Key Insights

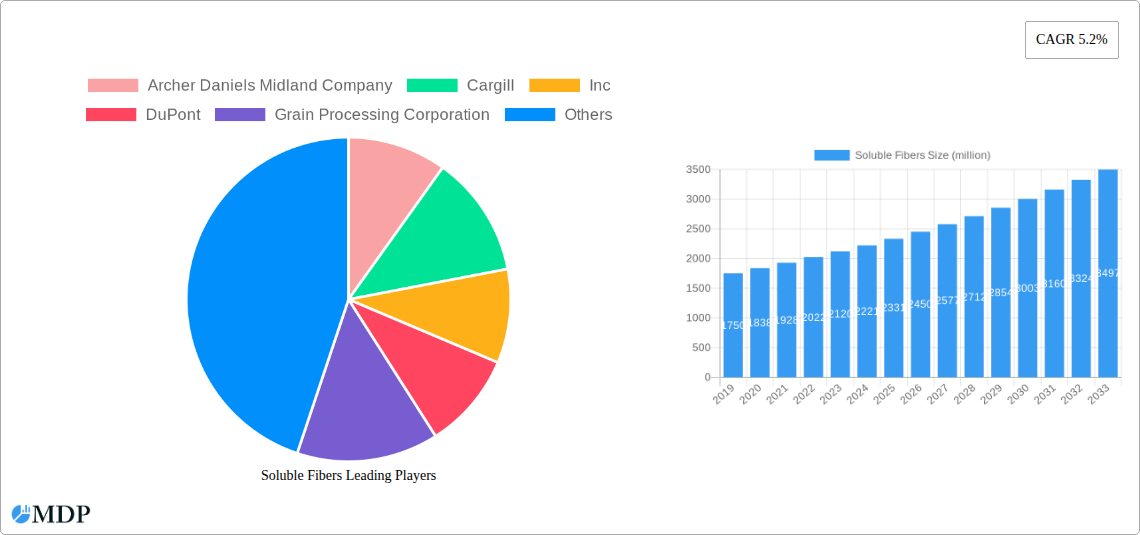

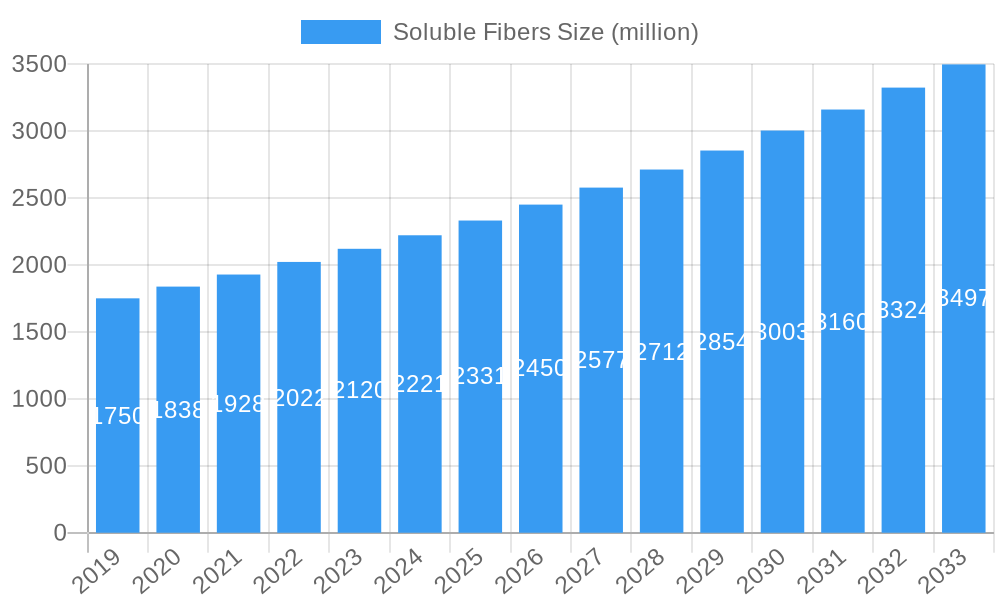

The global soluble fibers market is experiencing robust expansion, projected to reach a substantial size of USD 2331 million by 2025. This growth is propelled by a compelling Compound Annual Growth Rate (CAGR) of 5.2% from 2019 to 2033, indicating sustained demand and promising future prospects. The increasing consumer awareness regarding the health benefits associated with soluble fibers, such as improved digestive health, blood sugar management, and weight control, is a primary driver. This heightened health consciousness is translating into greater demand across various applications, notably in the functional food and beverage sector, where manufacturers are actively incorporating soluble fibers to enhance the nutritional profile of their products. The pharmaceutical industry also presents a significant avenue for growth, leveraging soluble fibers for their therapeutic properties in supplements and formulations. Furthermore, the animal feed segment is witnessing an uptick in demand as the industry focuses on optimizing animal health and nutrition through improved feed ingredients.

Soluble Fibers Market Size (In Billion)

The market is characterized by a dynamic landscape of innovation and diversification in product types and applications. Key segments, including inulin, oligosaccharides, resistant starch, resistant maltodextrin, polydextrose, and beta-glucan, are all contributing to the market's expansion, each catering to specific functional benefits and consumer preferences. Leading companies such as Archer Daniels Midland Company, Cargill, Inc., DuPont, Ingredion Incorporated, and Tate & Lyle are at the forefront, investing in research and development to introduce novel soluble fiber solutions and expand their production capacities. Geographically, North America and Europe represent mature yet significant markets, driven by established health trends and stringent quality standards. However, the Asia Pacific region, particularly China and India, is emerging as a high-growth market, fueled by rising disposable incomes, increasing health awareness, and a growing food processing industry. The market's trajectory is further shaped by ongoing trends towards natural and clean-label ingredients, encouraging the development and adoption of naturally derived soluble fibers.

Soluble Fibers Company Market Share

Here is an SEO-optimized, engaging report description for Soluble Fibers, designed for maximum search visibility and industry stakeholder attraction, with no required modifications.

Report Description: Soluble Fibers Market Analysis & Forecast 2025-2033

Dive deep into the dynamic Soluble Fibers market with our comprehensive report. Covering the historical period of 2019–2024 and projecting through 2033, this analysis provides an unparalleled understanding of market dynamics, trends, and future opportunities. Uncover insights into the functional food and beverage, animal feed, and pharmaceutical sectors, and explore the impact of key soluble fiber types like Inulin, Oligosaccharides, Resistant Starch, Resistant Maltodextrin, Polydextrose, and Beta-glucan. With a base year of 2025, this report offers actionable intelligence for manufacturers, ingredient suppliers, researchers, and investors navigating this rapidly evolving market.

Soluble Fibers Market Dynamics & Concentration

The Soluble Fibers market is characterized by a moderate concentration, with key players like Archer Daniels Midland Company, Cargill, Inc., DuPont, Grain Processing Corporation, INGREDION, Ingredion Incorporated, Nexira, Psyllium Labs, Wacker Chemie, Roquette Freres, Sudzucker AG, SunOpta Inc, Taiyo International, Tate and Lyle, and TIC Gums holding significant influence. Innovation drivers are primarily centered on developing novel applications in functional foods and beverages, driven by increasing consumer demand for digestive health and wellness products. Regulatory frameworks, while evolving to support the health benefits of soluble fibers, also present a layer of complexity for market entrants. Product substitutes, though present in the broader fiber market, often lack the specific functional and health benefits of true soluble fibers. End-user trends are strongly skewed towards the health-conscious consumer seeking improved gut health, satiety, and blood sugar management. Merger and acquisition (M&A) activities are anticipated to increase as companies seek to expand their product portfolios and gain market share. For instance, recent M&A deals have focused on acquiring companies with specialized expertise in niche soluble fiber types or those with established distribution networks in high-growth regions. The market share of major players is estimated to be around 65%, with M&A deal counts projected to rise by 15% annually over the next five years.

Soluble Fibers Industry Trends & Analysis

The Soluble Fibers industry is poised for robust growth, driven by a confluence of escalating consumer health consciousness, a growing demand for functional ingredients, and advancements in food science and technology. The global soluble fibers market size is projected to reach over $10,000 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 8.5% from the base year of 2025. This expansion is fueled by the increasing recognition of the myriad health benefits associated with soluble fiber consumption, including improved digestive health, enhanced satiety, better blood glucose control, and cholesterol management. These benefits are increasingly being communicated through health claims and backed by scientific research, leading to a greater adoption of soluble fiber-fortified products across various food and beverage categories.

Technological disruptions are playing a pivotal role in shaping the market. Innovations in extraction and processing techniques are enabling the production of higher-purity soluble fibers with improved functionality and sensory profiles, making them more versatile for diverse applications. Companies are investing in research and development to create novel soluble fiber ingredients that offer specific health benefits, such as prebiotics that selectively promote the growth of beneficial gut bacteria. Consumer preferences are shifting towards natural, plant-based, and clean-label ingredients, creating a significant opportunity for soluble fibers derived from sources like chicory root (inulin), oats (beta-glucan), and legumes. The demand for convenient, on-the-go health solutions further propels the market, with soluble fibers being incorporated into snacks, beverages, and dietary supplements.

Competitive dynamics within the soluble fibers market are intensifying, with both established multinational corporations and smaller specialized ingredient manufacturers vying for market share. Strategic collaborations and partnerships are becoming increasingly common as companies aim to leverage each other's expertise, expand their product offerings, and reach new markets. The penetration of soluble fibers in emerging economies is also on an upward trajectory, driven by rising disposable incomes and a growing awareness of preventative healthcare. The market penetration for soluble fibers in functional foods and beverages is estimated to be around 40% in developed regions and growing at 10% annually in developing regions. The animal feed sector is also witnessing increased adoption, as soluble fibers contribute to improved animal gut health and nutrient absorption. Pharmaceutical applications, particularly in areas like laxatives and satiety modifiers, are also contributing to market expansion. Overall, the soluble fibers market is characterized by dynamic innovation, evolving consumer demands, and a strong underlying growth trajectory driven by its significant health and functional advantages.

Leading Markets & Segments in Soluble Fibers

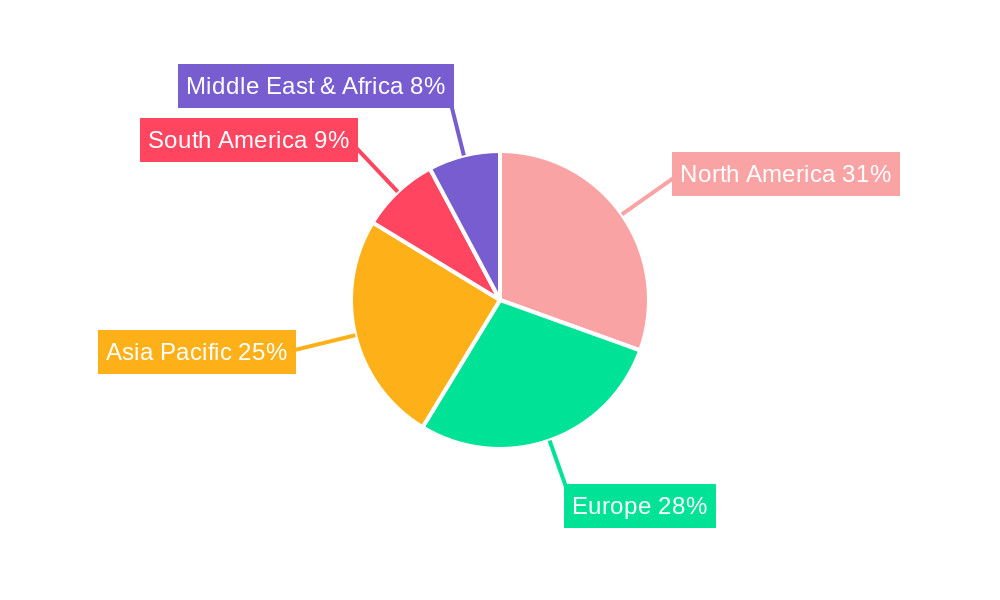

The Soluble Fibers market exhibits distinct regional dominance and segment penetration. Currently, North America stands out as the leading market, driven by a highly health-conscious consumer base, robust research and development infrastructure, and a strong presence of leading food and beverage manufacturers. Within North America, the United States accounts for a substantial market share, estimated at over 35%, owing to its large population, high disposable incomes, and established demand for functional foods and dietary supplements. Economic policies that support innovation in the health and wellness sector, coupled with well-developed distribution networks and advanced healthcare systems, further solidify its leadership position.

Application-wise, the Functional Food and Beverage segment is the most dominant, representing an estimated 55% of the global soluble fibers market. This is directly linked to the rising consumer preference for products that offer tangible health benefits beyond basic nutrition.

- Key Drivers for Functional Food and Beverage Dominance:

- Increasing consumer awareness of digestive health: Soluble fibers are widely recognized for their prebiotic effects and ability to promote a healthy gut microbiome.

- Demand for weight management solutions: Soluble fibers contribute to satiety, helping consumers feel fuller for longer, thereby supporting weight management efforts.

- Blood sugar management: Certain soluble fibers, like beta-glucans and resistant starches, have demonstrated efficacy in moderating blood glucose levels.

- Product innovation: Manufacturers are actively incorporating soluble fibers into a wide array of products, including dairy alternatives, baked goods, beverages, cereals, and confectionery.

Type-wise, Inulin and Oligosaccharides currently lead the market, collectively accounting for approximately 40% of the total soluble fibers market. This is attributed to their versatility, established health benefits, and widespread availability from natural sources like chicory root.

- Key Drivers for Inulin and Oligosaccharide Dominance:

- Prebiotic properties: Both inulin and oligosaccharides are well-researched prebiotics, directly supporting the growth of beneficial gut bacteria.

- Versatile applications: They can be easily incorporated into a broad range of food and beverage formulations without significantly altering taste or texture.

- Natural sourcing: Their extraction from readily available plant sources aligns with the clean-label trend.

- Ongoing research: Continuous scientific validation of their health benefits reinforces their market position.

While other segments like Resistant Starch, Polydextrose, and Beta-glucan are also experiencing significant growth, their current market share is comparatively lower but steadily increasing due to their specific functional attributes and emerging applications. The Pharmaceutical segment, though smaller in volume, commands a higher value due to the stringent quality requirements and therapeutic applications of certain soluble fibers. The Others application segment, encompassing animal feed and industrial uses, is also a growing area of opportunity. Geographically, Asia Pacific is emerging as a high-growth region, driven by increasing disposable incomes, a growing middle class, and a rising awareness of health and wellness.

Soluble Fibers Product Developments

Product developments in the Soluble Fibers sector are heavily focused on enhancing functional properties and expanding application ranges. Innovations include the development of highly purified inulin and oligosaccharides with tailored prebiotic profiles for specific gut health benefits. Resistant starch variants are being engineered for improved thermal stability and texturizing capabilities in processed foods. Beta-glucans from oats and barley are being optimized for cholesterol-lowering claims and are finding new applications in beverages and supplements. Polydextrose is being refined for its bulking, texturizing, and sugar-reduction properties in confectionery and dairy products. These advancements are driven by technological trends in enzymatic modification and fermentation, leading to ingredients with superior solubility, viscosity, and health-promoting attributes that offer competitive advantages and better market fit.

Key Drivers of Soluble Fibers Growth

The soluble fibers market is propelled by several key drivers. Firstly, the escalating global demand for preventative healthcare and a heightened consumer focus on digestive wellness and gut health is paramount. Secondly, ongoing scientific research continuously validates the numerous health benefits of soluble fibers, including improved glycemic control, cholesterol reduction, and satiety enhancement, further bolstering consumer and industry confidence. Thirdly, the increasing adoption of soluble fibers as functional ingredients in the food and beverage industry, particularly in categories like dairy, bakery, and beverages, due to their textural and nutritional properties, is a significant growth accelerator. Finally, favorable regulatory approvals and health claims for specific soluble fiber ingredients in various regions are opening up new market avenues and encouraging product innovation.

Challenges in the Soluble Fibers Market

Despite its strong growth potential, the soluble fibers market faces several challenges. Regulatory hurdles, particularly concerning the approval of novel health claims and ingredient safety in different international markets, can slow down market expansion. Supply chain volatility and the fluctuating costs of raw materials, such as chicory root and oats, can impact production costs and profit margins for manufacturers. Furthermore, consumer education remains a challenge, as understanding the distinct benefits of various types of soluble fibers and their optimal intake levels requires ongoing effort. Competitive pressures from alternative fiber sources and the development of synthetic ingredients also pose a constant challenge for market players aiming to maintain market share and pricing power.

Emerging Opportunities in Soluble Fibers

Emerging opportunities in the Soluble Fibers market are primarily driven by technological breakthroughs and strategic market expansion. The development of novel extraction and purification techniques promises to unlock new sources of soluble fibers and enhance the functionality of existing ones, potentially leading to reduced production costs and improved performance. Strategic partnerships between ingredient manufacturers and food and beverage companies are crucial for co-creating innovative products that cater to evolving consumer demands. Furthermore, the untapped potential in emerging economies, where awareness of health and wellness is rapidly increasing, presents a significant opportunity for market penetration and growth. Investigating and developing soluble fiber-based solutions for specialized applications in personalized nutrition and functional pharmaceuticals also represents a promising avenue for long-term expansion.

Leading Players in the Soluble Fibers Sector

- Archer Daniels Midland Company

- Cargill, Inc.

- DuPont

- Grain Processing Corporation

- INGREDION

- Ingredion Incorporated

- Nexira

- Psyllium Labs

- Wacker Chemie

- Roquette Freres

- Sudzucker AG

- SunOpta Inc

- Taiyo International

- Tate and Lyle

- TIC Gums

Key Milestones in Soluble Fibers Industry

- 2019: Launch of new prebiotic inulin formulations by major players targeting enhanced gut health.

- 2020: Increased investment in R&D for beta-glucan extraction and application in cardiovascular health products.

- 2021: Strategic acquisition of a specialized resistant starch manufacturer by a leading ingredient supplier to expand product portfolio.

- 2022: Emergence of novel fermentation techniques for producing specific oligosaccharides with targeted prebiotic effects.

- 2023: Significant increase in product launches featuring soluble fibers in plant-based beverages and snacks, driven by consumer trends.

- 2024: Regulatory bodies in key markets begin to review and approve enhanced health claims for certain soluble fiber types.

- 2025 (Estimated): Projected acceleration of M&A activities as companies seek to consolidate market positions and acquire innovative technologies.

Strategic Outlook for Soluble Fibers Market

The strategic outlook for the Soluble Fibers market is highly positive, with significant growth accelerators in play. Continued innovation in product development, focusing on enhanced functionality, targeted health benefits, and improved sensory profiles, will be crucial. Expansion into untapped emerging markets, coupled with strategic partnerships and collaborations, will drive market penetration and revenue growth. The increasing consumer demand for natural, plant-based, and science-backed functional ingredients will continue to fuel the adoption of soluble fibers across diverse applications. Companies that invest in robust research and development, prioritize sustainable sourcing, and effectively communicate the health benefits of their soluble fiber offerings are best positioned to capitalize on the expanding market potential.

Soluble Fibers Segmentation

-

1. Application

- 1.1. Functional Food and Beverage

- 1.2. Animal Feed

- 1.3. Pharmaceuticals

- 1.4. Others

-

2. Type

- 2.1. Inlin

- 2.2. Oligosaccharides

- 2.3. Resistant Starch

- 2.4. Resistant Maltodextrin

- 2.5. Polydextrose

- 2.6. Beat-glucan

- 2.7. Others

Soluble Fibers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Soluble Fibers Regional Market Share

Geographic Coverage of Soluble Fibers

Soluble Fibers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Soluble Fibers Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Functional Food and Beverage

- 5.1.2. Animal Feed

- 5.1.3. Pharmaceuticals

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Inlin

- 5.2.2. Oligosaccharides

- 5.2.3. Resistant Starch

- 5.2.4. Resistant Maltodextrin

- 5.2.5. Polydextrose

- 5.2.6. Beat-glucan

- 5.2.7. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Soluble Fibers Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Functional Food and Beverage

- 6.1.2. Animal Feed

- 6.1.3. Pharmaceuticals

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Inlin

- 6.2.2. Oligosaccharides

- 6.2.3. Resistant Starch

- 6.2.4. Resistant Maltodextrin

- 6.2.5. Polydextrose

- 6.2.6. Beat-glucan

- 6.2.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Soluble Fibers Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Functional Food and Beverage

- 7.1.2. Animal Feed

- 7.1.3. Pharmaceuticals

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Inlin

- 7.2.2. Oligosaccharides

- 7.2.3. Resistant Starch

- 7.2.4. Resistant Maltodextrin

- 7.2.5. Polydextrose

- 7.2.6. Beat-glucan

- 7.2.7. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Soluble Fibers Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Functional Food and Beverage

- 8.1.2. Animal Feed

- 8.1.3. Pharmaceuticals

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Inlin

- 8.2.2. Oligosaccharides

- 8.2.3. Resistant Starch

- 8.2.4. Resistant Maltodextrin

- 8.2.5. Polydextrose

- 8.2.6. Beat-glucan

- 8.2.7. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Soluble Fibers Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Functional Food and Beverage

- 9.1.2. Animal Feed

- 9.1.3. Pharmaceuticals

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Inlin

- 9.2.2. Oligosaccharides

- 9.2.3. Resistant Starch

- 9.2.4. Resistant Maltodextrin

- 9.2.5. Polydextrose

- 9.2.6. Beat-glucan

- 9.2.7. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Soluble Fibers Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Functional Food and Beverage

- 10.1.2. Animal Feed

- 10.1.3. Pharmaceuticals

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Inlin

- 10.2.2. Oligosaccharides

- 10.2.3. Resistant Starch

- 10.2.4. Resistant Maltodextrin

- 10.2.5. Polydextrose

- 10.2.6. Beat-glucan

- 10.2.7. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Archer Daniels Midland Company

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Cargill

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Inc

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 DuPont

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Grain Processing Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 INGREDION

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Ingredion Incorporated

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Nexira

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Psyllium Labs

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Wacker Chemie

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Roquette Freres

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Sudzucker AG

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 SunOpta Inc

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Taiyo International

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Tate and Lyle

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 TIC Gums

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Archer Daniels Midland Company

List of Figures

- Figure 1: Global Soluble Fibers Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Soluble Fibers Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Soluble Fibers Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Soluble Fibers Volume (K), by Application 2025 & 2033

- Figure 5: North America Soluble Fibers Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Soluble Fibers Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Soluble Fibers Revenue (undefined), by Type 2025 & 2033

- Figure 8: North America Soluble Fibers Volume (K), by Type 2025 & 2033

- Figure 9: North America Soluble Fibers Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Soluble Fibers Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Soluble Fibers Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Soluble Fibers Volume (K), by Country 2025 & 2033

- Figure 13: North America Soluble Fibers Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Soluble Fibers Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Soluble Fibers Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Soluble Fibers Volume (K), by Application 2025 & 2033

- Figure 17: South America Soluble Fibers Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Soluble Fibers Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Soluble Fibers Revenue (undefined), by Type 2025 & 2033

- Figure 20: South America Soluble Fibers Volume (K), by Type 2025 & 2033

- Figure 21: South America Soluble Fibers Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Soluble Fibers Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Soluble Fibers Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Soluble Fibers Volume (K), by Country 2025 & 2033

- Figure 25: South America Soluble Fibers Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Soluble Fibers Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Soluble Fibers Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Soluble Fibers Volume (K), by Application 2025 & 2033

- Figure 29: Europe Soluble Fibers Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Soluble Fibers Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Soluble Fibers Revenue (undefined), by Type 2025 & 2033

- Figure 32: Europe Soluble Fibers Volume (K), by Type 2025 & 2033

- Figure 33: Europe Soluble Fibers Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Soluble Fibers Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Soluble Fibers Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Soluble Fibers Volume (K), by Country 2025 & 2033

- Figure 37: Europe Soluble Fibers Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Soluble Fibers Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Soluble Fibers Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Soluble Fibers Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Soluble Fibers Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Soluble Fibers Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Soluble Fibers Revenue (undefined), by Type 2025 & 2033

- Figure 44: Middle East & Africa Soluble Fibers Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Soluble Fibers Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Soluble Fibers Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Soluble Fibers Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Soluble Fibers Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Soluble Fibers Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Soluble Fibers Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Soluble Fibers Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Soluble Fibers Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Soluble Fibers Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Soluble Fibers Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Soluble Fibers Revenue (undefined), by Type 2025 & 2033

- Figure 56: Asia Pacific Soluble Fibers Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Soluble Fibers Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Soluble Fibers Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Soluble Fibers Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Soluble Fibers Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Soluble Fibers Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Soluble Fibers Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Soluble Fibers Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Soluble Fibers Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Soluble Fibers Revenue undefined Forecast, by Type 2020 & 2033

- Table 4: Global Soluble Fibers Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Soluble Fibers Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Soluble Fibers Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Soluble Fibers Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Soluble Fibers Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Soluble Fibers Revenue undefined Forecast, by Type 2020 & 2033

- Table 10: Global Soluble Fibers Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Soluble Fibers Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Soluble Fibers Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Soluble Fibers Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Soluble Fibers Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Soluble Fibers Revenue undefined Forecast, by Type 2020 & 2033

- Table 22: Global Soluble Fibers Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Soluble Fibers Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Soluble Fibers Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Soluble Fibers Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Soluble Fibers Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Soluble Fibers Revenue undefined Forecast, by Type 2020 & 2033

- Table 34: Global Soluble Fibers Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Soluble Fibers Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Soluble Fibers Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Soluble Fibers Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Soluble Fibers Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Soluble Fibers Revenue undefined Forecast, by Type 2020 & 2033

- Table 58: Global Soluble Fibers Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Soluble Fibers Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Soluble Fibers Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Soluble Fibers Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Soluble Fibers Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Soluble Fibers Revenue undefined Forecast, by Type 2020 & 2033

- Table 76: Global Soluble Fibers Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Soluble Fibers Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Soluble Fibers Volume K Forecast, by Country 2020 & 2033

- Table 79: China Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Soluble Fibers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Soluble Fibers Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Soluble Fibers?

The projected CAGR is approximately 12.1%.

2. Which companies are prominent players in the Soluble Fibers?

Key companies in the market include Archer Daniels Midland Company, Cargill, Inc, DuPont, Grain Processing Corporation, INGREDION, Ingredion Incorporated, Nexira, Psyllium Labs, Wacker Chemie, Roquette Freres, Sudzucker AG, SunOpta Inc, Taiyo International, Tate and Lyle, TIC Gums.

3. What are the main segments of the Soluble Fibers?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Soluble Fibers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Soluble Fibers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Soluble Fibers?

To stay informed about further developments, trends, and reports in the Soluble Fibers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence