Key Insights

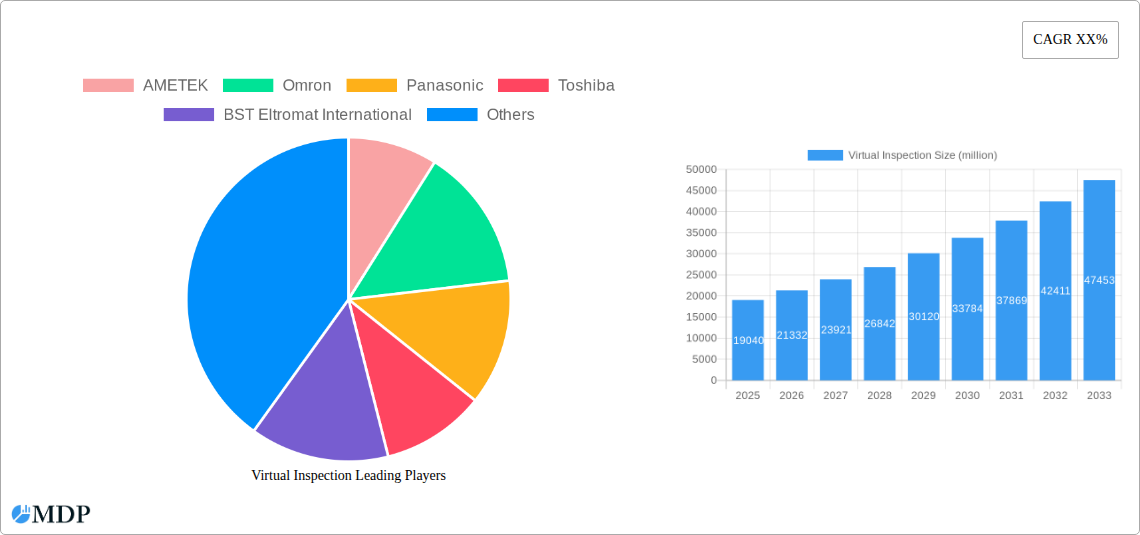

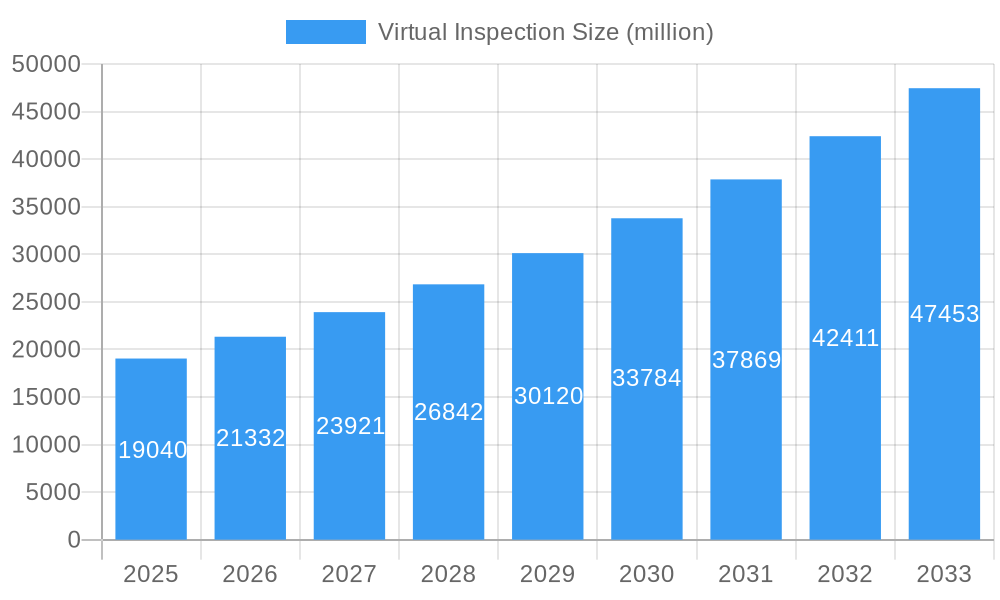

The global Virtual Inspection market is poised for significant expansion, projected to reach USD 19.04 billion in 2025. This growth is fueled by a robust Compound Annual Growth Rate (CAGR) of 11.8% over the forecast period of 2025-2033. The increasing demand for enhanced quality control, remote monitoring capabilities, and the integration of advanced technologies like AI and IoT are primary drivers. Industries such as pharmaceuticals, automotive, electronics, and oil and gas are increasingly adopting virtual inspection solutions to improve efficiency, reduce operational costs, and ensure compliance with stringent regulatory standards. The transition towards Industry 4.0 and smart manufacturing environments further accelerates this adoption, as businesses seek to optimize their production processes through real-time data analysis and automated inspection.

Virtual Inspection Market Size (In Billion)

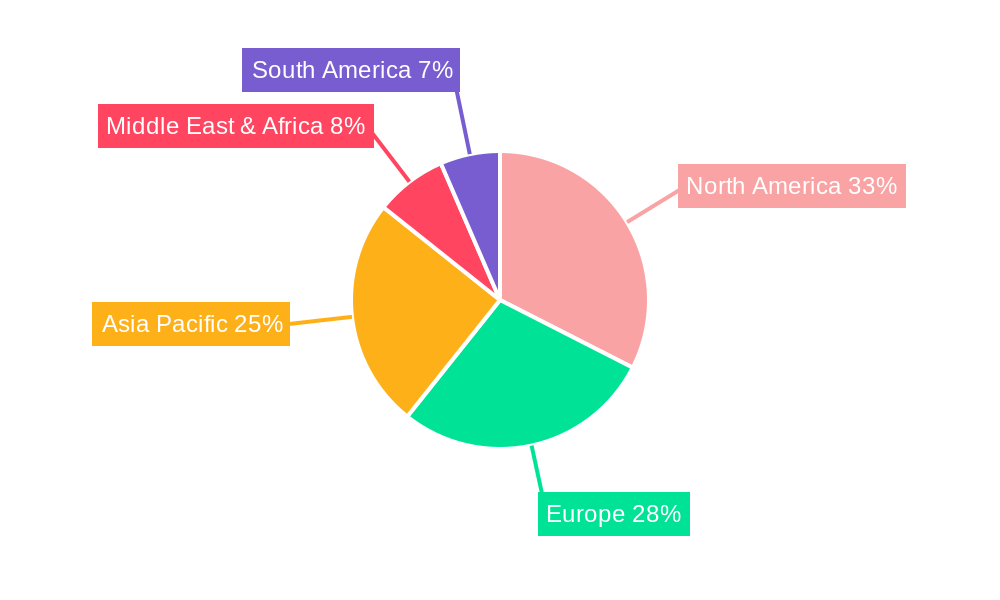

The market is characterized by a dynamic landscape with key players like AMETEK, Omron, Panasonic, and Toshiba innovating in both virtual inspection software and hardware. The virtual inspection software segment is expected to witness substantial growth due to advancements in image processing, machine learning algorithms for defect detection, and the development of user-friendly interfaces. Simultaneously, the hardware segment, encompassing high-resolution cameras, specialized sensors, and robust connectivity solutions, will see continuous innovation to support increasingly sophisticated inspection needs. Geographically, North America and Europe are anticipated to lead the market, driven by early adoption and strong R&D investments. However, the Asia Pacific region, particularly China and India, is expected to emerge as a high-growth area due to rapid industrialization and increasing investments in automation. The market's growth trajectory is also supported by the growing need for remote inspections, especially in hazardous environments or during challenging logistical situations, further solidifying the value proposition of virtual inspection technologies.

Virtual Inspection Company Market Share

Virtual Inspection Market Report: Harnessing Advanced Technologies for Enhanced Quality Control

This comprehensive report delves into the rapidly evolving Virtual Inspection market, a critical segment for industries prioritizing precision, efficiency, and compliance. The study meticulously analyzes market dynamics, industry trends, leading segments, product developments, growth drivers, challenges, emerging opportunities, key players, and significant milestones, providing actionable insights for stakeholders. Our analysis spans the Study Period: 2019–2033, with a Base Year: 2025, and an extensive Forecast Period: 2025–2033, building upon insights from the Historical Period: 2019–2024. The global virtual inspection market is projected to reach over USD 9.5 billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of approximately 12.5% during the forecast period.

Virtual Inspection Market Dynamics & Concentration

The Virtual Inspection market is characterized by a moderate to high concentration, driven by significant investments in research and development of advanced imaging and artificial intelligence technologies. Innovation drivers include the relentless pursuit of automated quality control, reduced manufacturing defects, and enhanced product safety across diverse sectors. Regulatory frameworks, particularly in pharmaceuticals and automotive, are increasingly mandating stringent quality standards, thereby pushing the adoption of virtual inspection solutions. Product substitutes, such as traditional manual inspection methods, are gradually being phased out due to their inherent inefficiencies and higher error rates. End-user trends are strongly leaning towards digital transformation initiatives and the implementation of Industry 4.0 principles, where virtual inspection plays a pivotal role. Mergers and acquisitions (M&A) activities are also significant, with an estimated over 40 M&A deals recorded during the historical period, indicating a consolidation trend as larger players acquire innovative smaller firms to expand their technology portfolios and market reach. Leading companies like AMETEK and Omron currently hold substantial market shares, estimated to be over 15% and 12% respectively, showcasing the competitive landscape.

Virtual Inspection Industry Trends & Analysis

The virtual inspection industry is experiencing a transformative growth trajectory fueled by several interconnected trends. A primary market growth driver is the escalating demand for superior product quality and reduced production costs across manufacturing sectors. Industries like Automotive, Electronics, and Pharmaceuticals are at the forefront, implementing virtual inspection to achieve zero-defect production goals. Technological disruptions, particularly in the realm of Artificial Intelligence (AI) and Machine Learning (ML), are revolutionizing virtual inspection capabilities. AI-powered algorithms can now perform complex defect detection, classification, and analysis with unparalleled accuracy and speed, far surpassing human capabilities. This technological advancement is a key contributor to the projected CAGR of 12.5%. Consumer preferences are also evolving, with a growing expectation for defect-free products, compelling manufacturers to invest in advanced quality assurance solutions. Competitive dynamics within the industry are intensifying, with companies continuously innovating to offer more sophisticated, user-friendly, and cost-effective virtual inspection systems. Market penetration for advanced virtual inspection solutions is estimated to reach over 60% in the high-tech manufacturing segment by 2030. The increasing integration of IoT devices and cloud computing further enhances data management and real-time analysis in virtual inspection, creating a connected and intelligent quality control ecosystem. The broader adoption of digital twins in manufacturing also necessitates robust virtual inspection capabilities for simulation and validation.

Leading Markets & Segments in Virtual Inspection

The Electronics segment stands as the dominant market within the virtual inspection landscape, driven by the intricate and miniaturized nature of electronic components requiring highly precise quality control. Within this segment, Automotive applications, particularly in the production of sensors, control units, and battery components for electric vehicles, represent a significant growth engine. Furthermore, the Pharmaceuticals sector is increasingly adopting virtual inspection for ensuring the sterility, integrity, and correct labeling of drugs and medical devices, propelled by stringent regulatory compliance.

Key Drivers for Dominance:

- Electronics:

- Miniaturization and Complexity: The relentless trend towards smaller and more complex electronic components necessitates sophisticated inspection techniques.

- High-Value Production: Defects in high-value electronics can lead to substantial financial losses, making advanced quality control a priority.

- Rapid Product Cycles: The need for rapid iteration and development in the electronics industry demands fast and efficient inspection processes.

- Automotive:

- Autonomous Driving Technology: The increasing reliance on complex sensor arrays and AI in autonomous vehicles demands exceptionally high standards for component quality.

- Electrification: The burgeoning electric vehicle market requires rigorous inspection of battery components and power electronics.

- Safety Regulations: Stringent automotive safety regulations mandate comprehensive quality assurance throughout the supply chain.

- Pharmaceuticals:

- Patient Safety: The paramount importance of patient safety drives the need for flawless drug manufacturing and packaging.

- Regulatory Compliance: Strict adherence to FDA, EMA, and other global regulatory standards necessitates robust and verifiable inspection processes.

- Counterfeit Prevention: Virtual inspection plays a crucial role in identifying and preventing counterfeit pharmaceuticals.

Virtual Inspection Software is emerging as a key growth segment, offering advanced algorithms for image analysis, defect detection, and data management. The estimated market size for virtual inspection software is projected to reach over USD 6.2 billion by 2033. Conversely, Virtual Inspection Hardware, encompassing high-resolution cameras, advanced lighting systems, and specialized sensors, continues to be essential, with its market size expected to exceed USD 3.3 billion by 2033. The interplay between sophisticated software and cutting-edge hardware is crucial for optimal virtual inspection performance.

Virtual Inspection Product Developments

Recent product developments in virtual inspection are characterized by the integration of AI and deep learning algorithms for enhanced defect detection accuracy and classification. Companies are focusing on developing compact, high-resolution imaging hardware and intelligent software platforms that offer real-time analysis and predictive maintenance insights. These innovations are designed to improve inspection speed, reduce false positives, and provide deeper insights into production processes. Key competitive advantages stem from enhanced automation, improved throughput, and the ability to inspect intricate and challenging geometries that were previously difficult to assess. The market is witnessing a surge in solutions tailored for specific industry needs, such as advanced metrology for aerospace or microbial detection for pharmaceuticals.

Key Drivers of Virtual Inspection Growth

The growth of the virtual inspection market is propelled by several powerful forces. Technologically, advancements in AI, machine learning, and high-resolution imaging are enabling more accurate and efficient defect detection. Economically, the rising cost of product recalls and the increasing demand for defect-free products are driving investment in quality control solutions. Regulatory mandates, especially in sensitive industries like pharmaceuticals and automotive, are crucial accelerators, enforcing higher quality standards. The broader adoption of Industry 4.0 principles and the need for operational efficiency also significantly contribute to the market's expansion. For example, the automotive sector's shift towards electric vehicles and autonomous driving systems necessitates a new level of component precision and reliability.

Challenges in the Virtual Inspection Market

Despite its strong growth trajectory, the virtual inspection market faces several challenges. High initial investment costs for sophisticated hardware and software can be a barrier for small and medium-sized enterprises. The need for specialized technical expertise to operate and maintain these advanced systems can also pose a challenge, leading to a skills gap. Data security and privacy concerns, especially with the increasing reliance on cloud-based solutions, require robust cybersecurity measures. Furthermore, the continuous need for software updates and recalibration to adapt to evolving product designs and manufacturing processes can add to the ongoing operational expenses. The integration of virtual inspection systems with existing legacy manufacturing infrastructure can also be complex and time-consuming, estimated to impact deployment timelines by up to 20%.

Emerging Opportunities in Virtual Inspection

Emerging opportunities in the virtual inspection market are vast and driven by continuous technological innovation and expanding application areas. The increasing adoption of the Internet of Things (IoT) is creating opportunities for smart, connected inspection systems that can monitor quality in real-time and transmit data to cloud platforms for advanced analytics. Strategic partnerships between AI developers and hardware manufacturers are leading to the creation of integrated, highly intelligent inspection solutions. Market expansion into emerging economies, coupled with government initiatives promoting advanced manufacturing, presents significant growth potential. Furthermore, the development of 3D virtual inspection and augmented reality (AR) applications for remote assistance and training opens new avenues for value creation. The growing demand for sustainable manufacturing practices also presents an opportunity for virtual inspection to reduce waste and material scrap.

Leading Players in the Virtual Inspection Sector

- AMETEK

- Omron

- Panasonic

- Toshiba

- BST Eltromat International

- Edmund Optics

- Elbit Vision Systems

- Electron Scientific Industries

- EPIC Systems

- IMS Systems

- ISRA Vision

- Jenoptik

- Konica Minolta

- Matrox Imaging

- Microscan Systems

- Verisk Analytics

Key Milestones in Virtual Inspection Industry

- 2019: Introduction of AI-powered defect recognition algorithms significantly improving accuracy in electronics inspection.

- 2020: Launch of cloud-based virtual inspection platforms enabling remote monitoring and data analysis, impacting over 500 companies globally.

- 2021: Major advancements in hyperspectral imaging for enhanced material analysis and defect detection in pharmaceuticals.

- 2022: Increased adoption of virtual inspection for battery quality control in the burgeoning electric vehicle market, contributing to over USD 2.1 billion in sector-specific investment.

- 2023: Development of end-to-end automated inspection solutions integrating machine vision with robotics, leading to a 15% increase in manufacturing efficiency for early adopters.

- 2024: Significant investments in deep learning models for predictive maintenance and anomaly detection in complex industrial settings, attracting over USD 1.5 billion in venture capital funding.

Strategic Outlook for Virtual Inspection Market

The strategic outlook for the virtual inspection market remains exceptionally positive, driven by an ongoing commitment to quality, efficiency, and innovation. Growth accelerators include the continued integration of AI and machine learning, the expansion of IoT connectivity, and the increasing demand for automated solutions across all manufacturing verticals. The market is poised for further expansion through the development of more sophisticated software capabilities and the creation of integrated hardware-software solutions. Strategic opportunities lie in targeting emerging industries such as advanced materials and renewable energy, as well as in penetrating underserved geographical markets. The focus on enhancing predictive capabilities and reducing downtime will further solidify virtual inspection's role as an indispensable tool for future manufacturing.

Virtual Inspection Segmentation

-

1. Application

- 1.1. Pharmaceuticals

- 1.2. Automotive

- 1.3. Electronics

- 1.4. Oil And Gas

- 1.5. Others

-

2. Types

- 2.1. Virtual Inspection Software

- 2.2. Virtual Inspection Hardware

Virtual Inspection Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Virtual Inspection Regional Market Share

Geographic Coverage of Virtual Inspection

Virtual Inspection REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Virtual Inspection Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pharmaceuticals

- 5.1.2. Automotive

- 5.1.3. Electronics

- 5.1.4. Oil And Gas

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Virtual Inspection Software

- 5.2.2. Virtual Inspection Hardware

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Virtual Inspection Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pharmaceuticals

- 6.1.2. Automotive

- 6.1.3. Electronics

- 6.1.4. Oil And Gas

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Virtual Inspection Software

- 6.2.2. Virtual Inspection Hardware

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Virtual Inspection Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pharmaceuticals

- 7.1.2. Automotive

- 7.1.3. Electronics

- 7.1.4. Oil And Gas

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Virtual Inspection Software

- 7.2.2. Virtual Inspection Hardware

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Virtual Inspection Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pharmaceuticals

- 8.1.2. Automotive

- 8.1.3. Electronics

- 8.1.4. Oil And Gas

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Virtual Inspection Software

- 8.2.2. Virtual Inspection Hardware

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Virtual Inspection Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pharmaceuticals

- 9.1.2. Automotive

- 9.1.3. Electronics

- 9.1.4. Oil And Gas

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Virtual Inspection Software

- 9.2.2. Virtual Inspection Hardware

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Virtual Inspection Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pharmaceuticals

- 10.1.2. Automotive

- 10.1.3. Electronics

- 10.1.4. Oil And Gas

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Virtual Inspection Software

- 10.2.2. Virtual Inspection Hardware

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 AMETEK

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Omron

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Panasonic

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Toshiba

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 BST Eltromat International

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Edmund Optics

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Elbit Vision Systems

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Electron Scientific industries

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 EPIC Systems

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 IMS Systems

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 ISRA Vision

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Jenoptik

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Konica Minolta

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Matrox Imaging

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Microscan Systems

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Verisk Analytics

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 AMETEK

List of Figures

- Figure 1: Global Virtual Inspection Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Virtual Inspection Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Virtual Inspection Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Virtual Inspection Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Virtual Inspection Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Virtual Inspection Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Virtual Inspection Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Virtual Inspection Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Virtual Inspection Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Virtual Inspection Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Virtual Inspection Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Virtual Inspection Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Virtual Inspection Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Virtual Inspection Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Virtual Inspection Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Virtual Inspection Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Virtual Inspection Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Virtual Inspection Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Virtual Inspection Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Virtual Inspection Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Virtual Inspection Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Virtual Inspection Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Virtual Inspection Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Virtual Inspection Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Virtual Inspection Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Virtual Inspection Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Virtual Inspection Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Virtual Inspection Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Virtual Inspection Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Virtual Inspection Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Virtual Inspection Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Virtual Inspection Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Virtual Inspection Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Virtual Inspection Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Virtual Inspection Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Virtual Inspection Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Virtual Inspection Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Virtual Inspection Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Virtual Inspection Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Virtual Inspection Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Virtual Inspection Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Virtual Inspection Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Virtual Inspection Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Virtual Inspection Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Virtual Inspection Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Virtual Inspection Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Virtual Inspection Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Virtual Inspection Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Virtual Inspection Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Virtual Inspection Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Virtual Inspection?

The projected CAGR is approximately 11.8%.

2. Which companies are prominent players in the Virtual Inspection?

Key companies in the market include AMETEK, Omron, Panasonic, Toshiba, BST Eltromat International, Edmund Optics, Elbit Vision Systems, Electron Scientific industries, EPIC Systems, IMS Systems, ISRA Vision, Jenoptik, Konica Minolta, Matrox Imaging, Microscan Systems, Verisk Analytics.

3. What are the main segments of the Virtual Inspection?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Virtual Inspection," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Virtual Inspection report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Virtual Inspection?

To stay informed about further developments, trends, and reports in the Virtual Inspection, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence