Key Insights into the Ceramic Solutions Market

The global Ceramic Solutions Market is poised for substantial growth, driven by escalating demand across diverse high-performance applications. Valued at $119.44 billion in 2025, the market is projected to expand at a Compound Annual Growth Rate (CAGR) of 3.6% through 2032, reaching an estimated $153.29 billion. This growth trajectory is underpinned by the indispensable role ceramic solutions play in modern industrial and technological advancement, offering unparalleled properties such as high temperature stability, wear resistance, corrosion immunity, and electrical insulation.

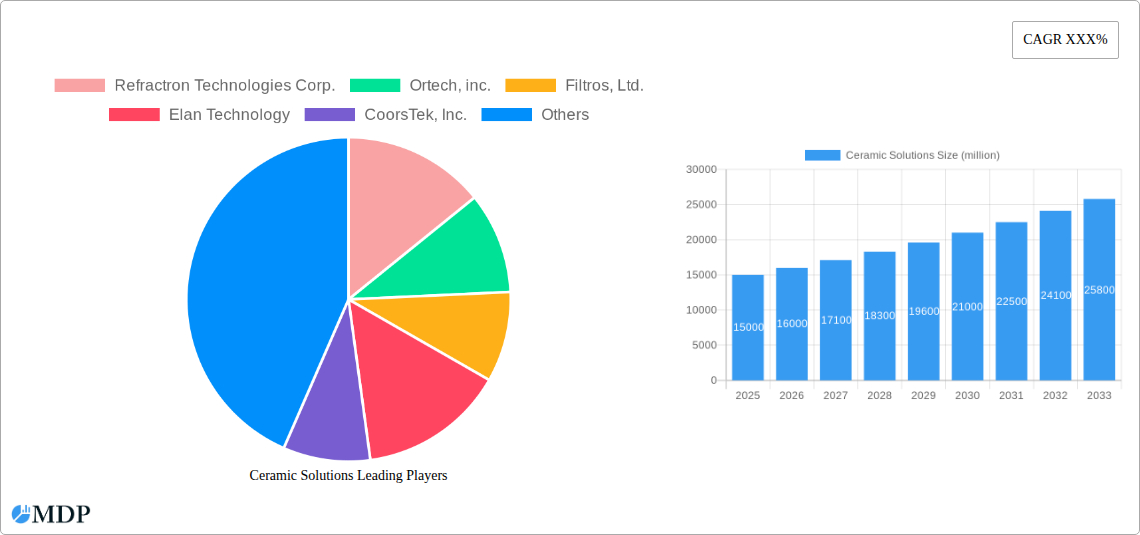

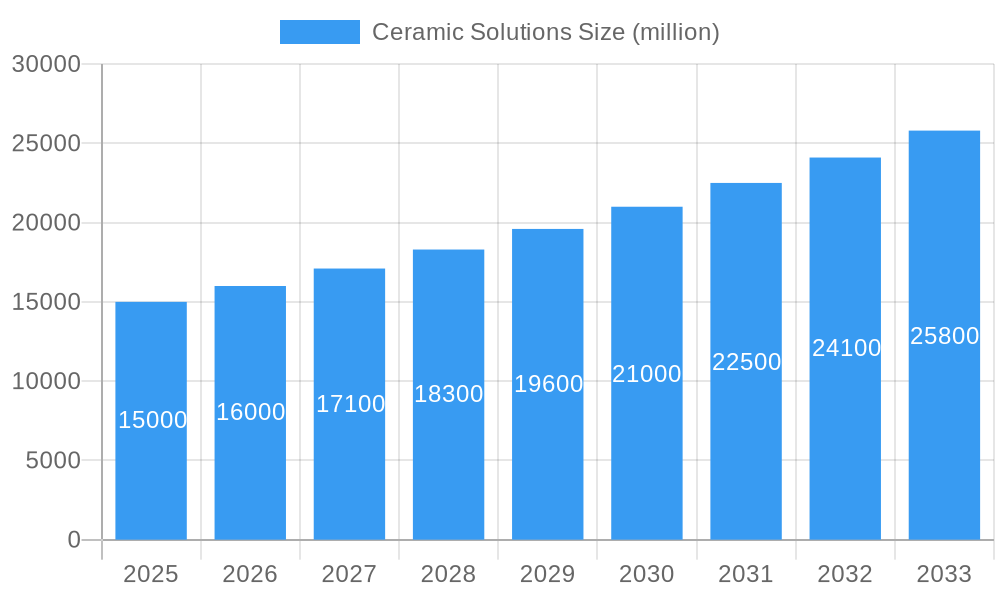

Ceramic Solutions Market Size (In Billion)

Key demand drivers include the rapid expansion of the Electronics & Semiconductors Market, where advanced ceramics are crucial for substrates, packaging, and dielectric components in miniaturized devices, 5G infrastructure, and AI hardware. The Automotive Ceramics Market is also a significant contributor, with increasing adoption of ceramic components in electric vehicles (EVs) for thermal management, battery safety, and lightweighting, alongside traditional uses in engine and exhaust systems. Furthermore, the aerospace & defense sector leverages ceramic solutions for high-performance components in jet engines, missile systems, and thermal protection systems, particularly with the rise of Ceramic Matrix Composites Market applications. The burgeoning healthcare sector, requiring biocompatible and sterilization-resistant materials for medical implants and instrumentation, further fuels market expansion.

Ceramic Solutions Company Market Share

Macroeconomic tailwinds such as global urbanization, industrialization in emerging economies, and persistent innovation in advanced manufacturing techniques are creating new avenues for ceramic applications. The shift towards sustainable manufacturing and energy-efficient systems also champions ceramic solutions due to their durability and inertness. Despite facing challenges such as high production costs and processing complexities for certain advanced grades, the intrinsic advantages of ceramics in harsh operating environments ensure their sustained demand. The forward-looking outlook for the Ceramic Solutions Market remains robust, with continued R&D investments focusing on new material compositions, advanced processing techniques, and expanding functional capabilities to meet the evolving requirements of critical end-user industries globally.

Monolithic Ceramics Segment Dominance in Ceramic Solutions Market

The Monolithic Ceramics Market segment stands as the largest by revenue share within the broader Ceramic Solutions Market, exhibiting a dominant position owing to its foundational applications across virtually all end-user industries. Monolithic ceramics, defined by their uniform structure and composition, serve as the backbone for countless high-performance components that demand superior mechanical, thermal, and electrical properties. This segment's dominance is multifaceted, stemming from the versatility and established manufacturing processes associated with materials such as alumina, silicon carbide, and zirconia, which are crucial constituents. The extensive applications span from wear-resistant components in industrial machinery to insulating parts in electronics, and from biocompatible implants in medical devices to robust structural elements in aerospace. The sheer volume and breadth of use cases solidify its leading position.

In the Electronics & Semiconductors Market, monolithic ceramic substrates provide essential thermal management and electrical insulation for integrated circuits, power modules, and sensors, facilitating the miniaturization and enhanced performance of electronic devices. The Alumina Market, a key sub-segment of monolithic ceramics, thrives here due to its excellent dielectric properties and cost-effectiveness. Similarly, the Automotive Ceramics Market heavily relies on monolithic components for spark plugs, oxygen sensors, catalytic converter supports, and increasingly for thermal barriers and structural components in electric vehicle battery packs and fuel cells, where high strength-to-weight ratios and thermal shock resistance are paramount. The Silicon Carbide Market also plays a critical role in high-power electronics and automotive applications, particularly where extreme temperatures and corrosive environments are present.

Leading players such as Kyocera Corporation, CeramTec GmbH, and CoorsTek, LLC, significantly contribute to the Monolithic Ceramics Market's growth through continuous innovation in material formulation and processing techniques. These companies invest heavily in R&D to enhance properties like fracture toughness, fatigue resistance, and dimensional stability, addressing the increasing performance demands from industrial machinery, chemical processing, and energy sectors. The segment’s growth is further propelled by the increasing complexity of industrial processes requiring components that can withstand extreme conditions, thus driving demand within the Industrial Ceramics Market. While Ceramic Coatings Market and Ceramic Matrix Composites Market are gaining traction due to their specialized advantages, the foundational and widespread utility of monolithic ceramics ensures its continued dominance and steady market share expansion within the Ceramic Solutions Market, adapting and evolving with technological advancements to maintain its critical role.

Key Market Drivers in Ceramic Solutions Market

The Ceramic Solutions Market is primarily propelled by several critical demand drivers, each underpinned by specific industry requirements and technological advancements. A primary driver is the accelerating demand from the Electronics & Semiconductors Market. The rapid proliferation of 5G technology, artificial intelligence (AI), and the Internet of Things (IoT) necessitates high-performance ceramic substrates and packaging solutions offering superior dielectric strength, thermal conductivity, and mechanical stability. For instance, the transition to advanced packaging techniques in semiconductor manufacturing requires precision ceramic components to dissipate heat efficiently, enabling higher component density and processing speeds. The global semiconductor industry's projected growth, with investments consistently exceeding $100 billion annually in recent years, directly translates into increased consumption of advanced ceramic materials for next-generation devices.

Another significant impetus comes from the Automotive Ceramics Market, particularly driven by the global shift towards electric vehicles (EVs) and stringent emission regulations for internal combustion engine (ICE) vehicles. Ceramic components provide essential thermal management in EV battery systems and power electronics, contributing to battery safety and efficiency. Moreover, the lightweighting trend in automotive manufacturing favors ceramic composites over metals to reduce vehicle weight and improve fuel efficiency or extend EV range. The projected increase in EV adoption to over 30% of new car sales by 2030 will significantly boost demand for ceramic insulators, sensors, and structural components. In the case of ICE vehicles, ceramic filters and catalytic converters remain critical for compliance with Euro 7 or equivalent emission standards, reducing particulate matter and NOx emissions by over 90%.

The Aerospace & Defense Market also serves as a robust demand driver, particularly for Ceramic Matrix Composites Market materials, due to the need for components capable of operating under extreme temperatures and pressures. These materials are utilized in advanced jet engines, missile systems, and hypersonic vehicles, offering high strength-to-weight ratios and superior thermal shock resistance. Investments in next-generation aircraft and defense systems, with global aerospace R&D spending regularly surpassing $50 billion per annum, continually push the boundaries for advanced ceramic applications. Lastly, the Industrial Ceramics Market sees sustained demand for wear-resistant and corrosion-resistant ceramic solutions in demanding environments. Industries such as chemical processing, mining, and oil & gas rely on ceramic components (e.g., pumps, valves, bearings) that can withstand abrasive media and corrosive chemicals, extending equipment lifespan and reducing maintenance costs by up to 50% compared to traditional metal alloys.

Competitive Ecosystem of Ceramic Solutions Market

The Ceramic Solutions Market is characterized by a diverse competitive landscape, featuring established global players and specialized innovators. These companies continually engage in R&D, strategic partnerships, and capacity expansions to maintain their market positions and cater to evolving industry demands.

- CoorsTek, LLC: A global leader in engineered ceramics, offering a vast portfolio of advanced ceramic materials and solutions across industrial, medical, automotive, and semiconductor sectors. The company focuses on precision manufacturing and customization to meet specific client needs for high-performance applications.

- Ortech, Inc.: Specializes in high-performance ceramic components, providing custom solutions for industrial, aerospace, and defense applications. Ortech is known for its expertise in materials like alumina, zirconia, and silicon nitride, tailored for extreme environments.

- Kyocera Corporation: A diversified multinational ceramic manufacturer, prominent in the Ceramic Solutions Market for fine ceramics, electronic components, and cutting tools. Kyocera leverages its extensive material science expertise to innovate across various end-user industries, including the Electronics & Semiconductors Market.

- Morgan Advanced Materials PLC: A global engineering company offering advanced ceramic materials, insulating fibers, and specialty products for thermal management, electrical insulation, and structural applications. Their focus includes high-temperature solutions for aerospace and industrial furnaces.

- CeramTec GmbH: A leading international manufacturer of advanced ceramics, with a strong focus on high-performance components for medical technology, automotive, electronics, and mechanical engineering. CeramTec is recognized for its precision ceramic products and material innovations.

- Saint-Gobain S.A.: A French multinational company producing a wide range of materials, including high-performance ceramics for industrial applications, refractories, and abrasive products. Their ceramic solutions are integrated into sectors requiring extreme durability and temperature resistance.

- 3M Company: A diversified technology company that offers ceramic-based solutions through its advanced materials division, including ceramic fibers, micro-spheres, and high-performance coatings. 3M leverages its material science capabilities for various industrial and consumer applications.

- NGK Insulators, Ltd.: A Japanese company globally recognized for its ceramic products, particularly insulators for power transmission, as well as industrial ceramics, automotive components like DPFs, and medical ceramics. NGK is a key player in the Advanced Ceramics Market.

- SCHOTT AG: An international technology group specializing in specialty glass and glass-ceramics, providing advanced materials for industries such as household appliances, optics, electronics, and pharmaceuticals. Their ceramic-glass composites offer unique thermal and mechanical properties.

- Rauschert GmbH & Co. KG: A German family-owned company that manufactures technical ceramics, ceramic heating elements, and components for various industrial applications, including electrical insulation and thermal processes. They emphasize customized ceramic solutions.

- Ibiden Co., Ltd.: A Japanese company involved in electronics and ceramics, known for its printed circuit boards and ceramic substrates used in the Electronics & Semiconductors Market. Ibiden also produces ceramic filters for environmental applications.

- Refractron Technologies Corp.: Specializes in high-temperature refractories and advanced ceramic materials, primarily serving the aerospace, defense, and industrial furnace markets. They focus on materials designed for extreme thermal and corrosive environments.

- Filtros, Ltd.: A manufacturer of porous ceramic media used for filtration, diffusion, and fluidization in various industrial processes. Their products are critical for environmental control, chemical processing, and water treatment applications.

- Elan Technology: A supplier of technical ceramic components and materials, specializing in custom ceramic solutions for medical, electrical, and industrial applications. Elan focuses on precision molding and manufacturing of intricate ceramic parts.

- Blasch Precision Ceramics: Known for its custom-shaped refractories and advanced ceramic solutions for applications in metal processing, chemical processing, and power generation. Blasch utilizes unique casting processes for complex ceramic geometries.

- AdTech Ceramics Company: Specializes in aluminum nitride (AlN) ceramic packages and substrates, catering primarily to the microelectronics and high-power semiconductor industries. AdTech provides solutions for high thermal conductivity and electrical isolation.

Recent Developments & Milestones in Ceramic Solutions Market

The Ceramic Solutions Market is continually evolving, marked by strategic alliances, technological advancements, and capacity expansions aimed at meeting escalating industrial demands and exploring new application frontiers.

- February 2025: Kyocera Corporation announced the development of a new advanced ceramic material with enhanced thermal shock resistance, targeting applications in high-temperature industrial furnaces and aerospace components. This innovation aims to extend component lifespan by up to 15% in extreme thermal cycling environments.

- November 2024: Morgan Advanced Materials PLC expanded its manufacturing capacity for Ceramic Matrix Composites Market components at its facility in the UK. This $25 million investment is designed to meet the growing demand from the aerospace industry for lightweight, high-temperature-resistant parts in next-generation engines.

- August 2024: CoorsTek, LLC partnered with a leading semiconductor equipment manufacturer to develop specialized Alumina Market and Silicon Carbide Market components for advanced wafer processing tools. The collaboration focuses on improving process precision and reducing contamination in semiconductor fabrication, critical for the Electronics & Semiconductors Market.

- April 2024: CeramTec GmbH launched a new line of biocompatible zirconia ceramics specifically designed for dental implants and medical instrumentation. These products offer superior strength and aesthetic properties, aiming to capture a larger share of the growing healthcare ceramics sector.

- January 2024: Saint-Gobain S.A. acquired a specialized European producer of Ceramic Coatings Market for industrial wear protection applications. This acquisition, valued at $70 million, strengthens Saint-Gobain's portfolio in surface engineering and expands its market reach in industrial maintenance.

- October 2023: NGK Insulators, Ltd. announced a breakthrough in solid-state battery technology using ceramic electrolytes, demonstrating improved energy density and safety profiles for electric vehicle applications. This development is expected to have a long-term impact on the Automotive Ceramics Market.

- July 2023: 3M Company introduced an innovative ceramic fiber insulation for extreme temperature applications, targeting the energy and chemical processing industries. This new material offers up to 20% better thermal efficiency compared to previous generations, reducing energy consumption.

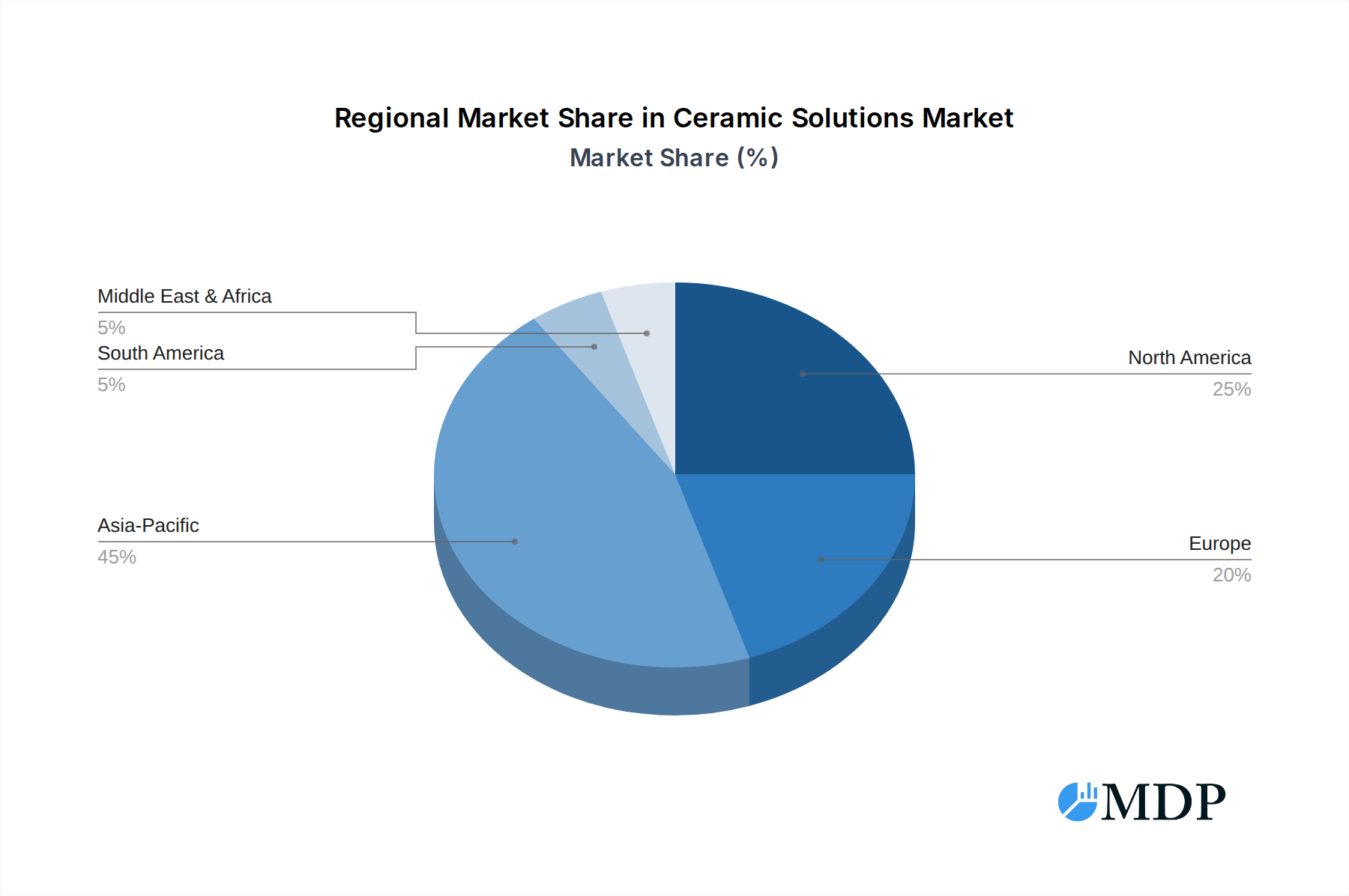

Regional Market Breakdown for Ceramic Solutions Market

The global Ceramic Solutions Market exhibits significant regional variations in terms of market share, growth dynamics, and primary demand drivers. Analyzing these regional landscapes is crucial for understanding the market's comprehensive development.

Asia Pacific currently dominates the Ceramic Solutions Market, holding an estimated 45-50% revenue share and projecting the highest CAGR of approximately 4.5%. This region's supremacy is attributed to its robust manufacturing base, particularly in China, Japan, South Korea, and India, which are major producers and consumers of advanced ceramics. The surging demand from the Electronics & Semiconductors Market, driven by rapid urbanization, technological advancements, and the presence of leading electronics manufacturers, is a key growth catalyst. Furthermore, the burgeoning automotive industry, particularly the Automotive Ceramics Market for EVs, and extensive infrastructure development in countries like China and India, significantly contribute to the region's ceramic consumption.

North America represents the second-largest market, accounting for an estimated 20-25% share, with a steady CAGR of around 3.0%. The region is characterized by a mature industrial landscape, strong R&D investments, and high adoption rates of advanced materials in critical sectors. The aerospace & defense industry is a significant consumer, utilizing high-performance ceramics for extreme environment applications. The expanding healthcare & medical sector, alongside the demand for wear-resistant components in the Industrial Ceramics Market, also fuels growth. The United States, with its strong innovation ecosystem and advanced manufacturing capabilities, leads this regional market.

Europe commands an estimated 18-22% share of the Ceramic Solutions Market, demonstrating a stable CAGR of approximately 2.8%. Countries like Germany, France, and the UK are at the forefront of advanced ceramic production and application. The region's stringent environmental regulations drive the adoption of ceramic filters and catalytic converters in the automotive sector. Additionally, the well-established industrial machinery, chemical, and energy sectors are significant users of corrosion-resistant and high-temperature Alumina Market and Silicon Carbide Market components, maintaining consistent demand for advanced ceramics.

The Middle East & Africa and South America collectively represent smaller but emerging markets, with CAGRs ranging from 3.8% to 4.2%. While their current market shares are modest, these regions are experiencing rapid industrialization, infrastructure development, and increased investments in oil & gas, mining, and manufacturing. These developments are gradually increasing the adoption of ceramic solutions, particularly for applications requiring wear and corrosion resistance in harsh operational environments. The rising focus on diversifying economies beyond natural resources also opens new opportunities for the Ceramic Solutions Market in these regions, making them areas of high future potential.

Ceramic Solutions Regional Market Share

Technology Innovation Trajectory in Ceramic Solutions Market

The Ceramic Solutions Market is undergoing a significant transformation driven by disruptive technological innovations that promise to redefine material capabilities and manufacturing paradigms. Among the most impactful emerging technologies are additive manufacturing, advanced sintering techniques, and the development of smart ceramics.

Additive Manufacturing (3D Printing) of Ceramics: This technology is revolutionizing the production of complex ceramic parts by enabling the creation of intricate geometries and customized designs that are impossible or cost-prohibitive with traditional methods. Techniques like stereolithography (SLA), binder jetting, and material extrusion are being adapted for ceramic powders, allowing for rapid prototyping and on-demand manufacturing. Adoption timelines are accelerating, particularly in aerospace, medical, and specialized industrial sectors where custom, high-performance components are critical. R&D investments are robust, focusing on developing new printable ceramic formulations and improving post-processing techniques (e.g., debinding and sintering) to achieve desired density and mechanical properties. This technology threatens incumbent business models reliant on economies of scale for simpler geometries but reinforces specialized manufacturers capable of high-value, bespoke solutions, especially for the Ceramic Matrix Composites Market.

Advanced Sintering Techniques: Innovations in sintering processes, such as Flash Sintering (FS) and Spark Plasma Sintering (SPS), are significantly impacting the Ceramic Solutions Market. These techniques use electric fields or pulsed currents to achieve rapid densification at lower temperatures and shorter durations compared to conventional methods. This not only reduces energy consumption by up to 70% but also helps retain fine grain structures, leading to enhanced mechanical properties like hardness and fracture toughness. SPS, for instance, allows for the consolidation of difficult-to-sinter materials and the creation of novel composites, including those utilizing Silicon Carbide Market components. Adoption is ongoing, particularly in high-value applications where material performance is paramount. R&D is focused on scaling these processes for industrial production and integrating them with advanced material development to yield superior Alumina Market and Zirconia Market products. These innovations reinforce incumbent players by enabling higher performance products and more efficient manufacturing.

Smart Ceramics and Functionalization: The trajectory of smart ceramics involves integrating sensing, actuating, and communication functionalities directly into ceramic materials. This includes developing piezoelectric ceramics for sensors and actuators, thermoelectric ceramics for energy harvesting, and magneto-electric ceramics for advanced electronic devices. The aim is to create 'active' ceramic components that can respond to environmental changes or perform specific functions within systems, addressing the needs of the Electronics & Semiconductors Market for integrated solutions. Adoption is in nascent stages for many applications but holds immense potential in fields like IoT, medical diagnostics, and structural health monitoring. R&D investments are high, involving interdisciplinary approaches combining material science, electronics, and data analytics. These technologies represent a significant reinforcement for incumbent players, allowing them to expand beyond traditional structural ceramics into higher-value functional markets and create new revenue streams within the Advanced Ceramics Market.

Sustainability & ESG Pressures on Ceramic Solutions Market

The Ceramic Solutions Market is increasingly subject to significant sustainability and ESG (Environmental, Social, and Governance) pressures, compelling manufacturers to re-evaluate their entire value chain from raw material sourcing to end-of-life management. These pressures are reshaping product development, procurement strategies, and operational practices, driving innovation towards more environmentally responsible and socially accountable solutions.

Circular Economy Mandates: There is a growing push for a circular economy model within the Ceramic Solutions Market, emphasizing the reduction, reuse, and recycling of ceramic waste. Traditional ceramic manufacturing can be energy-intensive and generate significant waste. Manufacturers are exploring methods to recycle ceramic off-cuts and spent materials back into the production cycle, reducing landfill burden and raw material consumption, particularly for materials from the Alumina Market and Zirconia Market. This involves developing new processing techniques that can effectively reprocess fired ceramics. Furthermore, product design is increasingly focused on designing for longevity and repairability, thereby extending the lifecycle of ceramic components, especially in high-value applications within the Industrial Ceramics Market.

Carbon Footprint Reduction: Achieving carbon neutrality and reducing greenhouse gas emissions is a critical ESG target. Ceramic production, particularly the high-temperature sintering processes, is energy-intensive. This has led to R&D efforts in more energy-efficient kilns, alternative energy sources (e.g., electric or hydrogen-powered furnaces), and advanced sintering techniques like flash sintering that reduce temperature and time requirements. Companies are also evaluating their scope 1, 2, and 3 emissions, seeking to decarbonize not only their direct operations but also their supply chains. This pressure influences material choices, favoring those that can be processed at lower temperatures or have a lower inherent carbon footprint.

Ethical Sourcing and Supply Chain Transparency: ESG criteria are increasingly scrutinizing the ethical and sustainable sourcing of raw materials. This includes ensuring that minerals like bauxite (for Alumina Market) or zircon (for Zirconia Market) are extracted responsibly, without contributing to deforestation, forced labor, or conflict. Companies in the Ceramic Solutions Market are implementing robust supply chain auditing and traceability systems to assure stakeholders of their commitment to ethical practices. This extends to labor standards and safety within manufacturing facilities, ensuring fair wages and safe working conditions. Such transparency is becoming a prerequisite for investment and procurement decisions, particularly from large multinational corporations and government contracts.

Environmental Regulations and Waste Management: Stricter environmental regulations concerning air emissions, wastewater discharge, and hazardous waste disposal are impacting ceramic manufacturers globally. This necessitates continuous investment in pollution control technologies and adherence to international standards. For instance, the production of Ceramic Coatings Market can involve chemical processes that require careful management of volatile organic compounds (VOCs). Companies are developing eco-friendly formulations and processes to minimize their environmental impact, ensuring compliance and enhancing their corporate reputation. These pressures are not merely regulatory burdens but are increasingly viewed as opportunities for innovation, driving the development of greener manufacturing processes and more sustainable ceramic products.

Ceramic Solutions Segmentation

-

1. Product Type

- 1.1. Monolithic Ceramics

- 1.2. Ceramic Coatings

- 1.3. Ceramic Matrix Composites

- 1.4. Ceramic Powders

-

2. Material Type

- 2.1. Alumina

- 2.2. Silicon Carbide

- 2.3. Zirconia

-

3. Application

- 3.1. Electrical Insulation

- 3.2. Thermal Barrier

- 3.3. Wear Resistance

- 3.4. Corrosion Resistance

- 3.5. Others

-

4. End User Industry

- 4.1. Electronics & Semiconductors

- 4.2. Automotive

- 4.3. Healthcare & Medical

- 4.4. Industrial & Machinery

- 4.5. Aerospace & Defense

- 4.6. Chemical & Petrochemical

- 4.7. Others

-

5. Sales Channel

- 5.1. Direct Sales

- 5.2. Distributors & Wholesalers

- 5.3. Online

Ceramic Solutions Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ceramic Solutions Regional Market Share

Geographic Coverage of Ceramic Solutions

Ceramic Solutions REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Monolithic Ceramics

- 5.1.2. Ceramic Coatings

- 5.1.3. Ceramic Matrix Composites

- 5.1.4. Ceramic Powders

- 5.2. Market Analysis, Insights and Forecast - by Material Type

- 5.2.1. Alumina

- 5.2.2. Silicon Carbide

- 5.2.3. Zirconia

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Electrical Insulation

- 5.3.2. Thermal Barrier

- 5.3.3. Wear Resistance

- 5.3.4. Corrosion Resistance

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by End User Industry

- 5.4.1. Electronics & Semiconductors

- 5.4.2. Automotive

- 5.4.3. Healthcare & Medical

- 5.4.4. Industrial & Machinery

- 5.4.5. Aerospace & Defense

- 5.4.6. Chemical & Petrochemical

- 5.4.7. Others

- 5.5. Market Analysis, Insights and Forecast - by Sales Channel

- 5.5.1. Direct Sales

- 5.5.2. Distributors & Wholesalers

- 5.5.3. Online

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. South America

- 5.6.3. Europe

- 5.6.4. Middle East & Africa

- 5.6.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Ceramic Solutions Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Monolithic Ceramics

- 6.1.2. Ceramic Coatings

- 6.1.3. Ceramic Matrix Composites

- 6.1.4. Ceramic Powders

- 6.2. Market Analysis, Insights and Forecast - by Material Type

- 6.2.1. Alumina

- 6.2.2. Silicon Carbide

- 6.2.3. Zirconia

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Electrical Insulation

- 6.3.2. Thermal Barrier

- 6.3.3. Wear Resistance

- 6.3.4. Corrosion Resistance

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by End User Industry

- 6.4.1. Electronics & Semiconductors

- 6.4.2. Automotive

- 6.4.3. Healthcare & Medical

- 6.4.4. Industrial & Machinery

- 6.4.5. Aerospace & Defense

- 6.4.6. Chemical & Petrochemical

- 6.4.7. Others

- 6.5. Market Analysis, Insights and Forecast - by Sales Channel

- 6.5.1. Direct Sales

- 6.5.2. Distributors & Wholesalers

- 6.5.3. Online

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Ceramic Solutions Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Monolithic Ceramics

- 7.1.2. Ceramic Coatings

- 7.1.3. Ceramic Matrix Composites

- 7.1.4. Ceramic Powders

- 7.2. Market Analysis, Insights and Forecast - by Material Type

- 7.2.1. Alumina

- 7.2.2. Silicon Carbide

- 7.2.3. Zirconia

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Electrical Insulation

- 7.3.2. Thermal Barrier

- 7.3.3. Wear Resistance

- 7.3.4. Corrosion Resistance

- 7.3.5. Others

- 7.4. Market Analysis, Insights and Forecast - by End User Industry

- 7.4.1. Electronics & Semiconductors

- 7.4.2. Automotive

- 7.4.3. Healthcare & Medical

- 7.4.4. Industrial & Machinery

- 7.4.5. Aerospace & Defense

- 7.4.6. Chemical & Petrochemical

- 7.4.7. Others

- 7.5. Market Analysis, Insights and Forecast - by Sales Channel

- 7.5.1. Direct Sales

- 7.5.2. Distributors & Wholesalers

- 7.5.3. Online

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. South America Ceramic Solutions Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Monolithic Ceramics

- 8.1.2. Ceramic Coatings

- 8.1.3. Ceramic Matrix Composites

- 8.1.4. Ceramic Powders

- 8.2. Market Analysis, Insights and Forecast - by Material Type

- 8.2.1. Alumina

- 8.2.2. Silicon Carbide

- 8.2.3. Zirconia

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Electrical Insulation

- 8.3.2. Thermal Barrier

- 8.3.3. Wear Resistance

- 8.3.4. Corrosion Resistance

- 8.3.5. Others

- 8.4. Market Analysis, Insights and Forecast - by End User Industry

- 8.4.1. Electronics & Semiconductors

- 8.4.2. Automotive

- 8.4.3. Healthcare & Medical

- 8.4.4. Industrial & Machinery

- 8.4.5. Aerospace & Defense

- 8.4.6. Chemical & Petrochemical

- 8.4.7. Others

- 8.5. Market Analysis, Insights and Forecast - by Sales Channel

- 8.5.1. Direct Sales

- 8.5.2. Distributors & Wholesalers

- 8.5.3. Online

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Europe Ceramic Solutions Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Monolithic Ceramics

- 9.1.2. Ceramic Coatings

- 9.1.3. Ceramic Matrix Composites

- 9.1.4. Ceramic Powders

- 9.2. Market Analysis, Insights and Forecast - by Material Type

- 9.2.1. Alumina

- 9.2.2. Silicon Carbide

- 9.2.3. Zirconia

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Electrical Insulation

- 9.3.2. Thermal Barrier

- 9.3.3. Wear Resistance

- 9.3.4. Corrosion Resistance

- 9.3.5. Others

- 9.4. Market Analysis, Insights and Forecast - by End User Industry

- 9.4.1. Electronics & Semiconductors

- 9.4.2. Automotive

- 9.4.3. Healthcare & Medical

- 9.4.4. Industrial & Machinery

- 9.4.5. Aerospace & Defense

- 9.4.6. Chemical & Petrochemical

- 9.4.7. Others

- 9.5. Market Analysis, Insights and Forecast - by Sales Channel

- 9.5.1. Direct Sales

- 9.5.2. Distributors & Wholesalers

- 9.5.3. Online

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East & Africa Ceramic Solutions Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Monolithic Ceramics

- 10.1.2. Ceramic Coatings

- 10.1.3. Ceramic Matrix Composites

- 10.1.4. Ceramic Powders

- 10.2. Market Analysis, Insights and Forecast - by Material Type

- 10.2.1. Alumina

- 10.2.2. Silicon Carbide

- 10.2.3. Zirconia

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Electrical Insulation

- 10.3.2. Thermal Barrier

- 10.3.3. Wear Resistance

- 10.3.4. Corrosion Resistance

- 10.3.5. Others

- 10.4. Market Analysis, Insights and Forecast - by End User Industry

- 10.4.1. Electronics & Semiconductors

- 10.4.2. Automotive

- 10.4.3. Healthcare & Medical

- 10.4.4. Industrial & Machinery

- 10.4.5. Aerospace & Defense

- 10.4.6. Chemical & Petrochemical

- 10.4.7. Others

- 10.5. Market Analysis, Insights and Forecast - by Sales Channel

- 10.5.1. Direct Sales

- 10.5.2. Distributors & Wholesalers

- 10.5.3. Online

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Asia Pacific Ceramic Solutions Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Monolithic Ceramics

- 11.1.2. Ceramic Coatings

- 11.1.3. Ceramic Matrix Composites

- 11.1.4. Ceramic Powders

- 11.2. Market Analysis, Insights and Forecast - by Material Type

- 11.2.1. Alumina

- 11.2.2. Silicon Carbide

- 11.2.3. Zirconia

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Electrical Insulation

- 11.3.2. Thermal Barrier

- 11.3.3. Wear Resistance

- 11.3.4. Corrosion Resistance

- 11.3.5. Others

- 11.4. Market Analysis, Insights and Forecast - by End User Industry

- 11.4.1. Electronics & Semiconductors

- 11.4.2. Automotive

- 11.4.3. Healthcare & Medical

- 11.4.4. Industrial & Machinery

- 11.4.5. Aerospace & Defense

- 11.4.6. Chemical & Petrochemical

- 11.4.7. Others

- 11.5. Market Analysis, Insights and Forecast - by Sales Channel

- 11.5.1. Direct Sales

- 11.5.2. Distributors & Wholesalers

- 11.5.3. Online

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 CoorsTek LLC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Ortech Inc.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Kyocera Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Morgan Advanced Materials PLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 CeramTec GmbH

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Saint-Gobain S.A.

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 3M Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 NGK Insulators Ltd.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 SCHOTT AG

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Rauschert GmbH & Co. KG

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Ibiden Co. Ltd.

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Refractron Technologies Corp.

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Filtros Ltd.

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Elan Technology

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 CoorsTek Inc.

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Blasch Precision Ceramics

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 AdTech Ceramics Company

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Others

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.1 CoorsTek LLC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Ceramic Solutions Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Ceramic Solutions Revenue (billion), by Product Type 2025 & 2033

- Figure 3: North America Ceramic Solutions Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: North America Ceramic Solutions Revenue (billion), by Material Type 2025 & 2033

- Figure 5: North America Ceramic Solutions Revenue Share (%), by Material Type 2025 & 2033

- Figure 6: North America Ceramic Solutions Revenue (billion), by Application 2025 & 2033

- Figure 7: North America Ceramic Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 8: North America Ceramic Solutions Revenue (billion), by End User Industry 2025 & 2033

- Figure 9: North America Ceramic Solutions Revenue Share (%), by End User Industry 2025 & 2033

- Figure 10: North America Ceramic Solutions Revenue (billion), by Sales Channel 2025 & 2033

- Figure 11: North America Ceramic Solutions Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 12: North America Ceramic Solutions Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Ceramic Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Ceramic Solutions Revenue (billion), by Product Type 2025 & 2033

- Figure 15: South America Ceramic Solutions Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: South America Ceramic Solutions Revenue (billion), by Material Type 2025 & 2033

- Figure 17: South America Ceramic Solutions Revenue Share (%), by Material Type 2025 & 2033

- Figure 18: South America Ceramic Solutions Revenue (billion), by Application 2025 & 2033

- Figure 19: South America Ceramic Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 20: South America Ceramic Solutions Revenue (billion), by End User Industry 2025 & 2033

- Figure 21: South America Ceramic Solutions Revenue Share (%), by End User Industry 2025 & 2033

- Figure 22: South America Ceramic Solutions Revenue (billion), by Sales Channel 2025 & 2033

- Figure 23: South America Ceramic Solutions Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 24: South America Ceramic Solutions Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Ceramic Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Ceramic Solutions Revenue (billion), by Product Type 2025 & 2033

- Figure 27: Europe Ceramic Solutions Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Europe Ceramic Solutions Revenue (billion), by Material Type 2025 & 2033

- Figure 29: Europe Ceramic Solutions Revenue Share (%), by Material Type 2025 & 2033

- Figure 30: Europe Ceramic Solutions Revenue (billion), by Application 2025 & 2033

- Figure 31: Europe Ceramic Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 32: Europe Ceramic Solutions Revenue (billion), by End User Industry 2025 & 2033

- Figure 33: Europe Ceramic Solutions Revenue Share (%), by End User Industry 2025 & 2033

- Figure 34: Europe Ceramic Solutions Revenue (billion), by Sales Channel 2025 & 2033

- Figure 35: Europe Ceramic Solutions Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 36: Europe Ceramic Solutions Revenue (billion), by Country 2025 & 2033

- Figure 37: Europe Ceramic Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 38: Middle East & Africa Ceramic Solutions Revenue (billion), by Product Type 2025 & 2033

- Figure 39: Middle East & Africa Ceramic Solutions Revenue Share (%), by Product Type 2025 & 2033

- Figure 40: Middle East & Africa Ceramic Solutions Revenue (billion), by Material Type 2025 & 2033

- Figure 41: Middle East & Africa Ceramic Solutions Revenue Share (%), by Material Type 2025 & 2033

- Figure 42: Middle East & Africa Ceramic Solutions Revenue (billion), by Application 2025 & 2033

- Figure 43: Middle East & Africa Ceramic Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 44: Middle East & Africa Ceramic Solutions Revenue (billion), by End User Industry 2025 & 2033

- Figure 45: Middle East & Africa Ceramic Solutions Revenue Share (%), by End User Industry 2025 & 2033

- Figure 46: Middle East & Africa Ceramic Solutions Revenue (billion), by Sales Channel 2025 & 2033

- Figure 47: Middle East & Africa Ceramic Solutions Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 48: Middle East & Africa Ceramic Solutions Revenue (billion), by Country 2025 & 2033

- Figure 49: Middle East & Africa Ceramic Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Ceramic Solutions Revenue (billion), by Product Type 2025 & 2033

- Figure 51: Asia Pacific Ceramic Solutions Revenue Share (%), by Product Type 2025 & 2033

- Figure 52: Asia Pacific Ceramic Solutions Revenue (billion), by Material Type 2025 & 2033

- Figure 53: Asia Pacific Ceramic Solutions Revenue Share (%), by Material Type 2025 & 2033

- Figure 54: Asia Pacific Ceramic Solutions Revenue (billion), by Application 2025 & 2033

- Figure 55: Asia Pacific Ceramic Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 56: Asia Pacific Ceramic Solutions Revenue (billion), by End User Industry 2025 & 2033

- Figure 57: Asia Pacific Ceramic Solutions Revenue Share (%), by End User Industry 2025 & 2033

- Figure 58: Asia Pacific Ceramic Solutions Revenue (billion), by Sales Channel 2025 & 2033

- Figure 59: Asia Pacific Ceramic Solutions Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 60: Asia Pacific Ceramic Solutions Revenue (billion), by Country 2025 & 2033

- Figure 61: Asia Pacific Ceramic Solutions Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ceramic Solutions Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Global Ceramic Solutions Revenue billion Forecast, by Material Type 2020 & 2033

- Table 3: Global Ceramic Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Global Ceramic Solutions Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 5: Global Ceramic Solutions Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 6: Global Ceramic Solutions Revenue billion Forecast, by Region 2020 & 2033

- Table 7: Global Ceramic Solutions Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Global Ceramic Solutions Revenue billion Forecast, by Material Type 2020 & 2033

- Table 9: Global Ceramic Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 10: Global Ceramic Solutions Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 11: Global Ceramic Solutions Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 12: Global Ceramic Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 13: United States Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Canada Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Mexico Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Ceramic Solutions Revenue billion Forecast, by Product Type 2020 & 2033

- Table 17: Global Ceramic Solutions Revenue billion Forecast, by Material Type 2020 & 2033

- Table 18: Global Ceramic Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 19: Global Ceramic Solutions Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 20: Global Ceramic Solutions Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 21: Global Ceramic Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Brazil Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Argentina Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Rest of South America Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Global Ceramic Solutions Revenue billion Forecast, by Product Type 2020 & 2033

- Table 26: Global Ceramic Solutions Revenue billion Forecast, by Material Type 2020 & 2033

- Table 27: Global Ceramic Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 28: Global Ceramic Solutions Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 29: Global Ceramic Solutions Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 30: Global Ceramic Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 31: United Kingdom Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Germany Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: France Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Italy Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Spain Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Russia Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Benelux Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Nordics Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of Europe Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Global Ceramic Solutions Revenue billion Forecast, by Product Type 2020 & 2033

- Table 41: Global Ceramic Solutions Revenue billion Forecast, by Material Type 2020 & 2033

- Table 42: Global Ceramic Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 43: Global Ceramic Solutions Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 44: Global Ceramic Solutions Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 45: Global Ceramic Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 46: Turkey Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Israel Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: GCC Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 49: North Africa Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: South Africa Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 51: Rest of Middle East & Africa Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Global Ceramic Solutions Revenue billion Forecast, by Product Type 2020 & 2033

- Table 53: Global Ceramic Solutions Revenue billion Forecast, by Material Type 2020 & 2033

- Table 54: Global Ceramic Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 55: Global Ceramic Solutions Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 56: Global Ceramic Solutions Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 57: Global Ceramic Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 58: China Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 59: India Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: Japan Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 61: South Korea Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: ASEAN Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 63: Oceania Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Rest of Asia Pacific Ceramic Solutions Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ceramic Solutions?

The projected CAGR is approximately 3.6%.

2. Which companies are prominent players in the Ceramic Solutions?

Key companies in the market include CoorsTek, LLC, Ortech, Inc., Kyocera Corporation, Morgan Advanced Materials PLC, CeramTec GmbH, Saint-Gobain S.A., 3M Company, NGK Insulators, Ltd., SCHOTT AG, Rauschert GmbH & Co. KG, Ibiden Co., Ltd., Refractron Technologies Corp., Filtros, Ltd., Elan Technology, CoorsTek, Inc., Blasch Precision Ceramics, AdTech Ceramics Company, Others.

3. What are the main segments of the Ceramic Solutions?

The market segments include Product Type, Material Type, Application, End User Industry, Sales Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 119.44 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ceramic Solutions," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ceramic Solutions report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ceramic Solutions?

To stay informed about further developments, trends, and reports in the Ceramic Solutions, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence