Key Insights

The Australian retail sector is poised for significant expansion, projected to grow at a Compound Annual Growth Rate (CAGR) of 3.1% from a base year of 2025. The market is estimated to reach 551.11 billion by the end of the forecast period. Key growth drivers include rising disposable incomes, a rapidly expanding e-commerce landscape, and a growing consumer preference for experiential retail. The widespread adoption of omnichannel strategies, integrating online and offline customer journeys, further fuels market momentum. However, market growth faces headwinds from economic uncertainty impacting consumer confidence, intense competition from established and emerging players, and escalating operational costs, including wages and supply chain challenges. The industry is segmented across food & grocery, general merchandise, electronics, and online marketplaces, featuring prominent players such as Coles Group, Woolworths Group Ltd, Aldi Group, Kmart Australia Ltd, Myer Group Pty Ltd, David Jones Properties Pty Ltd, JB Hi-Fi Ltd, and Kogan.com Ltd, necessitating continuous innovation and adaptation.

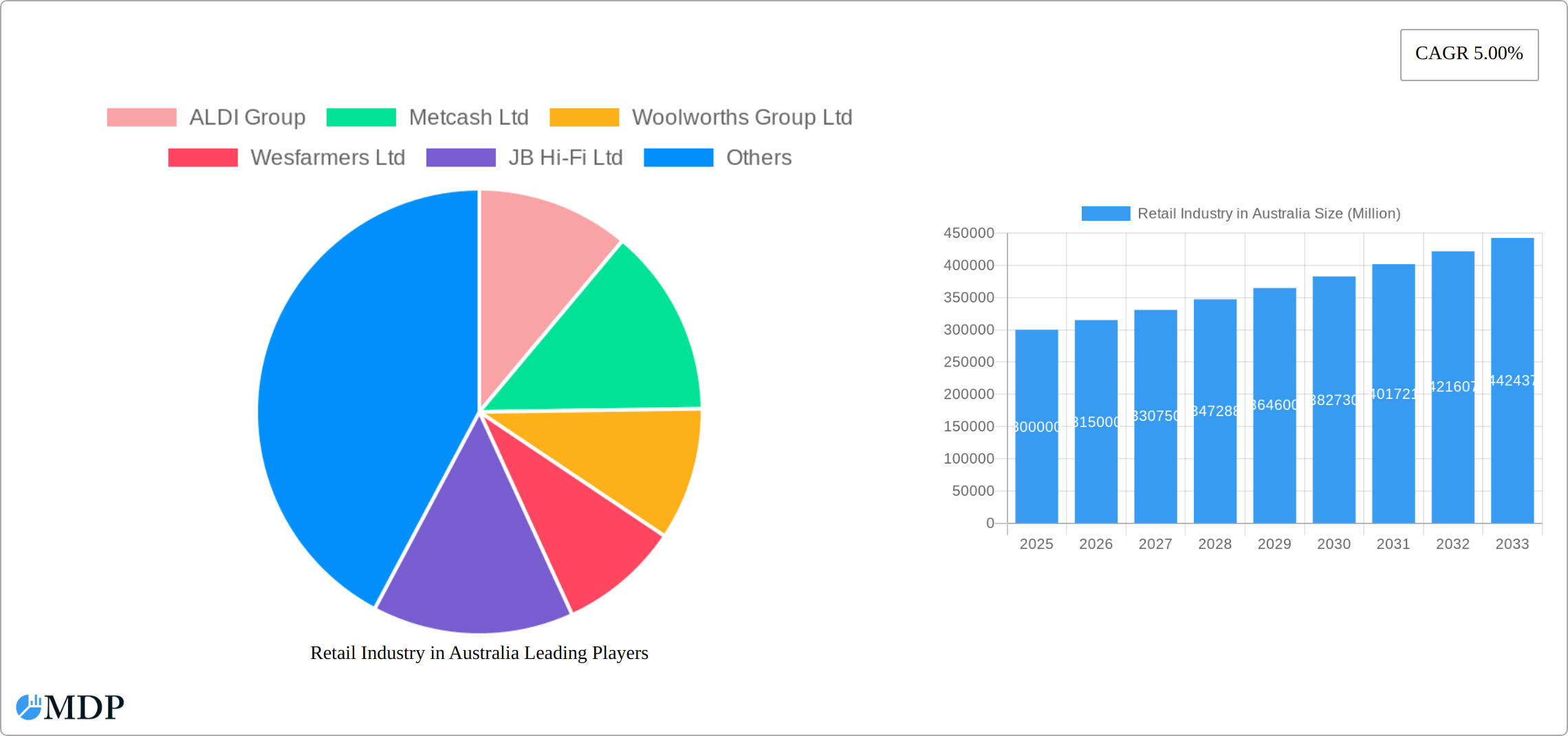

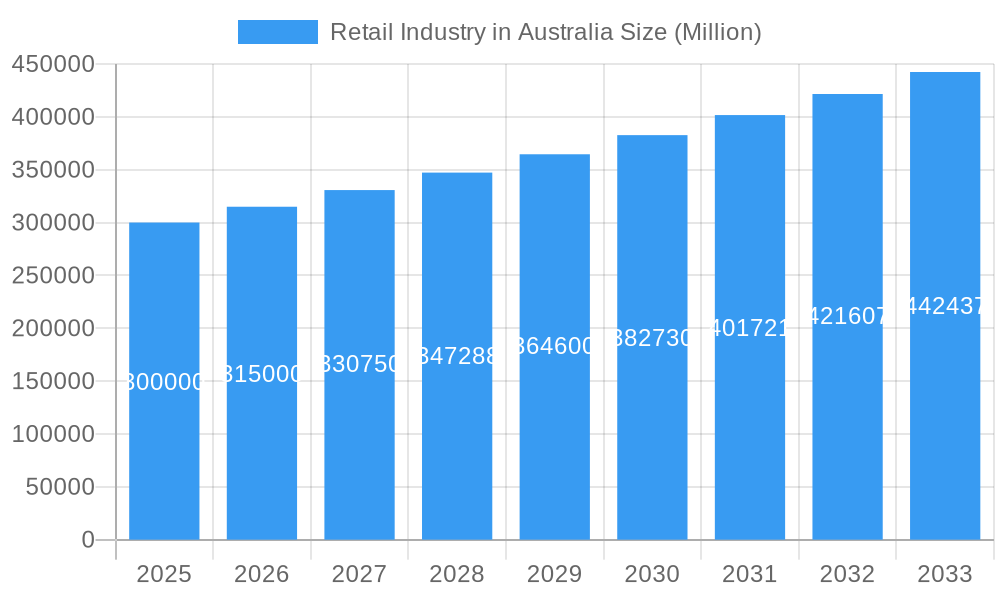

Retail Industry in Australia Market Size (In Billion)

Strategic partnerships, mergers, and acquisitions are expected to become increasingly vital. Retailers will prioritize supply chain optimization, enhanced customer experiences through personalization and loyalty programs, and sustainable sourcing to attract environmentally conscious consumers. Data analytics will be crucial for understanding consumer behavior and refining marketing and inventory management. The future of Australian retail hinges on embracing technology, responding to evolving consumer demands, and navigating a competitive market. The presence of diverse established and emerging competitors indicates a dynamic landscape offering both opportunities and challenges.

Retail Industry in Australia Company Market Share

Australian Retail Market Analysis: Size, Growth, and Forecast (2019-2033)

This comprehensive report offers in-depth analysis of Australia's retail market from 2019 to 2033, with a base year of 2025. Discover key trends, challenges, and opportunities within this expansive market. The study includes insights from leading companies such as ALDI Group, Metcash Ltd, Woolworths Group Ltd, Wesfarmers Ltd, JB Hi-Fi Ltd, Coles Group, Kmart Australia Ltd, Myer Group Pty Ltd, David Jones Properties Pty Ltd, and Kogan.com Ltd. Gain a competitive advantage by downloading this report.

Retail Industry in Australia Market Dynamics & Concentration

Australia's retail sector is characterized by a dynamic and evolving market structure, with a blend of dominance by major players and increasing competition from agile newcomers. While a few large groups, notably Woolworths Group Ltd and Coles Group, collectively command a substantial market share exceeding xx%, their dominance is continuously being challenged. This concentration influences pricing strategies, drives innovation in supply chains and customer service, and shapes the overall competitive landscape. The industry operates within a robust regulatory framework, encompassing stringent consumer protection laws like the Australian Consumer Law and comprehensive competition regulations under the Competition and Consumer Act, all designed to foster a fair and equitable marketplace. A significant and accelerating trend is the surge in online shopping, compelling traditional retailers to invest heavily in sophisticated e-commerce logistics and seamlessly integrated omnichannel strategies. The market is also experiencing consistent mergers and acquisitions (M&A) activity, with an average of xx M&A deals annually observed during the historical period (2019-2024). This ongoing consolidation is often driven by the pursuit of economies of scale, the need to acquire new capabilities, and strategic expansion into emerging or adjacent market segments. Furthermore, the rise of formidable substitutes, including global online marketplaces and increasingly sophisticated direct-to-consumer (DTC) brands, presents ongoing adaptation challenges and opportunities for traditional retailers, encouraging diversification and a focus on unique value propositions. A pivotal shift in consumer sentiment is also evident, with a growing demand for sustainable and ethically sourced products, placing a premium on transparency and responsible business practices across the entire retail value chain.

- Market Share Dominance: Woolworths & Coles combined hold approximately xx% of the market.

- M&A Activity (2019-2024): An average of xx merger and acquisition deals were completed annually, signaling ongoing industry consolidation.

- Key Regulatory Frameworks: The industry is governed by the Australian Consumer Law and the Competition and Consumer Act, ensuring fair market practices and consumer rights.

Retail Industry in Australia Industry Trends & Analysis

The Australian retail industry has demonstrated robust growth, achieving a Compound Annual Growth Rate (CAGR) of xx% during the historical period spanning from 2019 to 2024. Projections indicate a continued upward trajectory, with a forecasted CAGR of xx% expected for the forecast period from 2025 to 2033, albeit at a more moderated pace. This sustained growth is underpinned by several powerful economic and societal drivers. Firstly, a steadily increasing population combined with rising disposable incomes directly translates into higher consumer spending power. Secondly, the retail landscape is being fundamentally reshaped by pervasive technological advancements. The explosive growth of e-commerce, coupled with the widespread adoption of mobile shopping, has created new avenues for sales and customer engagement. Consumer preferences are actively evolving, with a strong emphasis on convenience, the desire for highly personalized shopping experiences, and a persistent demand for demonstrable value for money. The competitive arena is characterized by intense dynamism, where established retail giants and agile emerging online players are locked in a constant struggle for market share. The market penetration of online retail has been steadily increasing, reaching xx% in 2024 and is projected to further climb to xx% by 2033. These profound shifts necessitate that retailers continuously innovate and adapt their strategies to effectively meet the evolving demands of consumers and maintain a decisive competitive edge in this rapidly transforming market.

Leading Markets & Segments in Retail Industry in Australia

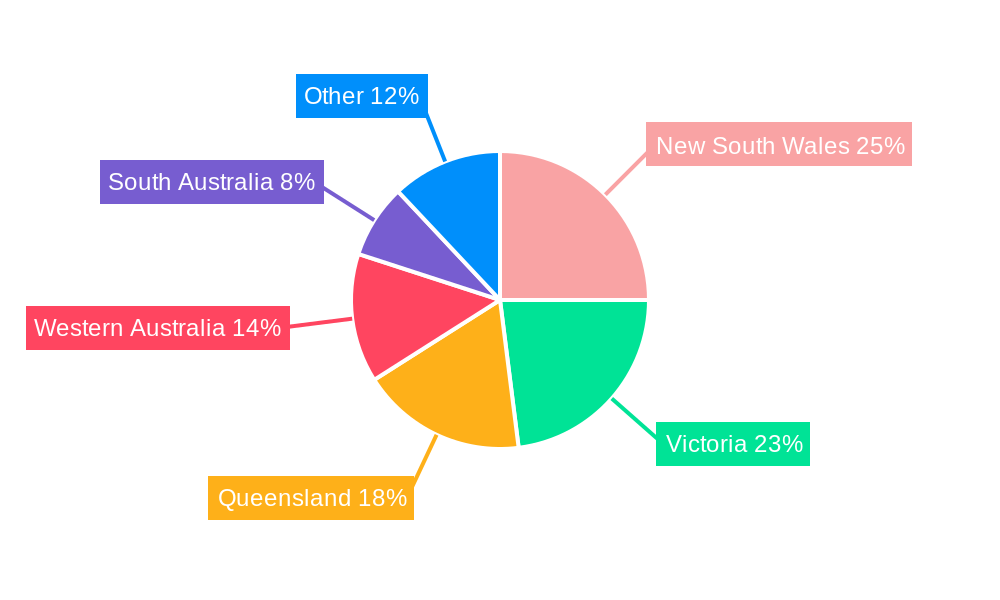

The Australian retail market is geographically diverse, with significant variations in consumer behavior and market dynamics across different regions. While a single dominant region isn't easily identified, major metropolitan areas like Sydney and Melbourne are consistently high-performing, driven by high population density, robust infrastructure, and strong consumer spending. The food retail segment accounts for the largest market share, followed by apparel and general merchandise.

- Key Drivers of Metropolitan Area Dominance:

- High Population Density

- Robust Infrastructure (Transportation & Logistics)

- Higher Disposable Incomes

- Strong Consumer Spending

- Well-established supply chains

The dominance of these regions is attributed to robust infrastructure, higher disposable income levels, and a significant concentration of population. However, growth in regional areas is also notable, driven by government initiatives to improve infrastructure and attract investment. The segment-wise dominance of food and grocery highlights the importance of affordability and convenience in the Australian consumer market.

Retail Industry in Australia Product Developments

Recent product and service innovations within the Australian retail sector are significantly focused on elevating the customer experience, promoting sustainability, and embedding cutting-edge technology. This includes the sophisticated deployment of AI-powered personalized recommendation engines, the creation of seamless and intuitive omnichannel shopping journeys that bridge online and offline interactions, and the pioneering integration of augmented reality (AR) and virtual reality (VR) technologies to enable immersive product visualization. Retailers are placing an increasing emphasis on responsible sourcing practices and the adoption of eco-friendly packaging solutions to resonate with a growing segment of environmentally conscious consumers. Furthermore, the strategic integration of advanced technologies such as AI for optimized inventory management and data-driven personalized marketing campaigns is driving enhanced operational efficiency and fostering deeper customer engagement. These multifaceted innovations are strategically aimed at not only improving overall customer satisfaction but also at bolstering operational efficiencies and securing a sustained competitive advantage in an ever-evolving retail ecosystem.

Key Drivers of Retail Industry in Australia Growth

The sustained and robust growth of the Australian retail industry is propelled by a confluence of significant factors. Foremost among these is the nation's stable economic environment and the consistent rise in disposable incomes, which directly stimulate consumer expenditure. Technological advancements, particularly the transformative impact of e-commerce and the strategic implementation of omnichannel approaches, are instrumental in expanding market reach and significantly enhancing customer engagement capabilities. Supportive government initiatives, including strategic investments in infrastructure development and the enactment of favorable policies, are crucial in cultivating an environment conducive to retail expansion. Moreover, the widespread adoption of convenient and secure digital payment methods is playing a pivotal role in streamlining transaction processes and ultimately driving higher sales conversion rates.

Challenges in the Retail Industry in Australia Market

The Australian retail sector faces several challenges. Increasing competition from both domestic and international players puts pressure on margins and necessitates cost-optimization strategies. Supply chain disruptions, exacerbated by global events, lead to stock shortages and increased costs. Evolving consumer preferences towards sustainability and ethical sourcing demand greater transparency and adaptation from retailers. Furthermore, stringent regulatory environments can impose significant compliance costs. These challenges significantly impact profitability and require innovative solutions for effective mitigation.

Emerging Opportunities in Retail Industry in Australia

The trajectory of long-term growth within Australia's retail sector is intrinsically linked to the strategic embrace of key opportunities. These include forging innovative strategic partnerships, committing to continuous technological advancement, and exploring astute market expansion. The sophisticated integration of Artificial Intelligence (AI) and big data analytics offers unparalleled potential for delivering hyper-personalized customer experiences and optimizing operational workflows. Strategic collaborations with leading technology firms can significantly enhance e-commerce capabilities and deepen customer engagement. Furthermore, venturing into underserved or niche market segments presents substantial growth potential and the opportunity to capture new customer bases. Embracing and championing sustainable business practices, coupled with the diligent cultivation of strong, reputable brand identities, will increasingly attract and retain environmentally conscious consumers, solidifying future market success.

Leading Players in the Retail Industry in Australia Sector

- ALDI Group

- Metcash Ltd

- Woolworths Group Ltd

- Wesfarmers Ltd

- JB Hi-Fi Ltd

- Coles Group

- Kmart Australia Ltd

- Myer Group Pty Ltd

- David Jones Properties Pty Ltd

- Kogan.com Ltd

Key Milestones in Retail Industry in Australia Industry

- November 2020: Wesfarmers expands Kmart's presence with new stores in Victoria and Western Australia, converting existing Target locations. This demonstrates aggressive expansion strategies within the group.

Strategic Outlook for Retail Industry in Australia Market

The Australian retail industry presents substantial growth potential driven by technological advancements, evolving consumer preferences, and a robust economy. Embracing omnichannel strategies, personalized marketing, and sustainable business practices will become crucial for success. Strategic partnerships and investments in technology will be key differentiators. The industry's future trajectory will depend on adapting to the dynamic market landscape and focusing on customer-centric innovation to navigate the competition and capture emerging opportunities.

Retail Industry in Australia Segmentation

-

1. Product

- 1.1. Food and Beverages

- 1.2. Personal and Household Care

- 1.3. Apparel, Footwear, and Accessories

- 1.4. Furniture, Toys, and Hobby

- 1.5. Electronic and Household Appliances

- 1.6. Other Products

-

2. Distribution Channel

- 2.1. Supermar

- 2.2. Specialty Stores

- 2.3. Online

- 2.4. Other Distribution Channels

Retail Industry in Australia Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Retail Industry in Australia Regional Market Share

Geographic Coverage of Retail Industry in Australia

Retail Industry in Australia REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Food and Beverages

- 5.1.2. Personal and Household Care

- 5.1.3. Apparel, Footwear, and Accessories

- 5.1.4. Furniture, Toys, and Hobby

- 5.1.5. Electronic and Household Appliances

- 5.1.6. Other Products

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Supermar

- 5.2.2. Specialty Stores

- 5.2.3. Online

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global Retail Industry in Australia Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Food and Beverages

- 6.1.2. Personal and Household Care

- 6.1.3. Apparel, Footwear, and Accessories

- 6.1.4. Furniture, Toys, and Hobby

- 6.1.5. Electronic and Household Appliances

- 6.1.6. Other Products

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Supermar

- 6.2.2. Specialty Stores

- 6.2.3. Online

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. North America Retail Industry in Australia Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Food and Beverages

- 7.1.2. Personal and Household Care

- 7.1.3. Apparel, Footwear, and Accessories

- 7.1.4. Furniture, Toys, and Hobby

- 7.1.5. Electronic and Household Appliances

- 7.1.6. Other Products

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Supermar

- 7.2.2. Specialty Stores

- 7.2.3. Online

- 7.2.4. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. South America Retail Industry in Australia Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Food and Beverages

- 8.1.2. Personal and Household Care

- 8.1.3. Apparel, Footwear, and Accessories

- 8.1.4. Furniture, Toys, and Hobby

- 8.1.5. Electronic and Household Appliances

- 8.1.6. Other Products

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Supermar

- 8.2.2. Specialty Stores

- 8.2.3. Online

- 8.2.4. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Europe Retail Industry in Australia Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Food and Beverages

- 9.1.2. Personal and Household Care

- 9.1.3. Apparel, Footwear, and Accessories

- 9.1.4. Furniture, Toys, and Hobby

- 9.1.5. Electronic and Household Appliances

- 9.1.6. Other Products

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Supermar

- 9.2.2. Specialty Stores

- 9.2.3. Online

- 9.2.4. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East & Africa Retail Industry in Australia Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Food and Beverages

- 10.1.2. Personal and Household Care

- 10.1.3. Apparel, Footwear, and Accessories

- 10.1.4. Furniture, Toys, and Hobby

- 10.1.5. Electronic and Household Appliances

- 10.1.6. Other Products

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Supermar

- 10.2.2. Specialty Stores

- 10.2.3. Online

- 10.2.4. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. Asia Pacific Retail Industry in Australia Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Food and Beverages

- 11.1.2. Personal and Household Care

- 11.1.3. Apparel, Footwear, and Accessories

- 11.1.4. Furniture, Toys, and Hobby

- 11.1.5. Electronic and Household Appliances

- 11.1.6. Other Products

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Supermar

- 11.2.2. Specialty Stores

- 11.2.3. Online

- 11.2.4. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ALDI Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Metcash Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Woolworths Group Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Wesfarmers Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 JB Hi-Fi Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Coles Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Kmart Australia Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Myer Group Pty Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 David Jones Properties Pty Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Kogan com Ltd**List Not Exhaustive

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 ALDI Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Retail Industry in Australia Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Retail Industry in Australia Revenue (billion), by Product 2025 & 2033

- Figure 3: North America Retail Industry in Australia Revenue Share (%), by Product 2025 & 2033

- Figure 4: North America Retail Industry in Australia Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 5: North America Retail Industry in Australia Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 6: North America Retail Industry in Australia Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Retail Industry in Australia Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Retail Industry in Australia Revenue (billion), by Product 2025 & 2033

- Figure 9: South America Retail Industry in Australia Revenue Share (%), by Product 2025 & 2033

- Figure 10: South America Retail Industry in Australia Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 11: South America Retail Industry in Australia Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 12: South America Retail Industry in Australia Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Retail Industry in Australia Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Retail Industry in Australia Revenue (billion), by Product 2025 & 2033

- Figure 15: Europe Retail Industry in Australia Revenue Share (%), by Product 2025 & 2033

- Figure 16: Europe Retail Industry in Australia Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 17: Europe Retail Industry in Australia Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 18: Europe Retail Industry in Australia Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Retail Industry in Australia Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Retail Industry in Australia Revenue (billion), by Product 2025 & 2033

- Figure 21: Middle East & Africa Retail Industry in Australia Revenue Share (%), by Product 2025 & 2033

- Figure 22: Middle East & Africa Retail Industry in Australia Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 23: Middle East & Africa Retail Industry in Australia Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 24: Middle East & Africa Retail Industry in Australia Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Retail Industry in Australia Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Retail Industry in Australia Revenue (billion), by Product 2025 & 2033

- Figure 27: Asia Pacific Retail Industry in Australia Revenue Share (%), by Product 2025 & 2033

- Figure 28: Asia Pacific Retail Industry in Australia Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 29: Asia Pacific Retail Industry in Australia Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Asia Pacific Retail Industry in Australia Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Retail Industry in Australia Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Retail Industry in Australia Revenue billion Forecast, by Product 2020 & 2033

- Table 2: Global Retail Industry in Australia Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Global Retail Industry in Australia Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Retail Industry in Australia Revenue billion Forecast, by Product 2020 & 2033

- Table 5: Global Retail Industry in Australia Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global Retail Industry in Australia Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Retail Industry in Australia Revenue billion Forecast, by Product 2020 & 2033

- Table 11: Global Retail Industry in Australia Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 12: Global Retail Industry in Australia Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Retail Industry in Australia Revenue billion Forecast, by Product 2020 & 2033

- Table 17: Global Retail Industry in Australia Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 18: Global Retail Industry in Australia Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Retail Industry in Australia Revenue billion Forecast, by Product 2020 & 2033

- Table 29: Global Retail Industry in Australia Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 30: Global Retail Industry in Australia Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Retail Industry in Australia Revenue billion Forecast, by Product 2020 & 2033

- Table 38: Global Retail Industry in Australia Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 39: Global Retail Industry in Australia Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Retail Industry in Australia Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Retail Industry in Australia?

The projected CAGR is approximately 3.1%.

2. Which companies are prominent players in the Retail Industry in Australia?

Key companies in the market include ALDI Group, Metcash Ltd, Woolworths Group Ltd, Wesfarmers Ltd, JB Hi-Fi Ltd, Coles Group, Kmart Australia Ltd, Myer Group Pty Ltd, David Jones Properties Pty Ltd, Kogan com Ltd**List Not Exhaustive.

3. What are the main segments of the Retail Industry in Australia?

The market segments include Product, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 551.11 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Demand for Food and Beverages Continues to be Strong Despite the COVID-19 Challenges.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

In November 2020, Wesfarmers retail businesses continued to expand their business. Kmart opened new stores in Camberwell and Casey in Victoria and Cockburn in Western Australia, all converted from Target stores, alongside its newest K Hub store in Bairnsdale in regional Victoria.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Retail Industry in Australia," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Retail Industry in Australia report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Retail Industry in Australia?

To stay informed about further developments, trends, and reports in the Retail Industry in Australia, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence