xx deals, totaling xx million in value.

Prefilled Pod Vape Industry Trends & Analysis

The Prefilled Pod Vape industry is poised for substantial growth, driven by a confluence of factors including increasing adoption rates among adult smokers seeking alternatives and the continuous innovation in device technology and e-liquid formulations. The market is expected to witness a Compound Annual Growth Rate (CAGR) of xx% over the forecast period. Market penetration is projected to reach xx% by 2033, indicating a significant shift in consumer behavior and nicotine consumption patterns. Technological disruptions, such as the development of advanced heating elements for better flavor delivery and longer-lasting battery life, are key differentiators. Consumer preferences are increasingly leaning towards devices offering a wider range of nicotine strengths and more sophisticated flavor options, moving beyond traditional tobacco flavors to include fruit, dessert, and menthol variants. Competitive dynamics are intensifying, with both established tobacco giants and specialized vape manufacturers vying for market dominance through product differentiation, aggressive marketing strategies, and expansion into new geographic regions. The introduction of high-puff count devices, such as those offering 8000-10000 puffs and over 10000 puffs, directly addresses consumer demand for extended usage and reduced frequency of replacements, further fueling market expansion. The accessibility of online sales channels has also played a pivotal role in reaching a wider consumer base, complementing traditional offline retail networks.

Leading Markets & Segments in Prefilled Pod Vape

The Asia-Pacific region is emerging as a dominant market for prefilled pod vapes, driven by a large and growing population, increasing disposable incomes, and a relatively more relaxed regulatory environment in some key countries compared to Western markets. Within this region, China stands out as a leading country due to the significant presence of major manufacturers like SMOORE and Shenzhen Yinghe Technology, coupled with a burgeoning domestic consumer base.

Analyzing the segments:

Application: Online Sales: This segment is experiencing explosive growth.

- Key Drivers: E-commerce penetration, convenience for consumers, targeted digital marketing, and the ability to offer a wider product selection.

- Dominance Analysis: Online platforms facilitate direct consumer access, bypassing traditional retail limitations and enabling agile response to market trends. The ease of comparison and purchase empowers consumers, leading to higher conversion rates. Online sales are projected to capture xx% of the market share by 2033.

Application: Offline Sales: While online channels are growing, offline sales remain crucial for brand visibility and immediate consumer access.

- Key Drivers: Impulse purchases, ability to physically interact with products, established distribution networks, and regulatory requirements in certain regions.

- Dominance Analysis: Traditional retail, including convenience stores and specialized vape shops, provides a tangible point of sale. This segment is critical for reaching consumers who prefer in-person shopping experiences and for complying with regulations that may restrict online sales of certain nicotine products. Offline sales are expected to maintain a significant presence, holding xx% of the market share.

Types: 8000-10000 Puffs: This category represents a significant and growing segment.

- Key Drivers: Enhanced user experience due to longer lifespan, perceived value for money, reduced environmental impact compared to lower-puff devices, and alignment with consumer desire for less frequent replacements.

- Dominance Analysis: The demand for high-puff count devices signifies a maturation of the market where users are looking for a more sustained vaping experience. This segment caters to both casual and regular users seeking convenience and efficiency. This segment is projected to account for xx% of the market.

Types: >10000 Puffs: This segment is at the forefront of innovation, offering the longest usage duration.

- Key Drivers: Premium user experience, convenience, and appealing to a segment of users seeking the ultimate long-lasting disposable vape solution.

- Dominance Analysis: As technology advances, devices with over 10000 puffs are becoming more feasible and desirable, pushing the boundaries of what disposable vapes can offer. This segment is expected to see rapid growth and capture a significant portion of the market by the end of the forecast period, projected to hold xx% of the market.

Types: Others: This includes devices with puff counts below 8000.

- Key Drivers: Entry-level pricing, variety for niche preferences, and appeal to consumers new to vaping.

- Dominance Analysis: While higher puff counts are gaining traction, the "Others" segment will continue to exist, catering to budget-conscious consumers or those who prefer shorter-term usage. This segment is expected to hold xx% of the market share.

Prefilled Pod Vape Product Developments

Recent product developments in the prefilled pod vape market are characterized by a significant push towards higher puff counts, exceeding 8000 and even 10000 puffs, offering extended usability and enhanced value for consumers. Innovations in battery technology are enabling these longer-lasting devices, while advanced coil designs are optimizing flavor delivery and vapor production. The market is also witnessing a surge in sophisticated flavor profiles, moving beyond traditional tobacco to offer a diverse range of fruit, dessert, and beverage-inspired options. Manufacturers are also focusing on sleek, ergonomic designs for improved portability and aesthetic appeal. Furthermore, there's a growing emphasis on user-friendly interfaces and safety features, aiming to provide a seamless and secure vaping experience. These advancements are crucial for differentiating products in a competitive landscape and meeting the evolving demands of adult nicotine consumers.

Key Drivers of Prefilled Pod Vape Growth

Several key drivers are fueling the robust growth of the prefilled pod vape market. Technologically, advancements in battery longevity and charging efficiency are enabling higher puff counts, making disposable vapes more convenient and cost-effective for consumers. Economically, the increasing disposable income in emerging markets, coupled with the perception of vapes as a less expensive alternative to traditional cigarettes, is driving adoption. Regulatory landscapes, while presenting challenges, are also indirectly fostering growth by creating clearer guidelines for product development and marketing, encouraging responsible innovation. Consumer preference for convenience, portability, and a wide array of flavor options continues to be a primary demand-side driver. The discreet nature of these devices also appeals to a segment of users looking for a less intrusive nicotine consumption method.

Challenges in the Prefilled Pod Vape Market

The prefilled pod vape market faces several significant challenges that could impede its growth trajectory. Stringent and evolving regulatory frameworks in various regions, particularly concerning nicotine content, flavor bans, and marketing restrictions, pose a substantial hurdle. Supply chain disruptions, exacerbated by global events, can impact manufacturing costs and product availability, leading to price volatility. Intense competitive pressures from both established tobacco companies and emerging vape brands can lead to market saturation and price wars, impacting profit margins. Furthermore, public health concerns and potential negative perceptions surrounding vaping, despite its role as a harm reduction tool, can influence consumer sentiment and regulatory responses. The illicit market for unregulated vape products also presents a challenge to legitimate businesses.

Emerging Opportunities in Prefilled Pod Vape

Emerging opportunities in the prefilled pod vape market lie in several key areas. Technological breakthroughs in solid-state battery technology and biodegradable materials for device components present avenues for enhanced sustainability and performance. Strategic partnerships with flavor houses and ingredient suppliers can lead to the development of novel and highly sought-after e-liquid formulations. Market expansion into underserved geographical regions, particularly in developing economies with growing adult smoking populations, offers significant untapped potential. The development of "smart" vape devices with integrated tracking and feedback mechanisms could also appeal to a tech-savvy consumer base. Furthermore, exploring nicotine salts and other advanced nicotine delivery systems can cater to diverse consumer preferences and potentially enhance satisfaction.

Leading Players in the Prefilled Pod Vape Sector

- BAT

- Altria Group

- SMOORE

- Shenzhen Yinghe Technology

- RLX Technology

- iMiracle

- ELUX

- HQD

- Geek Bar

- FLUM

- Blu

- 10 Motives

Key Milestones in Prefilled Pod Vape Industry

- 2019: Introduction of advanced nicotine salt formulations in prefilled pods, enhancing user experience and nicotine delivery.

- 2020: Significant increase in the launch of high-puff count devices (e.g., 3000-5000 puffs), responding to consumer demand for longer-lasting products.

- 2021: Growing regulatory scrutiny and bans on certain flavors in key markets like the US, prompting manufacturers to focus on tobacco and menthol alternatives.

- 2022: Expansion of major players like Geek Bar and FLUM into new international markets, accelerating global adoption.

- 2023: Rise of ultra-high puff count devices (8000-10000+ puffs) becoming mainstream, driven by battery technology improvements.

- 2024: Increased focus on sustainability, with some manufacturers exploring recyclable materials and eco-friendlier packaging solutions.

Strategic Outlook for Prefilled Pod Vape Market

The strategic outlook for the prefilled pod vape market remains overwhelmingly positive, driven by continuous innovation and expanding consumer adoption. Key growth accelerators include the relentless pursuit of higher puff counts and improved battery life, directly addressing consumer demand for convenience and value. Strategic opportunities lie in developing more sustainable product lines and exploring advanced nicotine delivery systems to cater to a broader range of preferences. Manufacturers that can effectively navigate evolving regulatory landscapes and build strong online and offline distribution networks will be best positioned for success. The market's ability to adapt to consumer trends, particularly in flavor innovation and device aesthetics, will be crucial for sustained growth and market leadership in the coming years.

Prefilled Pod Vape Segmentation

-

1. Application

- 1.1. Online Sales

- 1.2. Offline Sales

-

2. Types

- 2.1. 8000-10000 Puffs

- 2.2. >10000 Puffs

- 2.3. Others

Prefilled Pod Vape Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Prefilled Pod Vape Regional Market Share

Geographic Coverage of Prefilled Pod Vape

Prefilled Pod Vape REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 19.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Prefilled Pod Vape Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Online Sales

- 5.1.2. Offline Sales

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 8000-10000 Puffs

- 5.2.2. >10000 Puffs

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Prefilled Pod Vape Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Online Sales

- 6.1.2. Offline Sales

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 8000-10000 Puffs

- 6.2.2. >10000 Puffs

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Prefilled Pod Vape Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Online Sales

- 7.1.2. Offline Sales

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. 8000-10000 Puffs

- 7.2.2. >10000 Puffs

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Prefilled Pod Vape Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Online Sales

- 8.1.2. Offline Sales

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. 8000-10000 Puffs

- 8.2.2. >10000 Puffs

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Prefilled Pod Vape Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Online Sales

- 9.1.2. Offline Sales

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. 8000-10000 Puffs

- 9.2.2. >10000 Puffs

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Prefilled Pod Vape Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Online Sales

- 10.1.2. Offline Sales

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. 8000-10000 Puffs

- 10.2.2. >10000 Puffs

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 BAT

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Altria Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 SMOORE

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Shenzhen Yinghe Technology

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 RLX Technology

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 iMiracle

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 ELUX

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 HQD

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Geek Bar

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 FLUM

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Blu

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 10 Motives

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 BAT

List of Figures

- Figure 1: Global Prefilled Pod Vape Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Prefilled Pod Vape Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Prefilled Pod Vape Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Prefilled Pod Vape Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Prefilled Pod Vape Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Prefilled Pod Vape Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Prefilled Pod Vape Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Prefilled Pod Vape Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Prefilled Pod Vape Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Prefilled Pod Vape Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Prefilled Pod Vape Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Prefilled Pod Vape Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Prefilled Pod Vape Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Prefilled Pod Vape Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Prefilled Pod Vape Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Prefilled Pod Vape Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Prefilled Pod Vape Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Prefilled Pod Vape Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Prefilled Pod Vape Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Prefilled Pod Vape Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Prefilled Pod Vape Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Prefilled Pod Vape Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Prefilled Pod Vape Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Prefilled Pod Vape Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Prefilled Pod Vape Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Prefilled Pod Vape Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Prefilled Pod Vape Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Prefilled Pod Vape Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Prefilled Pod Vape Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Prefilled Pod Vape Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Prefilled Pod Vape Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Prefilled Pod Vape Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Prefilled Pod Vape Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Prefilled Pod Vape Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Prefilled Pod Vape Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Prefilled Pod Vape Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Prefilled Pod Vape Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Prefilled Pod Vape Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Prefilled Pod Vape Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Prefilled Pod Vape Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Prefilled Pod Vape Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Prefilled Pod Vape Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Prefilled Pod Vape Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Prefilled Pod Vape Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Prefilled Pod Vape Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Prefilled Pod Vape Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Prefilled Pod Vape Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Prefilled Pod Vape Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Prefilled Pod Vape Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Prefilled Pod Vape Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Prefilled Pod Vape?

The projected CAGR is approximately 19.5%.

2. Which companies are prominent players in the Prefilled Pod Vape?

Key companies in the market include BAT, Altria Group, SMOORE, Shenzhen Yinghe Technology, RLX Technology, iMiracle, ELUX, HQD, Geek Bar, FLUM, Blu, 10 Motives.

3. What are the main segments of the Prefilled Pod Vape?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Prefilled Pod Vape," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Prefilled Pod Vape report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Prefilled Pod Vape?

To stay informed about further developments, trends, and reports in the Prefilled Pod Vape, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence