Key Insights

The prescription pet food market is experiencing robust growth, driven by increasing pet ownership, rising pet humanization, and a greater awareness of preventative healthcare among pet owners. The market's expansion is fueled by advancements in veterinary science leading to more specialized diets tailored to specific pet health conditions, such as allergies, diabetes, and kidney disease. This trend toward proactive health management, combined with a willingness to invest in premium pet care, significantly boosts demand for prescription pet food. Major players like Mars, Nestle Purina, and Hill's Pet Nutrition dominate the market, leveraging strong brand recognition and extensive distribution networks. However, smaller companies specializing in niche dietary needs are also gaining traction, catering to the growing demand for customized solutions. Competition is fierce, with companies focusing on product innovation, enhanced palatability, and strategic partnerships with veterinary clinics to increase market penetration. The market segmentation is likely driven by pet type (dogs and cats), specific health conditions, and dietary requirements (e.g., hypoallergenic, weight management). Regional variations exist, with developed markets like North America and Europe exhibiting higher per capita consumption compared to emerging economies. While pricing remains a potential restraint for some consumers, the overall market outlook is positive, projected to continue its growth trajectory over the next decade.

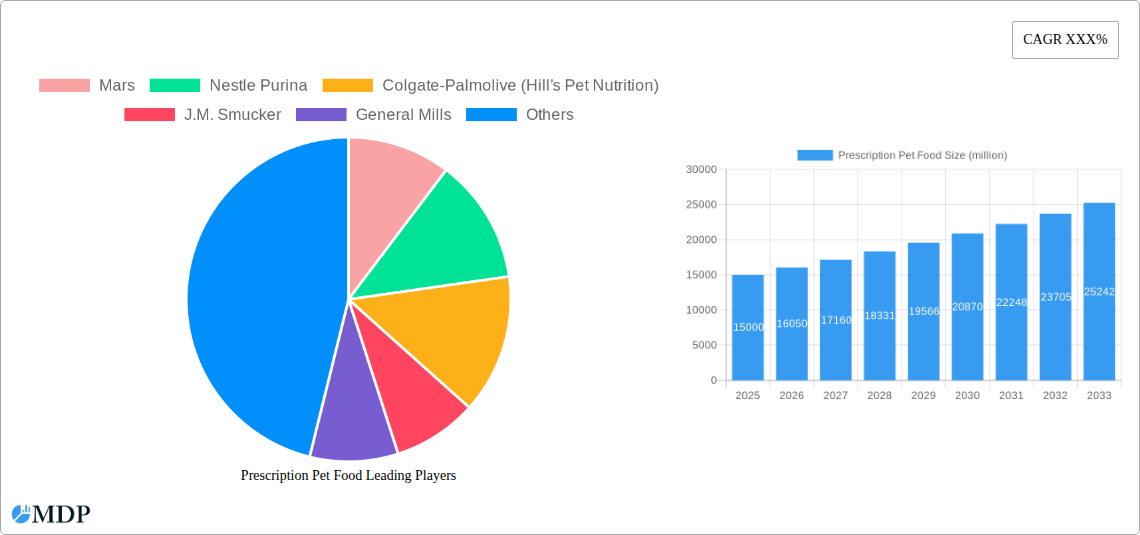

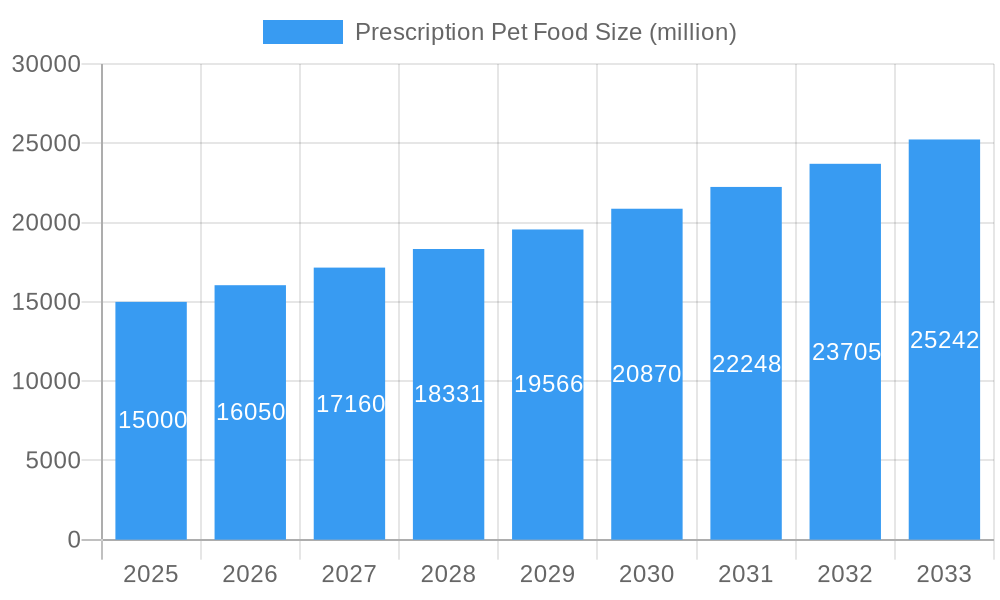

Prescription Pet Food Market Size (In Billion)

The forecast for the prescription pet food market indicates a sustained period of expansion, fueled by factors like increasing pet insurance coverage, which reduces the financial barrier to accessing premium pet food. Furthermore, the growing popularity of online pet food retailers and e-commerce platforms is streamlining access to these specialized diets. However, challenges remain, including the potential for increased regulatory scrutiny related to pet food labeling and ingredient sourcing. Manufacturers must prioritize transparency and uphold stringent quality control standards to maintain consumer trust. The market's future success hinges on innovation, meeting evolving consumer demands, and adapting to regulatory changes while upholding ethical sourcing practices. A focus on sustainable practices and environmentally responsible packaging is also likely to become increasingly important in attracting environmentally conscious pet owners.

Prescription Pet Food Company Market Share

Prescription Pet Food Market Report: 2019-2033 - A Comprehensive Analysis of a Multi-Billion Dollar Industry

This comprehensive report provides an in-depth analysis of the global prescription pet food market, projecting a market value exceeding $XX billion by 2033. The report covers the period 2019-2033, with a focus on the 2025-2033 forecast period and leverages data from the base year 2025. This detailed study is crucial for industry stakeholders, investors, and businesses seeking to navigate this rapidly evolving market. It offers actionable insights into market dynamics, competitive landscapes, and future growth opportunities.

Prescription Pet Food Market Dynamics & Concentration

The global prescription pet food market, valued at $XX billion in 2025, exhibits moderate concentration, with key players like Mars, Nestle Purina, and Colgate-Palmolive (Hill’s Pet Nutrition) holding significant market share. The market is driven by increasing pet ownership, rising pet healthcare spending, and growing awareness of the benefits of specialized nutrition for pets with specific health conditions. Regulatory frameworks concerning pet food safety and labeling play a crucial role, while product substitutes like home-cooked meals and generic prescription diets exert competitive pressure.

Key Market Dynamics:

- Market Share: Mars holds an estimated xx% market share, followed by Nestle Purina at xx% and Hill’s Pet Nutrition at xx%. Other players contribute to the remaining market share.

- M&A Activity: The historical period (2019-2024) witnessed approximately xx M&A deals, primarily focused on expanding product portfolios and geographical reach. The forecast period is expected to see a similar level of activity, driven by the desire to consolidate market share and gain access to innovative technologies.

- Innovation Drivers: Advancements in veterinary science and nutrition research are driving innovation in prescription pet food, leading to the development of specialized diets for various conditions like diabetes, allergies, and kidney disease.

- Regulatory Landscape: Stringent regulations regarding ingredient sourcing, labeling, and safety standards influence market dynamics, shaping product development and marketing strategies.

- End-User Trends: The growing humanization of pets and the increased willingness of pet owners to invest in their health contribute significantly to market growth.

Prescription Pet Food Industry Trends & Analysis

The prescription pet food market demonstrates robust growth, with a projected Compound Annual Growth Rate (CAGR) of xx% during 2025-2033. This expansion is fueled by several key factors: the rising prevalence of chronic diseases in pets, increased veterinary recommendations for specialized diets, and a shift toward preventative healthcare for companion animals. Technological advancements in pet food formulation and manufacturing processes further enhance product quality and efficiency. However, competitive intensity and price sensitivity remain significant challenges for market participants.

Key Trends:

- Market Growth Drivers: Increasing pet ownership, rising disposable incomes in developing economies, and an expanding middle class are all crucial drivers.

- Technological Disruptions: Precision nutrition technologies, personalized diet formulations based on genetic data, and improved palatability solutions are transforming the market.

- Consumer Preferences: Demand for natural, organic, and grain-free prescription diets is increasing. Transparency regarding ingredients and sourcing is also gaining importance.

- Competitive Dynamics: The market is characterized by intense competition, with major players focusing on product differentiation, brand building, and strategic partnerships to gain a competitive edge.

- Market Penetration: The market penetration of prescription pet food is expected to increase significantly over the forecast period, driven by rising awareness and availability.

Leading Markets & Segments in Prescription Pet Food

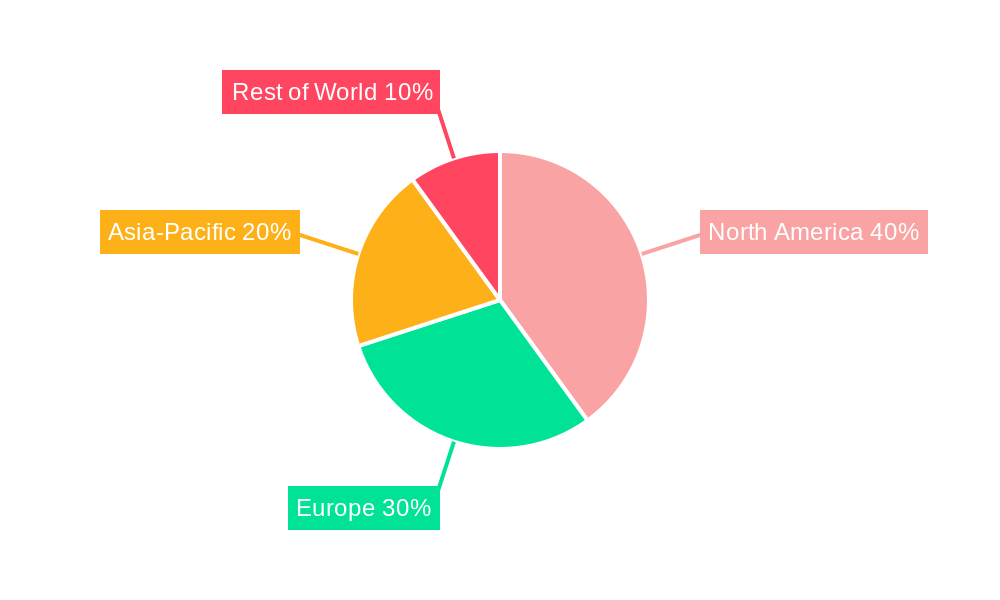

North America currently holds the dominant position in the global prescription pet food market, followed by Europe. This dominance is largely attributed to high pet ownership rates, advanced veterinary care infrastructure, and high per-capita pet spending. The dog food segment holds a larger market share compared to cat food, primarily due to the higher prevalence of dogs as companion animals.

Key Drivers:

- North America: High pet ownership, strong veterinary infrastructure, and significant disposable income levels drive market growth.

- Europe: Rising pet humanization trends and increasing awareness of pet health issues contribute to substantial market demand.

- Asia-Pacific: Rapidly growing pet ownership, increasing disposable incomes, and changing lifestyles are expected to fuel considerable market expansion.

Dominance Analysis: North America’s leading position stems from its advanced veterinary care infrastructure, high pet ownership rates and strong consumer spending. The high per capita income allows pet owners to invest more in premium pet products like prescription diets.

Prescription Pet Food Product Developments

Recent innovations in prescription pet food include the development of novel ingredients with improved digestibility and bioavailability, customized diet formulations catering to specific health needs, and technological advancements in food processing and packaging for extended shelf life and improved palatability. These innovations enhance the effectiveness and convenience of prescription pet foods, catering to the evolving demands of pet owners and veterinarians. The focus is on creating highly palatable and nutritious products tailored to address specific health issues, improving compliance and treatment outcomes.

Key Drivers of Prescription Pet Food Growth

Several factors contribute to the growth of the prescription pet food market. These include advancements in veterinary science leading to more effective treatment options for pet diseases, increased pet owner awareness about the importance of specialized nutrition, the rising humanization of pets and resulting increase in pet healthcare spending, and favorable regulatory environments supporting the development and marketing of specialized pet food products. Technological advances in pet food formulation and manufacturing further enhance product quality and availability.

Challenges in the Prescription Pet Food Market

The prescription pet food market faces certain challenges, including stringent regulatory hurdles for product approvals and labeling, supply chain disruptions due to global events and increased raw material costs, and intense competition among established players. These factors can increase the cost of production and hinder market expansion. Furthermore, price sensitivity among some pet owners can limit market penetration. The fluctuating prices of key ingredients also present a challenge, necessitating efficient cost management strategies.

Emerging Opportunities in Prescription Pet Food

The future of the prescription pet food market holds significant promise. Emerging opportunities include the development of personalized nutrition plans based on genetic testing and advanced data analytics. Strategic partnerships between pet food manufacturers and veterinary clinics can enhance market penetration and consumer reach. Expansion into emerging markets with a growing pet-owning population and increased disposable income offers further growth potential. Technological breakthroughs such as 3D printing and personalized food formulations will likely reshape the industry landscape.

Leading Players in the Prescription Pet Food Sector

- Mars

- Nestle Purina

- Colgate-Palmolive (Hill’s Pet Nutrition)

- J.M. Smucker

- General Mills

- Diamond Dog Foods

- Affinity Petcare (Agrolimen)

- Heristo

- Virbac

- Total Alimentos

- Spectrum Brands

- Nisshin Pet Food

- Champion Petfoods

- Unicharm

- Gambol

- Thai Union

- WellPet LLC

Key Milestones in Prescription Pet Food Industry

- 2020: Launch of several novel prescription diets addressing specific allergies and sensitivities.

- 2021: Increased focus on sustainable sourcing and environmentally friendly packaging.

- 2022: Significant investments in research and development to enhance product innovation and efficiency.

- 2023: Several major M&A deals aimed at expanding market share and product portfolios.

- 2024: Growing adoption of telehealth platforms for remote pet health consultations. Increased integration of data-driven personalized nutrition plans.

Strategic Outlook for Prescription Pet Food Market

The prescription pet food market is poised for significant growth in the coming years. Continued advancements in veterinary science and nutrition research, coupled with the increasing humanization of pets and rising pet healthcare expenditure, will drive market expansion. Strategic partnerships, technological innovations, and expansion into new markets will be key success factors. The focus on personalized nutrition and preventative health will further enhance market potential.

Prescription Pet Food Segmentation

-

1. Application

- 1.1. Dog

- 1.2. Cat

- 1.3. Others

-

2. Type

- 2.1. Weight Management

- 2.2. Digestive Care

- 2.3. Skin and Food Allergies

- 2.4. Kindney Care

- 2.5. Urinary Health

- 2.6. Liver Health

- 2.7. Diabetes

- 2.8. Illness and Surgery Recovery Support

- 2.9. Joint Support

- 2.10. Others

Prescription Pet Food Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Prescription Pet Food Regional Market Share

Geographic Coverage of Prescription Pet Food

Prescription Pet Food REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Prescription Pet Food Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Dog

- 5.1.2. Cat

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Weight Management

- 5.2.2. Digestive Care

- 5.2.3. Skin and Food Allergies

- 5.2.4. Kindney Care

- 5.2.5. Urinary Health

- 5.2.6. Liver Health

- 5.2.7. Diabetes

- 5.2.8. Illness and Surgery Recovery Support

- 5.2.9. Joint Support

- 5.2.10. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Prescription Pet Food Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Dog

- 6.1.2. Cat

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Weight Management

- 6.2.2. Digestive Care

- 6.2.3. Skin and Food Allergies

- 6.2.4. Kindney Care

- 6.2.5. Urinary Health

- 6.2.6. Liver Health

- 6.2.7. Diabetes

- 6.2.8. Illness and Surgery Recovery Support

- 6.2.9. Joint Support

- 6.2.10. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Prescription Pet Food Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Dog

- 7.1.2. Cat

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Weight Management

- 7.2.2. Digestive Care

- 7.2.3. Skin and Food Allergies

- 7.2.4. Kindney Care

- 7.2.5. Urinary Health

- 7.2.6. Liver Health

- 7.2.7. Diabetes

- 7.2.8. Illness and Surgery Recovery Support

- 7.2.9. Joint Support

- 7.2.10. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Prescription Pet Food Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Dog

- 8.1.2. Cat

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Weight Management

- 8.2.2. Digestive Care

- 8.2.3. Skin and Food Allergies

- 8.2.4. Kindney Care

- 8.2.5. Urinary Health

- 8.2.6. Liver Health

- 8.2.7. Diabetes

- 8.2.8. Illness and Surgery Recovery Support

- 8.2.9. Joint Support

- 8.2.10. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Prescription Pet Food Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Dog

- 9.1.2. Cat

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Weight Management

- 9.2.2. Digestive Care

- 9.2.3. Skin and Food Allergies

- 9.2.4. Kindney Care

- 9.2.5. Urinary Health

- 9.2.6. Liver Health

- 9.2.7. Diabetes

- 9.2.8. Illness and Surgery Recovery Support

- 9.2.9. Joint Support

- 9.2.10. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Prescription Pet Food Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Dog

- 10.1.2. Cat

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Weight Management

- 10.2.2. Digestive Care

- 10.2.3. Skin and Food Allergies

- 10.2.4. Kindney Care

- 10.2.5. Urinary Health

- 10.2.6. Liver Health

- 10.2.7. Diabetes

- 10.2.8. Illness and Surgery Recovery Support

- 10.2.9. Joint Support

- 10.2.10. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Mars

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Nestle Purina

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Colgate-Palmolive (Hill’s Pet Nutrition)

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 J.M. Smucker

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 General Mills

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Diamond Dog Foods

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Affinity Petcare (Agrolimen)

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Heristo

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Virbac

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Total Alimentos

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Spectrum Brands

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Nisshin Pet Food

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Champion Petfoods

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Unicharm

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Gambol

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Thai Union

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 WellPet LLC

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Mars

List of Figures

- Figure 1: Global Prescription Pet Food Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Prescription Pet Food Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Prescription Pet Food Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Prescription Pet Food Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Prescription Pet Food Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Prescription Pet Food Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Prescription Pet Food Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Prescription Pet Food Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Prescription Pet Food Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Prescription Pet Food Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Prescription Pet Food Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Prescription Pet Food Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Prescription Pet Food Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Prescription Pet Food Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Prescription Pet Food Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Prescription Pet Food Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Prescription Pet Food Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Prescription Pet Food Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Prescription Pet Food Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Prescription Pet Food Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Prescription Pet Food Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Prescription Pet Food Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Prescription Pet Food Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Prescription Pet Food Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Prescription Pet Food Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Prescription Pet Food Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Prescription Pet Food Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Prescription Pet Food Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Prescription Pet Food Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Prescription Pet Food Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Prescription Pet Food Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Prescription Pet Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Prescription Pet Food Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Prescription Pet Food Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Prescription Pet Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Prescription Pet Food Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Prescription Pet Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Prescription Pet Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Prescription Pet Food Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Prescription Pet Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Prescription Pet Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Prescription Pet Food Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Prescription Pet Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Prescription Pet Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Prescription Pet Food Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Prescription Pet Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Prescription Pet Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Prescription Pet Food Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Prescription Pet Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Prescription Pet Food Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Prescription Pet Food?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the Prescription Pet Food?

Key companies in the market include Mars, Nestle Purina, Colgate-Palmolive (Hill’s Pet Nutrition), J.M. Smucker, General Mills, Diamond Dog Foods, Affinity Petcare (Agrolimen), Heristo, Virbac, Total Alimentos, Spectrum Brands, Nisshin Pet Food, Champion Petfoods, Unicharm, Gambol, Thai Union, WellPet LLC.

3. What are the main segments of the Prescription Pet Food?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Prescription Pet Food," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Prescription Pet Food report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Prescription Pet Food?

To stay informed about further developments, trends, and reports in the Prescription Pet Food, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence