Key Insights

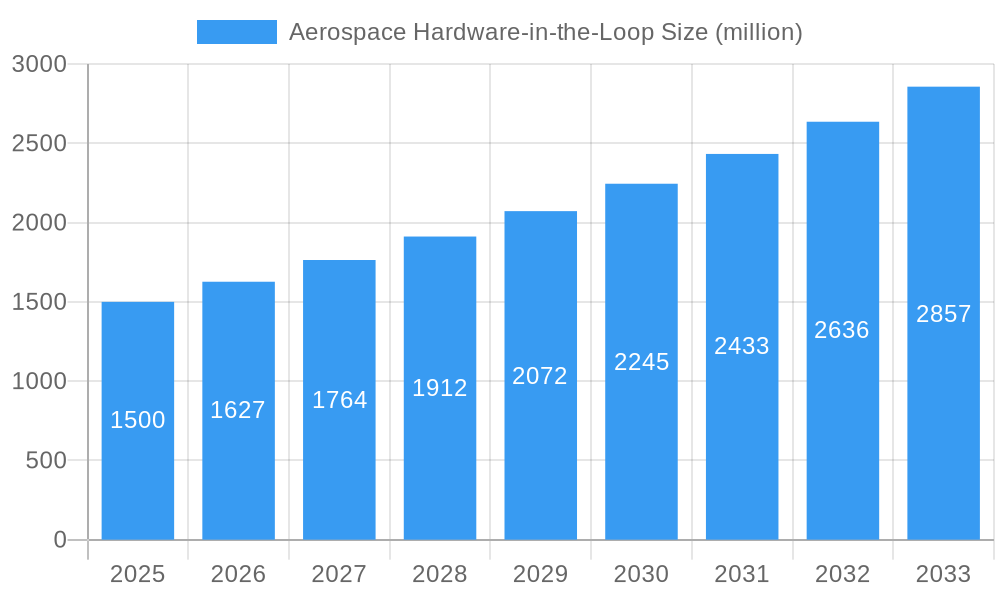

The Aerospace Hardware-in-the-Loop (HIL) market is experiencing substantial growth, fueled by the increasing complexity and rigorous testing demands of modern aerospace and space systems. With a current market size of 1.27 billion, the sector is projected to expand at a Compound Annual Growth Rate (CAGR) of 8.3% from 2025, reaching an estimated value of over 3 billion by the end of the forecast period. This expansion is primarily driven by the escalating need for advanced simulation technologies to validate critical flight control, avionics, and propulsion systems. Continuous innovation in commercial aviation, defense platforms, and the burgeoning commercial space sector directly correlates with a heightened demand for sophisticated HIL testing solutions. Furthermore, evolving regulatory frameworks and the imperative to reduce development costs and time-to-market are accelerating the adoption of these virtual testing environments. The "Others" application segment, encompassing areas like unmanned aerial vehicles (UAVs) and advanced aerospace research, is anticipated to show particularly robust growth.

Aerospace Hardware-in-the-Loop Market Size (In Billion)

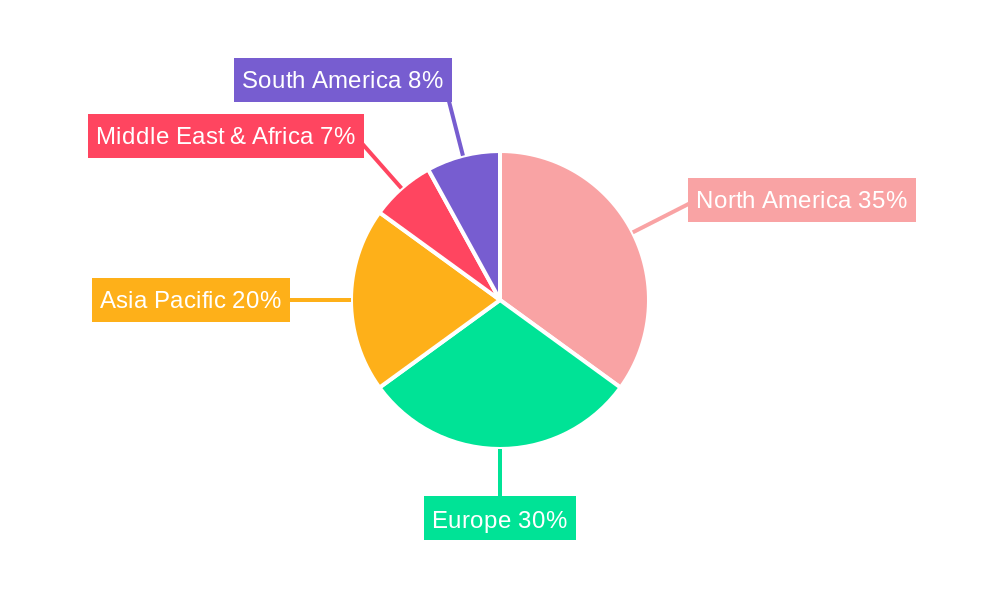

Key market segments include "Closed Loop HIL" and "Open Loop HIL" types, with closed-loop systems gaining traction due to their superior ability to deliver comprehensive and dynamic simulation. Leading companies such as DSPACE GmbH, National Instruments, and Opal-RT Technologies are at the forefront of innovation, providing advanced HIL solutions tailored to the aerospace sector's diverse needs. Geographically, North America and Europe currently lead the market, supported by established aerospace manufacturers and significant R&D investments. However, the Asia Pacific region, particularly China and India, is projected to exhibit the fastest growth, driven by its rapidly expanding aerospace industry and supportive government initiatives for indigenous defense and space capabilities. Market restraints include the substantial initial investment for sophisticated HIL systems and the requirement for specialized operational expertise.

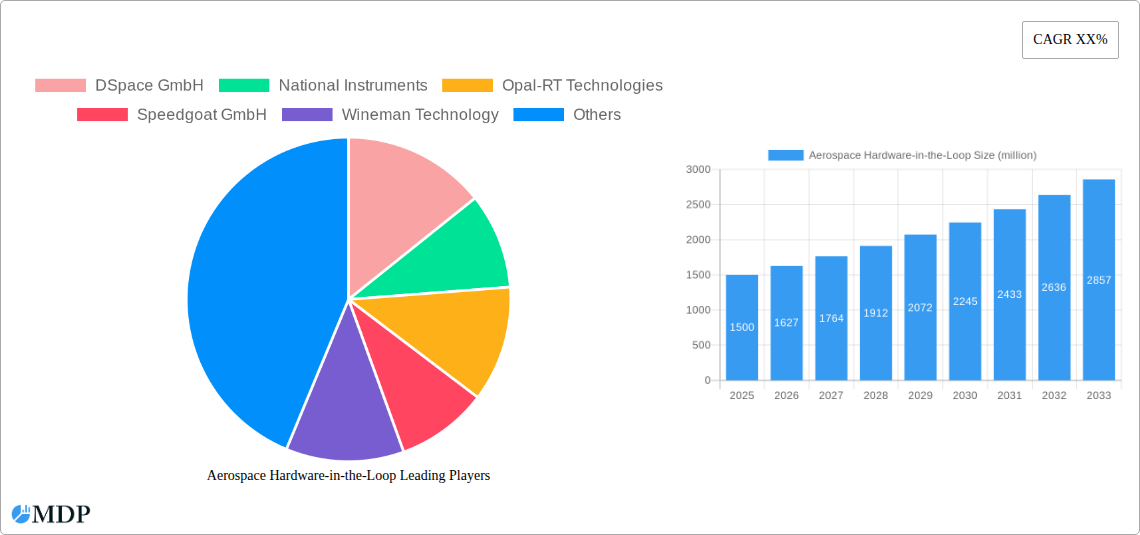

Aerospace Hardware-in-the-Loop Company Market Share

Aerospace Hardware-in-the-Loop Market Analysis: Trends, Drivers, and Forecasts

This comprehensive report provides in-depth insights into the dynamic Aerospace Hardware-in-the-Loop (HIL) market. Covering the period from 2019 to 2033, with a base year of 2025, this analysis offers unparalleled insights into market dynamics, industry trends, key segments, product innovations, growth drivers, challenges, emerging opportunities, leading players, and strategic outlooks. Understand how HIL technology is revolutionizing the testing and validation of critical aerospace systems, from next-generation aircraft and satellites to advanced military vehicles.

This report is essential for aerospace manufacturers, system integrators, HIL simulation providers, defense contractors, regulatory bodies, and investment firms seeking a detailed understanding of the market's trajectory. Optimized with high-traffic keywords such as "aerospace simulation," "hardware-in-the-loop testing," "avionics testing," "satellite testing," "military aerospace," and "flight control systems," this document maximizes search visibility for industry stakeholders.

Gain actionable intelligence on market share, CAGR, technological advancements, and competitive landscapes. Analyze the impact of key players like DSPACE GmbH, National Instruments, Opal-RT Technologies, Speedgoat GmbH, Wineman Technology, and Aegis Technologies in shaping the future of aerospace HIL. Whether your focus is on Closed Loop HIL or Open Loop HIL, this report delivers the data and analysis needed for informed strategic decisions and to capitalize on significant opportunities within this vital sector.

Aerospace Hardware-in-the-Loop Market Dynamics & Concentration

The Aerospace Hardware-in-the-Loop (HIL) market exhibits a moderate to high concentration, with a few key players dominating innovation and market share. DSPACE GmbH and National Instruments are prominent leaders, each holding estimated market shares in the range of 15-20% in recent years. The primary innovation drivers revolve around the increasing complexity of aerospace systems, the need for rigorous safety certification, and the demand for more efficient and cost-effective testing methodologies. Regulatory frameworks, particularly stringent airworthiness standards set by bodies like the FAA and EASA, are crucial in dictating the adoption and evolution of HIL technologies, pushing for greater fidelity and real-time simulation capabilities. Product substitutes, such as pure software simulation or bench testing, are gradually being displaced by the comprehensive validation offered by HIL. End-user trends highlight a growing preference for integrated testing solutions that encompass a wider range of system functionalities. Mergers and acquisitions (M&A) activity in the sector is moderate, with approximately 5-8 significant deals recorded annually over the historical period (2019-2024), often aimed at expanding technological portfolios or market reach. For instance, acquisitions of specialized simulation software companies by larger HIL providers have been notable.

Aerospace Hardware-in-the-Loop Industry Trends & Analysis

The Aerospace Hardware-in-the-Loop (HIL) industry is experiencing robust growth, driven by an escalating demand for advanced simulation and testing solutions across the aerospace and defense sectors. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033, reaching an estimated market size of over $5,000 million by the end of the forecast period. Key growth drivers include the increasing complexity of aircraft avionics, the continuous development of unmanned aerial vehicles (UAVs) and autonomous systems, and the rigorous safety and performance requirements for space missions. Technological disruptions are at the forefront, with advancements in real-time processing, high-fidelity modeling, sensor simulation, and the integration of artificial intelligence (AI) and machine learning (ML) into HIL platforms significantly enhancing their capabilities. Consumer preferences are shifting towards more comprehensive and integrated testing environments that can simulate a wider array of operational scenarios, including extreme environmental conditions and complex failure modes. Competitive dynamics are intense, with companies continually investing in R&D to offer more scalable, flexible, and accurate HIL systems. For example, the adoption of model-based systems engineering (MBSE) practices directly influences the design and implementation of HIL, requiring tighter integration between design and testing phases. Market penetration of advanced HIL solutions is steadily increasing, particularly within the commercial aviation and military segments, as organizations recognize the substantial cost and time savings associated with early and continuous testing. The development of highly realistic virtual environments and the simulation of electromagnetic interference (EMI) are also emerging trends that are shaping the industry.

Leading Markets & Segments in Aerospace Hardware-in-the-Loop

The Aircrafts segment is a dominant force within the Aerospace Hardware-in-the-Loop (HIL) market, projected to account for an estimated 45% of the total market value by 2030. This dominance is primarily fueled by the continuous demand for new aircraft development, stringent airworthiness certification processes, and the increasing complexity of modern avionics and flight control systems. North America, particularly the United States, leads as the dominant region, contributing over 35% of global market revenue, largely due to its extensive aerospace manufacturing base, significant defense spending, and advanced research and development capabilities. Within the types of HIL, Closed Loop HIL systems are witnessing higher adoption rates, accounting for an estimated 60% of the market share in 2025, owing to their ability to provide a fully interactive and validated testing environment for control systems. Key drivers for this dominance include:

- Economic Policies: Government investments in aerospace research and development, along with favorable tax incentives for aerospace manufacturers, particularly in North America and Europe, significantly boost demand.

- Infrastructure: The presence of world-class aerospace research facilities, testing centers, and a highly skilled workforce in leading regions supports the widespread adoption and advancement of HIL technology.

- Technological Advancements: The integration of advanced simulation techniques, real-time operating systems, and high-performance computing in Closed Loop HIL enables more accurate and comprehensive testing of complex aircraft systems.

- Regulatory Mandates: Stringent safety regulations for aircraft certification necessitate rigorous testing of flight control systems, making Closed Loop HIL an indispensable tool for compliance.

The Aerospace segment, encompassing commercial aviation and space applications, is also a significant contributor, with the Satellites application expected to show the highest growth rate, driven by the burgeoning commercial space industry and increased investment in satellite constellations. Military Vehicle applications are consistently strong due to ongoing modernization programs and the need for advanced simulation for combat systems.

Aerospace Hardware-in-the-Loop Product Developments

Product developments in the Aerospace Hardware-in-the-Loop (HIL) sector are characterized by a strong focus on enhancing simulation fidelity, real-time performance, and system integration capabilities. Companies are introducing advanced modular HIL platforms that allow for flexible configuration and scalability to meet diverse testing needs across Aircrafts, Aerospace, Satellites, and Military Vehicle applications. Innovations include sophisticated sensor simulation models, high-speed data acquisition systems, and the integration of advanced cyber-physical security testing within HIL environments. Competitive advantages are being gained through the development of open-architecture systems that facilitate easy integration with third-party software and hardware components. Furthermore, there is a growing trend towards cloud-based HIL solutions, enabling remote access and collaborative testing, thereby reducing deployment costs and improving accessibility for a wider range of industry stakeholders.

Key Drivers of Aerospace Hardware-in-the-Loop Growth

The growth of the Aerospace Hardware-in-the-Loop (HIL) market is primarily propelled by a confluence of technological advancements, economic factors, and regulatory mandates. Technologically, the increasing complexity of avionics, flight control systems, and communication networks in modern aircraft and spacecraft necessitates sophisticated validation methods. The demand for enhanced safety and reliability in aerospace systems, driven by stringent certification requirements from regulatory bodies like the FAA and EASA, is a critical economic driver. Furthermore, the drive for cost reduction and faster development cycles in the aerospace industry is pushing manufacturers towards more efficient testing methodologies like HIL. For example, the development of new generation fighter jets and commercial airliners relies heavily on HIL for early fault detection and system integration, significantly reducing the need for expensive and time-consuming physical prototypes and flight testing. The burgeoning commercial space sector, with its rapid satellite deployment, also contributes significantly to growth.

Challenges in the Aerospace Hardware-in-the-Loop Market

Despite its robust growth, the Aerospace Hardware-in-the-Loop (HIL) market faces several challenges that can impede its full potential. High initial investment costs for advanced HIL systems can be a significant barrier, particularly for smaller manufacturers or niche players, with initial setup costs potentially running into several million dollars. The complexity of integrating diverse hardware and software components from various suppliers requires specialized expertise, leading to potential integration challenges and extended development timelines. Furthermore, the evolving nature of aerospace technology means that HIL systems need continuous updates and recalibrations to remain effective, adding to the operational expenses. Stringent regulatory compliance requirements, while a driver of adoption, also present a challenge in terms of validation and certification of the HIL systems themselves. Lastly, a shortage of skilled personnel with expertise in both aerospace engineering and advanced simulation technologies can limit the widespread adoption and efficient utilization of HIL solutions.

Emerging Opportunities in Aerospace Hardware-in-the-Loop

The Aerospace Hardware-in-the-Loop (HIL) market is ripe with emerging opportunities that are set to catalyze long-term growth. A significant catalyst is the increasing adoption of Artificial Intelligence (AI) and Machine Learning (ML) in aerospace systems, which necessitates the development of advanced HIL environments capable of testing AI-driven decision-making and control algorithms. Strategic partnerships between HIL providers and AI technology firms are creating new avenues for innovation. Furthermore, the growing demand for autonomous systems, including drones and unmanned aerial vehicles (UAVs), is creating a substantial market for specialized HIL solutions focused on validating autonomous navigation, control, and communication systems. Market expansion strategies are also focusing on emerging aerospace markets in Asia-Pacific and the Middle East, where significant investments in aerospace infrastructure and defense modernization are underway. The development of digital twin technology and its integration with HIL testing promises to offer even more comprehensive lifecycle management and predictive maintenance capabilities.

Leading Players in the Aerospace Hardware-in-the-Loop Sector

- DSPACE GmbH

- National Instruments

- Opal-RT Technologies

- Speedgoat GmbH

- Wineman Technology

- Aegis Technologies

Key Milestones in Aerospace Hardware-in-the-Loop Industry

- 2019: Increased adoption of real-time operating systems in HIL platforms, enhancing simulation accuracy for complex flight dynamics.

- 2020: National Instruments (NI) acquires a specialized avionics testing company, strengthening its portfolio for aircraft systems.

- 2021: Opal-RT Technologies launches a new generation of high-performance HIL simulators optimized for electric and hybrid-electric aircraft propulsion systems.

- 2022: DSPACE GmbH introduces advanced cyber-physical security testing capabilities within its HIL solutions for defense applications.

- 2023: Speedgoat GmbH partners with leading aerospace research institutions to develop next-generation HIL testing for satellite control systems.

- 2024: Wineman Technology expands its offerings to include integrated HIL solutions for advanced unmanned aerial vehicle (UAV) flight control and sensor fusion testing.

- 2024: Aegis Technologies announces a significant expansion of its manufacturing capacity to meet the growing demand for aerospace HIL components.

Strategic Outlook for Aerospace Hardware-in-the-Loop Market

The strategic outlook for the Aerospace Hardware-in-the-Loop (HIL) market remains exceptionally positive, driven by the continuous innovation and increasing integration of HIL technologies across the aerospace lifecycle. Future growth accelerators will largely stem from the convergence of advanced simulation technologies with emerging trends such as electric and autonomous flight, advanced air mobility (AAM), and space exploration. Companies that can offer highly scalable, adaptable, and interconnected HIL solutions, potentially leveraging cloud infrastructure and AI-driven analytics, are poised for significant market share gains. Strategic opportunities lie in developing tailored HIL solutions for specific niche applications, such as hypersonics testing or resilient space systems. Furthermore, fostering collaborations with software developers, sensor manufacturers, and end-users will be crucial for creating comprehensive and cutting-edge testing environments that address the evolving demands of the aerospace industry. The market is expected to witness further consolidation and specialization as companies seek to strengthen their technological offerings and expand their global footprint.

Aerospace Hardware-in-the-Loop Segmentation

-

1. Application

- 1.1. Aircrafts

- 1.2. Aerospace

- 1.3. Satellites

- 1.4. Military Vehicle

- 1.5. Others

-

2. Types

- 2.1. Closed Loop HIL

- 2.2. Open Loop HIL

Aerospace Hardware-in-the-Loop Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Aerospace Hardware-in-the-Loop Regional Market Share

Geographic Coverage of Aerospace Hardware-in-the-Loop

Aerospace Hardware-in-the-Loop REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Aerospace Hardware-in-the-Loop Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Aircrafts

- 5.1.2. Aerospace

- 5.1.3. Satellites

- 5.1.4. Military Vehicle

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Closed Loop HIL

- 5.2.2. Open Loop HIL

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Aerospace Hardware-in-the-Loop Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Aircrafts

- 6.1.2. Aerospace

- 6.1.3. Satellites

- 6.1.4. Military Vehicle

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Closed Loop HIL

- 6.2.2. Open Loop HIL

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Aerospace Hardware-in-the-Loop Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Aircrafts

- 7.1.2. Aerospace

- 7.1.3. Satellites

- 7.1.4. Military Vehicle

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Closed Loop HIL

- 7.2.2. Open Loop HIL

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Aerospace Hardware-in-the-Loop Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Aircrafts

- 8.1.2. Aerospace

- 8.1.3. Satellites

- 8.1.4. Military Vehicle

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Closed Loop HIL

- 8.2.2. Open Loop HIL

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Aerospace Hardware-in-the-Loop Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Aircrafts

- 9.1.2. Aerospace

- 9.1.3. Satellites

- 9.1.4. Military Vehicle

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Closed Loop HIL

- 9.2.2. Open Loop HIL

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Aerospace Hardware-in-the-Loop Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Aircrafts

- 10.1.2. Aerospace

- 10.1.3. Satellites

- 10.1.4. Military Vehicle

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Closed Loop HIL

- 10.2.2. Open Loop HIL

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 DSpace GmbH

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 National Instruments

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Opal-RT Technologies

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Speedgoat GmbH

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Wineman Technology

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Aegis Technologies

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.1 DSpace GmbH

List of Figures

- Figure 1: Global Aerospace Hardware-in-the-Loop Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Aerospace Hardware-in-the-Loop Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Aerospace Hardware-in-the-Loop Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Aerospace Hardware-in-the-Loop Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Aerospace Hardware-in-the-Loop Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Aerospace Hardware-in-the-Loop Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Aerospace Hardware-in-the-Loop Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Aerospace Hardware-in-the-Loop Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Aerospace Hardware-in-the-Loop Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Aerospace Hardware-in-the-Loop Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Aerospace Hardware-in-the-Loop Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Aerospace Hardware-in-the-Loop Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Aerospace Hardware-in-the-Loop Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Aerospace Hardware-in-the-Loop Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Aerospace Hardware-in-the-Loop Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Aerospace Hardware-in-the-Loop Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Aerospace Hardware-in-the-Loop Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Aerospace Hardware-in-the-Loop Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Aerospace Hardware-in-the-Loop Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Aerospace Hardware-in-the-Loop Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Aerospace Hardware-in-the-Loop Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Aerospace Hardware-in-the-Loop Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Aerospace Hardware-in-the-Loop Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Aerospace Hardware-in-the-Loop Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Aerospace Hardware-in-the-Loop Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Aerospace Hardware-in-the-Loop Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Aerospace Hardware-in-the-Loop Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Aerospace Hardware-in-the-Loop Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Aerospace Hardware-in-the-Loop Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Aerospace Hardware-in-the-Loop Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Aerospace Hardware-in-the-Loop Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Aerospace Hardware-in-the-Loop Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Aerospace Hardware-in-the-Loop Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aerospace Hardware-in-the-Loop?

The projected CAGR is approximately 8.3%.

2. Which companies are prominent players in the Aerospace Hardware-in-the-Loop?

Key companies in the market include DSpace GmbH, National Instruments, Opal-RT Technologies, Speedgoat GmbH, Wineman Technology, Aegis Technologies.

3. What are the main segments of the Aerospace Hardware-in-the-Loop?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.27 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aerospace Hardware-in-the-Loop," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aerospace Hardware-in-the-Loop report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aerospace Hardware-in-the-Loop?

To stay informed about further developments, trends, and reports in the Aerospace Hardware-in-the-Loop, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence