Key Insights

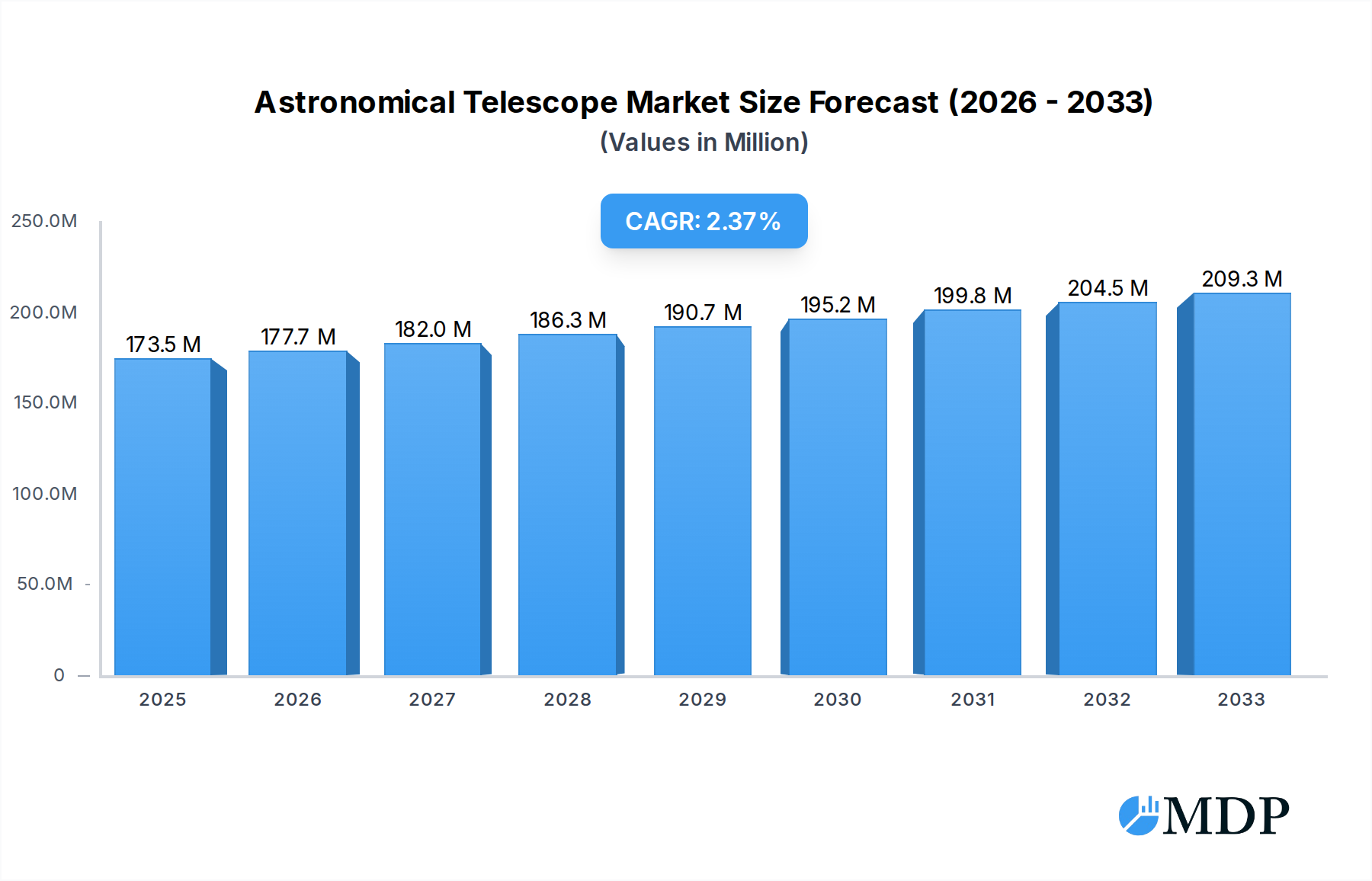

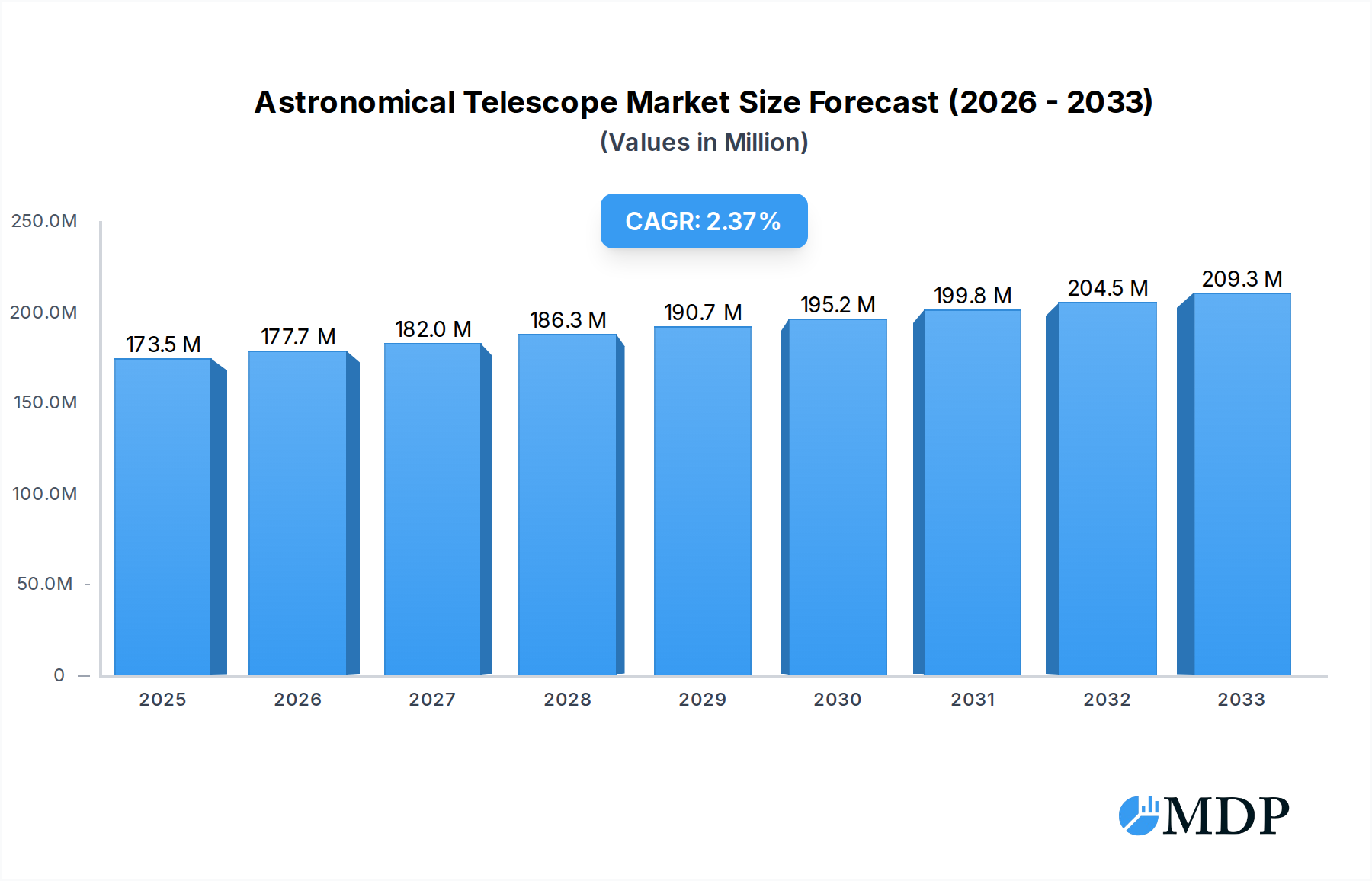

The global astronomical telescope market is poised for steady expansion, projected to reach $173.5 million in 2025. This growth is underpinned by a CAGR of 2.5% from 2025 to 2033, indicating a mature yet consistent upward trajectory. The market is propelled by a rising interest in astronomy among the general public, educational institutions seeking to enhance STEM learning, and scientific research bodies pushing the boundaries of cosmic discovery. The increasing affordability and sophistication of personal telescopes are democratizing stargazing, while advancements in optical technology are enabling more detailed observations for professional and amateur astronomers alike. Furthermore, a growing awareness of space exploration initiatives and the desire to understand our universe are contributing to this sustained demand for astronomical instruments.

Astronomical Telescope Market Size (In Million)

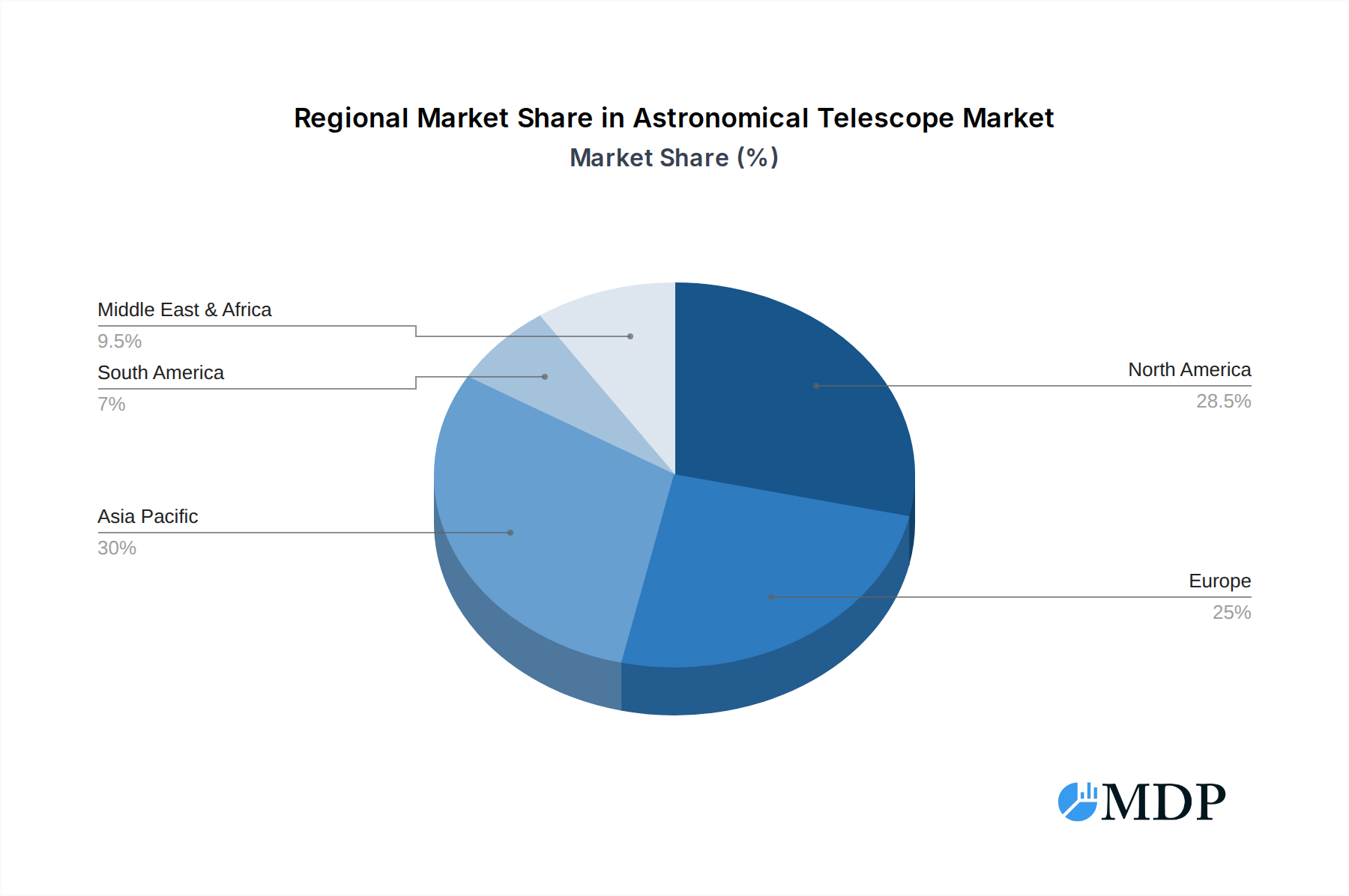

The market's segmentation reveals key areas of focus and opportunity. The "Personal" application segment is expected to remain a dominant force, driven by hobbyists and educational purposes, while "Educational Institutions" and "Scientific Research Institutions" represent significant growth avenues due to their continuous need for advanced observational tools. In terms of telescope types, the market is diverse, with Refracting, Reflector, and Catadioptric telescopes each catering to different user needs and observational goals. The competitive landscape features established players like Synta Technology (Celestron), JOC, and Takahashi, alongside emerging brands, fostering innovation and product development. Geographically, North America and Asia Pacific are anticipated to lead the market due to strong research infrastructure and a growing enthusiast base, respectively.

Astronomical Telescope Company Market Share

This in-depth report offers a definitive analysis of the global astronomical telescope market, projecting its trajectory from 2019 to 2033. With a base year of 2025 and a forecast period of 2025-2033, this study delves into market dynamics, key trends, leading players, and future opportunities within this captivating industry. We provide actionable insights for investors, manufacturers, and researchers seeking to understand and capitalize on the expanding universe of amateur and professional astronomy. The report leverages a wealth of data to illuminate market concentration, innovation drivers, regulatory landscapes, and emerging consumer preferences, equipping stakeholders with a competitive edge.

Astronomical Telescope Market Dynamics & Concentration

The astronomical telescope market exhibits a moderate concentration, with key players holding significant market share, yet ample room for niche innovation and new entrants. Synta Technology (Celestron) and JOC are prominent leaders, followed by Takahashi, Bosma, and Vixen Co. The market's dynamism is driven by continuous technological advancements, particularly in optics and digital integration, catering to a growing enthusiast base and increasing demand from educational and scientific institutions. Regulatory frameworks, while generally permissive, can influence manufacturing standards and import/export processes for specialized components. Product substitutes, such as astrophotography equipment with integrated imaging capabilities, present a growing consideration, although dedicated astronomical telescopes remain the primary tool for direct observation. End-user trends point towards a rising interest in accessible, user-friendly telescopes for personal use, alongside sophisticated instruments for scientific research. Merger and acquisition (M&A) activities, while not yet at an extreme level, are anticipated to increase as larger companies seek to consolidate their offerings and acquire innovative technologies. We project approximately five to eight significant M&A deals within the forecast period, indicating strategic consolidation.

Astronomical Telescope Industry Trends & Analysis

The astronomical telescope industry is poised for substantial growth, driven by a confluence of technological innovation, increasing public interest in space exploration, and a growing demand from educational and research sectors. The Compound Annual Growth Rate (CAGR) is estimated at 7.5% for the forecast period 2025–2033. This robust expansion is fueled by advancements in lens coatings, mirror technology, and the integration of digital components such as Go-To mount systems, Wi-Fi connectivity, and astrophotography capabilities. Consumer preferences are evolving, with a notable shift towards portable, lightweight, and user-friendly telescopes for amateur astronomers, alongside a persistent demand for high-aperture, high-resolution instruments for serious stargazing and scientific research. The penetration of smart telescopes, which offer automated alignment and guided tours of celestial objects, is rapidly increasing, making astronomy more accessible to a broader audience. Competitive dynamics are characterized by intense innovation from established players like Synta Technology (Celestron), Takahashi, and Nikon, alongside the emergence of specialized manufacturers like SharpStar and TianLang focusing on advanced astrophotography telescopes. The market penetration of advanced optical designs, such as apochromatic refractors and Ritchey-Chrétien reflectors, is growing within the professional and advanced amateur segments.

Leading Markets & Segments in Astronomical Telescope

The Personal application segment currently dominates the astronomical telescope market, driven by a burgeoning interest in amateur astronomy worldwide. This segment is characterized by strong demand in North America and Europe, with rapidly growing markets in Asia-Pacific, particularly China and India. Key drivers for this dominance include increased disposable income, a growing emphasis on STEM education and hobbyist activities, and the availability of a wider range of affordable yet capable telescopes.

Within the Types segment, Reflector Telescopes continue to hold a significant market share due to their cost-effectiveness and ability to achieve larger apertures for their price point, making them popular among entry-level to intermediate users. However, Refracting Telescopes, particularly apochromatic designs, are gaining traction among discerning enthusiasts and astrophotographers for their superior chromatic aberration control and sharp, contrasty images. Catadioptric Telescopes, such as Schmidt-Cassegrains and Maksutov-Cassegrains, offer a balance of aperture, portability, and optical quality, making them a strong contender in the mid-to-high end market.

Educational Institutions represent a stable and growing segment, driven by government initiatives to promote science education and the increasing adoption of telescopes in school curricula for hands-on learning experiences. Scientific Research Institutions, while a smaller segment in terms of unit volume, contribute significantly to market value with their demand for ultra-high-precision and specialized telescopes. The economic policies supporting scientific research and development, coupled with infrastructure development in observatories, are crucial for the growth of this segment.

Astronomical Telescope Product Developments

Product development in the astronomical telescope market is intensely focused on enhancing user experience and optical performance. Innovations include the integration of sophisticated digital electronics for automated tracking and imaging, lightweight yet robust materials for portability, and advanced optical coatings to minimize light loss and maximize contrast. Smart telescopes with built-in Wi-Fi and app connectivity are transforming the hobby by simplifying celestial object identification and astrophotography. Competitive advantages are being built on ease of use, portability, superior image quality, and advanced imaging capabilities, catering to both novice stargazers and seasoned astrophotographers.

Key Drivers of Astronomical Telescope Growth

Several key factors are propelling the astronomical telescope market forward. Technologically, advancements in optics, such as improved mirror and lens manufacturing, and the miniaturization of digital components are making telescopes more powerful and accessible. Economically, rising disposable incomes and a growing global middle class are fueling discretionary spending on hobbies like astronomy. Furthermore, increasing government and institutional investment in space exploration and STEM education directly translates to higher demand for astronomical instruments. The widespread availability of online astronomical communities and educational resources also plays a crucial role in fostering interest and driving sales.

Challenges in the Astronomical Telescope Market

Despite robust growth, the astronomical telescope market faces several challenges. Regulatory hurdles, particularly concerning the import/export of advanced optical components and potential tariffs, can impact supply chains and manufacturing costs. Supply chain disruptions, exacerbated by global events, can lead to extended lead times and increased prices. Intense competition among manufacturers, especially in the entry-level segment, can put pressure on profit margins. The high cost of sophisticated, high-aperture research-grade telescopes can also limit accessibility for some institutional buyers. Quantifiable impacts include potential delays in product launches and a 10-15% increase in production costs due to supply chain volatility.

Emerging Opportunities in Astronomical Telescope

Emerging opportunities in the astronomical telescope market are primarily driven by technological breakthroughs and strategic market expansion. The continued miniaturization and cost reduction of high-resolution imaging sensors present a significant opportunity for advanced astrophotography telescopes at more accessible price points. Strategic partnerships between telescope manufacturers and astrophotography software developers can create integrated solutions that attract new users. Furthermore, expanding into emerging economies with growing interest in science and technology, such as Southeast Asia and Latin America, offers substantial untapped market potential.

Leading Players in the Astronomical Telescope Sector

- Synta Technology (Celestron)

- JOC

- Takahashi

- Bosma

- Vixen Co

- SharpStar

- Vista Outdoor (Tasco)

- Astro-Physics

- Nikon

- Visionking

- TianLang

Key Milestones in Astronomical Telescope Industry

- 2019: Increased adoption of smartphone integration for telescope control and astrophotography.

- 2020: Growth in demand for compact and portable telescopes driven by outdoor recreation trends.

- 2021: Introduction of advanced AI-powered object recognition in smart telescopes.

- 2022: Focus on sustainable manufacturing practices and materials in telescope production.

- 2023: Significant advancements in mirror coating technology for enhanced reflectivity and durability.

- 2024: Rise of integrated astrophotography solutions combining telescopes, cameras, and software.

- 2025 (Projected): Increased market penetration of ultra-high-resolution digital sensors in consumer telescopes.

- 2026 (Projected): Potential for new market entrants with disruptive optical designs.

- 2027 (Projected): Consolidation through strategic M&A activities by major players.

- 2028-2033 (Projected): Continued integration of augmented reality for enhanced astronomical viewing experiences.

Strategic Outlook for Astronomical Telescope Market

The strategic outlook for the astronomical telescope market remains exceptionally bright, characterized by consistent growth and innovation. Key growth accelerators include the ongoing democratization of space exploration through advanced, user-friendly technology, and the increasing integration of digital and smart features. Manufacturers should focus on developing intuitive interfaces, portable designs, and robust astrophotography capabilities to capture the expanding amateur astronomy market. Strategic partnerships with educational institutions and research bodies will solidify market presence and foster long-term demand. The market is poised for sustained expansion, driven by a global fascination with the cosmos and continuous technological evolution.

Astronomical Telescope Segmentation

-

1. Application

- 1.1. Personal

- 1.2. Educational Institution

- 1.3. Scientific Research Institutions

-

2. Types

- 2.1. Refracting Telescope

- 2.2. Reflector Telescope

- 2.3. Catadioptric Telescope

Astronomical Telescope Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Astronomical Telescope Regional Market Share

Geographic Coverage of Astronomical Telescope

Astronomical Telescope REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Astronomical Telescope Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Personal

- 5.1.2. Educational Institution

- 5.1.3. Scientific Research Institutions

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Refracting Telescope

- 5.2.2. Reflector Telescope

- 5.2.3. Catadioptric Telescope

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Astronomical Telescope Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Personal

- 6.1.2. Educational Institution

- 6.1.3. Scientific Research Institutions

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Refracting Telescope

- 6.2.2. Reflector Telescope

- 6.2.3. Catadioptric Telescope

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Astronomical Telescope Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Personal

- 7.1.2. Educational Institution

- 7.1.3. Scientific Research Institutions

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Refracting Telescope

- 7.2.2. Reflector Telescope

- 7.2.3. Catadioptric Telescope

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Astronomical Telescope Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Personal

- 8.1.2. Educational Institution

- 8.1.3. Scientific Research Institutions

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Refracting Telescope

- 8.2.2. Reflector Telescope

- 8.2.3. Catadioptric Telescope

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Astronomical Telescope Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Personal

- 9.1.2. Educational Institution

- 9.1.3. Scientific Research Institutions

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Refracting Telescope

- 9.2.2. Reflector Telescope

- 9.2.3. Catadioptric Telescope

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Astronomical Telescope Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Personal

- 10.1.2. Educational Institution

- 10.1.3. Scientific Research Institutions

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Refracting Telescope

- 10.2.2. Reflector Telescope

- 10.2.3. Catadioptric Telescope

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Synta Technology (Celestron)

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 JOC

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Takahashi

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Bosma

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Vixen Co

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 SharpStar

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Vista Outdoor (Tasco)

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Astro-Physics

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Nikon

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Visionking

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 TianLang

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Synta Technology (Celestron)

List of Figures

- Figure 1: Global Astronomical Telescope Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Astronomical Telescope Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Astronomical Telescope Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Astronomical Telescope Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Astronomical Telescope Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Astronomical Telescope Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Astronomical Telescope Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Astronomical Telescope Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Astronomical Telescope Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Astronomical Telescope Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Astronomical Telescope Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Astronomical Telescope Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Astronomical Telescope Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Astronomical Telescope Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Astronomical Telescope Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Astronomical Telescope Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Astronomical Telescope Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Astronomical Telescope Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Astronomical Telescope Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Astronomical Telescope Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Astronomical Telescope Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Astronomical Telescope Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Astronomical Telescope Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Astronomical Telescope Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Astronomical Telescope Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Astronomical Telescope Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Astronomical Telescope Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Astronomical Telescope Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Astronomical Telescope Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Astronomical Telescope Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Astronomical Telescope Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Astronomical Telescope Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Astronomical Telescope Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Astronomical Telescope Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Astronomical Telescope Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Astronomical Telescope Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Astronomical Telescope Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Astronomical Telescope Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Astronomical Telescope Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Astronomical Telescope Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Astronomical Telescope Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Astronomical Telescope Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Astronomical Telescope Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Astronomical Telescope Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Astronomical Telescope Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Astronomical Telescope Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Astronomical Telescope Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Astronomical Telescope Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Astronomical Telescope Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Astronomical Telescope Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Astronomical Telescope?

The projected CAGR is approximately 2.5%.

2. Which companies are prominent players in the Astronomical Telescope?

Key companies in the market include Synta Technology (Celestron), JOC, Takahashi, Bosma, Vixen Co, SharpStar, Vista Outdoor (Tasco), Astro-Physics, Nikon, Visionking, TianLang.

3. What are the main segments of the Astronomical Telescope?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Astronomical Telescope," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Astronomical Telescope report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Astronomical Telescope?

To stay informed about further developments, trends, and reports in the Astronomical Telescope, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence