Key Insights

The global server microprocessor market is projected to reach a substantial XX million by 2033, expanding at a Compound Annual Growth Rate (CAGR) of 2.10% from 2019 to 2033. This steady growth is fueled by an increasing demand for robust and efficient computing power across various sectors, including consumer electronics, enterprise data centers, automotive, and industrial applications. The burgeoning adoption of cloud computing, artificial intelligence (AI), machine learning (ML), and big data analytics are primary drivers, necessitating higher-performance server microprocessors capable of handling complex workloads. Furthermore, the ongoing digital transformation initiatives across industries are bolstering the need for advanced server infrastructure, directly impacting the server microprocessor market. Innovations in chip architecture, such as the integration of specialized accelerators and improved power efficiency, are also contributing to market expansion. The automotive sector's increasing reliance on in-vehicle computing and autonomous driving technologies, along with the industrial internet of things (IIoT) and smart manufacturing, are opening new avenues for market growth.

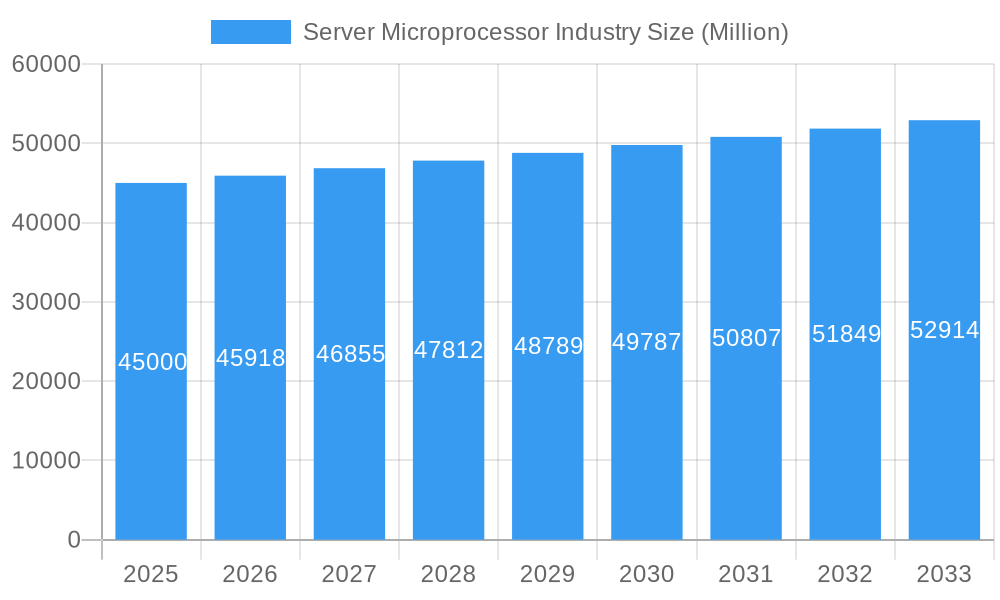

Server Microprocessor Industry Market Size (In Billion)

Despite the positive outlook, certain factors present challenges. The intense competition among established players and the evolving technological landscape require significant R&D investment, which can be a restraint for smaller entities. Supply chain disruptions and the increasing cost of raw materials for semiconductor manufacturing can also pose hurdles. However, the market is characterized by a strong trend towards heterogeneous computing, where specialized processors like GPUs and FPGAs are increasingly being integrated alongside traditional CPUs to optimize performance for specific tasks. This trend is particularly evident in high-performance computing (HPC) and AI workloads. The dominance of major manufacturers such as Intel, AMD, and Nvidia, alongside emerging players and foundries like TSMC, highlights the dynamic and competitive nature of this industry. Geographically, North America and Asia Pacific are expected to remain key markets due to the concentration of tech companies, cloud infrastructure providers, and a rapidly growing digital economy.

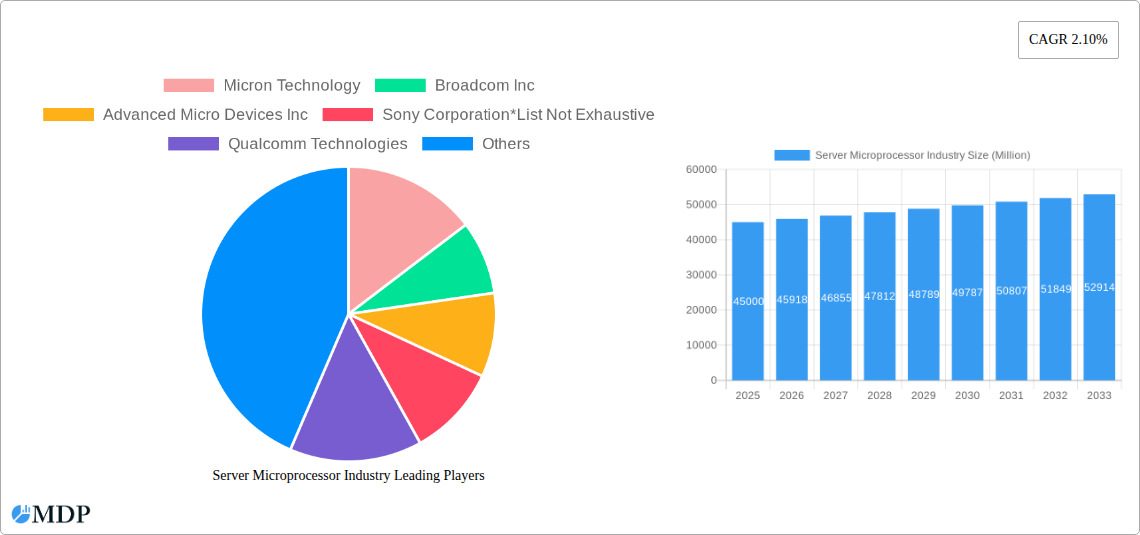

Server Microprocessor Industry Company Market Share

Unlock the Future of Computing: In-depth Server Microprocessor Industry Analysis (2019-2033)

Dive deep into the dynamic server microprocessor market with this comprehensive report. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this analysis provides critical insights into the forces shaping the server CPU market, enterprise server processors, and cloud computing processors. Essential for semiconductor manufacturers, data center operators, AI hardware providers, and technology investors, this report dissects the competitive landscape, identifies key growth drivers, and forecasts future trends. Explore the impact of RISC-V processors, ARM-based server CPUs, and innovations from industry giants like Intel, AMD, Nvidia, and Qualcomm.

Server Microprocessor Industry Market Dynamics & Concentration

The server microprocessor industry is characterized by a moderate to high concentration, with a few dominant players holding significant market share. Innovation drivers are primarily focused on increasing processing power, energy efficiency, and specialized functionalities for AI, cloud computing, and edge deployments. Regulatory frameworks, while generally favorable to technological advancement, can influence trade policies and domestic manufacturing initiatives. Product substitutes, such as specialized ASICs and FPGAs, offer competition in niche applications. End-user trends heavily favor enhanced performance for data-intensive workloads and cost-effective, scalable solutions for hyperscale data centers. Mergers and acquisition (M&A) activities, though not at an extremely high frequency, are strategic, often aimed at acquiring specific technologies or expanding market reach. For instance, recent M&A activities have focused on bolstering capabilities in areas like AI accelerators and advanced packaging. The market share distribution is dynamic, with historical data showing shifts influenced by technological breakthroughs and competitive strategies. The number of significant M&A deals within the past five years is estimated to be in the range of 5-10, signaling strategic consolidation and diversification.

Server Microprocessor Industry Industry Trends & Analysis

The server microprocessor industry is poised for substantial growth, driven by an insatiable demand for computing power across various sectors. The projected Compound Annual Growth Rate (CAGR) for the forecast period (2025–2033) is estimated at approximately 15%. This expansion is fueled by escalating digital transformation initiatives, the proliferation of big data analytics, the rapid advancements in Artificial Intelligence (AI) and Machine Learning (ML), and the continuous evolution of cloud computing infrastructure. The increasing adoption of ARM-based server processors and the growing interest in open-standard architectures like RISC-V are creating significant technological disruptions, challenging the traditional dominance of x86 architectures. Consumer preferences, while indirectly influencing the server market through demand for faster services, are less of a direct driver than the enterprise and hyperscale demands. Competitive dynamics are intensifying, with established players like Intel and AMD investing heavily in next-generation architectures, while companies like Nvidia are making significant inroads with their GPU-centric approach to accelerated computing. Qualcomm Technologies and Broadcom Inc. are also playing increasingly important roles, particularly in specialized server applications and networking. Market penetration of cloud-native processors is rapidly increasing, pushing the boundaries of performance per watt and total cost of ownership for data centers. The integration of AI accelerators directly into server CPUs is becoming a standard feature, catering to the burgeoning AI workloads.

Leading Markets & Segments in Server Microprocessor Industry

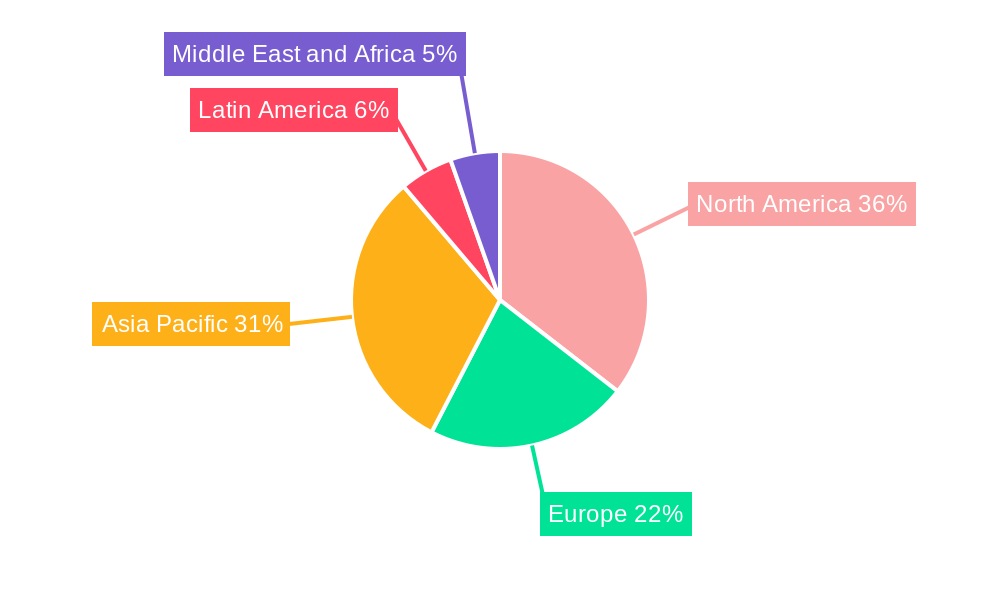

The Enterprise - Computer and Servers segment consistently dominates the server microprocessor market, accounting for an estimated 70% of the total market value. This dominance is driven by the critical role servers play in powering cloud infrastructure, enterprise data centers, and high-performance computing environments. Within this segment, CPUs remain the cornerstone, followed closely by GPUs for accelerated computing tasks. Geographically, North America currently leads the market due to its extensive cloud infrastructure, significant investments in AI research, and the presence of major technology companies.

- Dominant Segment: Enterprise - Computer and Servers

- Key Drivers:

- Exponential growth in data generation and the need for processing power.

- Widespread adoption of cloud services and hyperscale data centers.

- Increasing demand for AI and ML capabilities in enterprise applications.

- Server refresh cycles driven by performance and efficiency upgrades.

- Government initiatives supporting digital infrastructure development.

- Key Drivers:

- Dominant Region: North America

- Key Drivers:

- Concentration of major cloud providers and technology firms.

- Substantial R&D investments in AI and semiconductor technology.

- Robust economic policies favoring technological innovation.

- Advanced data center infrastructure and connectivity.

- Key Drivers:

The Consumer Electronics segment, though smaller in direct server microprocessor consumption, drives demand for underlying technologies that influence server evolution. The Automotive and Industrial segments are emerging as significant growth areas, particularly with the rise of autonomous vehicles and the Industrial Internet of Things (IIoT), requiring powerful and specialized edge server capabilities. The APU segment is gradually gaining traction as integrated solutions become more attractive for certain server configurations, while FPGAs continue to hold a strong position in specialized, high-throughput applications.

Server Microprocessor Industry Product Developments

Recent product developments in the server microprocessor industry are heavily focused on enhancing performance, power efficiency, and specialized capabilities. Innovations include the integration of AI accelerators directly into CPUs, advancements in chiplet architectures for greater modularity and customization, and the development of processors optimized for cloud-native workloads and edge computing. Companies are also prioritizing advanced packaging technologies to improve performance and reduce form factors. The competitive advantage for new products lies in their ability to deliver superior performance per watt, enhanced security features, and tailored solutions for specific applications like AI inference and data analytics, meeting the evolving market demands for faster, more efficient, and specialized computing.

Key Drivers of Server Microprocessor Industry Growth

The server microprocessor industry's growth is propelled by several interconnected factors. The relentless expansion of cloud computing and the burgeoning demand for hyperscale data centers represent a primary economic driver, necessitating more powerful and efficient server processors. Technological advancements, such as the development of AI and Machine Learning algorithms, directly increase the need for specialized server hardware capable of handling complex computations. Regulatory frameworks that encourage domestic chip manufacturing and innovation also play a crucial role, fostering a competitive environment. Furthermore, the increasing adoption of 5G technology and the Internet of Things (IoT) are creating new edge computing demands, driving the development of specialized microprocessors.

Challenges in the Server Microprocessor Industry Market

Despite robust growth, the server microprocessor industry faces significant challenges. Geopolitical tensions and trade disputes can disrupt global supply chains for essential raw materials and components, impacting production timelines and costs. The capital-intensive nature of semiconductor manufacturing, coupled with the long lead times for developing and launching new processors, poses financial barriers. Intense competition among established players and emerging entrants, particularly in the CPU and AI accelerator markets, can lead to price pressures and necessitate continuous, high-stakes R&D investments. The increasing complexity of chip design and manufacturing also presents technical hurdles. The estimated impact of supply chain disruptions on project timelines can range from 3-6 months, significantly affecting market availability.

Emerging Opportunities in Server Microprocessor Industry

The server microprocessor industry is ripe with emerging opportunities driven by transformative trends. The accelerating adoption of AI and Machine Learning across all industries presents a massive opportunity for specialized AI-accelerated server processors. The continued expansion of edge computing, fueled by IoT devices and 5G networks, creates a demand for low-power, high-performance microprocessors designed for distributed environments. Strategic partnerships between semiconductor manufacturers and cloud providers, as well as software developers, are crucial for co-optimizing hardware and software stacks, unlocking new performance benchmarks. Furthermore, the growing interest in open-source hardware architectures like RISC-V offers a pathway for increased innovation and reduced reliance on proprietary ecosystems, fostering a more competitive and diverse market.

Leading Players in the Server Microprocessor Industry Sector

- Micron Technology

- Broadcom Inc

- Advanced Micro Devices Inc

- Sony Corporation

- Qualcomm Technologies

- SK Hynix Inc

- Samsung Technologies

- Nvidia Corporation

- Taiwan Semiconductor Manufacturing Company Limited

- Intel Corporation

Key Milestones in Server Microprocessor Industry Industry

- November 2022: KIOXIA America, Inc. announced its collaboration with Ampere to qualify its CD6, CM6, and XD6 Series SSDs with platforms based on Ampere's Altra and Ampere Altra Max Cloud Native Processors. To address the demands of the modern cloud, Ampere has designed a server microprocessor architecture from the ground up. Its AArch64-based processors deliver performance, scalability, security, and power efficiency uniquely focused on today's hyperscale cloud and edge computing.

- April 2022: The Government of India announced the commencement of the Digital India RISC-V (DIR-V) program to secure commercial silicon and design victories for the next generations of microprocessors by December 2023. RISC-V is a public and transparent ISA that, via open standard cooperation, enables a new age of processor invention.

Strategic Outlook for Server Microprocessor Industry Market

The strategic outlook for the server microprocessor industry remains exceptionally strong, driven by sustained demand from cloud computing, AI, and the ever-expanding digital economy. Future growth will be accelerated by further integration of AI capabilities directly into server processors, the continued rise of ARM-based architectures offering compelling power and performance advantages, and the exploration of novel chiplet and heterogeneous computing designs. Companies that can effectively navigate supply chain complexities, invest strategically in cutting-edge R&D for specialized workloads, and forge strong partnerships across the ecosystem will be best positioned for long-term success. The increasing focus on energy efficiency and sustainability will also be a key differentiator, influencing product design and market adoption.

Server Microprocessor Industry Segmentation

-

1. Type

- 1.1. APU

- 1.2. CPU

- 1.3. GPU

- 1.4. FPGA

-

2. Application

- 2.1. Consumer Electronics

- 2.2. Enterprise - Computer and Servers

- 2.3. Automotive

- 2.4. Industrial

- 2.5. Other Applications

Server Microprocessor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Server Microprocessor Industry Regional Market Share

Geographic Coverage of Server Microprocessor Industry

Server Microprocessor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. APU

- 5.1.2. CPU

- 5.1.3. GPU

- 5.1.4. FPGA

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Consumer Electronics

- 5.2.2. Enterprise - Computer and Servers

- 5.2.3. Automotive

- 5.2.4. Industrial

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Server Microprocessor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. APU

- 6.1.2. CPU

- 6.1.3. GPU

- 6.1.4. FPGA

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Consumer Electronics

- 6.2.2. Enterprise - Computer and Servers

- 6.2.3. Automotive

- 6.2.4. Industrial

- 6.2.5. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Server Microprocessor Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. APU

- 7.1.2. CPU

- 7.1.3. GPU

- 7.1.4. FPGA

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Consumer Electronics

- 7.2.2. Enterprise - Computer and Servers

- 7.2.3. Automotive

- 7.2.4. Industrial

- 7.2.5. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Server Microprocessor Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. APU

- 8.1.2. CPU

- 8.1.3. GPU

- 8.1.4. FPGA

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Consumer Electronics

- 8.2.2. Enterprise - Computer and Servers

- 8.2.3. Automotive

- 8.2.4. Industrial

- 8.2.5. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Server Microprocessor Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. APU

- 9.1.2. CPU

- 9.1.3. GPU

- 9.1.4. FPGA

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Consumer Electronics

- 9.2.2. Enterprise - Computer and Servers

- 9.2.3. Automotive

- 9.2.4. Industrial

- 9.2.5. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Server Microprocessor Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. APU

- 10.1.2. CPU

- 10.1.3. GPU

- 10.1.4. FPGA

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Consumer Electronics

- 10.2.2. Enterprise - Computer and Servers

- 10.2.3. Automotive

- 10.2.4. Industrial

- 10.2.5. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Server Microprocessor Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. APU

- 11.1.2. CPU

- 11.1.3. GPU

- 11.1.4. FPGA

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Consumer Electronics

- 11.2.2. Enterprise - Computer and Servers

- 11.2.3. Automotive

- 11.2.4. Industrial

- 11.2.5. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Micron Technology

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Broadcom Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Advanced Micro Devices Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Sony Corporation*List Not Exhaustive

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Qualcomm Technologies

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 SK Hynix Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Samsung Technologies

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Nvidia Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Taiwan Semiconductor Manufacturing Company Limited

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Intel Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Micron Technology

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Server Microprocessor Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Server Microprocessor Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Server Microprocessor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Server Microprocessor Industry Revenue (billion), by Application 2025 & 2033

- Figure 5: North America Server Microprocessor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Server Microprocessor Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Server Microprocessor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Server Microprocessor Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: Europe Server Microprocessor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Server Microprocessor Industry Revenue (billion), by Application 2025 & 2033

- Figure 11: Europe Server Microprocessor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Server Microprocessor Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Server Microprocessor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Server Microprocessor Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Asia Pacific Server Microprocessor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Server Microprocessor Industry Revenue (billion), by Application 2025 & 2033

- Figure 17: Asia Pacific Server Microprocessor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Asia Pacific Server Microprocessor Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Server Microprocessor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Server Microprocessor Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Latin America Server Microprocessor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Latin America Server Microprocessor Industry Revenue (billion), by Application 2025 & 2033

- Figure 23: Latin America Server Microprocessor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Latin America Server Microprocessor Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America Server Microprocessor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Server Microprocessor Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Middle East and Africa Server Microprocessor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Server Microprocessor Industry Revenue (billion), by Application 2025 & 2033

- Figure 29: Middle East and Africa Server Microprocessor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa Server Microprocessor Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Server Microprocessor Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Server Microprocessor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Server Microprocessor Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global Server Microprocessor Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Server Microprocessor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Server Microprocessor Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global Server Microprocessor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Server Microprocessor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global Server Microprocessor Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 9: Global Server Microprocessor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Server Microprocessor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Server Microprocessor Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 12: Global Server Microprocessor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Server Microprocessor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Global Server Microprocessor Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Global Server Microprocessor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Server Microprocessor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global Server Microprocessor Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 18: Global Server Microprocessor Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Server Microprocessor Industry?

The projected CAGR is approximately 8.2%.

2. Which companies are prominent players in the Server Microprocessor Industry?

Key companies in the market include Micron Technology, Broadcom Inc, Advanced Micro Devices Inc, Sony Corporation*List Not Exhaustive, Qualcomm Technologies, SK Hynix Inc, Samsung Technologies, Nvidia Corporation, Taiwan Semiconductor Manufacturing Company Limited, Intel Corporation.

3. What are the main segments of the Server Microprocessor Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 118.3 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in Demand for High-performance and Energy-efficient Processors.

6. What are the notable trends driving market growth?

Consumer electronics Segment is Expected to Drive the Market Demand.

7. Are there any restraints impacting market growth?

Decrease in Demand for PCs.

8. Can you provide examples of recent developments in the market?

November 2022 : KIOXIA America, Inc. announced its collaboration with Ampere to qualify its CD6, CM6, and XD6 Series SSDs with platforms based on Ampere's Altra and Ampere Altra Max Cloud Native Processors. To address the demands of the modern cloud, Ampere has designed a server microprocessor architecture from the ground up. Its AArch64-based processors deliver performance, scalability, security, and power efficiency uniquely focused on today's hyperscale cloud and edge computing.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Server Microprocessor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Server Microprocessor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Server Microprocessor Industry?

To stay informed about further developments, trends, and reports in the Server Microprocessor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence