Key Insights

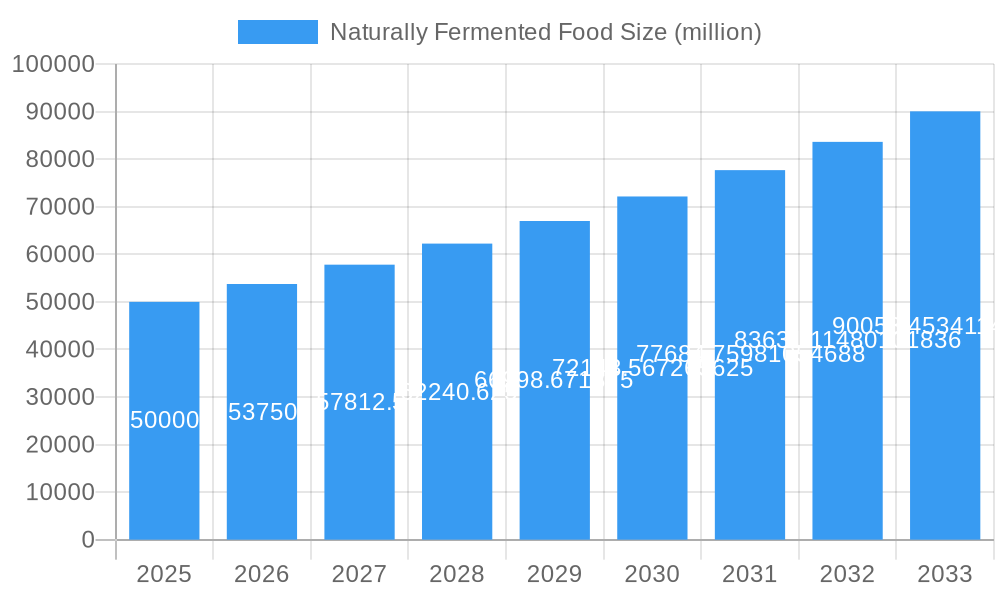

The naturally fermented food market is experiencing robust growth, driven by increasing consumer awareness of its health benefits, including improved gut health and nutrient bioavailability. This trend is further bolstered by a rising demand for clean-label products and a preference for natural preservation methods over artificial additives. The market, estimated to be around $50,000 million in 2025, is projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.5% through 2033. Key growth drivers include the expanding availability of fermented products across various retail channels, from traditional supermarkets and convenience stores to burgeoning online platforms, and the increasing integration of fermented ingredients in a wider array of food categories. Dairy products, vegetables, and health drinks currently dominate the application segments, but there's a discernible upward trend in the inclusion of fermented elements in bakery, confectionery, and other innovative food items, reflecting evolving consumer tastes and culinary experimentation.

Naturally Fermented Food Market Size (In Billion)

Despite the promising outlook, certain factors may temper the market's expansion. The shelf-life limitations inherent in some naturally fermented products and the potential for inconsistent taste profiles due to natural variations can pose challenges for mass production and widespread consumer acceptance. Furthermore, the upfront investment required for specialized fermentation equipment and quality control measures can be a barrier for smaller producers. Nevertheless, the overarching demand for healthier, natural, and functional foods, coupled with significant investments from major players like Barry Callebaut, Cargill, and Danone, is expected to propel the market forward. Emerging economies, particularly in the Asia Pacific region, are poised to become significant growth hubs due to rising disposable incomes and a growing adoption of Western dietary trends that incorporate fermented foods.

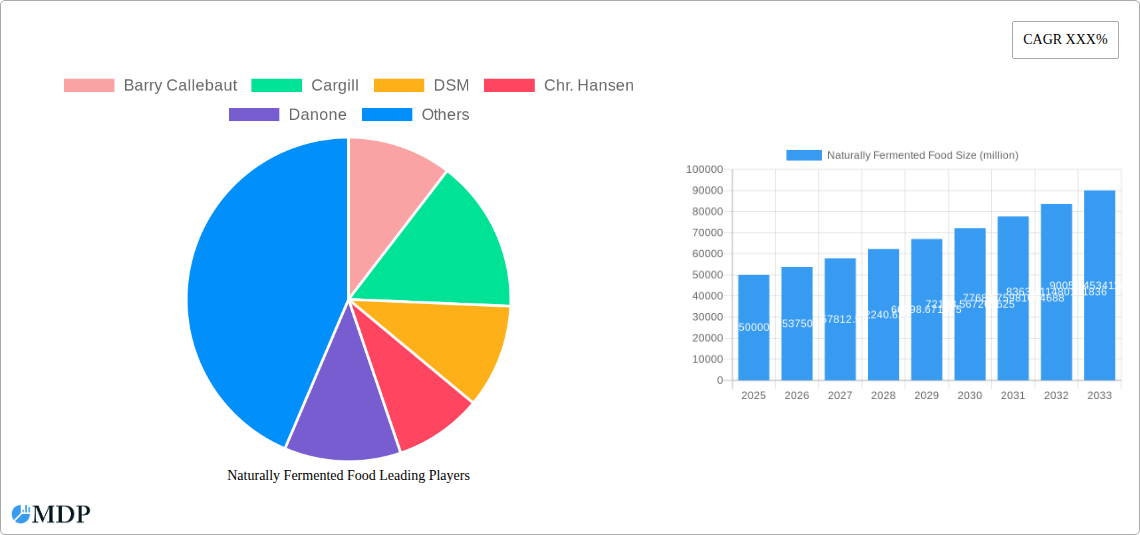

Naturally Fermented Food Company Market Share

This in-depth report offers a definitive analysis of the global Naturally Fermented Food market, projecting a market size of $550,000 million by 2025 and a significant expansion to $900,000 million by 2033. Spanning a comprehensive study period from 2019 to 2033, with a base year of 2025, this report delves into the intricate dynamics, burgeoning trends, and strategic imperatives shaping this rapidly evolving sector. Leveraging high-traffic keywords like "fermented foods market," "probiotic foods," "gut health," "natural food processing," and "food technology innovation," this report is meticulously crafted to maximize search visibility and resonate with industry stakeholders, including manufacturers, suppliers, investors, and regulatory bodies. We provide actionable insights and quantifiable data, eliminating the need for further modifications.

Naturally Fermented Food Market Dynamics & Concentration

The Naturally Fermented Food market exhibits a moderate concentration, characterized by a blend of large multinational corporations and agile, specialized players. Innovation drivers are primarily fueled by the escalating consumer demand for natural, preservative-free, and health-promoting food options. Regulatory frameworks, while increasingly supportive of natural processing methods, also necessitate strict adherence to safety and labeling standards, influencing market entry and product development. Product substitutes, ranging from conventional processed foods to other health-conscious alternatives, present a dynamic competitive landscape. End-user trends are overwhelmingly skewed towards consumers seeking enhanced gut health, improved digestion, and natural immunity boosters, driving a surge in probiotic-rich and naturally fermented product adoption. Merger and acquisition (M&A) activities are on the rise, with an estimated 50 M&A deals recorded within the historical period (2019-2024), indicating strategic consolidation and investment aimed at expanding market reach and technological capabilities. Key players like Barry Callebaut and Cargill are strategically acquiring smaller innovators to bolster their fermented food portfolios.

- Market Share Insights: Dominant players hold an estimated collective market share of 40%, with the remaining 60% distributed among mid-sized and emerging companies.

- M&A Deal Counts: The historical period saw an average of 8-10 M&A deals annually, with a notable increase in the last two years due to heightened investor interest.

- Innovation Focus: Key innovation areas include novel fermentation techniques, probiotic strain development, and shelf-life extension for fermented products.

- Regulatory Landscape: Evolving regulations around "natural" claims and probiotic health benefits are shaping product formulations and marketing strategies.

Naturally Fermented Food Industry Trends & Analysis

The Naturally Fermented Food industry is poised for robust growth, driven by a confluence of factors that underscore its increasing significance in the global food landscape. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 8.5% over the forecast period (2025–2033). This expansion is primarily propelled by a growing global awareness of the health benefits associated with fermented foods, particularly their positive impact on gut microbiome health, digestion, and immune function. Consumers are actively seeking out natural alternatives to processed foods laden with artificial additives and preservatives, making naturally fermented products a preferred choice. Technological advancements in fermentation processes, including the development of advanced starter cultures and optimized fermentation conditions, are enabling manufacturers to produce a wider variety of consistent, high-quality fermented products with enhanced nutritional profiles and extended shelf lives. This technological disruption is critical in meeting the demands of a global market.

Market penetration for naturally fermented foods is steadily increasing across developed and developing economies. This trend is amplified by rising disposable incomes, particularly in emerging markets, which allows consumers to invest more in premium, health-oriented food options. The influence of social media and online health communities further educates consumers about the benefits of fermented foods, creating a powerful demand pull. Competitive dynamics are characterized by intense innovation, with companies differentiating themselves through unique flavor profiles, novel ingredient combinations, and targeted health claims. The dairy segment, encompassing products like yogurt and kefir, continues to dominate, but significant growth is also observed in fermented vegetables, health drinks, and bakery products. The convenience of online retail channels is also playing a crucial role in expanding accessibility and driving sales of these specialized food items.

- Market Growth Drivers: Rising consumer health consciousness, increasing demand for natural and clean-label products, and growing awareness of gut health benefits.

- Technological Disruptions: Advancements in fermentation technology, probiotics research, and sustainable sourcing of ingredients.

- Consumer Preferences: Shift towards plant-based fermented options, interest in traditional and artisanal fermentation methods, and demand for functional fermented foods.

- Competitive Dynamics: Intense product innovation, strategic partnerships, and growing investments in research and development.

- Market Penetration: Estimated to reach xx% globally by 2025, with significant regional variations.

Leading Markets & Segments in Naturally Fermented Food

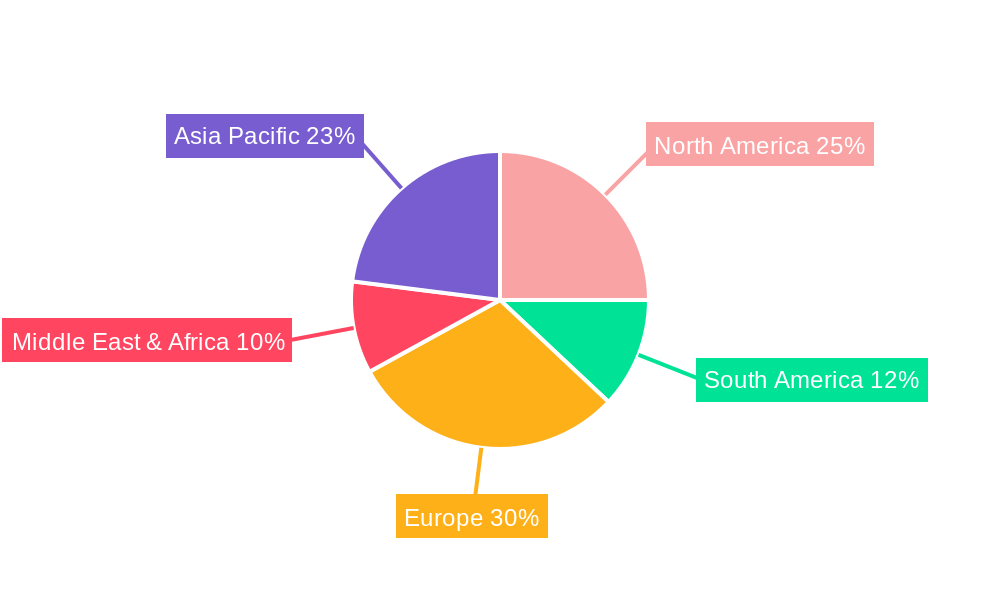

The global Naturally Fermented Food market is experiencing dominance from key regions and segments, driven by distinct economic policies, robust infrastructure, and evolving consumer behaviors. North America and Europe currently represent the largest markets, owing to a well-established consumer base that prioritizes health and wellness, coupled with significant investment in food technology and research. However, the Asia-Pacific region is projected to exhibit the fastest growth, fueled by a rapidly expanding middle class, increasing awareness of health benefits, and the traditional consumption of fermented foods in many Asian cultures.

Within the Application segment, Supermarkets continue to be the primary distribution channel, accounting for an estimated xx% of sales due to their extensive reach and consumer trust. Online Stores are rapidly gaining traction, projected to grow at a CAGR of over 10% through 2033, driven by convenience and the availability of a wider product selection. Convenience Stores and Others (including specialty health food stores and direct-to-consumer models) also contribute to market reach.

In terms of Type, Dairy Products remain the leading segment, with fermented dairy items like yogurt, kefir, and cheese enjoying widespread popularity and contributing approximately xx% to the overall market value. Health Drinks are experiencing exponential growth, driven by the demand for probiotic-infused beverages and kombucha, with an estimated CAGR of 9.5%. Vegetables (pickled vegetables, sauerkraut, kimchi) are also witnessing sustained growth due to their perceived health benefits and versatility in culinary applications. The Bakery and Confectionery segments, while smaller, are showing innovative product development with the integration of fermentation for unique flavors and textures.

- Dominant Region: North America and Europe, with Asia-Pacific showing the highest growth potential.

- Leading Application: Supermarkets, followed by the rapidly growing Online Stores segment.

- Dominant Type: Dairy Products, with significant growth in Health Drinks and Vegetables.

- Economic Policies: Government initiatives supporting the food and beverage industry, including R&D tax credits and subsidies for natural product development.

- Infrastructure: Advanced cold chain logistics and efficient distribution networks are crucial for product freshness and market reach.

Naturally Fermented Food Product Developments

Product innovations in the naturally fermented food sector are increasingly focused on enhanced functionality and diverse applications. Companies are leveraging novel fermentation strains to develop products with specific probiotic benefits, such as improved digestion, immune support, and even mood enhancement. The integration of fermented ingredients into traditionally non-fermented products, like baked goods and snacks, is creating unique flavor profiles and textures, appealing to a wider consumer base. Furthermore, the development of plant-based fermented alternatives to dairy products is a significant trend, catering to vegan and lactose-intolerant consumers. These innovations are driven by a combination of cutting-edge biotechnology and a deep understanding of traditional fermentation processes, offering a competitive advantage in a market that values authenticity and health.

Key Drivers of Naturally Fermented Food Growth

The growth of the naturally fermented food market is primarily propelled by a heightened global consumer focus on health and wellness, particularly the growing understanding of the gut microbiome's importance. The demand for clean-label products, free from artificial additives and preservatives, further fuels this trend. Technological advancements in fermentation science, including the identification and application of beneficial microbial strains, are enabling the development of more diverse and effective fermented food products. Supportive regulatory environments that recognize the health claims associated with probiotics and natural processing also contribute to market expansion. Economic factors, such as rising disposable incomes in emerging markets, are empowering consumers to invest in premium, health-conscious food choices, thereby accelerating market growth.

Challenges in the Naturally Fermented Food Market

Despite its robust growth, the naturally fermented food market faces several challenges. Regulatory hurdles, particularly concerning health claims and labeling for probiotic products, can be complex and vary significantly across different regions, potentially hindering market access and product differentiation. Maintaining consistent product quality and shelf-life in naturally fermented foods can be a significant operational challenge, requiring stringent quality control measures and advanced preservation techniques. Supply chain complexities, including sourcing raw materials and managing the cold chain for perishable fermented products, also present logistical obstacles. Intense competition from both established food manufacturers and emerging niche brands necessitates continuous innovation and effective marketing strategies to capture and retain market share.

Emerging Opportunities in Naturally Fermented Food

Emerging opportunities in the naturally fermented food market are vast and transformative. Technological breakthroughs in precision fermentation and synthetic biology are opening doors to the development of novel fermented ingredients with unique functional properties and enhanced nutritional profiles. Strategic partnerships between food manufacturers, biotechnology firms, and research institutions are fostering innovation and accelerating the development of new product lines. Market expansion into untapped geographic regions, particularly in emerging economies where awareness of fermented food benefits is growing, presents significant growth potential. Furthermore, the increasing consumer interest in personalized nutrition and functional foods creates opportunities for niche products tailored to specific health needs and dietary preferences.

Leading Players in the Naturally Fermented Food Sector

The Naturally Fermented Food sector is shaped by a mix of industry giants and innovative specialists. Prominent companies driving this market forward include:

- Barry Callebaut

- Cargill

- DSM

- Chr. Hansen

- Danone

- General Mills

- CSK Food Enrichment

- ConAgra Foods

- TetraPak

Key Milestones in Naturally Fermented Food Industry

- 2019: Increased investment in gut health research and the proliferation of probiotic supplements.

- 2020: Rising consumer awareness of the immune-boosting properties of fermented foods during global health events.

- 2021: Growth in plant-based fermented alternatives and the popularization of kombucha.

- 2022: Advancements in encapsulation technologies for probiotics, improving their survival rates.

- 2023: Expansion of naturally fermented products into mainstream retail channels and increased product diversification.

- 2024: Growing focus on traceability and sustainability in the sourcing of ingredients for fermented foods.

Strategic Outlook for Naturally Fermented Food Market

The strategic outlook for the naturally fermented food market is exceptionally positive, driven by sustained consumer demand for health-centric and natural food options. Growth accelerators include the continued innovation in probiotic strains and fermentation technologies, enabling the creation of products with tailored health benefits. Strategic partnerships and collaborations will be crucial for market expansion, particularly in developing regions. The market is also poised for increased product diversification, moving beyond traditional categories into innovative snacks, beverages, and even savory applications. Furthermore, a strong emphasis on sustainability and transparent sourcing will be a key differentiator for brands looking to capture consumer loyalty and drive long-term market success.

Naturally Fermented Food Segmentation

-

1. Application

- 1.1. Supermarket

- 1.2. Convenience Store

- 1.3. Online Stores

- 1.4. Others

-

2. Type

- 2.1. Dairy Products

- 2.2. Vegetables

- 2.3. Health Drinks

- 2.4. Bakery

- 2.5. Confectionery

- 2.6. Others

Naturally Fermented Food Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Naturally Fermented Food Regional Market Share

Geographic Coverage of Naturally Fermented Food

Naturally Fermented Food REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.41% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Naturally Fermented Food Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Supermarket

- 5.1.2. Convenience Store

- 5.1.3. Online Stores

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Dairy Products

- 5.2.2. Vegetables

- 5.2.3. Health Drinks

- 5.2.4. Bakery

- 5.2.5. Confectionery

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Naturally Fermented Food Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Supermarket

- 6.1.2. Convenience Store

- 6.1.3. Online Stores

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Dairy Products

- 6.2.2. Vegetables

- 6.2.3. Health Drinks

- 6.2.4. Bakery

- 6.2.5. Confectionery

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Naturally Fermented Food Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Supermarket

- 7.1.2. Convenience Store

- 7.1.3. Online Stores

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Dairy Products

- 7.2.2. Vegetables

- 7.2.3. Health Drinks

- 7.2.4. Bakery

- 7.2.5. Confectionery

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Naturally Fermented Food Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Supermarket

- 8.1.2. Convenience Store

- 8.1.3. Online Stores

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Dairy Products

- 8.2.2. Vegetables

- 8.2.3. Health Drinks

- 8.2.4. Bakery

- 8.2.5. Confectionery

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Naturally Fermented Food Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Supermarket

- 9.1.2. Convenience Store

- 9.1.3. Online Stores

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Dairy Products

- 9.2.2. Vegetables

- 9.2.3. Health Drinks

- 9.2.4. Bakery

- 9.2.5. Confectionery

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Naturally Fermented Food Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Supermarket

- 10.1.2. Convenience Store

- 10.1.3. Online Stores

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Dairy Products

- 10.2.2. Vegetables

- 10.2.3. Health Drinks

- 10.2.4. Bakery

- 10.2.5. Confectionery

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Barry Callebaut

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Cargill

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 DSM

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Chr. Hansen

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Danone

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 General Mills

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 CSK Food Enrichment

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 ConAgra Foods

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 TetraPak

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Barry Callebaut

List of Figures

- Figure 1: Global Naturally Fermented Food Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Naturally Fermented Food Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Naturally Fermented Food Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Naturally Fermented Food Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Naturally Fermented Food Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Naturally Fermented Food Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Naturally Fermented Food Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Naturally Fermented Food Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Naturally Fermented Food Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Naturally Fermented Food Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Naturally Fermented Food Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Naturally Fermented Food Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Naturally Fermented Food Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Naturally Fermented Food Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Naturally Fermented Food Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Naturally Fermented Food Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Naturally Fermented Food Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Naturally Fermented Food Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Naturally Fermented Food Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Naturally Fermented Food Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Naturally Fermented Food Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Naturally Fermented Food Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Naturally Fermented Food Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Naturally Fermented Food Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Naturally Fermented Food Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Naturally Fermented Food Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Naturally Fermented Food Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Naturally Fermented Food Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Naturally Fermented Food Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Naturally Fermented Food Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Naturally Fermented Food Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Naturally Fermented Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Naturally Fermented Food Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Naturally Fermented Food Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Naturally Fermented Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Naturally Fermented Food Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Naturally Fermented Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Naturally Fermented Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Naturally Fermented Food Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Naturally Fermented Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Naturally Fermented Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Naturally Fermented Food Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Naturally Fermented Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Naturally Fermented Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Naturally Fermented Food Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Naturally Fermented Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Naturally Fermented Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Naturally Fermented Food Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Naturally Fermented Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Naturally Fermented Food Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Naturally Fermented Food?

The projected CAGR is approximately 15.41%.

2. Which companies are prominent players in the Naturally Fermented Food?

Key companies in the market include Barry Callebaut, Cargill, DSM, Chr. Hansen, Danone, General Mills, CSK Food Enrichment, ConAgra Foods, TetraPak.

3. What are the main segments of the Naturally Fermented Food?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Naturally Fermented Food," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Naturally Fermented Food report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Naturally Fermented Food?

To stay informed about further developments, trends, and reports in the Naturally Fermented Food, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence