Key Insights

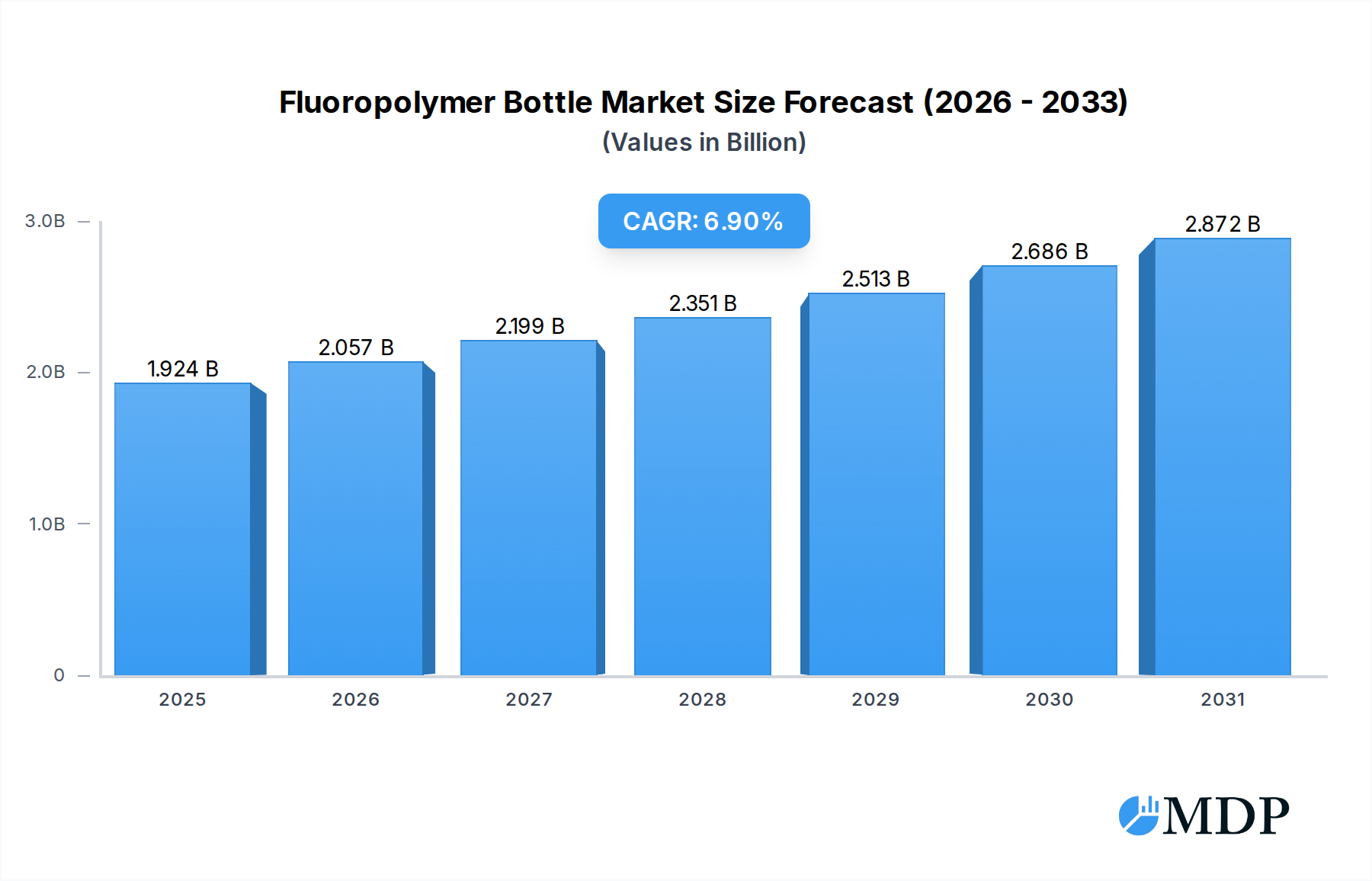

The Fluoropolymer Bottle Market is demonstrating robust expansion, currently valued at an estimated $1.8 billion in 2025. Projections indicate a substantial growth trajectory, with the market expected to reach approximately $3.27 billion by 2034, propelled by a compound annual growth rate (CAGR) of 6.9% over the forecast period. This significant growth is primarily driven by the escalating demand for high-purity, chemically inert, and temperature-resistant packaging solutions across critical industries. The unique properties of fluoropolymers, including exceptional chemical resistance, minimal extractables, and resistance to extreme temperatures, make them indispensable for storing and transporting aggressive chemicals, sensitive pharmaceutical formulations, and biological reagents.

Fluoropolymer Bottle Market Size (In Billion)

Key demand drivers include the expansion of the High-Purity Chemical Market, especially within the semiconductor manufacturing sector, which necessitates ultra-clean and non-reactive containers to prevent contamination of sensitive materials. Furthermore, the burgeoning Pharmaceutical Packaging Market and Biotechnology Tools Market are significant contributors, as fluoropolymer bottles ensure the integrity and stability of high-value drug substances, reagents, and samples. Regulatory stringency regarding material compatibility and container purity in these sectors further underpins market growth. The increasing adoption of advanced analytical techniques in research and academic laboratories also fuels the demand for high-performance Laboratory Consumables Market products, including fluoropolymer bottles.

Fluoropolymer Bottle Company Market Share

Macro tailwinds such as ongoing innovation in fluoropolymer material science, leading to enhanced performance characteristics and broader application scope, are also playing a crucial role. The shift towards sustainable manufacturing practices and the development of recyclable or bio-based fluoropolymer alternatives, while nascent, present long-term opportunities for market players. The rising demand from emerging economies, particularly in Asia Pacific, for sophisticated industrial and healthcare infrastructure is another potent growth accelerator. The inherent advantages of fluoropolymer bottles over traditional materials like glass or conventional plastics in terms of safety, durability, and chemical inertness solidify their critical position in highly specialized applications, ensuring a sustained positive outlook for the Fluoropolymer Bottle Market into the next decade.

PFA and PTFE Material Type Dominance in Fluoropolymer Bottle Market

Within the Fluoropolymer Bottle Market, the material type segment, specifically Perfluoroalkoxy (PFA) and Polytetrafluoroethylene (PTFE), represents the single largest segment by revenue share, asserting a dominant position due to their unparalleled performance characteristics crucial for highly demanding applications. While granular revenue share data for individual material types isn't explicitly provided, industry analysis consistently places PFA and PTFE at the forefront in value-driven segments due to their superior properties compared to other fluoropolymers like FEP, ETFE, PVDF, PCTFE, and ECTFE. These two materials command premium pricing and are indispensable in sectors where compromise on purity, chemical inertness, and thermal stability is unacceptable.

PFA bottles are highly valued for their exceptional chemical resistance, broad temperature range capability (from cryogenic to high temperatures up to 260°C), and excellent electrical insulation properties. Critically, PFA is melt-processible, allowing for a broader range of fabrication techniques and producing smooth, non-porous surfaces that prevent particle shedding and minimize extractables. This makes PFA bottles the material of choice for the storage and transfer of ultra-high-purity chemicals, aggressive acids, bases, and organic solvents, particularly in the semiconductor, pharmaceutical, and biotechnology industries. Manufacturers such as Savillex Corporation and Nalgene (Thermo Fisher Scientific) extensively utilize PFA for their high-end bottle lines, targeting applications where trace contamination can lead to significant process failures or compromised product integrity.

PTFE, while not melt-processible in the same way as PFA, offers the highest level of chemical resistance and lowest coefficient of friction among all fluoropolymers. PTFE bottles are typically manufactured through specialized molding and sintering processes. They are favored for applications requiring extreme chemical inertness and resistance to virtually all chemicals, solvents, and corrosive agents, often used for laboratory standards, high-acidity samples, or highly aggressive media that even PFA might struggle with under certain conditions. Companies like Zeus Industrial Products, Inc. and Fluorotherm Polymers, Inc. are prominent in offering PTFE-based solutions, capitalizing on its robust chemical profile.

The dominance of PFA and PTFE is attributed to several factors. Firstly, the stringent regulatory requirements in end-user industries such as pharmaceuticals and semiconductors mandate materials that will not leach contaminants into sensitive formulations. PFA and PTFE inherently meet these criteria due to their stable C-F bonds. Secondly, the increasing complexity and value of chemicals and biological reagents necessitate packaging that preserves their integrity without degradation or interaction. The ongoing expansion of the High-Purity Chemical Market and the growing complexity of biological drugs in the Biotechnology Tools Market directly amplify the demand for these premium materials.

While other fluoropolymers like FEP offer good chemical resistance and melt-processibility at a lower cost than PFA, they typically do not match the ultimate purity and thermal performance of PFA. PVDF provides excellent abrasion resistance and mechanical strength, making it suitable for certain Industrial Packaging Market applications but is generally less chemically inert than PFA or PTFE. Consequently, the revenue share of PFA and PTFE is not only maintained but is expected to consolidate further in the high-value segments, as end-users continue to prioritize performance and purity over cost for critical applications, ensuring their enduring supremacy in the Fluoropolymer Bottle Market.

Key Market Drivers & Constraints in Fluoropolymer Bottle Market

The Fluoropolymer Bottle Market's trajectory is shaped by a confluence of potent drivers and inherent constraints, each influencing its growth and adoption. A primary driver is the accelerating demand for high-purity chemical storage and transport solutions across various high-tech sectors. For instance, the global semiconductor industry, projected to grow significantly, relies heavily on ultra-high-purity (UHP) chemicals, often specifying fluoropolymer bottles to prevent contamination. Any trace of metallic ions or organic leachables can compromise chip manufacturing processes, making the inertness of materials like PFA and PTFE critical. This imperative for contamination control drives significant investment in advanced fluoropolymer containers.

Another significant driver is the stringent regulatory landscape in the Pharmaceutical Packaging Market and Biotechnology Tools Market. Regulatory bodies like the FDA and EMA impose strict guidelines on packaging materials to ensure drug stability, safety, and efficacy. Fluoropolymer bottles, particularly those made from PFA, meet these rigorous standards due to their low extractable profiles and exceptional chemical resistance, which are crucial for preventing interactions with sensitive APIs (Active Pharmaceutical Ingredients) and biological reagents. The projected growth in biopharmaceuticals and personalized medicine amplifies this demand, as these high-value products require the utmost material integrity.

Conversely, the high cost of fluoropolymer resins acts as a substantial constraint on the Fluoropolymer Bottle Market. Materials such as PFA and PTFE are significantly more expensive than conventional plastics like HDPE or PP, and even other engineering plastics. This cost factor can deter adoption in less sensitive or bulk industrial applications where the superior properties of fluoropolymers might be over-specified or where budget constraints are tighter. This cost differential creates a barrier to entry for new applications outside of critical, high-value sectors, limiting the broader Plastic Bottle Market penetration of fluoropolymer options.

Furthermore, the specialized manufacturing processes required for fluoropolymer bottles, particularly for materials like PTFE that are not melt-processible, contribute to higher production costs and complexity. This often requires highly specialized equipment and skilled labor, which can limit the number of manufacturers and create supply chain bottlenecks. While the performance benefits justify the cost in specialized niches, this constraint impacts market scalability. The competitive landscape from alternative materials, such as high-grade borosilicate glass in some laboratory settings or advanced polyethylene and polypropylene resins with barrier coatings, also presents a constraint. These alternatives offer competitive price points for applications where fluoropolymer's extreme properties are not strictly necessary, challenging the market share of fluoropolymer bottles in certain segments.

Competitive Ecosystem of Fluoropolymer Bottle Market

The Fluoropolymer Bottle Market is characterized by a mix of specialized manufacturers focusing on high-performance plastics and broader chemical/life science conglomerates. Competition hinges on material expertise, manufacturing precision, and adherence to stringent industry standards.

- Savillex Corporation: A prominent player renowned for its high-purity fluoropolymer products, particularly PFA bottles, specializing in applications requiring ultra-low trace metal contamination, making them essential for the semiconductor and analytical laboratory sectors.

- Saint-Gobain Performance Plastics: A global leader offering a wide array of advanced material solutions, including fluoropolymer products tailored for critical fluid handling and storage in the chemical, pharmaceutical, and industrial sectors.

- Thermo Fisher Scientific: A major scientific instrumentation and consumables provider, offering Nalgene brand fluoropolymer bottles that are widely used in research, clinical, and industrial laboratories for their reliability and chemical resistance.

- DWK Life Sciences: Known for its DURAN Group, Wheaton, and Kimble brands, this company provides high-quality laboratory glassware and plasticware, including specialized fluoropolymer containers for demanding scientific applications.

- Nalgene (Thermo Fisher Scientific): A leading brand under Thermo Fisher Scientific, offering a comprehensive range of plastic labware, with a strong portfolio of PFA and FEP bottles critical for corrosive chemical handling and sterile media storage.

- AMETEK Fluoropolymer Products: Specializes in fluoropolymer components and systems, focusing on providing high-performance solutions for chemical processing, semiconductor manufacturing, and other industries requiring chemical inertness.

- Entegris, Inc.: A key supplier to the semiconductor industry, offering advanced materials handling solutions, including high-purity fluoropolymer containers and fluid management systems essential for semiconductor manufacturing processes.

- NICHIAS Corporation: A Japanese company providing a diverse range of industrial products, including fluoropolymer-lined equipment and components, serving various industries with solutions for high-purity fluid transport and storage.

- Zeus Industrial Products, Inc.: A leading polymer extrusion manufacturer, recognized for its expertise in custom fluoropolymer tubing and components, with capabilities extending to specialized container applications requiring high chemical resistance.

- Fluorotherm Polymers, Inc.: Focuses on innovative fluoropolymer products, including custom tubing and heat exchangers, offering expertise in applications demanding high temperature and chemical resistance.

- Chang Zhou Feng Di Plastic Technology: A Chinese manufacturer specializing in fluoroplastic products, including bottles, catering to industrial and laboratory applications with competitive solutions.

- AGC Chemicals Americas: A subsidiary of AGC Inc., a global chemical company, providing a range of fluorochemicals and fluoropolymer materials used in various high-performance applications, including bottle manufacturing.

- Daikin Industries Ltd.: A diversified global manufacturer, including a strong chemicals division that produces fluoropolymers, which serve as essential raw materials for fluoropolymer bottle production globally.

Recent Developments & Milestones in Fluoropolymer Bottle Market

The Fluoropolymer Bottle Market has witnessed a steady stream of advancements and strategic activities aimed at enhancing product performance, sustainability, and market reach. These developments reflect the industry's response to evolving end-user demands and technological progress.

- March 2024: Savillex Corporation announced the expansion of its PFA bottle manufacturing capacity in North America, addressing the surging demand from the semiconductor and life sciences sectors for ultra-high-purity packaging, particularly for the High-Purity Chemical Market.

- January 2024: A major fluoropolymer resin producer, Daikin Industries Ltd., unveiled new grades of sustainable fluoropolymers with reduced environmental impact, signaling a shift towards greener materials that could influence future fluoropolymer bottle compositions.

- November 2023: Entegris, Inc. launched a new line of advanced PFA containers designed specifically for next-generation lithography chemicals, offering enhanced safety features and improved chemical compatibility for sub-10nm semiconductor manufacturing processes.

- August 2023: Thermo Fisher Scientific (Nalgene) introduced a new range of FEP bottles featuring improved clarity and resistance to photo-degradation, catering to Laboratory Consumables Market needs for sensitive light-reactive reagents.

- June 2023: Saint-Gobain Performance Plastics partnered with a leading pharmaceutical company to develop custom fluoropolymer bottle solutions for novel mRNA vaccine storage, emphasizing inertness and temperature stability crucial for the Pharmaceutical Packaging Market.

- April 2023: Zeus Industrial Products, Inc. highlighted its capabilities in producing custom fluoropolymer components for medical devices and diagnostics, including specialized bottle inserts and liners, indicating a strategic focus on high-value segments within the Biotechnology Tools Market.

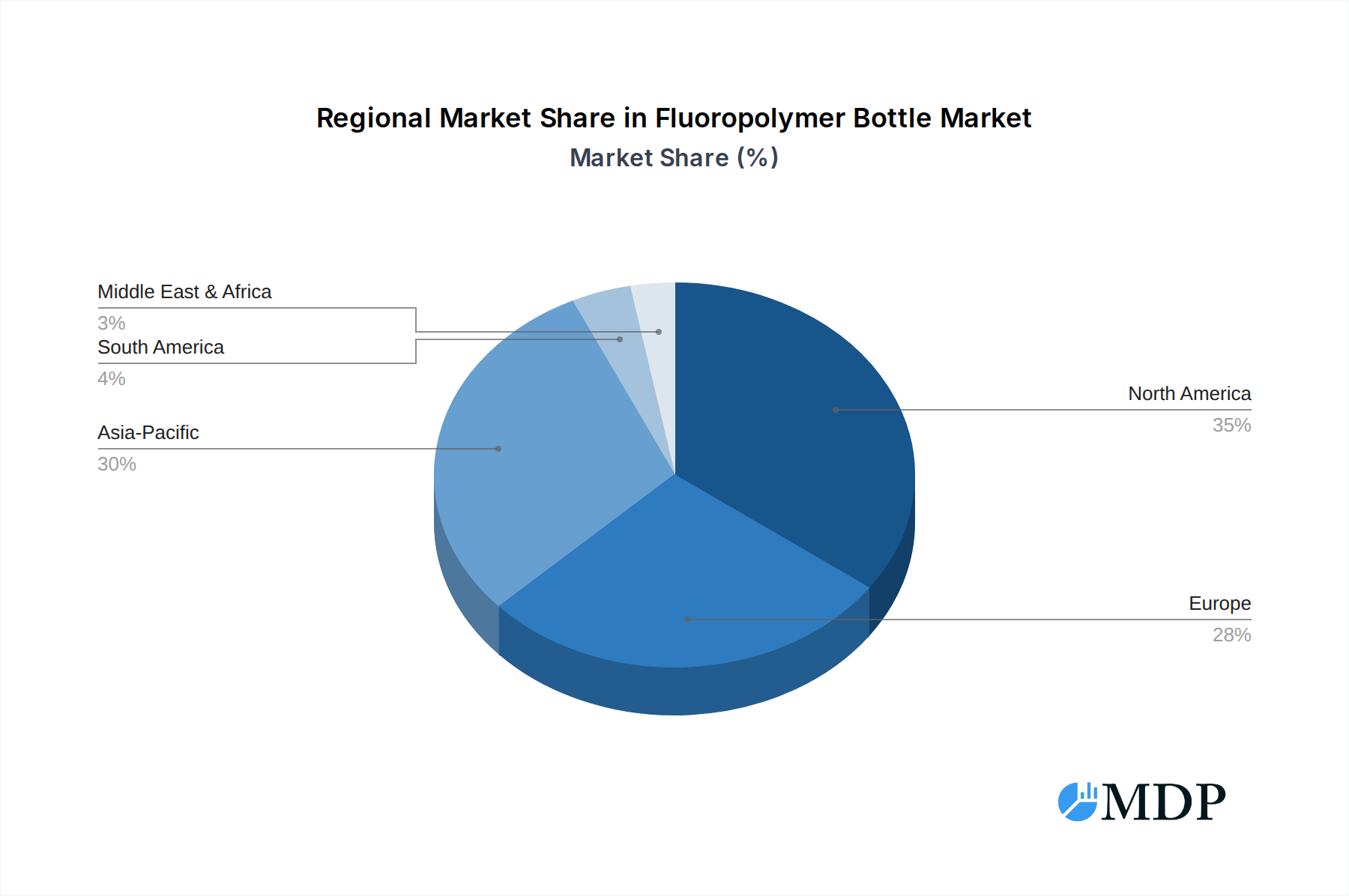

Regional Market Breakdown for Fluoropolymer Bottle Market

The global Fluoropolymer Bottle Market exhibits distinct regional dynamics driven by industrial development, regulatory frameworks, and technological adoption rates. While specific regional market values are inferred, the growth trajectories and key drivers vary significantly across geographies.

North America holds a substantial share of the Fluoropolymer Bottle Market, primarily driven by its well-established pharmaceutical, biotechnology, and semiconductor industries. The United States, in particular, is a major consumer due to its robust R&D infrastructure and strict regulatory environment necessitating high-purity packaging. The demand for Chemical Storage Market solutions in advanced manufacturing and life sciences, coupled with a high adoption rate of premium laboratory consumables, underpins the market. North America is considered a mature market with a stable, albeit steady, growth rate.

Europe represents another significant market, characterized by stringent environmental and safety regulations, particularly in Germany, France, and the UK. The region's strong chemical, pharmaceutical, and research sectors are key demand generators. Countries like Germany, with its robust chemical and automotive industries, and Switzerland, with its leading pharmaceutical sector, are major contributors. The emphasis on high-quality and sustainable packaging solutions supports the Fluoropolymer Bottle Market here, with growth driven by continuous innovation and adherence to quality standards. This region, like North America, is also relatively mature but continues to see steady demand.

Asia Pacific is poised to be the fastest-growing region in the Fluoropolymer Bottle Market, exhibiting a significantly higher CAGR than other regions. This accelerated growth is primarily fueled by rapid industrialization, expanding manufacturing capabilities, and burgeoning pharmaceutical and semiconductor industries in China, India, Japan, and South Korea. Investments in new semiconductor fabs in Taiwan and South Korea, coupled with the growth of the High-Purity Chemical Market across the region, are major demand drivers. The increasing focus on improving healthcare infrastructure and expanding R&D activities in countries like China and India further stimulates the adoption of fluoropolymer bottles. The cost-effectiveness of local production also plays a role in its rapid expansion.

Middle East & Africa (MEA) and South America collectively represent emerging markets for fluoropolymer bottles. While smaller in overall market share, these regions are expected to demonstrate moderate growth. In MEA, investments in petrochemicals and industrial diversification are slowly driving demand, especially for specialized Industrial Packaging Market applications. In South America, particularly Brazil and Argentina, the growing pharmaceutical sector and increasing R&D investments are gradually contributing to market expansion. However, these regions face challenges such as economic volatility and less developed industrial infrastructure compared to leading markets, impacting their pace of adoption.

Fluoropolymer Bottle Regional Market Share

Pricing Dynamics & Margin Pressure in Fluoropolymer Bottle Market

The pricing dynamics in the Fluoropolymer Bottle Market are intrinsically linked to the high-performance characteristics of fluoropolymers and the specialized nature of their applications. Average selling prices (ASPs) for fluoropolymer bottles are considerably higher than those for standard Plastic Bottle Market products, reflecting the premium cost of raw materials (PTFE, PFA, FEP resins), complex manufacturing processes, and the value proposition of superior chemical inertness and purity. PFA bottles, offering the highest level of performance and melt-processibility, typically command the highest ASPs, followed by PTFE and FEP.

Margin structures across the value chain are generally robust in this niche market, especially for manufacturers offering highly specialized, ultra-high-purity products for critical applications like semiconductor manufacturing or pharmaceutical grade storage. Raw material suppliers, such as Daikin Industries Ltd. and AGC Chemicals Americas, hold significant pricing power due to the proprietary nature and high barriers to entry in fluoropolymer resin production. Fabricators, like Savillex Corporation or specialized divisions of Thermo Fisher Scientific, then add value through precision molding, specialized cleaning processes (e.g., acid washing), and certification to meet specific industry standards (e.g., USP Class VI for pharma). These value-added steps justify higher margins.

Key cost levers influencing pricing include the volatile cost of crude oil (a feedstock for some fluoropolymer precursors), energy prices for high-temperature processing, and the cost of highly specialized equipment and cleanroom facilities. Fluctuations in the Specialty Polymers Market commodity cycles, particularly for fluorine-based chemicals, directly impact the cost of fluoropolymer resins, subsequently affecting the pricing of finished bottles. Intense competition, especially from Asian manufacturers who might offer more cost-effective solutions for less stringent applications, can exert margin pressure on global players. However, for critical, high-purity applications, the emphasis remains on performance and reliability rather than cost, allowing leading manufacturers to maintain premium pricing. Technological advancements aimed at reducing manufacturing waste or improving processing efficiency can offer avenues for cost optimization and margin enhancement, while stringent quality control and certification processes remain non-negotiable cost components.

Investment & Funding Activity in Fluoropolymer Bottle Market

Investment and funding activity in the Fluoropolymer Bottle Market, while not as prolific as in broader tech sectors, is consistently directed towards strategic growth areas, primarily focusing on capacity expansion, material innovation, and enhancing product offerings for high-value end-user industries. Over the past 2-3 years, M&A activity has been more about strategic consolidation or vertical integration rather than widespread venture funding rounds, given the mature and specialized nature of many players. Large chemical companies or industrial conglomerates often acquire smaller, specialized fabricators to gain market share or specific technological expertise.

For instance, major players in the Industrial Packaging Market and Chemical Storage Market spheres have shown interest in acquiring niche fluoropolymer manufacturers to diversify their product portfolios and cater to the growing demand for high-purity applications. While no major publicly announced M&A deals specifically for fluoropolymer bottle manufacturers have dominated headlines in the immediate past, parent companies or divisions involved in fluoropolymer production continually evaluate opportunities to strengthen their positions in advanced materials.

Strategic partnerships are more common, often between fluoropolymer resin producers and bottle manufacturers to co-develop new material grades with enhanced properties (e.g., improved clarity, barrier properties, or sustainability profiles) or with end-users to create custom solutions for novel applications. For example, collaborations between fluoropolymer bottle suppliers and Biotechnology Tools Market companies are crucial for developing specialized containers for sensitive biologics and cell therapies. Similarly, partnerships with semiconductor equipment manufacturers ensure that fluoropolymer fluid handling components meet the evolving demands of advanced chip manufacturing.

Sub-segments attracting the most capital include those serving the semiconductor industry (driven by the insatiable demand for ultra-high-purity chemicals and advanced manufacturing) and the pharmaceutical/biotechnology sectors (fueled by the rapid growth in biologics, gene therapies, and personalized medicine). Investments are typically geared towards expanding cleanroom manufacturing capabilities, upgrading existing equipment for higher precision, and R&D into next-generation fluoropolymer materials that offer even lower extractables or improved environmental footprints. While venture funding for pure-play fluoropolymer bottle startups is rare, strategic investments by established players within the Specialty Polymers Market underscore the long-term confidence in this indispensable, high-performance niche.

Fluoropolymer Bottle Segmentation

-

1. Material Type

- 1.1. PTFE (Polytetrafluoroethylene)

- 1.2. PFA (Perfluoroalkoxy)

- 1.3. FEP (Fluorinated Ethylene Propylene)

- 1.4. ETFE (Ethylene Tetrafluoroethylene)

- 1.5. PVDF (Polyvinylidene Fluoride)

- 1.6. PCTFE (Polychlorotrifluoroethylene)

- 1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

-

2. Size

- 2.1. 100 ml

- 2.2. 250 ml

- 2.3. 500 ml

- 2.4. 1L

- 2.5. 2L

- 2.6. Others

-

3. End User Industry

- 3.1. Chemical Industry

- 3.2. Pharmaceutical Industry

- 3.3. Biotechnology Companies

- 3.4. Research & Academic Laboratories

- 3.5. Others

-

4. Distribution Channel

- 4.1. Direct Sales

- 4.2. Distributors & Wholesalers

- 4.3. Online

Fluoropolymer Bottle Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fluoropolymer Bottle Regional Market Share

Geographic Coverage of Fluoropolymer Bottle

Fluoropolymer Bottle REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. PTFE (Polytetrafluoroethylene)

- 5.1.2. PFA (Perfluoroalkoxy)

- 5.1.3. FEP (Fluorinated Ethylene Propylene)

- 5.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 5.1.5. PVDF (Polyvinylidene Fluoride)

- 5.1.6. PCTFE (Polychlorotrifluoroethylene)

- 5.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 5.2. Market Analysis, Insights and Forecast - by Size

- 5.2.1. 100 ml

- 5.2.2. 250 ml

- 5.2.3. 500 ml

- 5.2.4. 1L

- 5.2.5. 2L

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by End User Industry

- 5.3.1. Chemical Industry

- 5.3.2. Pharmaceutical Industry

- 5.3.3. Biotechnology Companies

- 5.3.4. Research & Academic Laboratories

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.4.1. Direct Sales

- 5.4.2. Distributors & Wholesalers

- 5.4.3. Online

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. South America

- 5.5.3. Europe

- 5.5.4. Middle East & Africa

- 5.5.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Global Fluoropolymer Bottle Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. PTFE (Polytetrafluoroethylene)

- 6.1.2. PFA (Perfluoroalkoxy)

- 6.1.3. FEP (Fluorinated Ethylene Propylene)

- 6.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 6.1.5. PVDF (Polyvinylidene Fluoride)

- 6.1.6. PCTFE (Polychlorotrifluoroethylene)

- 6.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 6.2. Market Analysis, Insights and Forecast - by Size

- 6.2.1. 100 ml

- 6.2.2. 250 ml

- 6.2.3. 500 ml

- 6.2.4. 1L

- 6.2.5. 2L

- 6.2.6. Others

- 6.3. Market Analysis, Insights and Forecast - by End User Industry

- 6.3.1. Chemical Industry

- 6.3.2. Pharmaceutical Industry

- 6.3.3. Biotechnology Companies

- 6.3.4. Research & Academic Laboratories

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.4.1. Direct Sales

- 6.4.2. Distributors & Wholesalers

- 6.4.3. Online

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. North America Fluoropolymer Bottle Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. PTFE (Polytetrafluoroethylene)

- 7.1.2. PFA (Perfluoroalkoxy)

- 7.1.3. FEP (Fluorinated Ethylene Propylene)

- 7.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 7.1.5. PVDF (Polyvinylidene Fluoride)

- 7.1.6. PCTFE (Polychlorotrifluoroethylene)

- 7.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 7.2. Market Analysis, Insights and Forecast - by Size

- 7.2.1. 100 ml

- 7.2.2. 250 ml

- 7.2.3. 500 ml

- 7.2.4. 1L

- 7.2.5. 2L

- 7.2.6. Others

- 7.3. Market Analysis, Insights and Forecast - by End User Industry

- 7.3.1. Chemical Industry

- 7.3.2. Pharmaceutical Industry

- 7.3.3. Biotechnology Companies

- 7.3.4. Research & Academic Laboratories

- 7.3.5. Others

- 7.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.4.1. Direct Sales

- 7.4.2. Distributors & Wholesalers

- 7.4.3. Online

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. South America Fluoropolymer Bottle Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. PTFE (Polytetrafluoroethylene)

- 8.1.2. PFA (Perfluoroalkoxy)

- 8.1.3. FEP (Fluorinated Ethylene Propylene)

- 8.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 8.1.5. PVDF (Polyvinylidene Fluoride)

- 8.1.6. PCTFE (Polychlorotrifluoroethylene)

- 8.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 8.2. Market Analysis, Insights and Forecast - by Size

- 8.2.1. 100 ml

- 8.2.2. 250 ml

- 8.2.3. 500 ml

- 8.2.4. 1L

- 8.2.5. 2L

- 8.2.6. Others

- 8.3. Market Analysis, Insights and Forecast - by End User Industry

- 8.3.1. Chemical Industry

- 8.3.2. Pharmaceutical Industry

- 8.3.3. Biotechnology Companies

- 8.3.4. Research & Academic Laboratories

- 8.3.5. Others

- 8.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.4.1. Direct Sales

- 8.4.2. Distributors & Wholesalers

- 8.4.3. Online

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Europe Fluoropolymer Bottle Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. PTFE (Polytetrafluoroethylene)

- 9.1.2. PFA (Perfluoroalkoxy)

- 9.1.3. FEP (Fluorinated Ethylene Propylene)

- 9.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 9.1.5. PVDF (Polyvinylidene Fluoride)

- 9.1.6. PCTFE (Polychlorotrifluoroethylene)

- 9.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 9.2. Market Analysis, Insights and Forecast - by Size

- 9.2.1. 100 ml

- 9.2.2. 250 ml

- 9.2.3. 500 ml

- 9.2.4. 1L

- 9.2.5. 2L

- 9.2.6. Others

- 9.3. Market Analysis, Insights and Forecast - by End User Industry

- 9.3.1. Chemical Industry

- 9.3.2. Pharmaceutical Industry

- 9.3.3. Biotechnology Companies

- 9.3.4. Research & Academic Laboratories

- 9.3.5. Others

- 9.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.4.1. Direct Sales

- 9.4.2. Distributors & Wholesalers

- 9.4.3. Online

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. Middle East & Africa Fluoropolymer Bottle Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 10.1.1. PTFE (Polytetrafluoroethylene)

- 10.1.2. PFA (Perfluoroalkoxy)

- 10.1.3. FEP (Fluorinated Ethylene Propylene)

- 10.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 10.1.5. PVDF (Polyvinylidene Fluoride)

- 10.1.6. PCTFE (Polychlorotrifluoroethylene)

- 10.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 10.2. Market Analysis, Insights and Forecast - by Size

- 10.2.1. 100 ml

- 10.2.2. 250 ml

- 10.2.3. 500 ml

- 10.2.4. 1L

- 10.2.5. 2L

- 10.2.6. Others

- 10.3. Market Analysis, Insights and Forecast - by End User Industry

- 10.3.1. Chemical Industry

- 10.3.2. Pharmaceutical Industry

- 10.3.3. Biotechnology Companies

- 10.3.4. Research & Academic Laboratories

- 10.3.5. Others

- 10.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.4.1. Direct Sales

- 10.4.2. Distributors & Wholesalers

- 10.4.3. Online

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 11. Asia Pacific Fluoropolymer Bottle Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 11.1.1. PTFE (Polytetrafluoroethylene)

- 11.1.2. PFA (Perfluoroalkoxy)

- 11.1.3. FEP (Fluorinated Ethylene Propylene)

- 11.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 11.1.5. PVDF (Polyvinylidene Fluoride)

- 11.1.6. PCTFE (Polychlorotrifluoroethylene)

- 11.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 11.2. Market Analysis, Insights and Forecast - by Size

- 11.2.1. 100 ml

- 11.2.2. 250 ml

- 11.2.3. 500 ml

- 11.2.4. 1L

- 11.2.5. 2L

- 11.2.6. Others

- 11.3. Market Analysis, Insights and Forecast - by End User Industry

- 11.3.1. Chemical Industry

- 11.3.2. Pharmaceutical Industry

- 11.3.3. Biotechnology Companies

- 11.3.4. Research & Academic Laboratories

- 11.3.5. Others

- 11.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.4.1. Direct Sales

- 11.4.2. Distributors & Wholesalers

- 11.4.3. Online

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Savillex Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Saint-Gobain Performance Plastics

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Thermo Fisher Scientific

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DWK Life Sciences

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Nalgene (Thermo Fisher Scientific)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 AMETEK Fluoropolymer Products

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Entegris Inc.

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 NICHIAS Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Zeus Industrial Products Inc.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Fluorotherm Polymers Inc.

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Chang Zhou Feng Di Plastic Technology

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 AGC Chemicals Americas

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Daikin Industries Ltd.

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Others

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Savillex Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Fluoropolymer Bottle Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Fluoropolymer Bottle Revenue (billion), by Material Type 2025 & 2033

- Figure 3: North America Fluoropolymer Bottle Revenue Share (%), by Material Type 2025 & 2033

- Figure 4: North America Fluoropolymer Bottle Revenue (billion), by Size 2025 & 2033

- Figure 5: North America Fluoropolymer Bottle Revenue Share (%), by Size 2025 & 2033

- Figure 6: North America Fluoropolymer Bottle Revenue (billion), by End User Industry 2025 & 2033

- Figure 7: North America Fluoropolymer Bottle Revenue Share (%), by End User Industry 2025 & 2033

- Figure 8: North America Fluoropolymer Bottle Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 9: North America Fluoropolymer Bottle Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 10: North America Fluoropolymer Bottle Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Fluoropolymer Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 12: South America Fluoropolymer Bottle Revenue (billion), by Material Type 2025 & 2033

- Figure 13: South America Fluoropolymer Bottle Revenue Share (%), by Material Type 2025 & 2033

- Figure 14: South America Fluoropolymer Bottle Revenue (billion), by Size 2025 & 2033

- Figure 15: South America Fluoropolymer Bottle Revenue Share (%), by Size 2025 & 2033

- Figure 16: South America Fluoropolymer Bottle Revenue (billion), by End User Industry 2025 & 2033

- Figure 17: South America Fluoropolymer Bottle Revenue Share (%), by End User Industry 2025 & 2033

- Figure 18: South America Fluoropolymer Bottle Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 19: South America Fluoropolymer Bottle Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 20: South America Fluoropolymer Bottle Revenue (billion), by Country 2025 & 2033

- Figure 21: South America Fluoropolymer Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 22: Europe Fluoropolymer Bottle Revenue (billion), by Material Type 2025 & 2033

- Figure 23: Europe Fluoropolymer Bottle Revenue Share (%), by Material Type 2025 & 2033

- Figure 24: Europe Fluoropolymer Bottle Revenue (billion), by Size 2025 & 2033

- Figure 25: Europe Fluoropolymer Bottle Revenue Share (%), by Size 2025 & 2033

- Figure 26: Europe Fluoropolymer Bottle Revenue (billion), by End User Industry 2025 & 2033

- Figure 27: Europe Fluoropolymer Bottle Revenue Share (%), by End User Industry 2025 & 2033

- Figure 28: Europe Fluoropolymer Bottle Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 29: Europe Fluoropolymer Bottle Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Europe Fluoropolymer Bottle Revenue (billion), by Country 2025 & 2033

- Figure 31: Europe Fluoropolymer Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East & Africa Fluoropolymer Bottle Revenue (billion), by Material Type 2025 & 2033

- Figure 33: Middle East & Africa Fluoropolymer Bottle Revenue Share (%), by Material Type 2025 & 2033

- Figure 34: Middle East & Africa Fluoropolymer Bottle Revenue (billion), by Size 2025 & 2033

- Figure 35: Middle East & Africa Fluoropolymer Bottle Revenue Share (%), by Size 2025 & 2033

- Figure 36: Middle East & Africa Fluoropolymer Bottle Revenue (billion), by End User Industry 2025 & 2033

- Figure 37: Middle East & Africa Fluoropolymer Bottle Revenue Share (%), by End User Industry 2025 & 2033

- Figure 38: Middle East & Africa Fluoropolymer Bottle Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 39: Middle East & Africa Fluoropolymer Bottle Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 40: Middle East & Africa Fluoropolymer Bottle Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East & Africa Fluoropolymer Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 42: Asia Pacific Fluoropolymer Bottle Revenue (billion), by Material Type 2025 & 2033

- Figure 43: Asia Pacific Fluoropolymer Bottle Revenue Share (%), by Material Type 2025 & 2033

- Figure 44: Asia Pacific Fluoropolymer Bottle Revenue (billion), by Size 2025 & 2033

- Figure 45: Asia Pacific Fluoropolymer Bottle Revenue Share (%), by Size 2025 & 2033

- Figure 46: Asia Pacific Fluoropolymer Bottle Revenue (billion), by End User Industry 2025 & 2033

- Figure 47: Asia Pacific Fluoropolymer Bottle Revenue Share (%), by End User Industry 2025 & 2033

- Figure 48: Asia Pacific Fluoropolymer Bottle Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 49: Asia Pacific Fluoropolymer Bottle Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 50: Asia Pacific Fluoropolymer Bottle Revenue (billion), by Country 2025 & 2033

- Figure 51: Asia Pacific Fluoropolymer Bottle Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fluoropolymer Bottle Revenue billion Forecast, by Material Type 2020 & 2033

- Table 2: Global Fluoropolymer Bottle Revenue billion Forecast, by Size 2020 & 2033

- Table 3: Global Fluoropolymer Bottle Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 4: Global Fluoropolymer Bottle Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 5: Global Fluoropolymer Bottle Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Fluoropolymer Bottle Revenue billion Forecast, by Material Type 2020 & 2033

- Table 7: Global Fluoropolymer Bottle Revenue billion Forecast, by Size 2020 & 2033

- Table 8: Global Fluoropolymer Bottle Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 9: Global Fluoropolymer Bottle Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 10: Global Fluoropolymer Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Global Fluoropolymer Bottle Revenue billion Forecast, by Material Type 2020 & 2033

- Table 15: Global Fluoropolymer Bottle Revenue billion Forecast, by Size 2020 & 2033

- Table 16: Global Fluoropolymer Bottle Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 17: Global Fluoropolymer Bottle Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 18: Global Fluoropolymer Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Brazil Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Argentina Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of South America Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Fluoropolymer Bottle Revenue billion Forecast, by Material Type 2020 & 2033

- Table 23: Global Fluoropolymer Bottle Revenue billion Forecast, by Size 2020 & 2033

- Table 24: Global Fluoropolymer Bottle Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 25: Global Fluoropolymer Bottle Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 26: Global Fluoropolymer Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 27: United Kingdom Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Germany Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: France Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Italy Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Spain Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Russia Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Benelux Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Nordics Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Global Fluoropolymer Bottle Revenue billion Forecast, by Material Type 2020 & 2033

- Table 37: Global Fluoropolymer Bottle Revenue billion Forecast, by Size 2020 & 2033

- Table 38: Global Fluoropolymer Bottle Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 39: Global Fluoropolymer Bottle Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 40: Global Fluoropolymer Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 41: Turkey Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Israel Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: GCC Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: North Africa Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: South Africa Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Middle East & Africa Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Global Fluoropolymer Bottle Revenue billion Forecast, by Material Type 2020 & 2033

- Table 48: Global Fluoropolymer Bottle Revenue billion Forecast, by Size 2020 & 2033

- Table 49: Global Fluoropolymer Bottle Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 50: Global Fluoropolymer Bottle Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 51: Global Fluoropolymer Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 52: China Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 53: India Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 55: South Korea Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: ASEAN Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 57: Oceania Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Rest of Asia Pacific Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fluoropolymer Bottle?

The projected CAGR is approximately 6.9%.

2. Which companies are prominent players in the Fluoropolymer Bottle?

Key companies in the market include Savillex Corporation, Saint-Gobain Performance Plastics, Thermo Fisher Scientific, DWK Life Sciences, Nalgene (Thermo Fisher Scientific), AMETEK Fluoropolymer Products, Entegris, Inc., NICHIAS Corporation, Zeus Industrial Products, Inc., Fluorotherm Polymers, Inc., Chang Zhou Feng Di Plastic Technology, AGC Chemicals Americas, Daikin Industries Ltd., Others.

3. What are the main segments of the Fluoropolymer Bottle?

The market segments include Material Type, Size, End User Industry, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.8 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fluoropolymer Bottle," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fluoropolymer Bottle report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fluoropolymer Bottle?

To stay informed about further developments, trends, and reports in the Fluoropolymer Bottle, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence