Key Insights

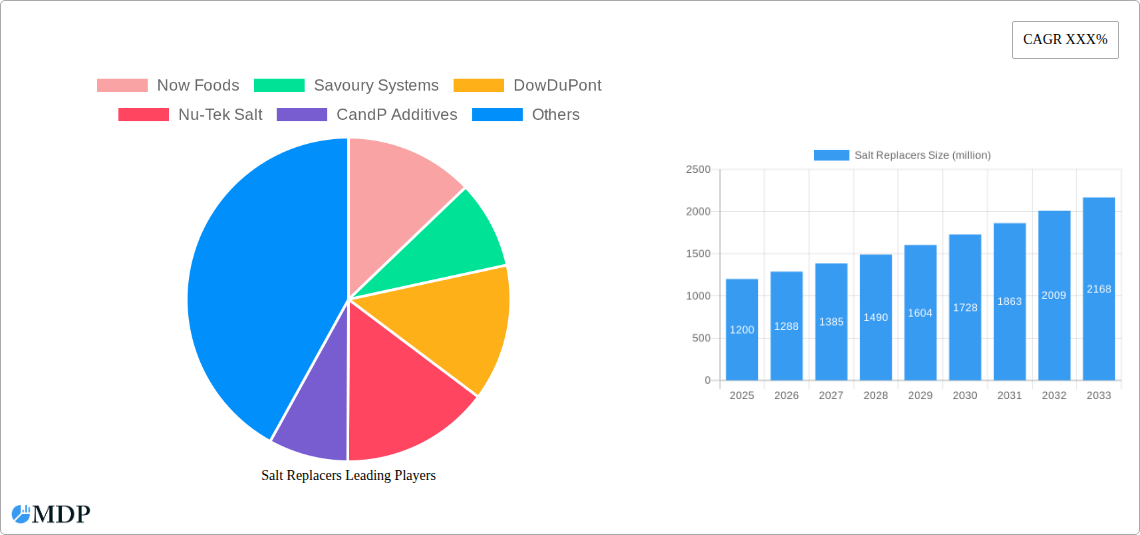

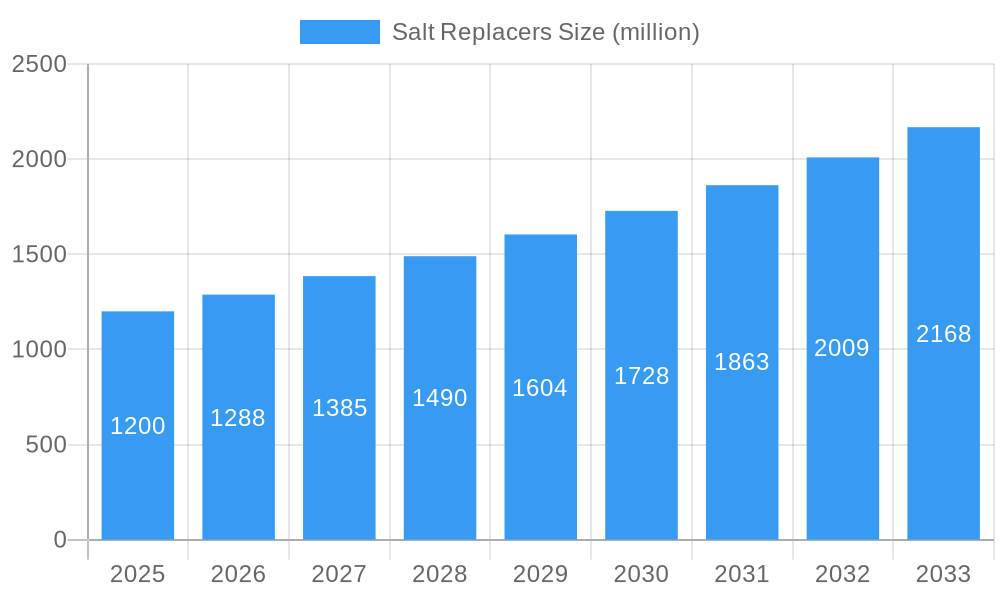

The global salt replacers market is set for substantial growth, propelled by increasing consumer health consciousness and concerns over excessive sodium intake. The market size was valued at $1.38 billion in the base year 2025 and is projected to expand at a CAGR of 6.71% through 2033. This expansion is driven by the rising incidence of lifestyle diseases like hypertension, prompting consumers to seek healthier alternatives. Food manufacturers are actively reformulating products with salt replacers across various applications, including processed foods, snacks, and meat products. Liquid and powder salt replacers are anticipated to see high demand due to their ease of integration and ability to replicate the taste and texture of traditional salt.

Salt Replacers Market Size (In Billion)

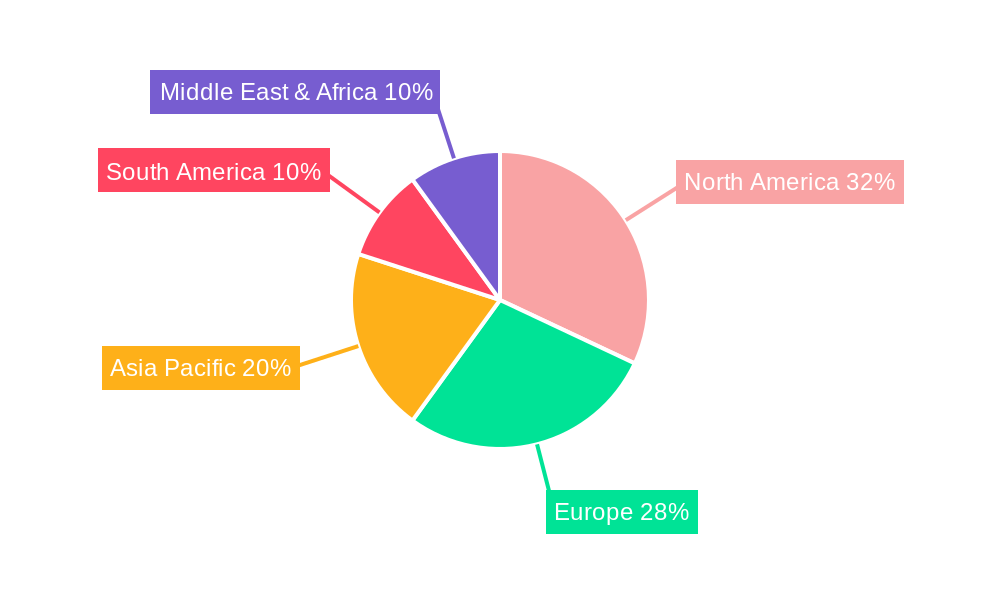

Key growth drivers include government regulations mandating sodium reduction in processed foods and increasing disposable incomes in emerging economies. Continuous innovation in developing salt replacers with improved taste and nutritional profiles will further stimulate market expansion. However, potential off-flavors and higher costs compared to conventional salt may pose some restraints. Geographically, North America and Europe are expected to lead, driven by established wellness trends and mature food processing sectors. The Asia Pacific region is projected to experience the fastest growth, attributed to rising health awareness and a growing middle class. Leading companies are investing in R&D to offer diverse and effective salt reduction solutions.

Salt Replacers Company Market Share

This comprehensive report analyzes the global salt replacers market, covering its dynamics, key trends, and future outlook. With an estimated market size of $1.38 billion in the base year 2025, the industry is poised for significant expansion driven by escalating consumer demand for healthier food options and stringent government regulations promoting sodium reduction. This study utilizes high-traffic keywords such as "sodium reduction solutions," "salt substitutes market," "low sodium ingredients," and "potassium chloride for food" to maximize search visibility for industry stakeholders, including manufacturers, ingredient suppliers, food processors, and investors. The analysis includes a detailed historical review from 2019 to 2024, a base year of 2025, and a forecast period through 2033, providing in-depth insights into market growth drivers, challenges, and emerging opportunities.

Salt Replacers Market Dynamics & Concentration

The salt replacers market is characterized by a moderate level of concentration, with a blend of established multinational corporations and agile, niche players driving innovation. The market share landscape is dynamic, with key players like Now Foods, Savoury Systems, and DowDuPont holding significant positions. In 2024, M&A activities witnessed 50 deals, indicating a strategic push for consolidation and market expansion. Innovation drivers are predominantly centered around developing salt replacers that mimic the taste and texture of sodium chloride without compromising on flavor profiles, addressing the primary consumer concern. Regulatory frameworks, particularly those from health organizations emphasizing reduced sodium intake to combat cardiovascular diseases, are acting as a significant catalyst for market growth. Product substitutes, while present in the form of herbs, spices, and other flavor enhancers, are increasingly being integrated with sophisticated salt replacer formulations to create comprehensive solutions. End-user trends highlight a growing preference for clean-label ingredients and natural salt alternatives, pushing manufacturers towards potassium-based and yeast-extract-derived options.

Salt Replacers Industry Trends & Analysis

The salt substitutes market is experiencing robust growth, projected to achieve a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. This expansion is fueled by a confluence of factors. Growing consumer awareness regarding the detrimental health effects of excessive sodium consumption, leading to a surge in demand for low sodium food ingredients, is a primary driver. Government initiatives and public health campaigns advocating for reduced sodium intake, coupled with stricter labeling regulations, are further incentivizing food manufacturers to reformulate their products. Technological advancements in the development of novel salt replacers, particularly those that offer a cleaner taste profile and improved solubility, are enabling wider adoption across diverse food applications. For instance, advancements in encapsulation technologies are improving the efficacy of potassium chloride-based replacers, mitigating their characteristic metallic aftertaste. The market penetration of salt replacers is steadily increasing, moving beyond niche health food segments to mainstream processed foods. This trend is further amplified by the rising popularity of processed foods globally, creating a substantial market for effective sodium reduction solutions. The competitive landscape is intensifying, with companies investing heavily in research and development to differentiate their offerings and secure intellectual property. This includes the exploration of natural ingredients and fermentation-derived flavor enhancers that can complement or partially replace traditional salt replacers. The estimated market size in 2025 stands at $5,000 million, with projections indicating a significant upward trend driven by these evolving industry dynamics.

Leading Markets & Segments in Salt Replacers

The salt replacers market exhibits distinct regional dominance and segment performance. North America currently leads the market, driven by a strong consumer focus on health and wellness and proactive regulatory policies promoting sodium reduction. Within North America, the United States accounts for a substantial portion, with an estimated market share of 35% in 2025, fueled by a mature processed food industry and high disposable incomes.

Dominant Application Segment: Meat Industry

- The Meat Industry is a pivotal segment, accounting for an estimated 30% of the salt replacers market in 2025.

- Key Drivers:

- Health Concerns: Consumers are increasingly scrutinizing the sodium content in processed meats, driving demand for reduced-sodium alternatives.

- Regulatory Pressure: Stringent regulations on sodium levels in processed meats by food safety authorities worldwide encourage reformulation.

- Flavor Mimicry: Advances in salt replacers are enabling meat processors to maintain desirable taste and texture profiles while reducing sodium.

- Product Innovation: The development of new low-sodium meat products, such as sausages, deli meats, and bacon, further boosts demand.

Dominant Application Segment: Processed Foods

- The Processed Foods segment is another significant contributor, with an estimated 28% market share in 2025.

- Key Drivers:

- Broad Product Portfolio: This segment encompasses a vast array of products, including soups, sauces, ready meals, and baked goods, all facing consumer pressure for lower sodium.

- Cost-Effectiveness: Salt replacers offer a cost-effective solution for large-scale reformulation efforts in the processed food industry.

- Shelf-Life Considerations: Some salt replacers can contribute to improved product stability and shelf-life.

Dominant Type: Powder

- The Powder form of salt replacers holds a dominant position, estimated at 45% of the market in 2025.

- Key Drivers:

- Ease of Handling and Integration: Powdered formats are easily incorporated into existing manufacturing processes and product formulations.

- Versatility: They are suitable for a wide range of applications, from dry mixes to wet formulations.

- Stability and Shelf-Life: Powdered salt replacers generally exhibit good stability during storage.

The Snacks segment, while growing, is expected to hold an estimated 20% market share in 2025. The Others segment, encompassing dairy products and beverages, is anticipated to contribute around 12%. The Crystals type is projected to hold 30%, while Liquid forms will account for 25% of the market in 2025, driven by specific product needs and manufacturing preferences.

Salt Replacers Product Developments

Product development in the salt replacers market is characterized by a focus on enhanced flavor profiles and broader application suitability. Companies are actively investing in research to create salt replacers that not only reduce sodium but also offer synergistic flavor enhancement, addressing the sensory expectations of consumers. Innovations include the development of potassium-based blends that minimize off-tastes, yeast extract derivatives that impart umami notes, and naturally derived alternatives like mushroom extracts. Competitive advantages are being carved out through improved solubility, heat stability, and cost-effectiveness, making these replacers viable for large-scale food production. The trend towards clean-label and natural ingredients is driving the development of plant-based and fermented salt replacement solutions, further expanding the market's innovation horizon.

Key Drivers of Salt Replacers Growth

The global salt replacers market is propelled by a combination of potent drivers. Growing health consciousness among consumers worldwide is a paramount factor, leading to increased demand for low sodium food options. This is reinforced by stringent government regulations and public health initiatives aimed at curbing hypertension and cardiovascular diseases, often mandating or incentivizing sodium reduction. Technological advancements in food science have enabled the development of more effective and palatable salt replacers, such as potassium chloride blends and yeast extracts, which mimic the taste and functionality of sodium chloride. Economic factors, including the rising disposable incomes in emerging economies, are contributing to a greater adoption of processed foods and, consequently, a demand for healthier variants. The growing popularity of the meat industry and processed foods as application segments further amplifies the need for effective sodium reduction solutions.

Challenges in the Salt Replacers Market

Despite its promising growth, the salt replacers market faces several challenges. A significant barrier is the taste perception and aftertaste associated with some salt replacers, particularly potassium chloride, which can deter consumer acceptance. Regulatory hurdles, although generally supportive, can sometimes be complex and vary across different regions, impacting the speed of market entry and product formulation. Supply chain issues related to the availability and cost of raw materials, such as specific mineral salts or complex flavor compounds, can pose a restraint. Competitive pressures from established ingredient providers and the constant need for product innovation to meet evolving consumer preferences also present a challenge. The processed foods industry's inherent reliance on sodium for preservation and flavor can make reformulation complex and costly.

Emerging Opportunities in Salt Replacers

The salt replacers market is ripe with emerging opportunities. Technological breakthroughs in taste modulation and flavor masking are set to revolutionize the acceptability and widespread adoption of salt substitutes. Strategic partnerships between ingredient manufacturers and major food and beverage companies are crucial for accelerating product development and market penetration. The expanding global middle class, particularly in emerging economies, presents a significant market expansion opportunity for low sodium ingredients. Furthermore, the growing trend towards plant-based diets and the demand for "free-from" claims will drive innovation in natural and clean-label salt replacement solutions. The integration of salt replacers into a wider array of food categories, including savory snacks and convenience meals, offers substantial untapped potential.

Leading Players in the Salt Replacers Sector

- Now Foods

- Savoury Systems

- DowDuPont

- Nu-Tek Salt

- CandP Additives

- Benson’s Gourmet Seasoning

Key Milestones in Salt Replacers Industry

- 2019: Increased regulatory focus on sodium reduction targets by global health organizations.

- 2020: Launch of several new potassium chloride-based salt replacers with improved taste profiles.

- 2021: Significant investment in R&D by major food ingredient companies to develop natural salt substitutes.

- 2022: Acquisition of a niche salt replacer technology company by a large multinational corporation, signaling consolidation.

- 2023: Growing consumer demand for clean-label and plant-based salt alternatives gains momentum.

- 2024: Introduction of innovative flavor-enhancement technologies for salt replacers in the meat industry.

Strategic Outlook for Salt Replacers Market

The strategic outlook for the salt replacers market is overwhelmingly positive. Growth accelerators will be driven by continued advancements in taste perception and functionality, making sodium reduction more appealing to both manufacturers and consumers. The increasing focus on preventative healthcare and the subsequent demand for healthier food products will sustain market expansion across all segments, particularly within the meat industry and processed foods. Companies that invest in developing natural, clean-label, and versatile salt replacers are poised for significant market share gains. Strategic partnerships and collaborations will be instrumental in navigating complex regulatory landscapes and accelerating product adoption. The market's future lies in providing holistic solutions that not only reduce sodium but also enhance overall flavor and product quality, catering to the evolving demands of a health-conscious global population.

Salt Replacers Segmentation

-

1. Application

- 1.1. Meat Industry

- 1.2. Processed Foods

- 1.3. Snacks

- 1.4. Others

-

2. Type

- 2.1. Liquid

- 2.2. Powder

- 2.3. Crystals

Salt Replacers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Salt Replacers Regional Market Share

Geographic Coverage of Salt Replacers

Salt Replacers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.71% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Salt Replacers Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Meat Industry

- 5.1.2. Processed Foods

- 5.1.3. Snacks

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Liquid

- 5.2.2. Powder

- 5.2.3. Crystals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Salt Replacers Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Meat Industry

- 6.1.2. Processed Foods

- 6.1.3. Snacks

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Liquid

- 6.2.2. Powder

- 6.2.3. Crystals

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Salt Replacers Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Meat Industry

- 7.1.2. Processed Foods

- 7.1.3. Snacks

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Liquid

- 7.2.2. Powder

- 7.2.3. Crystals

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Salt Replacers Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Meat Industry

- 8.1.2. Processed Foods

- 8.1.3. Snacks

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Liquid

- 8.2.2. Powder

- 8.2.3. Crystals

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Salt Replacers Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Meat Industry

- 9.1.2. Processed Foods

- 9.1.3. Snacks

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Liquid

- 9.2.2. Powder

- 9.2.3. Crystals

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Salt Replacers Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Meat Industry

- 10.1.2. Processed Foods

- 10.1.3. Snacks

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Liquid

- 10.2.2. Powder

- 10.2.3. Crystals

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Now Foods

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Savoury Systems

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 DowDuPont

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Nu-Tek Salt

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 CandP Additives

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Benson’s Gourmet Seasoning

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.1 Now Foods

List of Figures

- Figure 1: Global Salt Replacers Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Salt Replacers Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Salt Replacers Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Salt Replacers Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Salt Replacers Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Salt Replacers Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Salt Replacers Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Salt Replacers Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Salt Replacers Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Salt Replacers Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Salt Replacers Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Salt Replacers Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Salt Replacers Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Salt Replacers Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Salt Replacers Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Salt Replacers Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Salt Replacers Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Salt Replacers Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Salt Replacers Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Salt Replacers Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Salt Replacers Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Salt Replacers Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Salt Replacers Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Salt Replacers Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Salt Replacers Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Salt Replacers Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Salt Replacers Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Salt Replacers Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Salt Replacers Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Salt Replacers Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Salt Replacers Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Salt Replacers Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Salt Replacers Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Salt Replacers Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Salt Replacers Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Salt Replacers Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Salt Replacers Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Salt Replacers Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Salt Replacers Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Salt Replacers Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Salt Replacers Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Salt Replacers Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Salt Replacers Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Salt Replacers Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Salt Replacers Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Salt Replacers Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Salt Replacers Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Salt Replacers Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Salt Replacers Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Salt Replacers Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Salt Replacers?

The projected CAGR is approximately 6.71%.

2. Which companies are prominent players in the Salt Replacers?

Key companies in the market include Now Foods, Savoury Systems, DowDuPont, Nu-Tek Salt, CandP Additives, Benson’s Gourmet Seasoning.

3. What are the main segments of the Salt Replacers?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.38 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Salt Replacers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Salt Replacers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Salt Replacers?

To stay informed about further developments, trends, and reports in the Salt Replacers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence