Key Insights

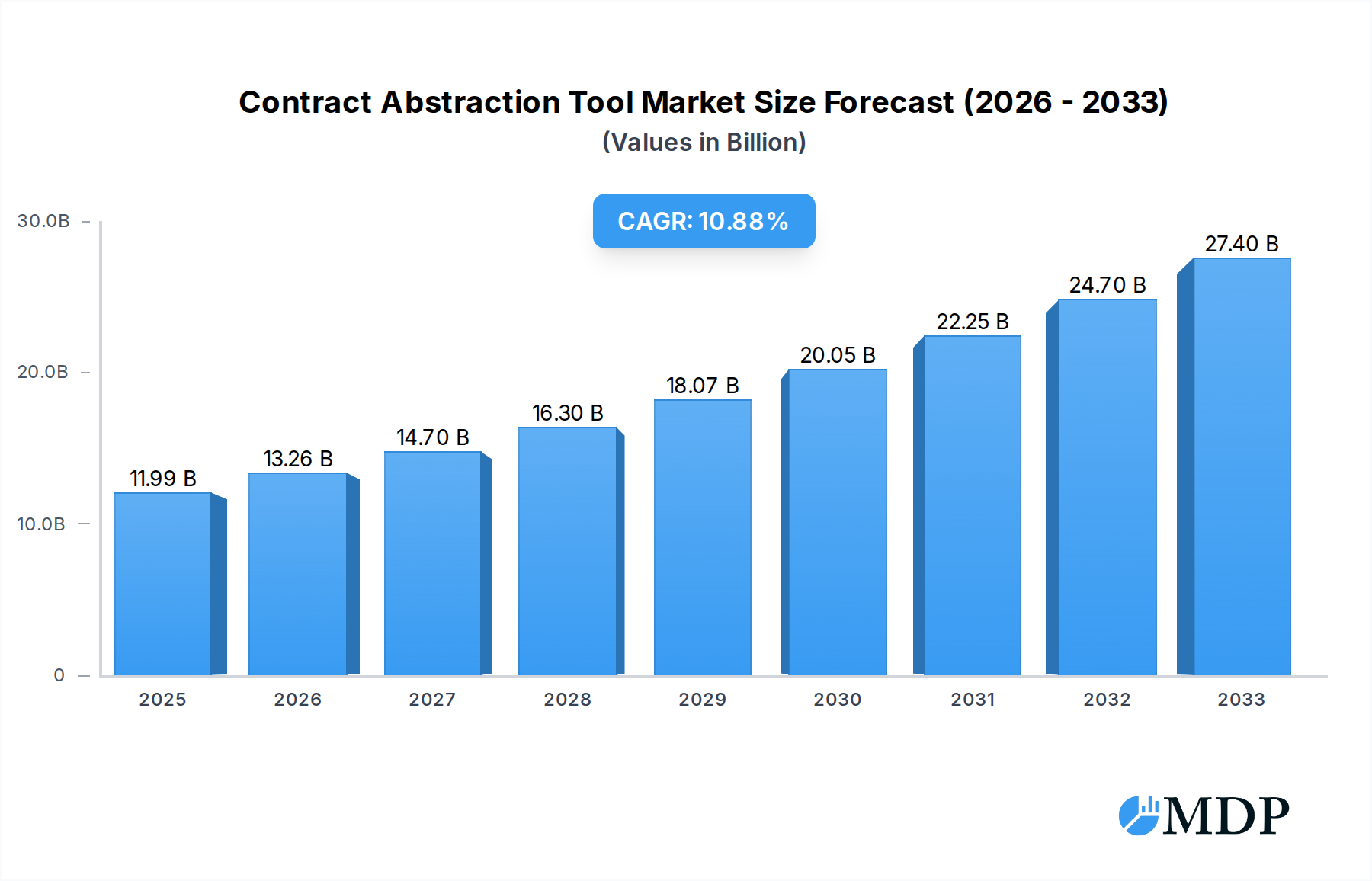

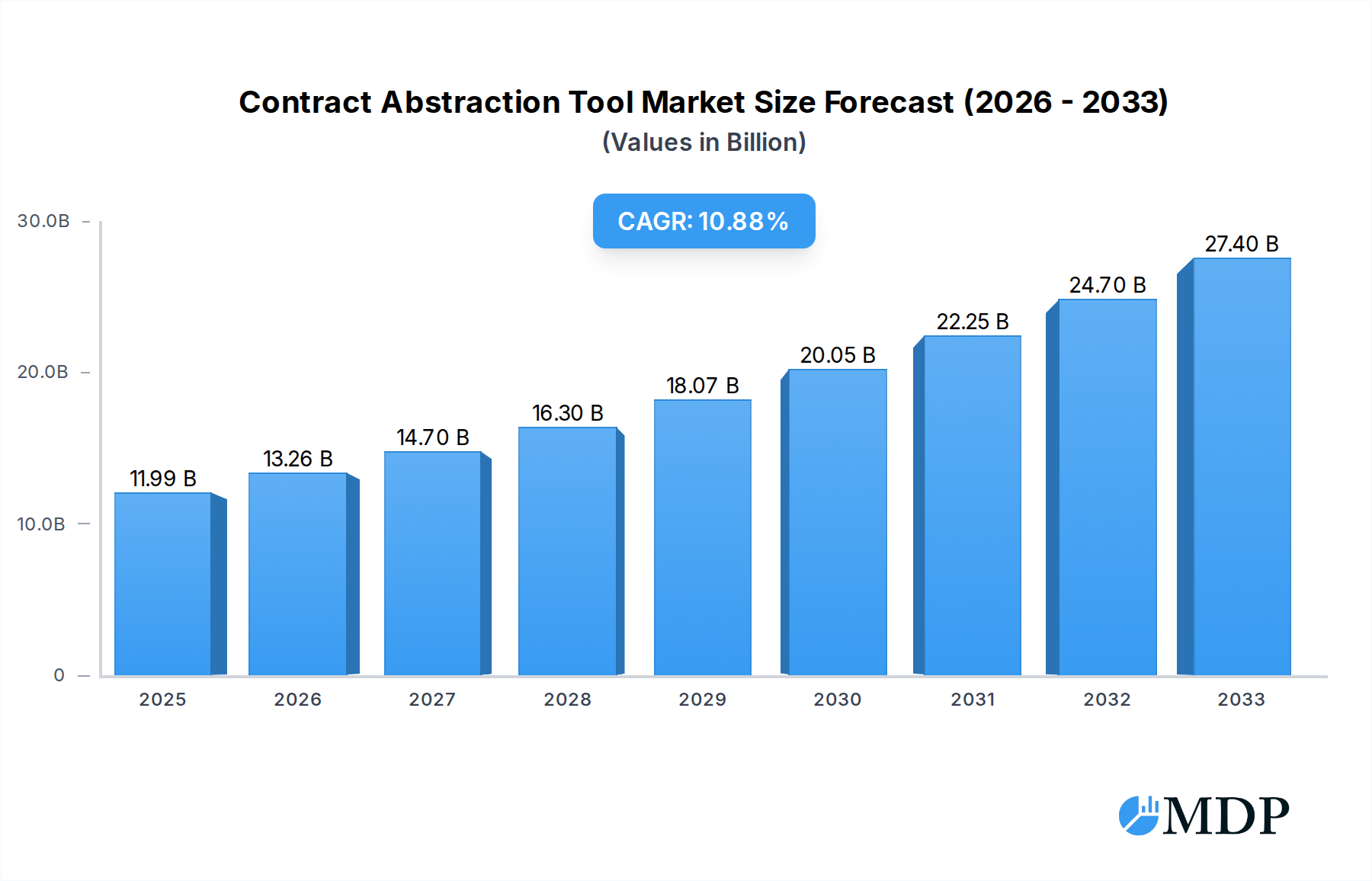

The Contract Abstraction Tool market is poised for significant expansion, projected to reach $11.99 billion by 2025, driven by an impressive CAGR of 10.62% over the forecast period. This robust growth is fueled by the increasing volume and complexity of contracts across all business sectors, necessitating advanced solutions for efficient data extraction and analysis. Large enterprises, facing vast repositories of legal documents, are key adopters, leveraging these tools to mitigate risks, ensure compliance, and streamline operations. Simultaneously, Small and Medium-sized Enterprises (SMEs) are increasingly recognizing the value proposition, with cloud-based solutions offering an accessible and scalable entry point into contract management automation. The demand for enhanced contract review speed, accuracy, and the reduction of manual errors are paramount drivers, compelling businesses to invest in sophisticated AI-powered abstraction tools.

Contract Abstraction Tool Market Size (In Billion)

The market's trajectory is further shaped by evolving trends such as the integration of AI and machine learning for deeper insights, natural language processing (NLP) for semantic understanding, and the growing adoption of automated workflows in legal departments. While the market benefits from these advancements, certain restraints, such as the initial investment costs for on-premises solutions and the need for specialized technical expertise, may present challenges for some organizations. However, the clear benefits of improved operational efficiency, cost savings through early risk detection, and enhanced strategic decision-making through readily accessible contract data are expected to outweigh these limitations. Key players like DocuSign, IBM, and ContractPodAi are at the forefront, offering innovative solutions that cater to diverse enterprise needs, further solidifying the market's growth potential in the coming years.

Contract Abstraction Tool Company Market Share

Contract Abstraction Tool Market: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report provides a comprehensive analysis of the global Contract Abstraction Tool market, covering historical trends, current dynamics, and future projections. With a study period from 2019 to 2033, a base year of 2025, and an estimated year also of 2025, this report leverages expert insights and data-driven projections to deliver actionable intelligence for industry stakeholders. We analyze the market's trajectory, identify key growth drivers, explore emerging opportunities, and highlight leading players and their strategic initiatives. This report is designed for immediate use, offering a definitive view of the contract abstraction tool landscape.

Contract Abstraction Tool Market Dynamics & Concentration

The global Contract Abstraction Tool market is characterized by a dynamic and evolving competitive landscape. Market concentration is moderately high, with several established players and a growing number of innovative startups vying for market share. Innovation drivers are primarily centered around advancements in Artificial Intelligence (AI) and Machine Learning (ML) for enhanced data extraction accuracy, natural language processing (NLP) for semantic understanding of contract clauses, and the increasing demand for automated contract review processes across various industries. Regulatory frameworks, particularly around data privacy and contract compliance, are also shaping market evolution, pushing for more robust and secure abstraction solutions. Product substitutes, while present in the form of manual abstraction or less sophisticated document management systems, are increasingly being outpaced by the efficiency and accuracy offered by dedicated contract abstraction tools. End-user trends indicate a strong preference for cloud-based solutions due to their scalability, accessibility, and cost-effectiveness, although on-premises solutions remain relevant for organizations with stringent data security requirements. Mergers and Acquisitions (M&A) activities are significant, with larger technology firms acquiring specialized AI contract abstraction companies to integrate advanced capabilities into their existing portfolios and expand market reach. For instance, the acquisition of Seal Software by DocuSign exemplifies this trend, consolidating market power and accelerating product development. The M&A deal count is projected to remain robust, indicating a healthy appetite for consolidation and strategic expansion. Market share is increasingly being influenced by the ability of vendors to demonstrate tangible ROI through time savings, risk reduction, and improved contract compliance for their clients. The market is transitioning from a niche offering to a critical component of enterprise legal tech stacks.

- Market Concentration: Moderately high with established vendors and emerging innovators.

- Innovation Drivers: AI/ML for accuracy, NLP for semantic understanding, automation.

- Regulatory Influence: Data privacy, contract compliance driving demand for secure solutions.

- Product Substitutes: Manual abstraction, basic document management systems.

- End-User Trends: Strong preference for cloud-based solutions, with on-premises options for specific needs.

- M&A Activities: Significant, driven by consolidation and integration of advanced AI capabilities.

- M&A Deal Count: Expected to remain robust, indicating strategic expansion.

Contract Abstraction Tool Industry Trends & Analysis

The global Contract Abstraction Tool market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 18.7% from 2025 to 2033. This robust growth is fueled by a confluence of factors, including the accelerating digital transformation initiatives across enterprises, the increasing volume and complexity of contracts managed by organizations, and the burgeoning demand for efficient and accurate legal operations. Technological disruptions, particularly in the realm of Artificial Intelligence (AI) and Machine Learning (ML), are at the forefront of this market evolution. Advanced AI algorithms are enabling contract abstraction tools to move beyond simple keyword extraction to sophisticated semantic analysis, identifying critical clauses, obligations, risks, and opportunities within contracts with unprecedented accuracy. This capability directly addresses the growing need for proactive risk management and strategic contract lifecycle management. Consumer preferences are increasingly leaning towards solutions that offer seamless integration with existing business workflows, intuitive user interfaces, and demonstrable return on investment (ROI). The ability of these tools to significantly reduce manual effort, minimize human error, and accelerate contract review cycles is a major draw for businesses seeking to optimize their legal and procurement processes. Competitive dynamics are intensifying as new entrants leverage cutting-edge AI technologies to challenge established players. This competition is driving continuous innovation, leading to the development of more specialized and feature-rich contract abstraction solutions tailored to specific industry needs. Market penetration is expanding rapidly across various sectors, including finance, healthcare, manufacturing, and technology, as organizations recognize the strategic advantage of automating contract data extraction and analysis. The increasing adoption of AI-powered legal technologies is a significant trend, pushing the boundaries of what is possible in contract management. Furthermore, the growing emphasis on data-driven decision-making within legal departments necessitates tools that can reliably extract and organize critical contract information. The market is also witnessing a trend towards broader application of these tools beyond core legal departments, extending to sales, procurement, and compliance teams, highlighting their cross-functional utility. The projected market size is estimated to reach over $5.8 billion by 2025, with significant expansion anticipated throughout the forecast period.

Leading Markets & Segments in Contract Abstraction Tool

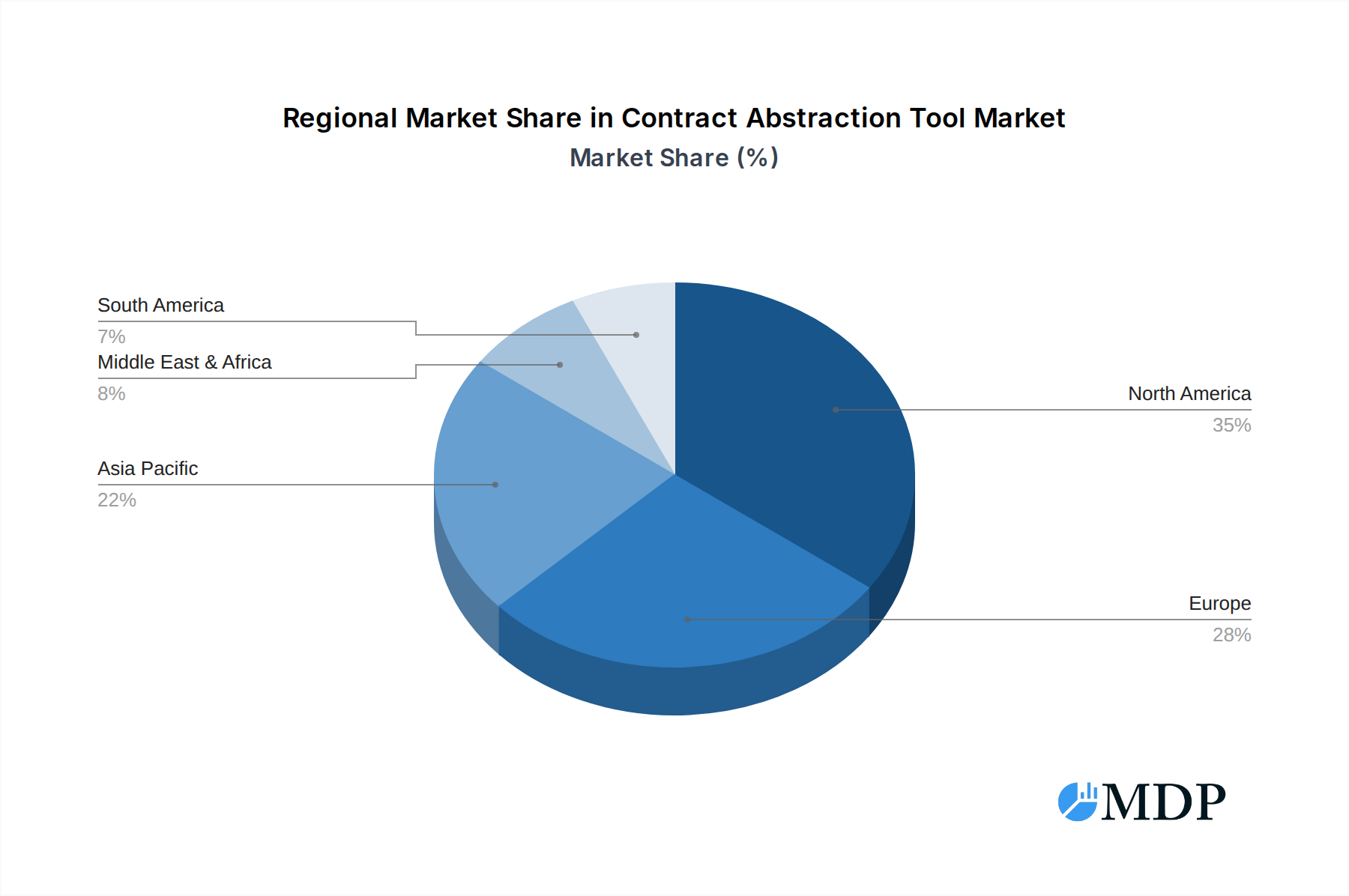

The global Contract Abstraction Tool market is experiencing significant growth and diversification, with North America emerging as the dominant region. This dominance is driven by a robust legal technology ecosystem, a high rate of enterprise adoption of digital solutions, and strong regulatory frameworks that encourage compliance and efficiency. Within North America, the United States leads due to its large enterprise market and a well-established legal services industry that actively seeks innovation.

Application Segments:

- Large Enterprises: This segment represents the largest share of the market.

- Key Drivers: High volume of contracts, complex legal requirements, significant financial stakes in contract management, and the need for advanced risk mitigation.

- Dominance Analysis: Large enterprises often have dedicated legal and procurement departments with the budget and resources to invest in sophisticated AI-powered contract abstraction tools. They benefit immensely from the time savings and error reduction that these tools provide, leading to significant cost efficiencies and improved compliance. The sheer scale of their operations necessitates robust solutions that can handle massive contract portfolios.

- SMEs (Small and Medium-sized Enterprises): This segment is exhibiting the fastest growth.

- Key Drivers: Increasing awareness of the benefits of contract automation, cost-effective cloud-based solutions, and the growing need for SMEs to compete on a level playing field with larger organizations.

- Dominance Analysis: As cloud-based contract abstraction tools become more accessible and affordable, SMEs are increasingly adopting them. These tools empower smaller businesses to manage their contracts more efficiently, reduce legal risks, and free up valuable resources that can be redirected to core business activities. The scalability of cloud solutions makes them particularly attractive for SMEs with fluctuating contract volumes.

Type Segments:

- Cloud Based: This segment is the fastest-growing and most dominant.

- Key Drivers: Scalability, flexibility, accessibility from anywhere, lower upfront costs, continuous updates, and ease of integration with other cloud-based business applications. Economic policies favoring digital infrastructure and the widespread availability of high-speed internet contribute to its growth.

- Dominance Analysis: The inherent advantages of cloud computing align perfectly with the needs of modern businesses. Cloud-based contract abstraction tools offer a cost-effective and agile solution for organizations of all sizes. They allow for rapid deployment and scaling, adapting to changing business needs without significant IT overhead.

- On-premises: This segment holds a smaller but stable market share.

- Key Drivers: Organizations with stringent data security and regulatory compliance requirements, particularly in highly regulated industries like finance and government, may prefer on-premises solutions for greater control over their data.

- Dominance Analysis: While the trend is towards cloud, on-premises solutions remain crucial for specific sectors where data sovereignty and strict security protocols are paramount. These solutions require significant upfront investment in hardware and IT infrastructure but offer unparalleled control and customization for organizations with these specific needs.

Contract Abstraction Tool Product Developments

Recent product developments in the contract abstraction tool market focus on enhancing AI capabilities for deeper analysis and broader application. Innovations include advanced NLP for understanding nuanced legal language, improved anomaly detection for identifying risky clauses, and seamless integration with broader contract lifecycle management (CLM) platforms. Competitive advantages are being carved out through specialized AI models tailored for specific industries, such as finance or healthcare, and by offering robust security features for sensitive data. The emphasis is on delivering intelligent automation that not only extracts data but also provides actionable insights, reducing manual review time by an estimated 70% and minimizing errors by approximately 95%. These advancements are crucial for meeting the evolving demands of legal and business professionals seeking efficiency and accuracy.

Key Drivers of Contract Abstraction Tool Growth

The growth of the contract abstraction tool market is propelled by several key factors. The rapid advancement and adoption of Artificial Intelligence (AI) and Machine Learning (ML) technologies are fundamental, enabling more accurate and efficient contract analysis. Increasing digital transformation initiatives across industries necessitate automated solutions for managing vast volumes of contracts. Furthermore, a growing awareness of the potential for significant cost savings and risk reduction through streamlined contract review processes is a major economic driver. Regulatory pressures and the need for enhanced compliance further bolster demand for sophisticated contract abstraction tools, ensuring adherence to legal standards and data privacy.

- Technological Advancements: AI, ML, and NLP for enhanced accuracy and insights.

- Digital Transformation: Enterprise-wide adoption of digital processes and automation.

- Cost Savings & Risk Reduction: Demonstrable ROI through efficiency and error minimization.

- Regulatory Compliance: Need for robust tools to meet legal and data privacy requirements.

Challenges in the Contract Abstraction Tool Market

Despite robust growth, the Contract Abstraction Tool market faces several challenges. High implementation costs and the perceived complexity of integrating new technologies can be barriers for some organizations, particularly SMEs. Resistance to change within legal departments, often accustomed to traditional manual processes, also presents a hurdle. Ensuring the accuracy and reliability of AI-driven abstraction, especially with highly complex or ambiguous contracts, remains an ongoing development area. Moreover, data security concerns, particularly for cloud-based solutions, require continuous investment in robust cybersecurity measures and compliance with evolving data privacy regulations. The competitive landscape also presents challenges, with a crowded market requiring vendors to constantly innovate to differentiate themselves and offer clear value propositions.

- Implementation Costs & Complexity: High upfront investment and integration challenges.

- Resistance to Change: Traditional reliance on manual contract review.

- AI Accuracy & Reliability: Ongoing development for complex and nuanced contracts.

- Data Security Concerns: Ensuring robust cybersecurity for cloud-based solutions.

- Market Saturation: Need for continuous innovation and differentiation.

Emerging Opportunities in Contract Abstraction Tool

Emerging opportunities in the Contract Abstraction Tool market are driven by technological breakthroughs and expanding application areas. The integration of advanced AI models, such as Generative AI, holds promise for more sophisticated contract drafting assistance and risk assessment. Strategic partnerships between contract abstraction tool providers and broader legal technology ecosystems, including e-discovery and compliance platforms, are creating comprehensive solution offerings. Furthermore, market expansion into emerging economies and specialized industry verticals with unique contract needs (e.g., intellectual property, real estate) presents significant growth potential. The growing demand for proactive contract management, moving beyond simple review to predictive analytics and strategic insights, is another key catalyst for long-term growth.

Leading Players in the Contract Abstraction Tool Sector

- Summize

- Parley Pro

- Brightleaf

- Onit, Inc

- HighIQ

- Avenir

- DocuSign

- Cenza

- IBM

- DealSumm

- Aavenir

- ContractPodAi

- Kira Systems

- LegalSifter

- Seal Software (DocuSign)

- LexCheck

- eBrevia

Key Milestones in Contract Abstraction Tool Industry

- 2019: Increased venture capital funding for AI-powered legal tech startups, driving innovation in contract abstraction.

- 2020: Wider adoption of remote work accelerated the demand for cloud-based legal solutions, including contract abstraction.

- 2021: Significant advancements in Natural Language Processing (NLP) capabilities enhanced the accuracy of AI-driven contract analysis.

- 2022: DocuSign's acquisition of Seal Software signaled market consolidation and the growing importance of advanced contract intelligence.

- 2023: Emergence of specialized AI models tailored for specific industry contracts, such as those in healthcare and finance.

- 2024: Greater focus on integrating contract abstraction tools with broader CLM platforms for end-to-end contract lifecycle management.

- 2025 (Estimated): Projected market value exceeding $5.8 billion, with continued strong CAGR.

- 2026-2033 (Forecast): Expected sustained growth driven by AI evolution, global digital transformation, and increasing regulatory demands.

Strategic Outlook for Contract Abstraction Tool Market

The strategic outlook for the Contract Abstraction Tool market is exceptionally positive, driven by the ongoing digital transformation and the indispensable role of efficient contract management. Growth accelerators include the continuous refinement of AI and ML algorithms, leading to more nuanced and predictive contract analytics. The expansion of cloud-based solutions will democratize access to these advanced tools, particularly for SMEs. Strategic opportunities lie in fostering deeper integrations with other enterprise software systems and developing specialized solutions for niche industries. The market will likely witness further consolidation as larger players seek to acquire innovative technologies and expand their offerings. A sustained focus on providing tangible ROI through enhanced efficiency, reduced risk, and improved compliance will be paramount for continued success.

Contract Abstraction Tool Segmentation

-

1. Application

- 1.1. Large Enterprises

- 1.2. SMEs

-

2. Type

- 2.1. Cloud Based

- 2.2. On-premises

Contract Abstraction Tool Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Contract Abstraction Tool Regional Market Share

Geographic Coverage of Contract Abstraction Tool

Contract Abstraction Tool REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.62% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Contract Abstraction Tool Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Large Enterprises

- 5.1.2. SMEs

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Cloud Based

- 5.2.2. On-premises

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Contract Abstraction Tool Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Large Enterprises

- 6.1.2. SMEs

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Cloud Based

- 6.2.2. On-premises

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Contract Abstraction Tool Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Large Enterprises

- 7.1.2. SMEs

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Cloud Based

- 7.2.2. On-premises

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Contract Abstraction Tool Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Large Enterprises

- 8.1.2. SMEs

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Cloud Based

- 8.2.2. On-premises

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Contract Abstraction Tool Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Large Enterprises

- 9.1.2. SMEs

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Cloud Based

- 9.2.2. On-premises

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Contract Abstraction Tool Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Large Enterprises

- 10.1.2. SMEs

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Cloud Based

- 10.2.2. On-premises

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Summize

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Parley Pro

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Brightleaf

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Onit Inc

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 HighIQ

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Avenir

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 DocuSign

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Cenza

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 IBM

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Cenza

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 DealSumm

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Aavenir

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 ContractPodAi

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Kira Systems

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 LegalSifter

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Seal Software (DocuSign)

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 LexCheck

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 eBrevia

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.1 Summize

List of Figures

- Figure 1: Global Contract Abstraction Tool Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Contract Abstraction Tool Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Contract Abstraction Tool Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Contract Abstraction Tool Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Contract Abstraction Tool Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Contract Abstraction Tool Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Contract Abstraction Tool Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Contract Abstraction Tool Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Contract Abstraction Tool Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Contract Abstraction Tool Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Contract Abstraction Tool Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Contract Abstraction Tool Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Contract Abstraction Tool Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Contract Abstraction Tool Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Contract Abstraction Tool Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Contract Abstraction Tool Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Contract Abstraction Tool Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Contract Abstraction Tool Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Contract Abstraction Tool Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Contract Abstraction Tool Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Contract Abstraction Tool Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Contract Abstraction Tool Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Contract Abstraction Tool Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Contract Abstraction Tool Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Contract Abstraction Tool Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Contract Abstraction Tool Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Contract Abstraction Tool Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Contract Abstraction Tool Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Contract Abstraction Tool Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Contract Abstraction Tool Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Contract Abstraction Tool Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Contract Abstraction Tool Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Contract Abstraction Tool Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Contract Abstraction Tool Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Contract Abstraction Tool Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Contract Abstraction Tool Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Contract Abstraction Tool Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Contract Abstraction Tool Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Contract Abstraction Tool Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Contract Abstraction Tool Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Contract Abstraction Tool Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Contract Abstraction Tool Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Contract Abstraction Tool Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Contract Abstraction Tool Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Contract Abstraction Tool Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Contract Abstraction Tool Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Contract Abstraction Tool Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Contract Abstraction Tool Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Contract Abstraction Tool Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Contract Abstraction Tool Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Contract Abstraction Tool?

The projected CAGR is approximately 10.62%.

2. Which companies are prominent players in the Contract Abstraction Tool?

Key companies in the market include Summize, Parley Pro, Brightleaf, Onit, Inc, HighIQ, Avenir, DocuSign, Cenza, IBM, Cenza, DealSumm, Aavenir, ContractPodAi, Kira Systems, LegalSifter, Seal Software (DocuSign), LexCheck, eBrevia.

3. What are the main segments of the Contract Abstraction Tool?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.99 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Contract Abstraction Tool," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Contract Abstraction Tool report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Contract Abstraction Tool?

To stay informed about further developments, trends, and reports in the Contract Abstraction Tool, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence