Key Insights

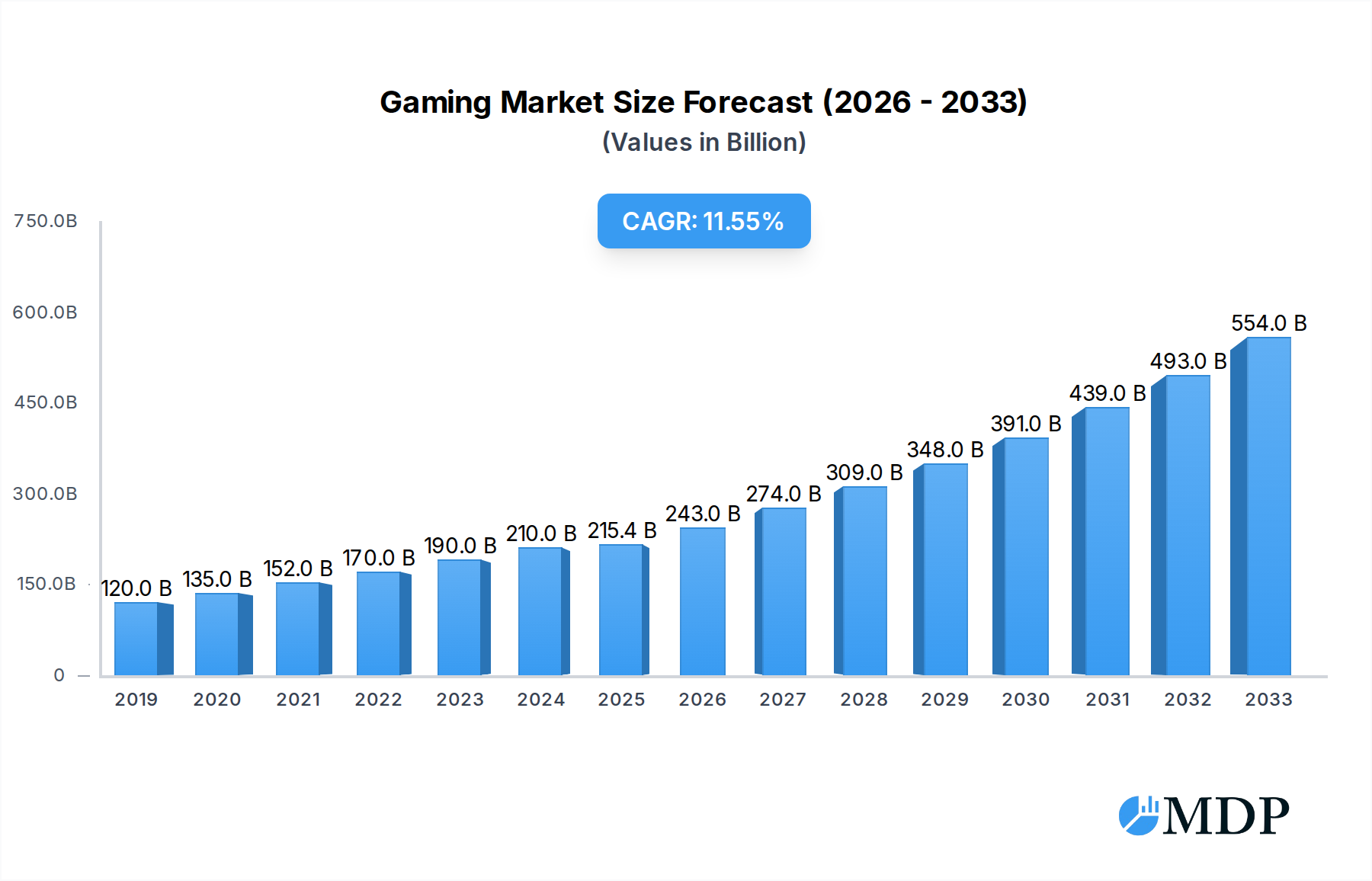

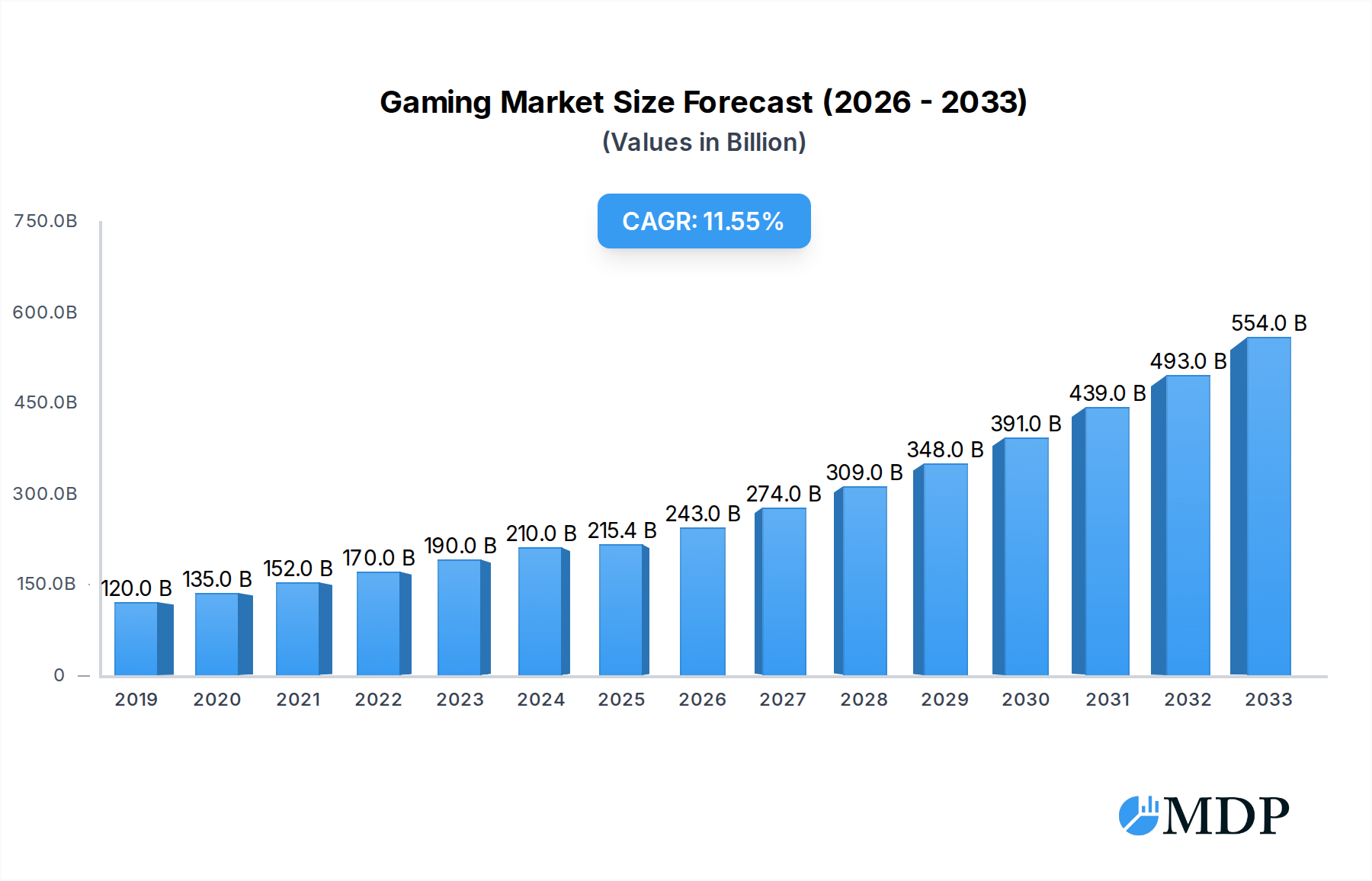

The global gaming market is experiencing robust expansion, projected to reach a substantial $215,430 million by 2025, fueled by an impressive Compound Annual Growth Rate (CAGR) of 12.8%. This dynamic sector is characterized by a confluence of innovative technologies, evolving player demographics, and increasing accessibility across diverse platforms. The proliferation of mobile devices and advancements in cloud gaming are democratizing access, enabling a wider audience to engage with sophisticated gaming experiences. Furthermore, the rise of esports and the increasing integration of social features within games are fostering vibrant communities and driving deeper engagement. Significant investments from major technology and entertainment giants underscore the immense potential and strategic importance of this market. The continued development of virtual and augmented reality technologies also promises to usher in new frontiers for immersive gameplay, further propelling market growth.

Gaming Market Size (In Billion)

The gaming industry's growth trajectory is further supported by strong performance across its various segments. Mobile gaming, in particular, is a dominant force, capitalizing on the widespread adoption of smartphones and the availability of free-to-play titles. Console gaming continues to hold a significant share, driven by high-fidelity experiences and exclusive titles from industry leaders. PC gaming remains a cornerstone, distinguished by its deep customization options and the thriving ecosystem of online multiplayer games and streaming. Emerging markets, particularly in the Asia Pacific region, are anticipated to be key growth engines, owing to their large, digitally connected populations and a burgeoning middle class with increasing disposable income for entertainment. While the market is largely propelled by innovation and consumer demand, factors such as the increasing cost of game development and potential regulatory shifts could present challenges that market players will need to navigate strategically.

Gaming Company Market Share

This comprehensive report delves deep into the dynamic global gaming market, a sector projected to surpass $200 million in value. We meticulously analyze market trends, innovations, and strategic imperatives from the historical period of 2019–2024, with a robust forecast extending to 2033. Leveraging the Base Year of 2025 and Estimated Year of 2025, this study provides unparalleled insights for industry stakeholders.

Gaming Market Dynamics & Concentration

The global gaming market exhibits a moderate level of concentration, with a few key players holding significant market share. However, a vibrant ecosystem of innovative independent studios and emerging technologies fosters healthy competition. Innovation drivers are primarily fueled by advancements in graphics, artificial intelligence, virtual reality (VR), and augmented reality (AR), pushing the boundaries of immersive gameplay. Regulatory frameworks vary significantly across regions, influencing content guidelines, monetization strategies, and player data privacy. Product substitutes are increasingly prevalent, ranging from other entertainment forms to alternative gaming platforms. End-user trends reveal a growing demand for personalized experiences, social interaction within games, and accessible, free-to-play models. Merger and acquisition (M&A) activities have been robust, with an estimated 500+ deals valued in the billions of dollars during the historical period. This consolidation aims to acquire new technologies, expand user bases, and diversify portfolios. For instance, key acquisitions have reshaped the landscape of mobile gaming and PC gaming.

- Market Share Analysis: Dominant players command significant portions of the market, though niche segments offer substantial growth potential.

- M&A Deal Counts: Historically, M&A activity has averaged 50+ deals per year, indicating a strong trend of consolidation and strategic partnerships.

- Innovation Focus: Investments in R&D for VR/AR and AI are pivotal for sustained competitive advantage.

- Regulatory Impact: Evolving regulations in regions like Europe and Asia necessitate adaptive business strategies.

Gaming Industry Trends & Analysis

The gaming industry is experiencing unprecedented growth, driven by a confluence of technological advancements, shifting consumer preferences, and increased accessibility. The Compound Annual Growth Rate (CAGR) for the overall gaming market is projected at an impressive 15% during the forecast period of 2025–2033. Market penetration continues to expand globally, with billions of individuals engaging with various forms of gaming. The rise of mobile gaming has been a transformative force, democratizing access and attracting a vast new demographic. Cloud gaming services are gaining traction, promising to lower hardware barriers and enable seamless play across devices. Esports is evolving into a mainstream entertainment phenomenon, with professional leagues, substantial prize pools, and dedicated fan bases. The integration of blockchain technology and NFTs is exploring new monetization models and ownership paradigms, though this remains a nascent area with ongoing debate. Social gaming features and community building are integral to player retention and engagement strategies. The demand for hyper-realistic graphics and more sophisticated gameplay mechanics continues to push the boundaries of console gaming and PC gaming. Content creation by players and influencers is becoming an increasingly vital aspect of game promotion and community development.

Leading Markets & Segments in Gaming

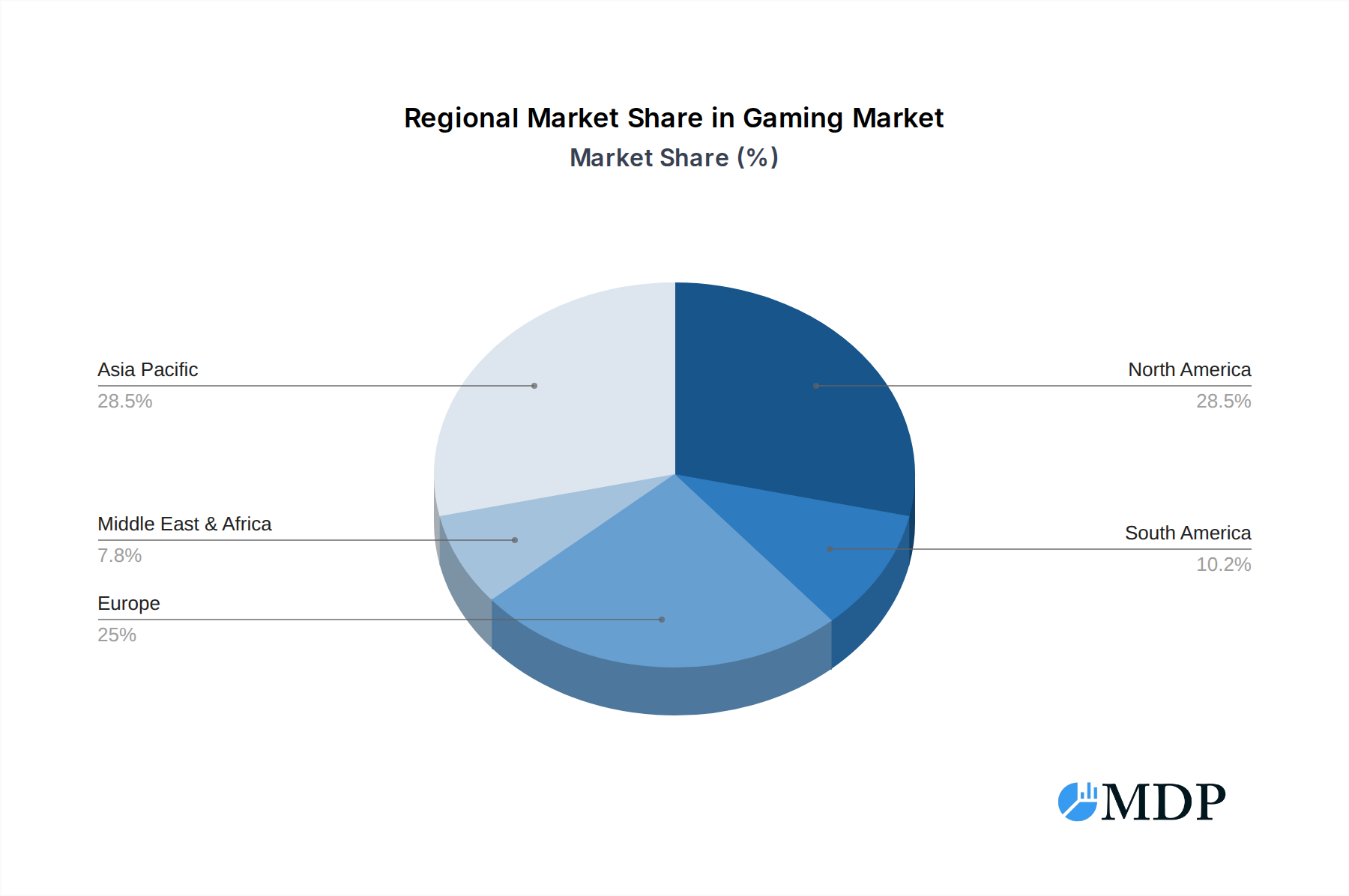

The Asia-Pacific region stands out as the dominant force in the global gaming market, driven by rapid economic growth, a massive digitally connected population, and a strong cultural affinity for gaming. Within this region, China represents the single largest market, contributing an estimated 35% of global gaming revenue. Mobile gaming reigns supreme globally, accounting for over 60% of market share. This dominance is fueled by the widespread adoption of smartphones and the accessibility of free-to-play titles. Amateur gamers constitute the largest user segment, representing over 90% of the total player base, seeking entertainment and casual engagement. However, the Professional segment, particularly within esports, is experiencing exponential growth, attracting significant investment and viewership.

- Dominant Region: Asia-Pacific, with China as the primary market driver.

- Dominant Type: Mobile Gaming, due to its ubiquity and accessibility.

- Dominant Application: Amateur, comprising the vast majority of the player base.

- Key Drivers of Regional Dominance (Asia-Pacific):

- Economic Policies: Supportive government initiatives and investment in digital infrastructure.

- Infrastructure: Widespread internet penetration and affordable mobile devices.

- Cultural Factors: Strong gaming culture and high adoption rates of new technologies.

- Key Drivers of Segment Dominance (Mobile Gaming & Amateur Application):

- Accessibility & Affordability: Low entry cost and availability on ubiquitous devices.

- Diverse Content: A vast array of genres catering to all preferences.

- Social Connectivity: Integrated social features enhancing engagement.

Gaming Product Developments

Product innovations in the gaming sector are characterized by a relentless pursuit of enhanced immersion and interactivity. Advancements in graphics rendering, spatial audio, and haptic feedback technologies are creating more realistic and engaging player experiences. The integration of AI is leading to more sophisticated non-player characters (NPCs) and procedurally generated content, offering dynamic gameplay. Cloud gaming solutions are democratizing access to high-fidelity gaming, eliminating the need for expensive hardware. Furthermore, the exploration of blockchain technology and NFTs is paving the way for new forms of digital ownership and in-game economies. These developments are crucial for maintaining competitive advantage and capturing new market segments.

Key Drivers of Gaming Growth

Several key factors are propelling the growth of the gaming market. Technological advancements, particularly in graphics processing, AI, and cloud computing, are enabling more sophisticated and accessible gaming experiences. The increasing global internet penetration and smartphone adoption are expanding the addressable market, especially in emerging economies. Evolving consumer preferences towards interactive entertainment and social gaming experiences are fostering higher engagement. Furthermore, supportive economic policies in many regions, alongside a growing esports ecosystem, are creating a favorable environment for sustained expansion.

Challenges in the Gaming Market

Despite robust growth, the gaming market faces several challenges. Stringent regulatory frameworks in certain countries regarding in-game monetization and data privacy can create operational complexities. Supply chain disruptions, particularly for hardware components like GPUs, can impact the availability and pricing of gaming consoles and PCs. Intense competition from established players and new entrants necessitates continuous innovation and strategic marketing. Furthermore, the rising cost of game development and marketing campaigns presents a significant barrier for smaller studios. The potential for negative public perception surrounding addiction or ethical concerns also requires careful management.

Emerging Opportunities in Gaming

The gaming industry is ripe with emerging opportunities. The continued expansion of cloud gaming presents a significant catalyst for broader market penetration. The metaverse concept, though still developing, offers a long-term vision for persistent, interconnected virtual worlds with new monetization and social interaction possibilities. The integration of AI into game design and player engagement promises more personalized and adaptive experiences. Strategic partnerships between traditional entertainment companies and gaming studios are unlocking cross-media synergies. Furthermore, the growing demand for location-based augmented reality games and experiences offers a unique avenue for innovation.

Leading Players in the Gaming Sector

- Activision Blizzard

- Electronic Arts

- Microsoft

- NetEase

- Nintendo

- Sony

- Tencent

- ChangYou

- DeNA

- GungHo

- Apple

- Nexon

- Sega

- Warner Bros

- Namco Bandai

- Ubisoft

- Square Enix

- Take-Two Interactive

- King Digital Entertainment

Key Milestones in Gaming Industry

- 2019: Launch of Google Stadia, pushing cloud gaming into mainstream awareness.

- 2020: Release of next-generation consoles PlayStation 5 and Xbox Series X/S, driving hardware sales and ushering in a new era of graphical fidelity.

- 2021: Significant surge in NFT gaming and play-to-earn models, attracting considerable investment and debate.

- 2022: Continued growth of esports, with major tournaments attracting millions of viewers and substantial prize pools.

- 2023: Increased focus on cross-platform play and persistent online worlds, blurring lines between different gaming ecosystems.

- 2024: Advancements in AI-driven game development and personalized player experiences becoming more prominent.

Strategic Outlook for Gaming Market

The strategic outlook for the gaming market remains exceptionally strong, fueled by ongoing technological innovation and evolving consumer engagement. Growth accelerators include the continued maturation of cloud gaming, the exploration of decentralized technologies like blockchain for unique player economies, and the increasing integration of AI for personalized gameplay. Strategic partnerships and mergers will continue to consolidate market power and foster innovation. The expansion into new geographic markets and the development of metaverse-like experiences represent significant future growth potential. Investing in user acquisition, retention through engaging content, and adapting to emerging monetization strategies will be critical for success.

Gaming Segmentation

-

1. Application

- 1.1. Amateur

- 1.2. Professional

-

2. Types

- 2.1. Mobile Gaming

- 2.2. Console Gaming

- 2.3. PC Gaming

Gaming Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Gaming Regional Market Share

Geographic Coverage of Gaming

Gaming REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Gaming Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Amateur

- 5.1.2. Professional

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Mobile Gaming

- 5.2.2. Console Gaming

- 5.2.3. PC Gaming

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Gaming Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Amateur

- 6.1.2. Professional

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Mobile Gaming

- 6.2.2. Console Gaming

- 6.2.3. PC Gaming

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Gaming Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Amateur

- 7.1.2. Professional

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Mobile Gaming

- 7.2.2. Console Gaming

- 7.2.3. PC Gaming

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Gaming Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Amateur

- 8.1.2. Professional

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Mobile Gaming

- 8.2.2. Console Gaming

- 8.2.3. PC Gaming

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Gaming Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Amateur

- 9.1.2. Professional

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Mobile Gaming

- 9.2.2. Console Gaming

- 9.2.3. PC Gaming

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Gaming Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Amateur

- 10.1.2. Professional

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Mobile Gaming

- 10.2.2. Console Gaming

- 10.2.3. PC Gaming

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Activision Blizzard

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Electronic Arts

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Microsoft

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 NetEase

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Nintendo

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Sony

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Tencent

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 ChangYou

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 DeNA

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 GungHo

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Apple

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Google

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Nexon

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Sega

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Warner Bros

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Namco Bandai

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Ubisoft

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Square Enix

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Take-Two Interactive

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 King Digital Entertainment

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 Activision Blizzard

List of Figures

- Figure 1: Global Gaming Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Gaming Revenue (million), by Application 2025 & 2033

- Figure 3: North America Gaming Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Gaming Revenue (million), by Types 2025 & 2033

- Figure 5: North America Gaming Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Gaming Revenue (million), by Country 2025 & 2033

- Figure 7: North America Gaming Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Gaming Revenue (million), by Application 2025 & 2033

- Figure 9: South America Gaming Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Gaming Revenue (million), by Types 2025 & 2033

- Figure 11: South America Gaming Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Gaming Revenue (million), by Country 2025 & 2033

- Figure 13: South America Gaming Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Gaming Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Gaming Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Gaming Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Gaming Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Gaming Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Gaming Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Gaming Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Gaming Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Gaming Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Gaming Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Gaming Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Gaming Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Gaming Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Gaming Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Gaming Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Gaming Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Gaming Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Gaming Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Gaming Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Gaming Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Gaming Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Gaming Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Gaming Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Gaming Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Gaming Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Gaming Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Gaming Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Gaming Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Gaming Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Gaming Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Gaming Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Gaming Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Gaming Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Gaming Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Gaming Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Gaming Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Gaming Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Gaming Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Gaming?

The projected CAGR is approximately 12.8%.

2. Which companies are prominent players in the Gaming?

Key companies in the market include Activision Blizzard, Electronic Arts, Microsoft, NetEase, Nintendo, Sony, Tencent, ChangYou, DeNA, GungHo, Apple, Google, Nexon, Sega, Warner Bros, Namco Bandai, Ubisoft, Square Enix, Take-Two Interactive, King Digital Entertainment.

3. What are the main segments of the Gaming?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 215430 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Gaming," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Gaming report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Gaming?

To stay informed about further developments, trends, and reports in the Gaming, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence